7-2 End of Day: Corn and Beans Close in the Green, But Well Off Their Highs

The CME and Total Farm Marketing Offices Will Be Closed

Thursday, July 4, in Observance of Independence Day

All prices as of 2:00 pm Central Time

| Corn | ||

| SEP ’24 | 408 | 1 |

| DEC ’24 | 421.25 | 0.75 |

| DEC ’25 | 456.5 | -2.25 |

| Soybeans | ||

| AUG ’24 | 1150.25 | 4.25 |

| NOV ’24 | 1113 | 2 |

| NOV ’25 | 1111.25 | -2.75 |

| Chicago Wheat | ||

| SEP ’24 | 581 | -9.25 |

| DEC ’24 | 604.75 | -7.75 |

| JUL ’25 | 634.75 | -7 |

| K.C. Wheat | ||

| SEP ’24 | 592.25 | -7.25 |

| DEC ’24 | 608.75 | -6.5 |

| JUL ’25 | 630 | -4.75 |

| Mpls Wheat | ||

| SEP ’24 | 631 | -1.25 |

| DEC ’24 | 649.25 | -1.5 |

| SEP ’25 | 679 | 5.5 |

| S&P 500 | ||

| SEP ’24 | 5556 | 22.25 |

| Crude Oil | ||

| SEP ’24 | 81.96 | -0.36 |

| Gold | ||

| OCT ’24 | 2358.4 | -3.5 |

Grain Market Highlights

- With the prospect of a large crop looming, and carryover weakness from the wheat market, corn futures were unable to hold the majority of their earlier gains despite the reporting of a 100,000 mt flash sale.

- Like corn, the soybean market was unable to hold most of its gains from earlier in the session. Good to excellent crop ratings that remain the highest since 2020 continue to add pressure, but sharply higher soybean oil lent support.

- Soybean oil extended yesterday’s gains, closing sharply higher, supported by lower-than-expected soybean oil stocks from updated Census crush data. Meanwhile, soybean meal settled mixed, with the August contract closing higher while the deferred contracts closed lower.

- A fast harvest pace and pressure from lower Matif wheat futures weighed on the wheat complex, which settled mostly lower on potential profit taking from yesterday’s rally.

