8-14 Opening Update: Grains Slide Following Yesterday’s Gains

We are excited to offer you a new way to follow the markets! While CME Group policy changes mean our daily updates will no longer show pricing data, you can now explore our interactive quote board, featuring up-to-date charts to help you track market trends.

Grain Market Insider Interactive Quote Board

- Corn futures are lower to start the day erasing yesterday’s gains so far. While a decline in the Dollar index yesterday was supportive, traders are still faced with a huge crop and estimated carryout of over 2 billion bushels.

- Estimates for today’s export sales report see corn sales in a range between 1,150k and 2,800k tons with an average guess of 1,967k. This would compare to 3,334k last week and 921k tons a year ago at this time.

- US ethanol stocks fell by 4.7% to 22.649m bbl which was well below the average analyst estimate of 23.722m. Plant production came in higher at 1.093m barrels per day.

Corn Futures Slump to Start August: After a quiet May–July stretch, corn futures broke support near 391 to start August. A weekly close below this level could shift focus to the August 2024 low near 360, while upside targets include an unfilled gap at 413, resistance at 420, and a second gap at 430.

- Soybeans are trading lower to start the day following three days of very sharp gains that were fueled by a surprise reduction in acreage in Tuesday’s WASDE report. Soybean meal is trading higher while soybean oil is lower.

- Estimates for today’s export sales report see soybean sales in a range between 450k and 1,600k tons with an average guess of 950k tons. This would compare to 1,013k last week and 1,481k a year ago at this time.

- In Brazil, soybean production is expected to rise by nearly 1 mmt to 170.5 mmt as a result of better than expected yields. The USDA has not yet increased production estimates for Brazil.

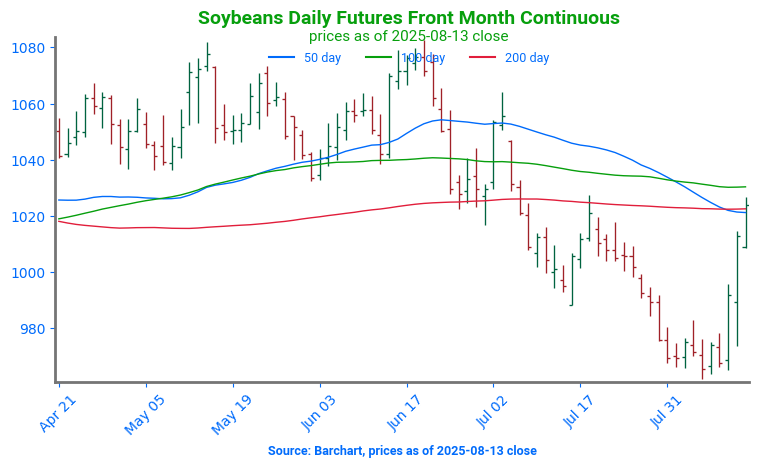

Soybeans Test April Lows: Soybean futures remain locked in a broader sideways trend after failing to clear key resistance at the May high of $10.82 in mid-June. With largely favorable weather throughout much of the growing season, the market has struggled to build bullish momentum, and the path of least resistance has remained lower. Technically, a breakout above the 100-day moving average could open the door to filling the gap left over the July 4th weekend near $10.50. On the downside, initial support is seen around the $10.00 mark, with stronger technical support at the April lows near $9.80.

- Wheat is mixed to start the day with Chicago and KC wheat trading lower along with the rest of the grains while Minneapolis wheat is slightly higher. Despite a relatively friendly USDA report, wheat has struggled near the $5 level with larger Russian and Ukrainian production weighing on prices along with US harvest.

- Estimates for today’s export sales report see wheat sales in a range between 400k and 850k tons with an average guess of 600k tons. This would compare to 738k last week and 273k a year ago at this time.

- In Germany, the 2025 grain output forecast has been raised for both wheat and corn. Total grains are estimated at 43 mmt up from 41.7 mmt last month with wheat at 22.4 mmt compared to 21.6 mmt a month ago. This is due to larger acreage and better yields than expected.

