7-22 End of Day: Grain Markets Start the Week Off Strong

All prices as of 2:00 pm Central Time

| Corn | ||

| SEP ’24 | 400.25 | 9.75 |

| DEC ’24 | 415 | 10.25 |

| DEC ’25 | 457 | 8.75 |

| Soybeans | ||

| AUG ’24 | 1117.75 | 20.5 |

| NOV ’24 | 1068.75 | 32.75 |

| NOV ’25 | 1083 | 26.75 |

| Chicago Wheat | ||

| SEP ’24 | 548 | 5.25 |

| DEC ’24 | 573 | 5 |

| JUL ’25 | 608.25 | 5 |

| K.C. Wheat | ||

| SEP ’24 | 571.75 | 1.75 |

| DEC ’24 | 588 | 1.25 |

| JUL ’25 | 605 | 2.25 |

| Mpls Wheat | ||

| SEP ’24 | 622.75 | 13 |

| DEC ’24 | 640.25 | 10.75 |

| SEP ’25 | 666.25 | 5.75 |

| S&P 500 | ||

| SEP ’24 | 5613.5 | 59.75 |

| Crude Oil | ||

| SEP ’24 | 78.4 | -0.24 |

| Gold | ||

| OCT ’24 | 2419.5 | -3.5 |

Grain Market Highlights

- Carry over strength from neighboring soybeans triggered a round of short covering to begin the week following Friday’s Commitment of Traders (COT) report that showed managed funds still hold a near record net short position.

- New crop contracts led soybeans higher with support from sharply higher soybean meal and oil. A warmer and drier near-term forecast likely triggered short covering from managed funds, which according to Friday’s COT report, hold a record net short soybean position.

- Following a day of two sided trade, all three wheat classes settled in the green. Support came from potential crop concerns in the dry areas of Canada and the US northern Plains, and quality concerns for the French and German wheat crop.