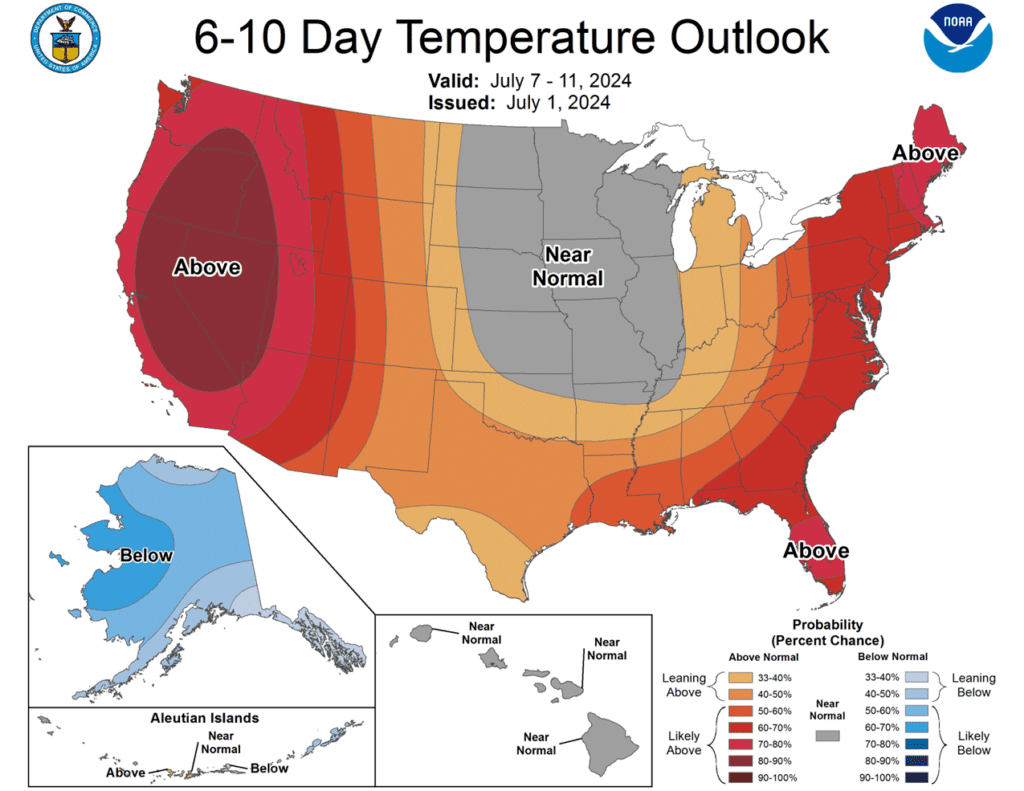

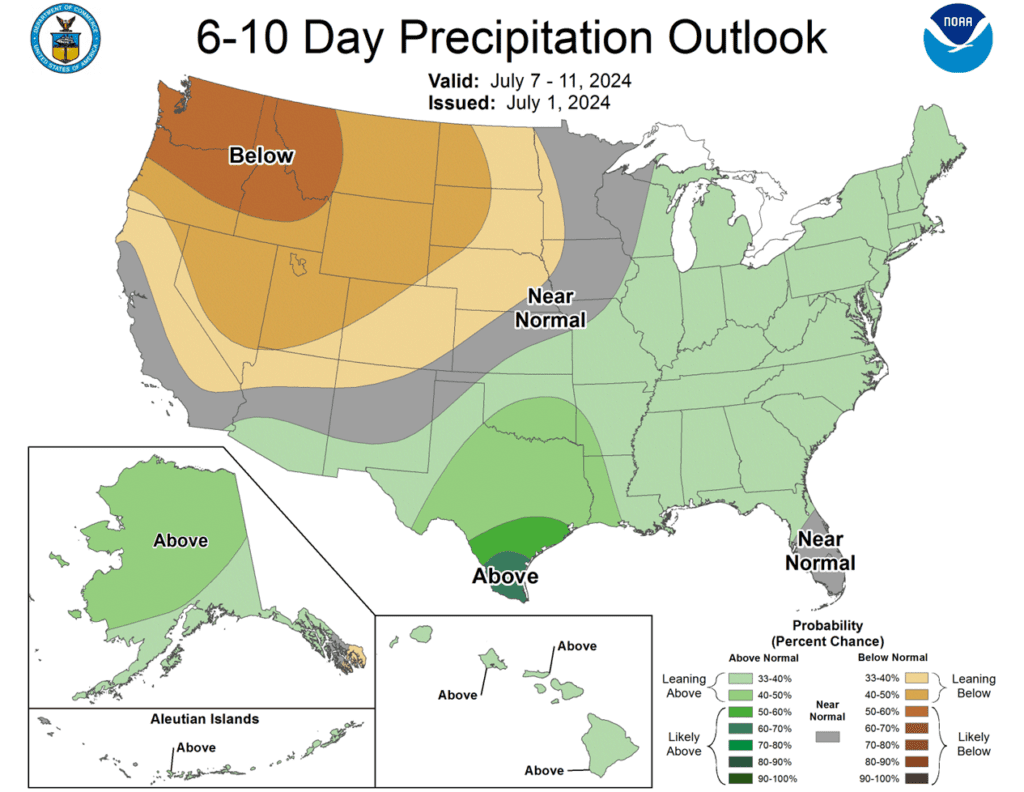

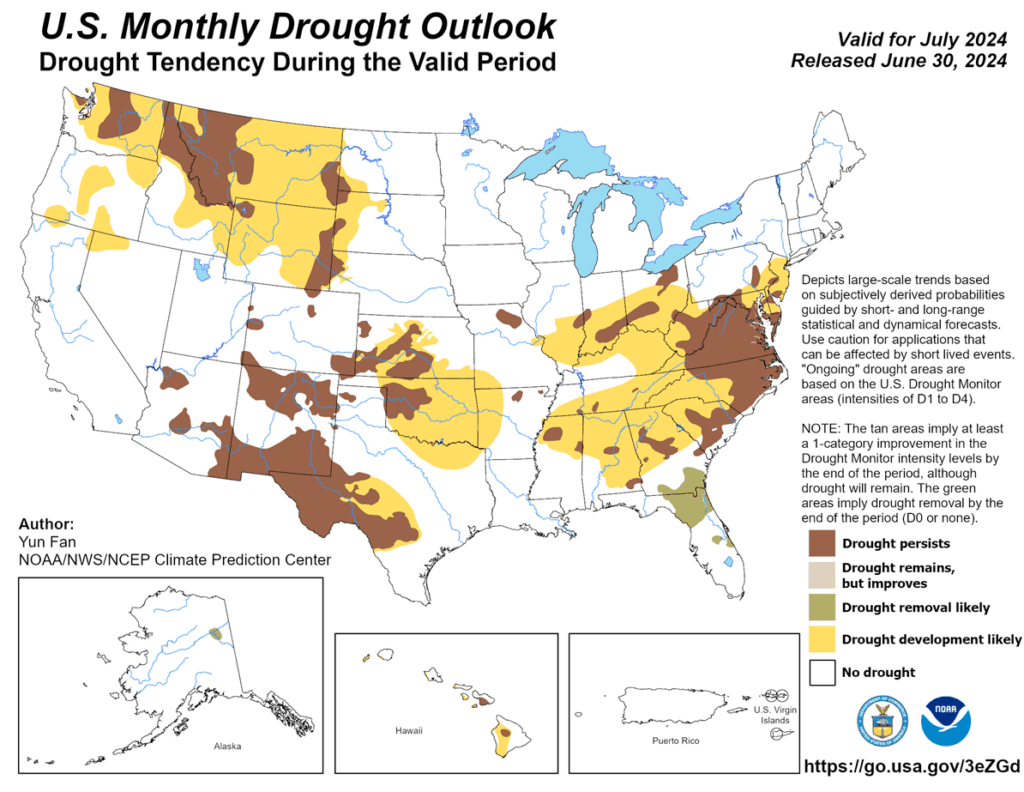

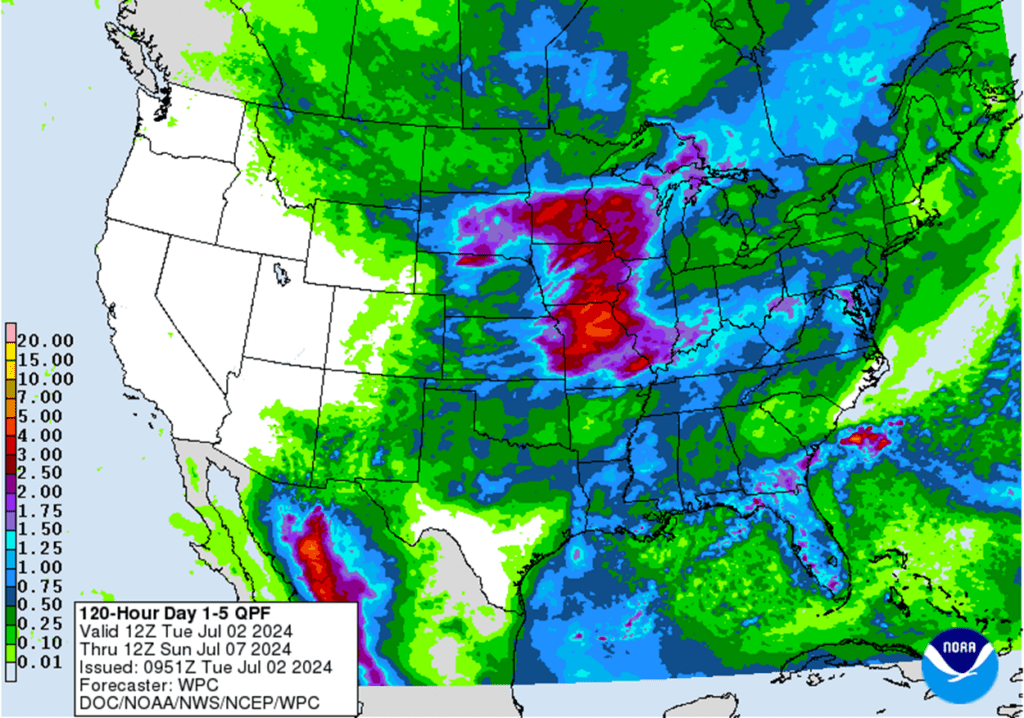

- To see the updated US 5-day precipitation forecast, 6-10 day Temperature and Precipitation Outlooks, and the Monthly US Drought Outlook courtesy of NOAA, the Weather Prediction Center, and NDMC scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

The June Stocks and Acreage reports gave the corn market little in the way of bullish news as both numbers came in above expectations, increasing the possibility of a carryout in excess of 2 billion bushels for the 24/25 crop year. While the market has a bearish tilt, demand has been solid, and the 2024 growing season is still young with lots of potential ahead as weather remains the dominant market mover.

- No new action is recommended for 2023 corn. Any remaining old crop 2023 corn should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 corn – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 corn. We recently recommended buying Dec ’24 470 and 510 calls after Dec ’24 closed below 451, for their relative value and because we are at that time of year of high volatility when markets can move swiftly. Moving forward, our current strategy is to target the value of 29 cents to exit the Dec ’24 470 calls. Exiting the 470 calls at 29 cents will allow you to lock in gains in case prices fall back and hold the remaining 510 calls at or near a net neutral cost, which should continue to protect existing sales and give you confidence to make further sales if the market rallies sharply. To take further action, we are targeting the 490 – 510 area to recommend making additional sales versus Dec ’24.

- No new action is currently recommended for 2025 corn. As we move through the growing season with its potential for high volatility, we are looking for higher prices and anticipate issuing two more sales recommendations before the beginning of September. Also given the tendency for the growing season to provide some of the best pricing opportunities for the next crop year we will also be watching the calendar along with price action to make additional recommendations. We will be looking to make another sales recommendation by July 8 if our upside objectives aren’t met by then.