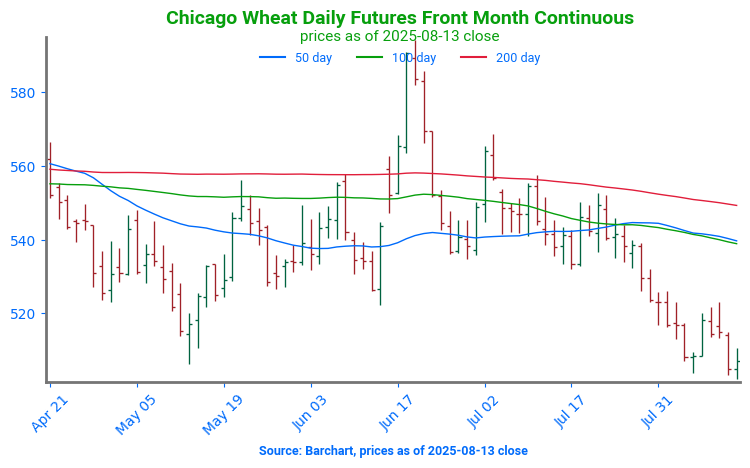

Chicago Wheat Holds Range: Chicago wheat’s sharp rally in mid-June proved short-lived, with futures retreating toward the upper end of their 2025 trading range. Initial support is expected just above the 500 level, which marked the lows back in May and has since acted as a solid floor. On the upside, a weekly close above 558 would be seen as a constructive technical signal and could open the door for a retest of the recent highs near 590.

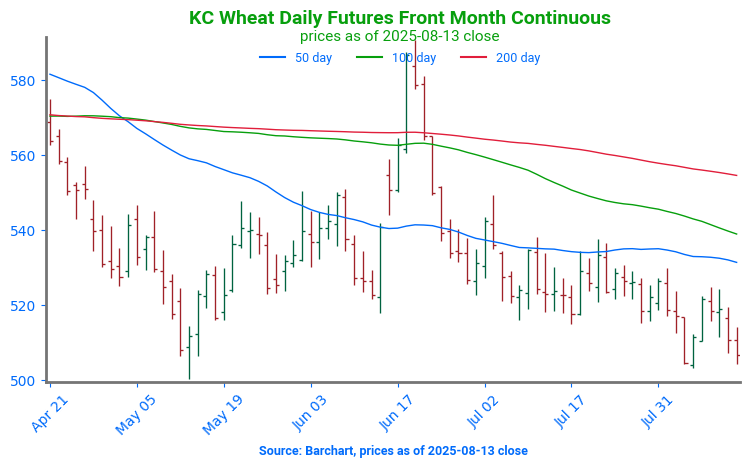

KC Wheat Pulls Back Below Key Averages, Support at June Lows: KC wheat futures saw a strong rally in June, briefly testing the April highs near 580. However, late-month weakness pulled prices back below both the 100 and 200-day moving averages, which now serve as key resistance levels. On the downside, initial support is seen at the June low of 517.75, with secondary support near the May low around 500.

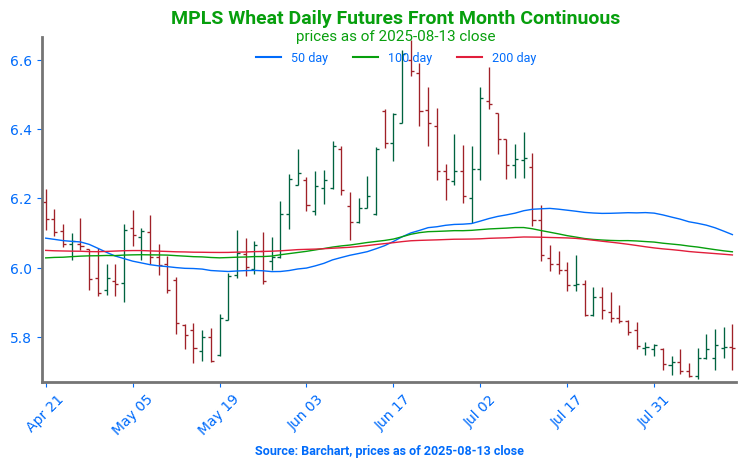

Spring Wheat Futures Test Key Support After July Slide: Spring wheat futures have come under pressure in July, weighed down by improving crop conditions and generally favorable weather across key growing areas. Technically, a cluster of major moving averages just above the 600 mark presents the first layer of upside resistance, with a chart gap near 650 serving as a secondary target if momentum builds. On the downside, the May lows near 580 should provide firm support in the event of further weakness.

Grain Market Insider is provided by Stewart-Peterson Inc., a publishing company.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing by Stewart-Peterson and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Stewart-Peterson Inc. Reproduction of this information without prior written permission is prohibited. Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. The data contained herein is believed to be drawn from reliable sources but cannot be guaranteed. Reproduction and distribution of this information without prior written permission is prohibited. This material has been prepared by a sales or trading employee or agent of Total Farm Marketing and is, or is in the nature of, a solicitation. Any decisions you may make to buy, sell or hold a position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to Total Farm Marketing.

Stewart-Peterson Inc., Stewart-Peterson Group Inc., and SP Risk Services LLC are each part of the family of companies within Total Farm Marketing (TFM). Stewart-Peterson Inc. is a publishing company. Stewart-Peterson Group Inc. is registered with the Commodity Futures Trading Commission (CFTC) as an introducing broker and is a member of National Futures Association. SP Risk Services LLC is an insurance agency. A customer may have relationships with any or all three companies.