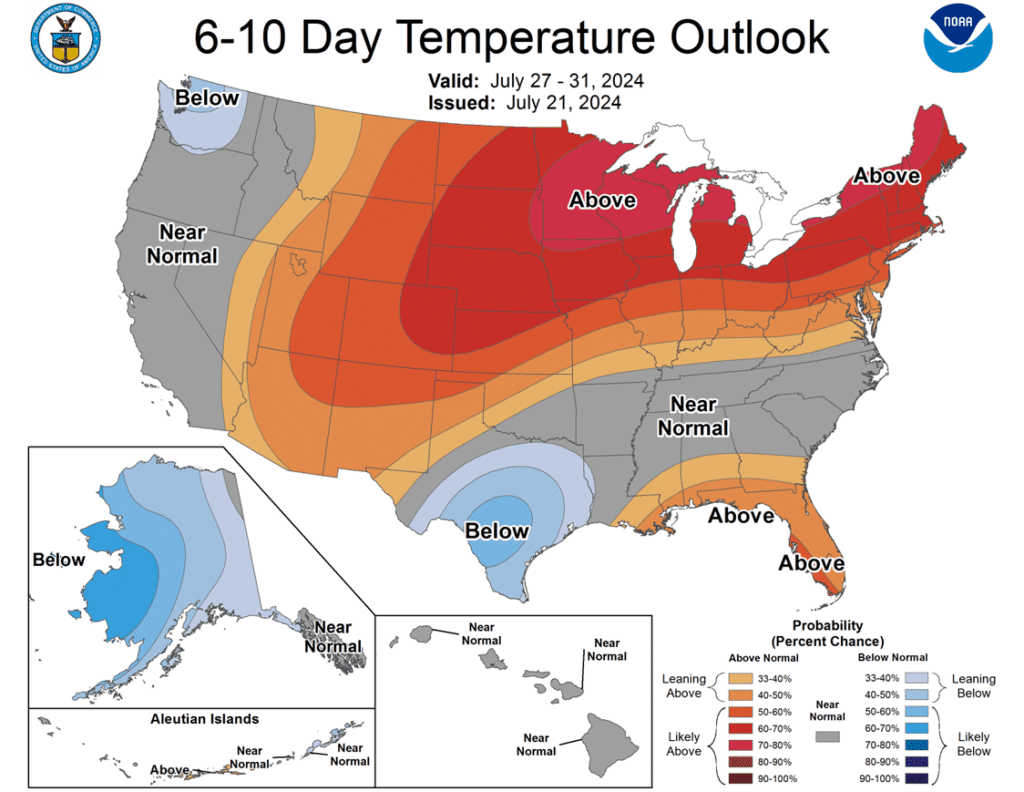

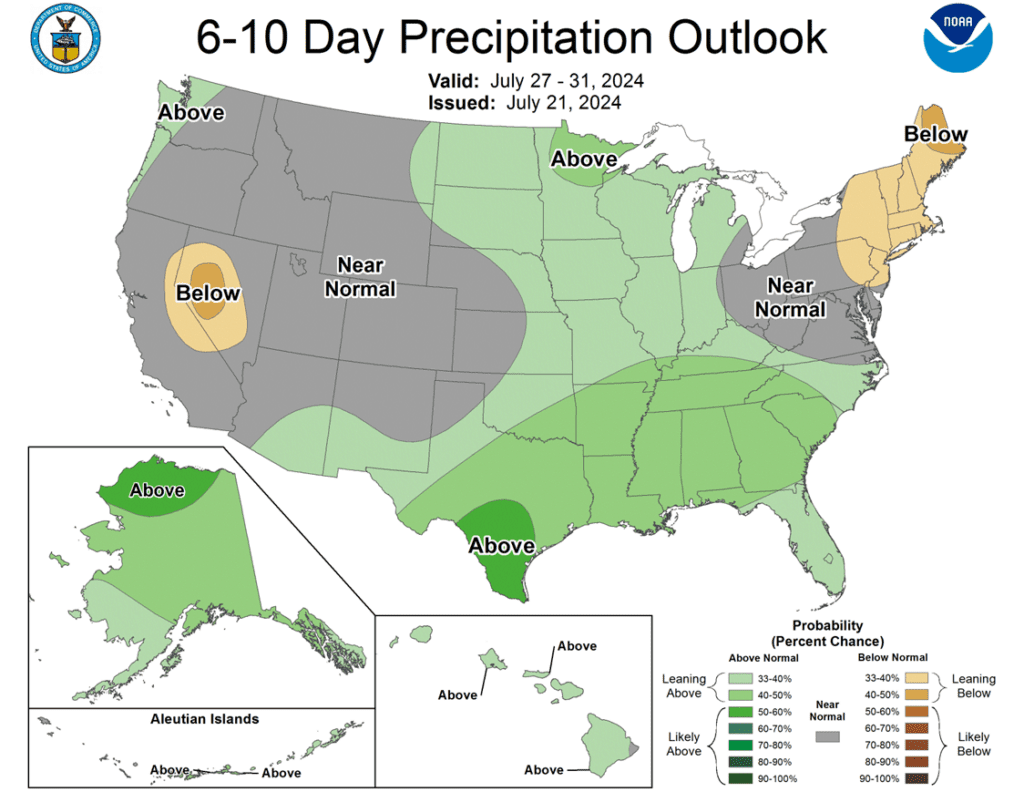

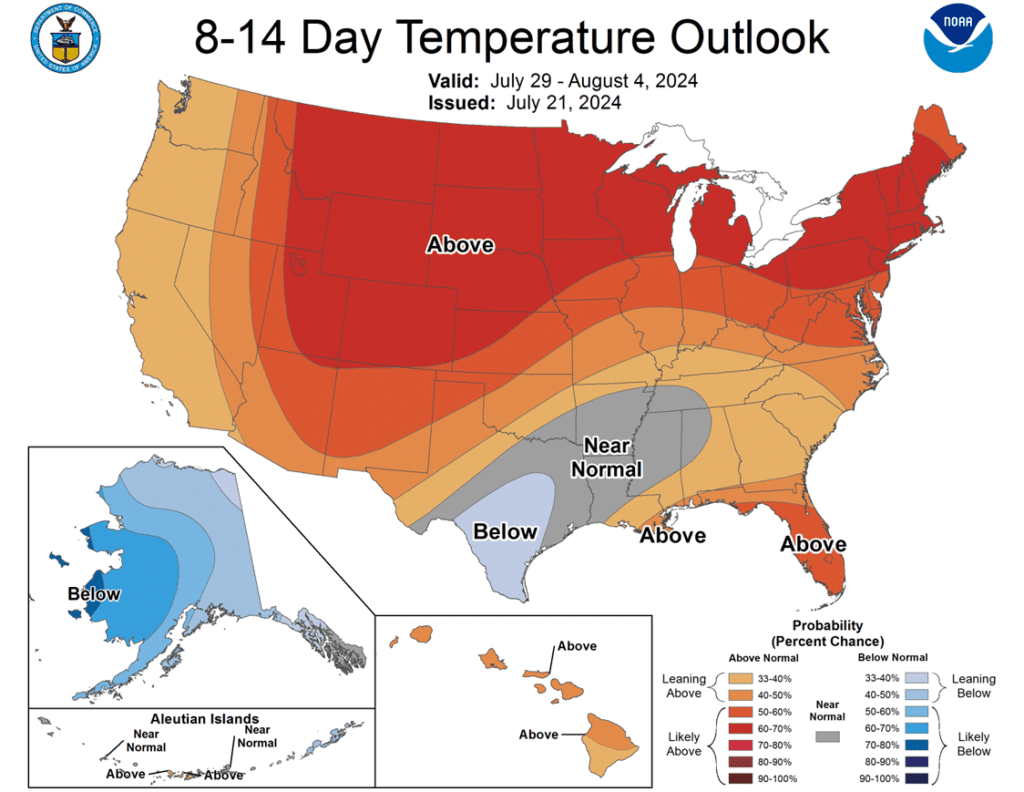

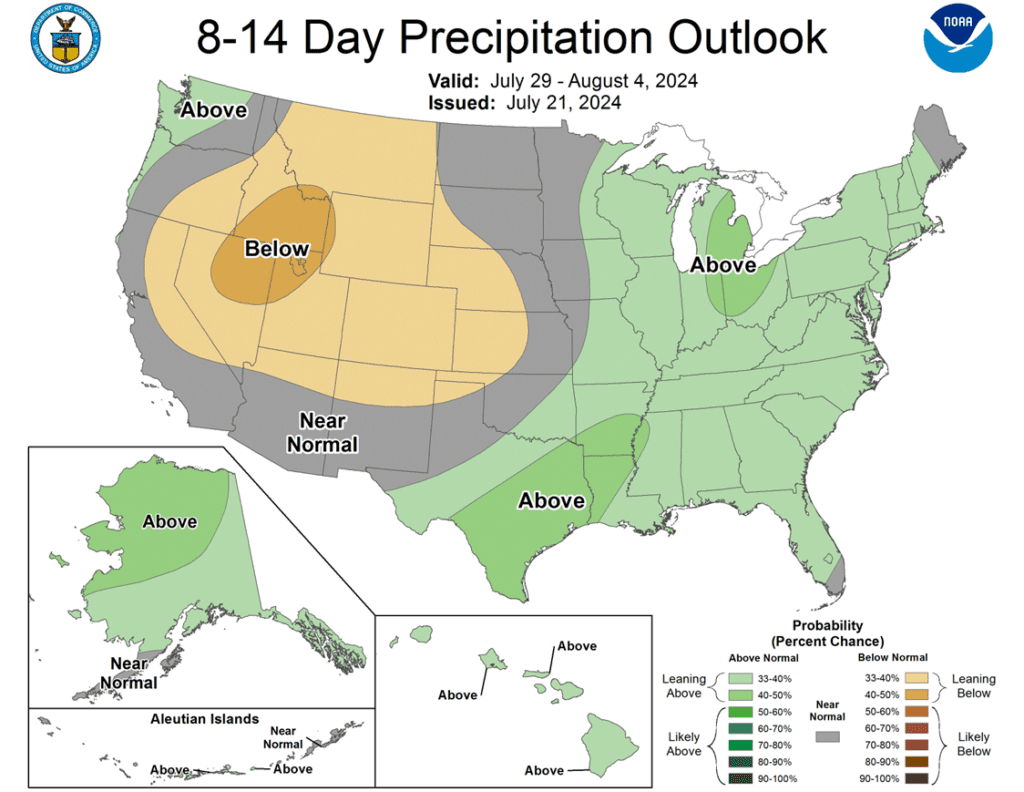

- To see the updated US 5-day precipitation forecast, and 6-10 and 8-14 day Temperature and Precipitation Outlooks, courtesy of NOAA, the Weather Prediction Center, and NDMC scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