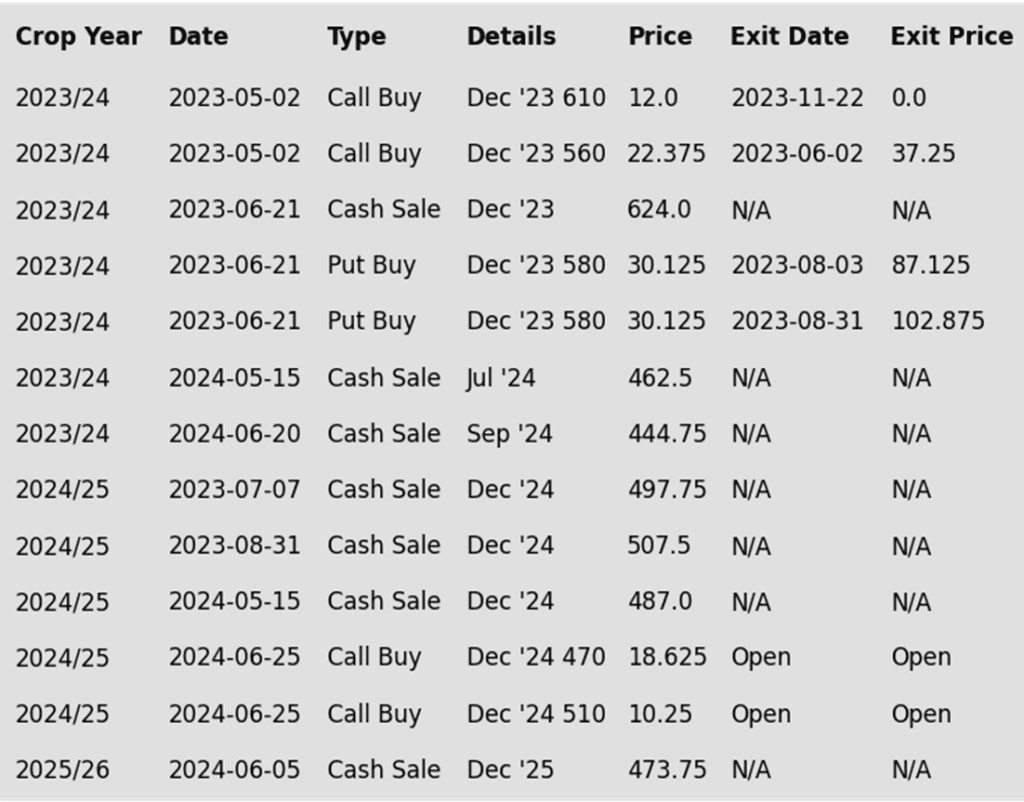

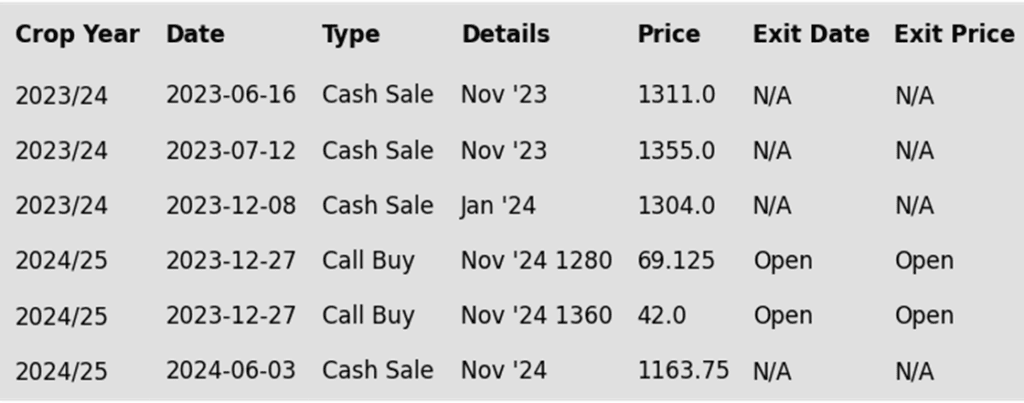

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn futures softened from early session gains to finish mixed on the session, as the prospects of large supplies, lack of consistent demand, and weakness in the wheat market weighed on corn futures.

- Overall demand has become more stagnant for corn, but old crop USDA targets will still likely be reached. New crop export demand has been disappointing compared to the last handful of years. Demand will be a key for the market to find stability. The USDA announced a flash sale of corn, with Columbia purchasing 100,000 mt (3.9 MB) of old crop corn.

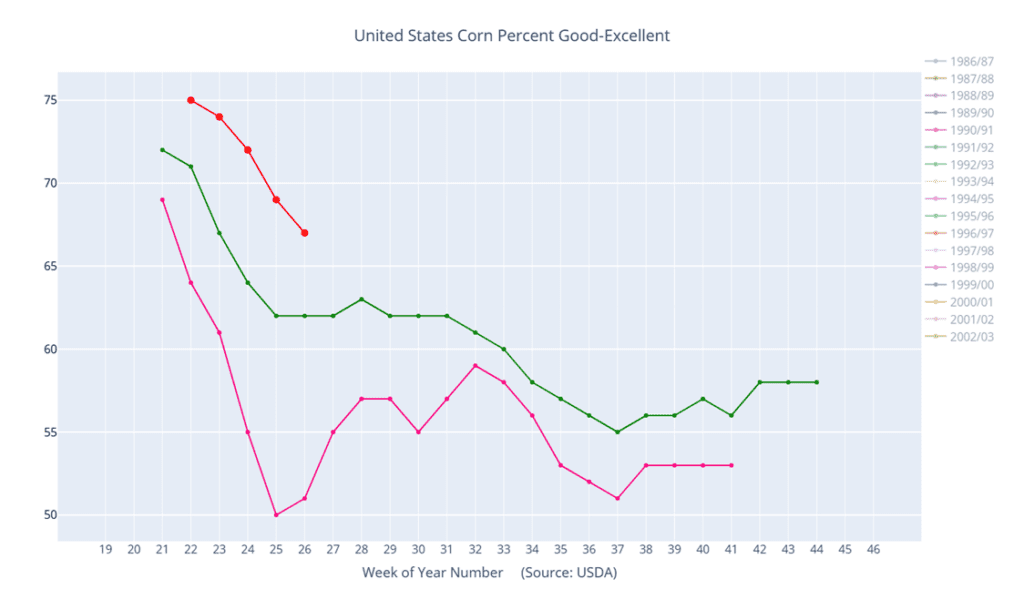

- On Monday afternoon’s Crop Progress report, the USDA reported that corn conditions fell to 67% good to excellent, down 2% from last week, and slightly below market expectations. This rating is well above last year’s 51% G/E rating.

- The Brazilian Real is trading at its lowest level versus the US Dollar since January 2022. The weakening Brazilian currency improves the competitiveness of Brazilian corn and soybeans versus the US on the global export market.

- Weather forecasts will remain a major focus for the markets going into the key July weather time frame. While the forecast remains on the warm side, precipitation remains active into the middle of the month. Currently, weather is non-threatening overall to crop production.

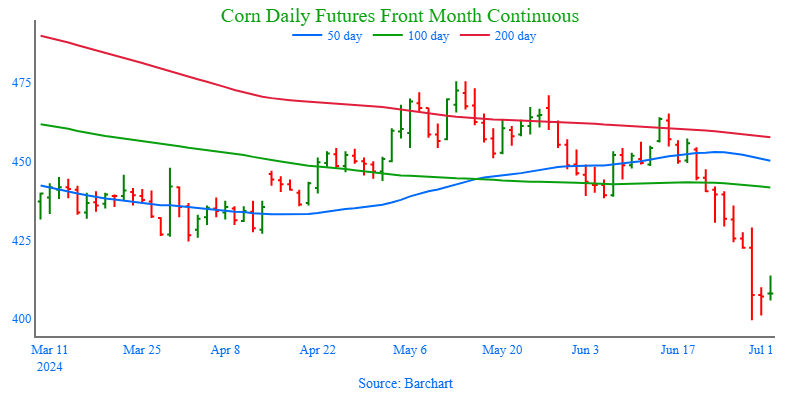

Above: Bearish stocks and acreage numbers pushed prices through the February low of 408 ¾. The next level of potential support lies near 393. Initial overhead resistance may enter the market between 420 and 430.

Above: Corn condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

Weighed down by sluggish export demand and non-threatening weather, the soybean market was on a choppy downward trajectory leading up to the June stocks and acreage reports. Although June 1 stocks came in above expectations, acreage came in below, leaving less margin for error if growing conditions turn hot and dry later on. With much of the growing season ahead of us, a weather-related issue or surge in demand appears to be the most likely catalysts to push prices back near their recent highs.

- No new action is recommended for 2023 soybeans. As we progress into the 2024 growing season, time is becoming limited to market the remaining 2023 old crop inventory. Although we are currently targeting a rebound to the 1275 – 1325 area versus Aug ’24 futures as our Plan A strategy, for what will likely be our final sales recommendation for the 2023 crop, we also don’t want to carry old crop inventory past mid-July due to seasonal weakness. Taking this into consideration, if the market does not present the opportunity to make sales at our Plan A target, our Plan B strategy will be to issue our final sales recommendation sometime in mid-July.

- No new action is recommended for the 2024 crop. At the end of December, we recommended buying Nov ’24 1280 and 1360 calls due to the amount of uncertainty in the 2024 soybean crop and to give you confidence to make sales and protect those sales in an extended rally. Given that the market has retreated since that time, we are targeting the lower 1200s versus Nov ’24 futures to exit 1/3 of the 1280 calls to help preserve equity. Most recently we employed our Plan B strategy with the close below 1180 in Nov ’24 and recommended making additional sales due to the potential change in trend. With much of the growing season still ahead of us, should the market turn back higher, we continue to target the 1260 – 1290 range from our Plan A strategy to potentially make two additional sales recommendations.

- No Action is currently recommended for 2025 Soybeans. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