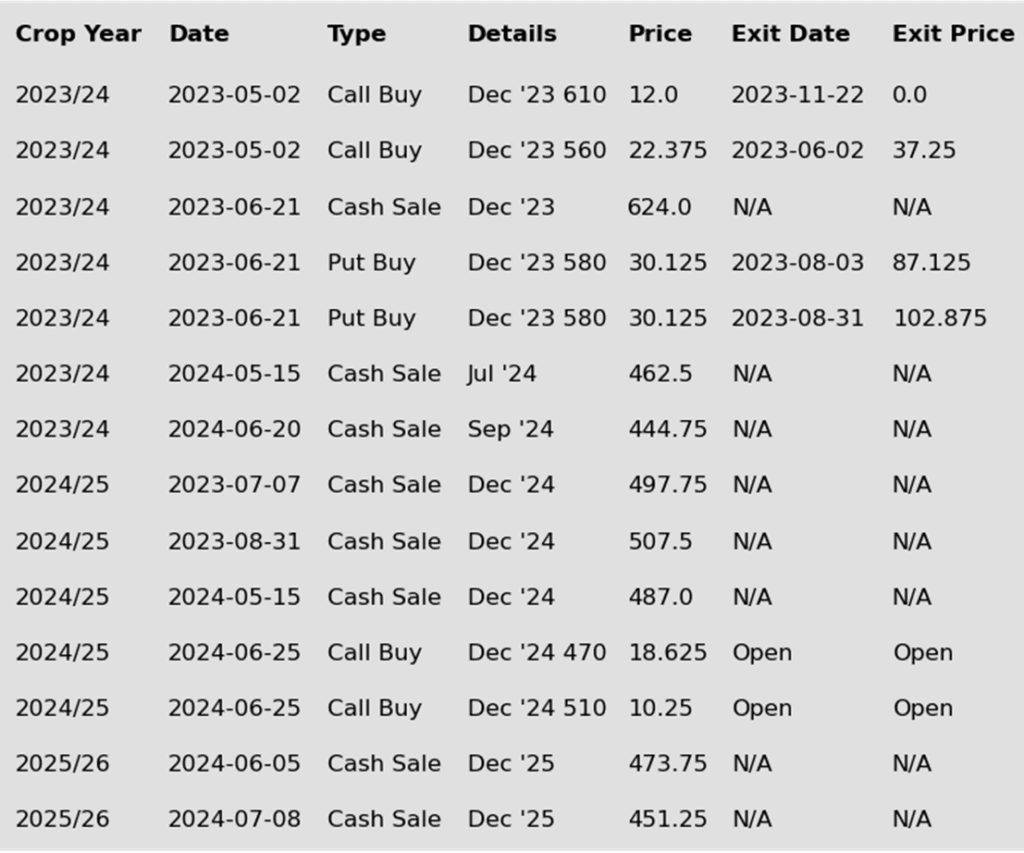

The USDA’s July WASDE report surprised the market by lowering 23/24 corn ending stocks below the low end of expectations resulting in a much lower than expected 24/25 ending stocks projection of 2.097 billion bushels. While this leaves new crop supplies at “adequate” levels, any increase in demand or drop in production could lead to short covering by the funds and higher prices.

- No new action is recommended for 2023 corn. Any remaining old crop 2023 corn should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 corn – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 corn. We recently recommended buying Dec ’24 470 and 510 calls after Dec ’24 closed below 451, for their relative value and because we are at that time of year of high volatility when markets can move swiftly. Moving forward, our current strategy is to target the value of 29 cents to exit the Dec ’24 470 calls. Exiting the 470 calls at 29 cents will allow you to lock in gains in case prices fall back and hold the remaining 510 calls at or near a net neutral cost, which should continue to protect existing sales and give you confidence to make further sales if the market rallies sharply. To take further action, we are targeting the 490 – 510 area to recommend making additional sales versus Dec ’24.

- No new action is currently recommended for 2025 corn. Considering we are at the time of year to get early sales made for next year’s crop, we recently issued our first sales recommendation for the 2025 corn crop. Given that the growing season has potential for high volatility and can provide some of the best pricing opportunities for the next crop year, we will also be watching the calendar along with price action. If our current Plan A upside objective in the 490 – 510 range isn’t met by our Plan B sales deadline of July 23, we will likely make another sales recommendation at that time.

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

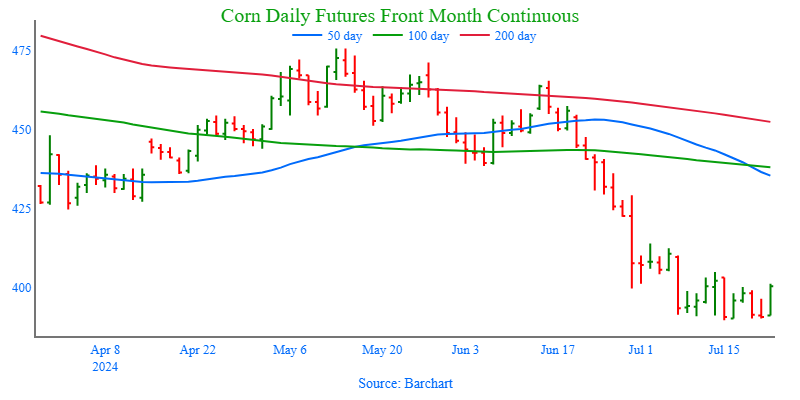

- Strong buying entered the corn market to start the week as spill over strength from the soybean market triggered a short covering rally in an oversold market. Despite the strength, December corn remains in the sideways range of 405 – 415 that it has been trading in since July 8.