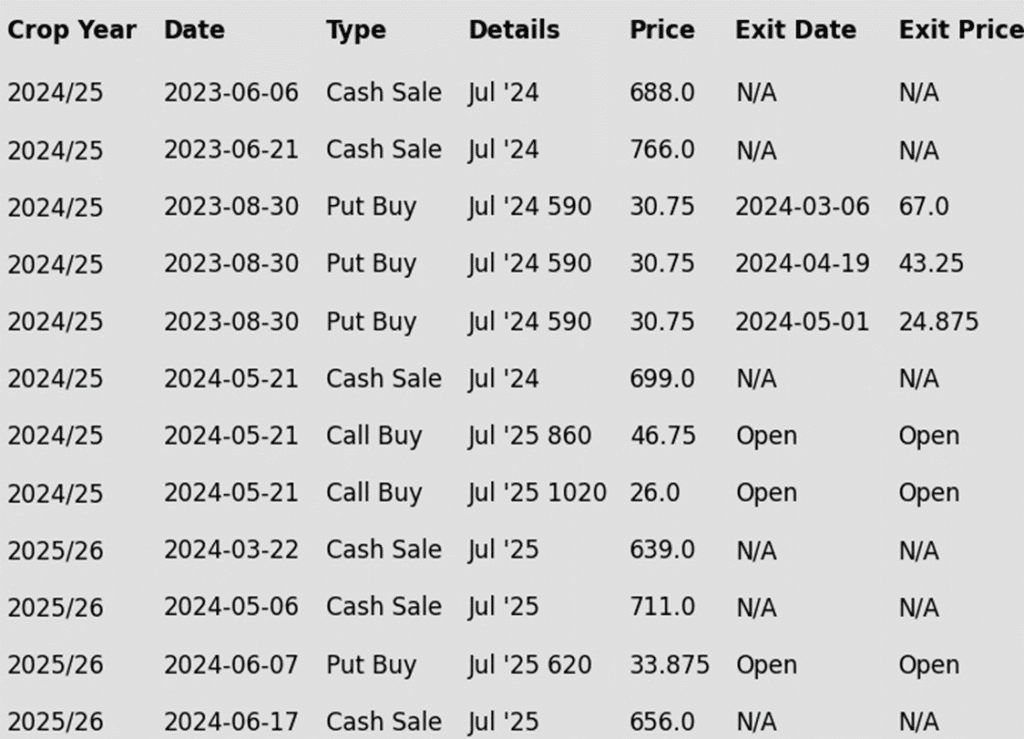

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans closed higher but faded significantly from their highs earlier this morning, which saw prices in the August contract up as much as 16 cents. Bull spreading between August and November soybeans continued today with the spread widening. Soybean meal was bull spread as well with the front month higher but deferred lower, and soybean oil was higher.

- Yesterday afternoon, the USDA released its Crop Progress report which showed no changes to the good to excellent ratings that remained at 67%. Trade was expecting a slight 1-point decline. 20% of the crop is blooming, which is on par with a year ago and compares to 8% last week. 3% of the crop is setting pods which is also on par with last year’s pace.

- Domestic crush demand has been very firm and has been a supportive factor with export demand so slow. 192 mb of soybeans were crushed in May which is higher than a year ago. Profitable crush margins are supporting this demand and are also contributing to the bull spreading as producers buy cash soybeans.

- Soybean oil was higher for the fifth consecutive day and was a large source of support for soybeans throughout the day. Today, the USDA said that renewable biodiesel capacity was up 4.1 billion pounds in April compared to a year ago at that time. In addition, India may be placing higher tariffs on Chinese goods which could cause trade conflicts that could move China to buy soybean oil from the US instead.

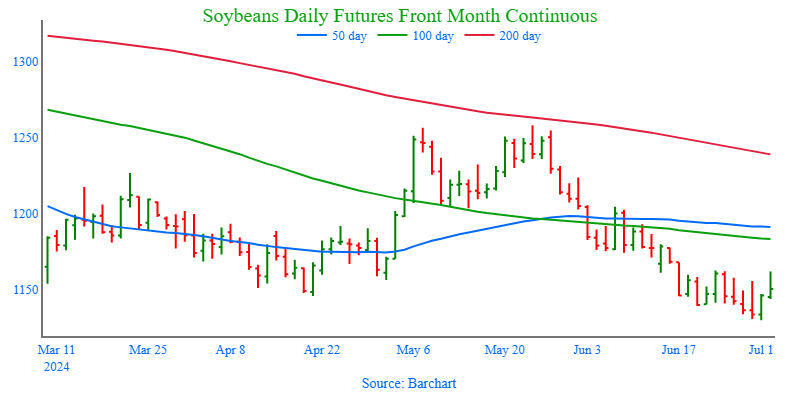

Above: Support in the area of 1130 – 1125 appears to be holding. If prices recover to the upside, they may encounter initial overhead resistance near 1160 – 1165 with further resistance up towards 1185 – 1200. Otherwise, if they retreat further, support may be found near 1045.

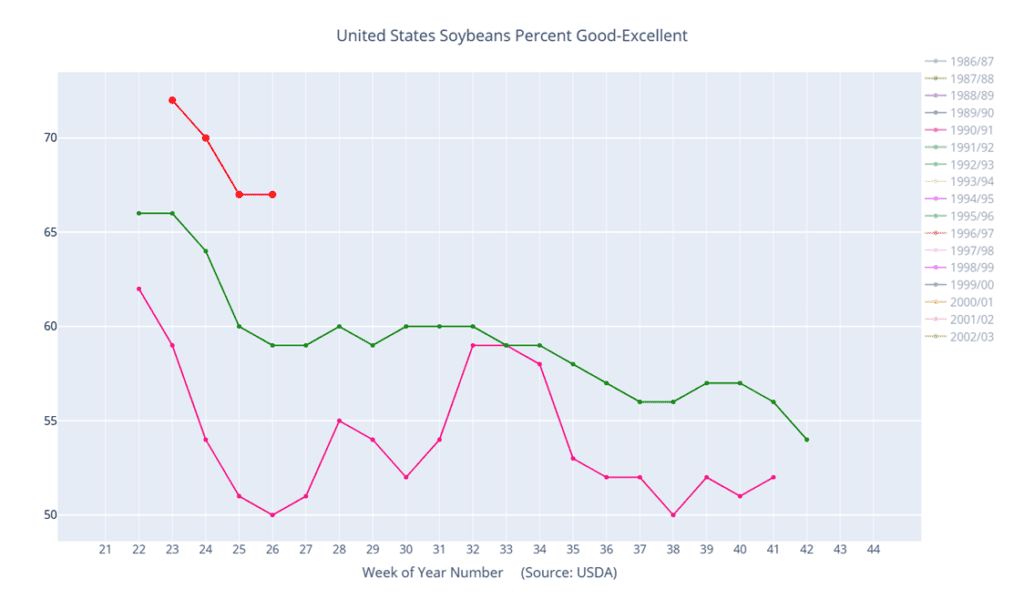

Above: Soybeans condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Wheat

Market Notes: Wheat

- Despite higher closes for corn and soybeans, wheat failed to follow suit. The pressure from winter wheat harvest, a lower close for Paris milling wheat futures, and potential profit-taking after yesterday’s rally may be contributing factors. However, Chicago and Kansas City September contracts managed to hold the 10-day moving average as support today after rallying above it yesterday.