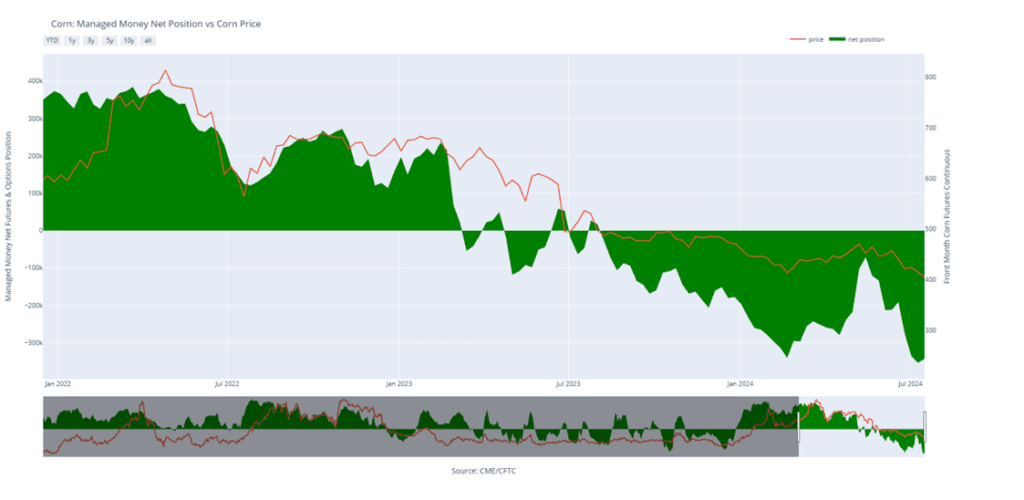

- On Friday’s Commitment of Traders report, managed hedge funds slightly reduced their record net short position in corn. Last week funds were net buyers of 10,587 corn contracts, but still hold a sizeable net short position of 343,396 contracts.

- The USDA will release the next round of crop ratings on Monday afternoon. Expectations are for corn ratings to remain steady to slightly higher over last week’s numbers. Last week, corn was rated 65% good/excellent, which was trending 11% higher than last year.

- The key second crop (safrinha) corn harvest in Brazil is progressing quickly. Brazil Ag analyst, AgRural, stated that 83% of the second crop corn was harvested, up from 74% last week. Last year, only 47% of the crop was harvested in this time window. Brazil’s second crop corn is approximately 75% of their corn production

- Weather forecasts going into the end of July are turning less friendly for crop development going into the first part of August as temperatures are trending warmer than average, and moisture in normal to below normal. While most of the corn crop is in good condition, weather will still play a key role in finishing the crop into harvest.

Above: The corn market continues to consolidate as it corrects from being oversold. If prices break out above the 404 – 415 resistance area, they could run toward 425 – 430. To the downside, a break below 391 could suggest a further decline towards the 362 – 360 area.

Above: Corn Managed Money Funds net position as of Tuesday, July 16. Net position in Green versus price in Red. Managers net bought 10,587 contracts between July 9 – 16, bringing their total position to a net short 343,396 contracts.

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

Active

Sell AUG ’24 Cash

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

Weighed down by sluggish export demand and favorable weather, the soybean market experienced a choppy downward trajectory leading up to the USDA’s July WASDE report. While the USDA lowered old crop ending stocks more than expected, resulting in a larger-than-anticipated drop in new crop carryout projections, the 435 mb projected carryout remains a bearish factor given the current demand picture. With much of the growing season still ahead, the lower anticipated supply leaves less margin for error if growing conditions turn hot and dry. For now, a weather-related issue or a surge in demand appears to be the most likely catalyst to push prices higher.

- Grain Market Insider sees a continued opportunity to sell a portion of your 2023 soybean crop. With no bullish surprises in last week’s WASDE report, and since the market has not provided an opportunity to make a sale at our Plan A target, we are employing our Plan B time stop strategy, considering that we try not to carry old crop bushels past mid-July due to seasonal weakness. Therefore, we are making what will be our last sales recommendation for the 2023 soybean crop at this time.

- No new action is recommended for the 2024 crop. At the end of December, we recommended buying Nov ’24 1280 and 1360 calls due to the amount of uncertainty in the 2024 soybean crop and to give you confidence to make sales and protect those sales in an extended rally. Given that the market has retreated since that time, we are targeting the mid-1100s versus Nov ’24 futures to exit 1/3 of the 1280 calls to help preserve equity. Most recently we employed our Plan B strategy with the close below 1180 in Nov ’24 and recommended making additional sales due to the potential change in trend. With much of the growing season still ahead of us, should the market turn back higher, we are targeting the upper 1100s to low 1200s from our Plan A strategy to potentially make two additional sales recommendations.

- No Action is currently recommended for 2025 Soybeans. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

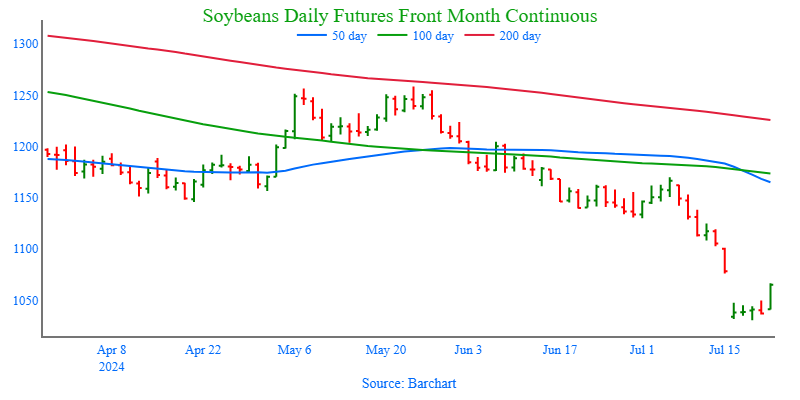

- Soybeans ended the day sharply higher, quickly erasing last week’s losses. While funds hold a record net short position in soybeans, the forecasts predicting short-term dry weather likely triggered today’s short covering rally. Both soybean meal and oil ended the day higher as well.

- Later today, the USDA will release its Crop Progress report and expectations are that good to excellent ratings will increase for soybeans by 1% from last week. The upcoming hot and dry weather could pose a challenge later this week, but conditions have been relatively good so far this season.

- Both soybean meal and oil closed higher today with meal leading the way up, with the strong close in both products adding to already impressive crush margins. These margins have improved significantly which has spurred domestic demand as processors scoop up cheap cash soybeans. This has also propped up nearby soybean prices relative to new crop months.

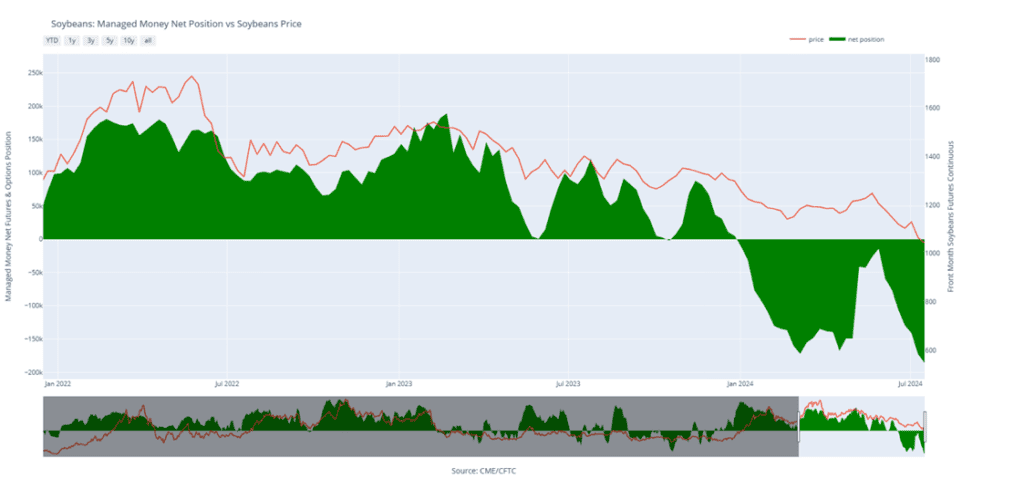

- According to Friday’s CFTC report, funds added to their short position in soybeans as of July 16. They sold 13,145 contracts, increasing their net short position to a record 185,750 contracts.

Above: The large gap on the continuous chart represents the roll from the August soybean contract to the September, where the 50-cent premium in the August contract relative to the September contract is no longer represented. That said, support for the September contract on a break below 1030 may come in near the 1000 psychological level with further support around 985. Overhead, a turnaround toward higher prices may encounter resistance between 1065 – 1075.

Above: Soybean Managed Money Funds net position as of Tuesday, July 16. Net position in Green versus price in Red. Money Managers net sold 13,145 contracts between July 9 – 16, bringing their total position to a net short 185,750 contracts.

Wheat

Market Notes: Wheat

- After a two-sided trade, all three US wheat classes closed higher, led by Minneapolis futures; this was likely a result of spring wheat development concerns from dryness in parts of Canada and the US northern Plains. Corn and soybeans were sharply higher today as well, offering support to wheat. However, this may be more of a technical bounce from oversold conditions, wherein funds are covering some of their short positions. Additional support came from continued talk of quality concerns for the French and German wheat crops.

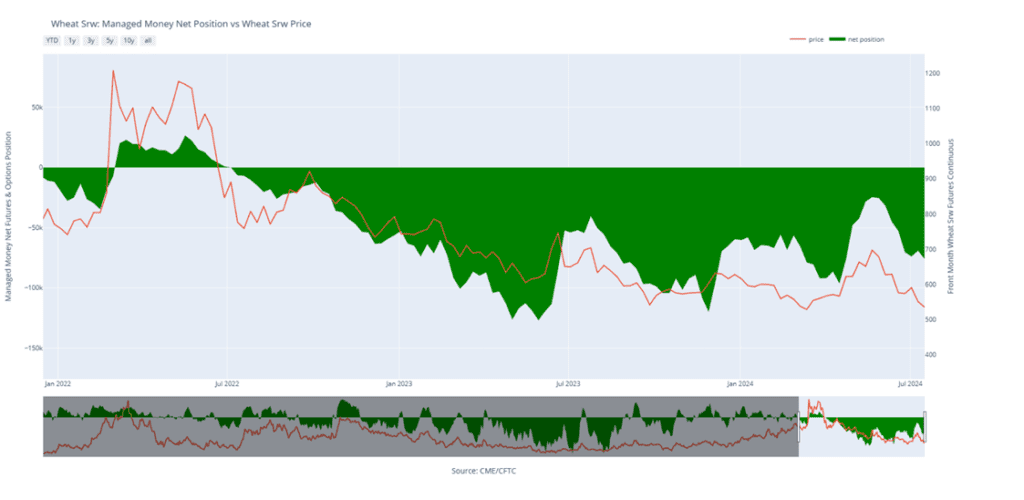

- Friday’s CFTC report indicated that as of July 16, managed funds increased their short position in Chicago wheat to 75,886 contracts from 69,137 contracts the previous week. Additionally, for the same time period, they added to their short position in Kansas City wheat, going from 40,811 to 43,896 contracts. Their total short position in wheat, when you add in Minneapolis futures, is close to 145,000 contracts, their largest wheat short position in three months.

- Weekly wheat inspections of 8.7 mb brought total 24/25 inspections to 95 mb. This is up 20% versus last year, and wheat inspections are running ahead of the pace needed to reach the USDA’s 825 mb 24/25 export projection.

- According to IKAR, Russian wheat export values ended last week at $219 per mt, unchanged from the previous week. Additionally, SovEcon said that Russia shipped 710,000 mt of grain last week, compared with 600,000 mt the week prior. Of that total, 660,000 mt was said to be wheat.

- The Wheat Quality Council kicked off their hard red spring wheat tour today in Fargo, North Dakota. With the ND crop rated at 82% good to excellent as of July 15, they are expected to find good quality wheat. While the majority of the tour is within North Dakota, there will be some travel through northern South Dakota and western Minnesota.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

Active

Exit Half JUL ’25 620 Puts ~ 67c

2026

No New Action

Chicago Wheat Action Plan Summary

Since rallying nearly 200 cents from the March low to the May high, largely on fund short covering from Russian crop concerns and dryness in the southwestern Plains, prices have fallen from their peak with seasonal weakness and a quick harvest pace. Although prices remain weak, the market shows signs of being oversold, which can be supportive in the event prices turn back higher, while the breakout above the December highs suggests there is potential for a test of the 2023 summer highs post-harvest.