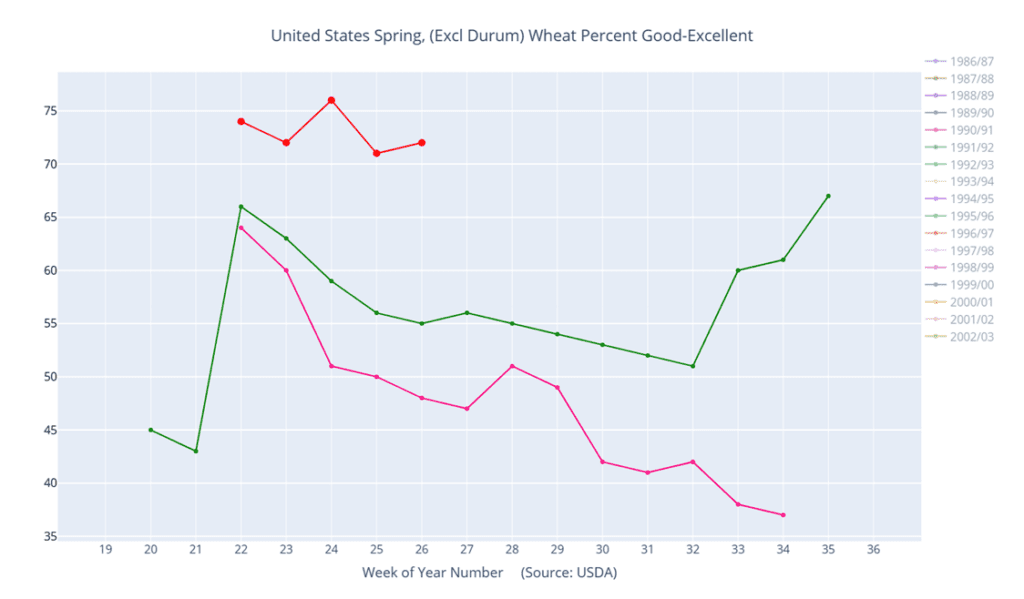

- Additional pressure may have come from yesterday’s Crop Progress report, which showed winter wheat harvest at 54% complete, compared to the 39% average and 33% a year ago. This harvest pressure could limit any upside rallies for now. Furthermore, spring wheat conditions improved by 1% to 72% good to excellent, with only 4% of the crop rated poor to very poor.

- According to Argus, Ukraine’s 24/25 wheat crop production is estimated at 20.3 mmt, an increase from their previous estimate but still 2.2 mmt below last year’s level. The year-on-year decline is attributed to lower yields and harvested acreage.

- The EU’s Monitoring Agricultural Resources unit (MARS) estimates that Russia’s 24/25 wheat production may be below average, forecasting a crop of 82.5 mmt, about 5% under the average and down from 93.6 mmt in 2023. Frost damage in May and drought in June are cited as reasons for the yield decline.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Chicago Wheat Action Plan Summary

Since rallying nearly 200 cents from the March low to the May high, largely on fund short covering from Russian crop concerns and dryness in the southwestern Plains, prices have fallen from their peak with seasonal weakness and the onset of harvest. Although the market is showing signs of weakness, it is also becoming oversold, which can be supportive in the event prices turn back higher, and the recent breakout above the December highs suggests there is potential for a test of the 2023 summer highs post-harvest.

- No new action is currently recommended for 2023 Chicago wheat. Any remaining 2023 soft red winter wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 Chicago wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Chicago wheat. Considering the recent rally in wheat, we recommended taking advantage of the elevated prices to make additional sales and buy upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 740 – 760 versus Sept ’24 to recommend further sales and to target a selling price of about 73 cents in the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is currently recommended for 2025 Chicago Wheat. Given the weakness in the wheat market we recently employed our Plan B strategy and recommended making an additional sale as prices broke through 667 support. Moving forward, we continue to target the value of 68 cents in the July ’25 620 puts (double the original approximate cost) to exit half of the original previously recommended position, leaving the balance to continue to provide downside coverage with a net neutral cost. To take further action, our strategy is to target the 750 – 780 range to recommend making additional sales.