- No new action is recommended for 2024 Chicago wheat. Considering the recent rally in wheat, we recommended taking advantage of the elevated prices to make additional sales and buy upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 740 – 760 versus Sept ’24 to recommend further sales and to target a selling price of about 73 cents in the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- Grain Market Insider sees a continued opportunity to sell half of your July ‘25 620 Chicago Wheat puts at approximately 67 cents in premium minus fees and commission. Last month Grain Market Insider recommended buying July ’25 620 Chicago wheat puts for approximately 34 cents in premium plus commission and fees to protect the downside from further potential price erosion. At the time, July Chicago wheat had just broken through support near 706. The breaking of 706 support increased the risk of the market retreating further. Since that time July ’25 Chicago wheat has dropped over 100 cents, with the July ’25 620 Chicago wheat puts having roughly doubled in value. Though prices are depressed following this market drop, plenty of time remains to market the ’25 crop, and plenty of unknowns remain that could rally prices. Grain Market Insider recommends selling half of the previously recommended July ’25 620 Chicago wheat puts to lock in gains in case prices rally back and holding the remaining puts at a net neutral cost, which will continue to protect any unsold bushels if prices erode further.

- No action is currently recommended for 2026 Chicago Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

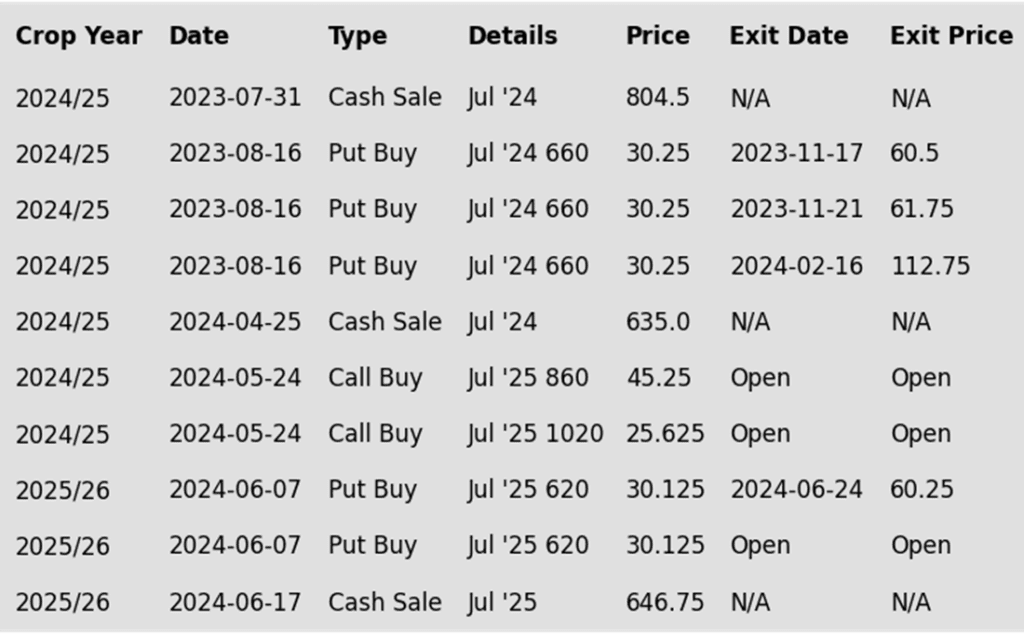

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

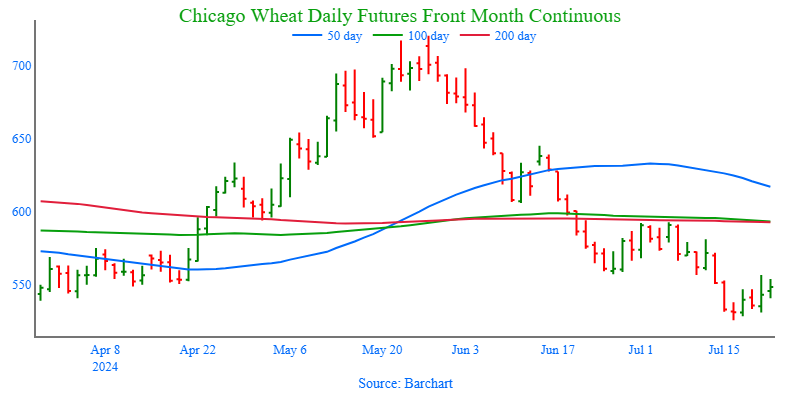

Above: The consolidation of the Chicago wheat market shows support below the market around just above the March 523 ½ low. Should the market continue higher, upside resistance could be found between 555 and 580, with additional resistance between 590 and 600. While a close below 523 ½ could suggest a lower trend towards 500 psychological support, with further support in the 490 – 470 area.

Above: Chicago Wheat Managed Money Funds net position as of Tuesday, July 16. Net position in Green versus price in Red. Money Managers net sold 6,749 contracts between July 9 – 16, bringing their total position to a net short 75,886 contracts.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

KC Wheat Action Plan Summary

Since the end of May the wheat market has been trending lower as concerns regarding Russia’s shrinking wheat crop have waned, and US HRW harvest yields have been higher than expected. During this time managed funds started reestablishing their short positions while the market continues to show signs of being oversold. While harvest pressure and falling Black Sea export prices continue to weigh on US prices, the funds’ short position and oversold conditions could culminate in a short covering rally on any increase in demand as world wheat ending stocks are expected to fall yet again this year.

- No new action is recommended for 2024 KC wheat. Considering the recent upside breakout in KC wheat, we recommended buying upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 725 – 750 versus Sept ’24 to recommend further sales and to target a selling price of about 71 cents on the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is currently recommended for 2025 KC Wheat. We recently recommended exiting half of the previously recommended July ’25 620 puts once they reached 60 cents (double the original approximate cost) to realize gains in case the market rallies back, while still holding the remaining 620 puts at, or near, a net neutral cost for continued downside coverage on any unsold bushels. Looking ahead, our strategy is to target the 680 – 710 range to recommend making additional sales.

- No action is currently recommended for 2026 KC Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

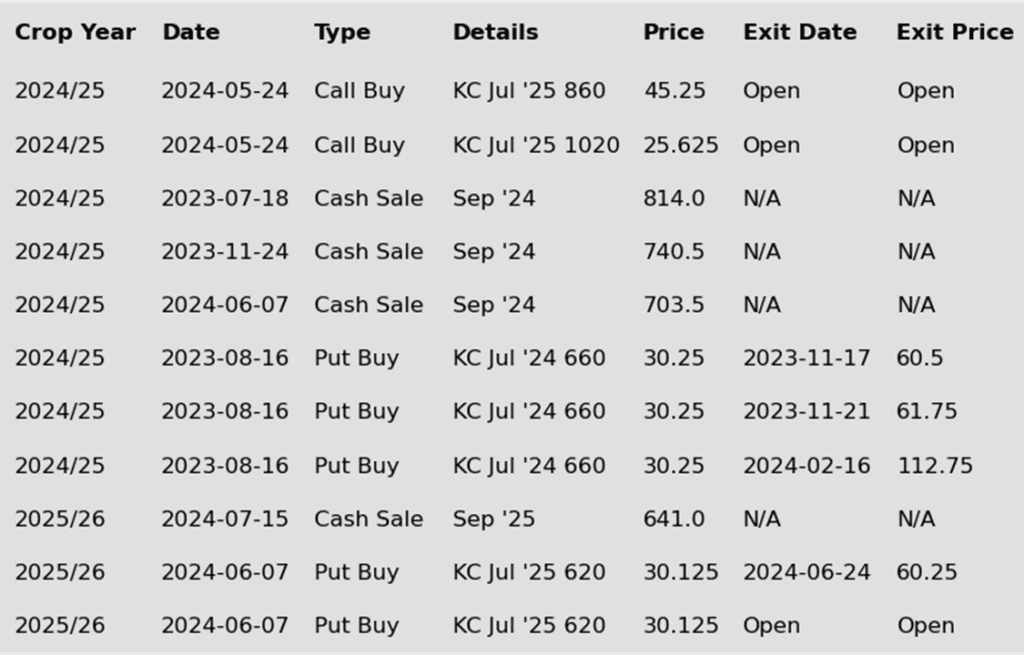

To date, Grain Market Insider has issued the following KC recommendations:

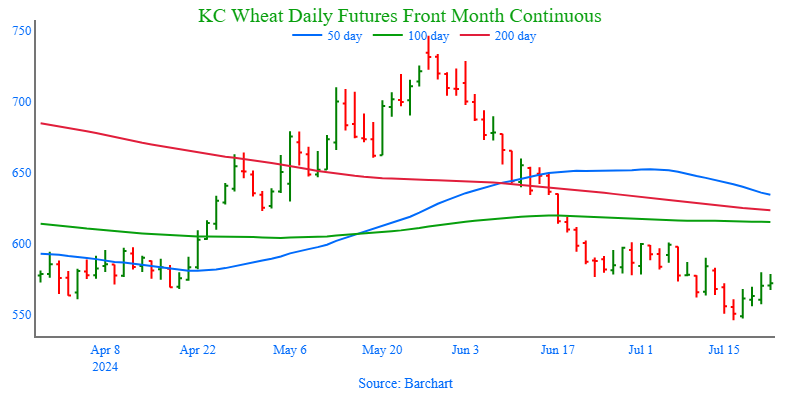

Above: After finding support just below 550, KC wheat prices could continue higher and encounter resistance near 600, as they move towards the 634 – 654 resistance area. A reversal lower, and a break below 545 could find further support in the 530 area.

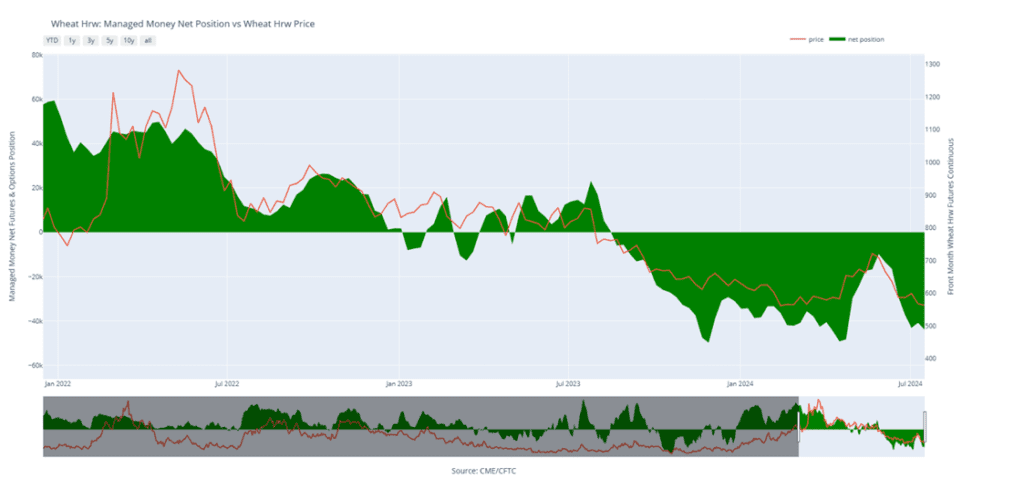

Above: KC Wheat Managed Money Funds net position as of Tuesday, July 16. Net position in Green versus price in Red. Money Managers net sold 3,085 contracts between July 9 – 16, bringing their total position to a net short 43,896 contracts.

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

Active

Sell SEP ’25 Cash

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

Since the end of May, the wheat market has been in a down trend as concerns about Russia’s shrinking wheat crop have eased and the US winter wheat crop exceeded expectations. During this period, managed funds reestablished their short positions in Minneapolis wheat. Though declining Russian export prices continue to keep a lid on US prices, smaller crops in Europe and the Black Sea region could increase US demand, potentially triggering a short-covering rally with the fund’s newly reestablished short position, especially as global wheat ending stocks are projected to decline again this year.

- No new action is recommended for 2023 Minneapolis wheat. Any remaining 2023 spring wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 Minneapolis wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Minneapolis wheat. With the recent close below the 712 support level, Grain Market Insider implemented its Plan B stop strategy, recommending additional sales for the 2024 crop due to waning upside momentum and an increased likelihood of a downward trend. Given the heightened volatility and the amount of time that remains to market this crop, we will maintain the current July ’25 KC wheat 860 and 1020 call options. Our target is a selling price of about 71 cents for the 860 calls to achieve a net neutral cost on the remaining 1020 calls. These 1020 calls will continue to protect existing sales and provide confidence to make additional sales at higher prices.

- Grain Market Insider sees a continued opportunity to sell a portion of your anticipated 2025 spring wheat production. Since rallying in late June, the market has retraced back toward its lows, and has broken the 644 support level. The breaking of 644 support suggests that our Plan A upside targets are now less likely to be achieved, and prices could trend lower. Considering this and that it is the time of year to begin getting early sales on the books for next year, Grain Market Insider is implementing its Plan B Stop strategy and recommends selling a portion of your 2025 spring wheat crop using either Sept ’25 futures or a Sept ’25 HTA contract, so that basis can be set at a more advantageous time later on.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

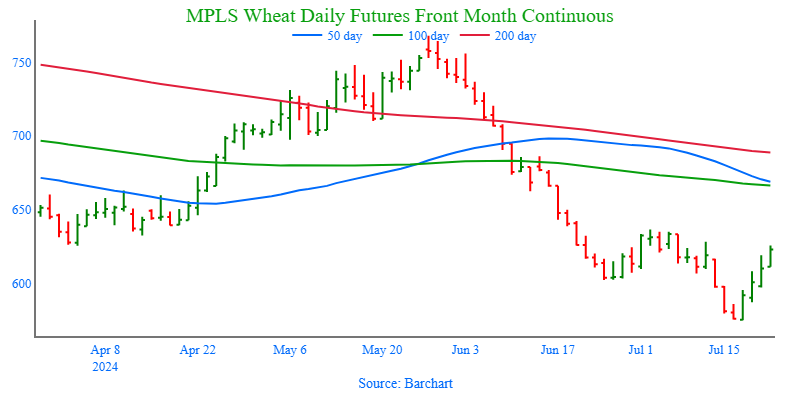

Above: The bullish key reversal posted on July 17 indicates that support lies just below the market around 575, and given that the market is oversold, prices could run toward the July highs near 636. Below 575, support should remain in the 550 – 540 area.

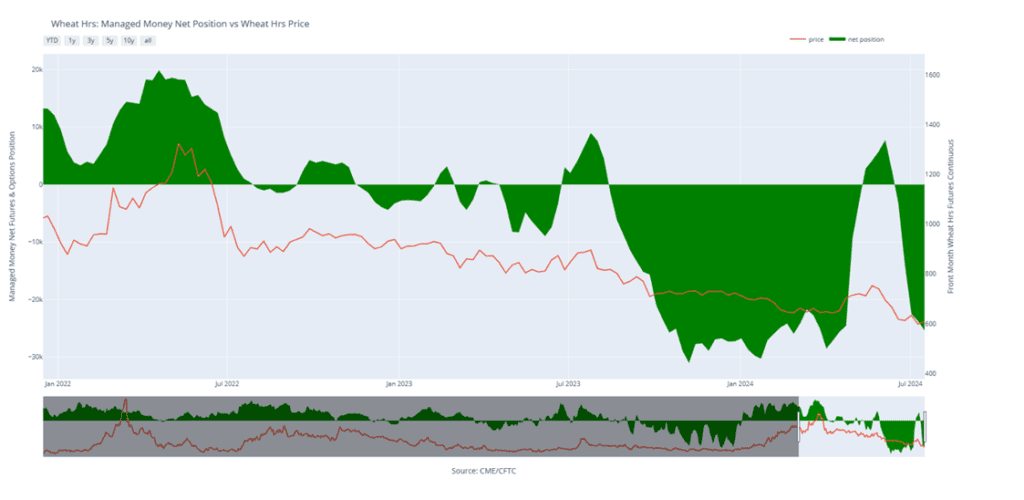

Above: Minneapolis Wheat Managed Money Funds net position as of Tuesday, July 16. Net position in Green versus price in Red. Money Managers net sold 1,638 contracts between July 9 – 16, bringing their total position to a net short 25,361 contracts.

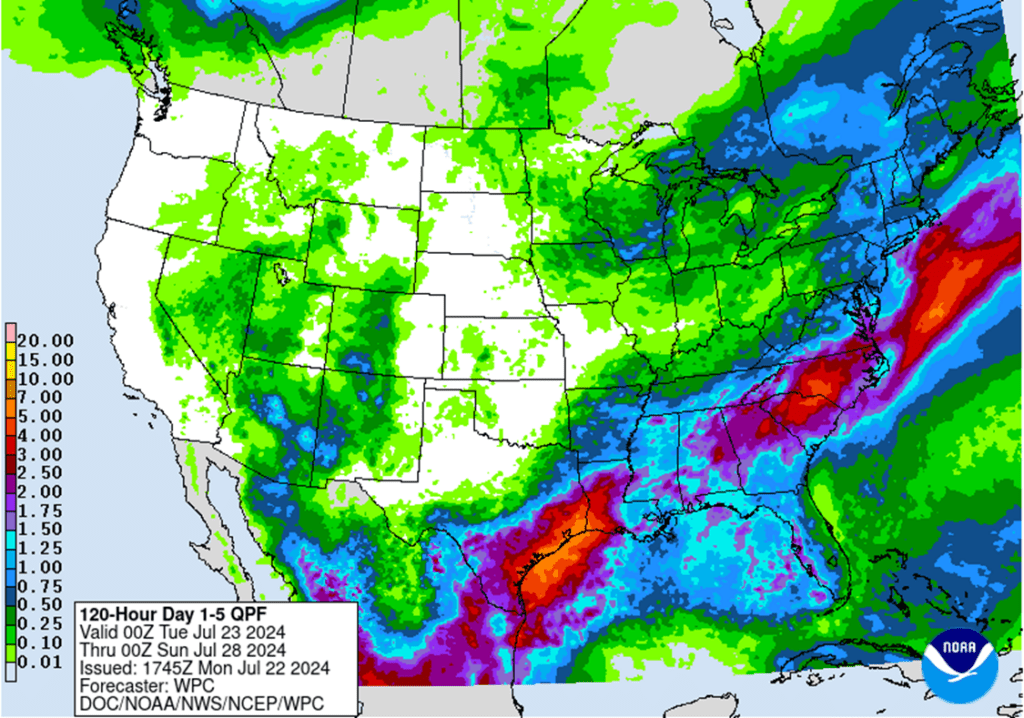

Other Charts / Weather

US 5-day precipitation forecast courtesy of NOAA, Weather Prediction Center.