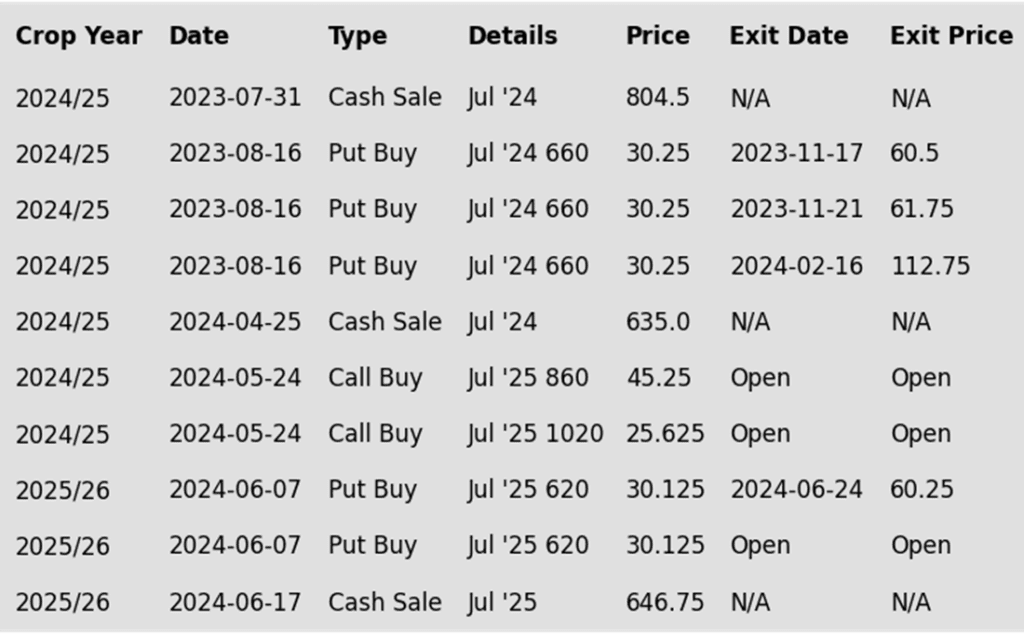

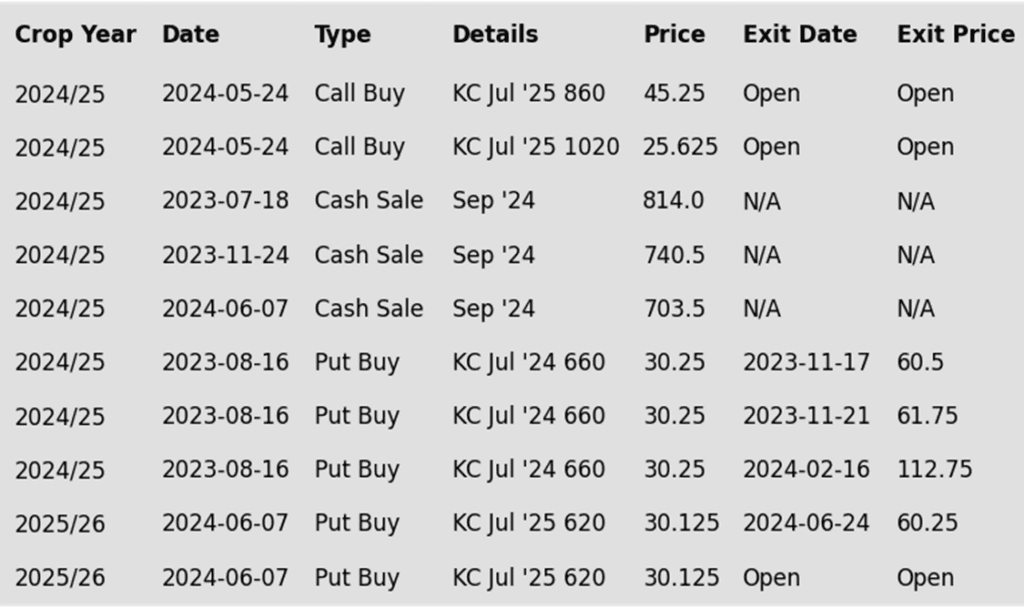

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

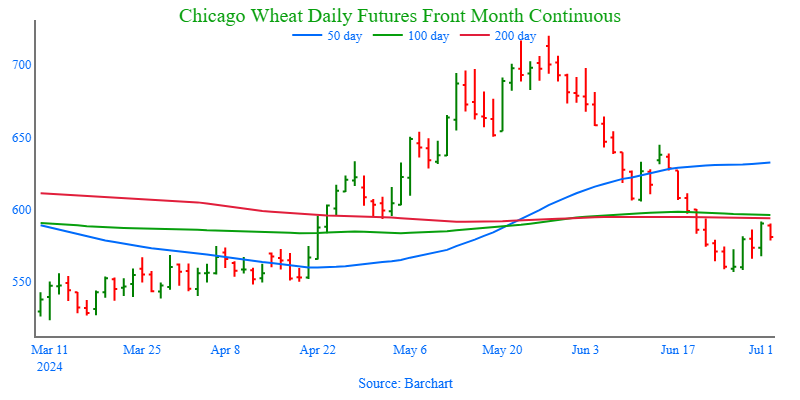

Above: Sept ’24 Chicago wheat appears to have found support in the 555 – 560 area, and considering the oversold conditions, it could rebound toward the 595 – 605 level where psychological and technical resistance sits. A move above there could lead to a test of the 630 – 645 area, while below 555 the market may find further support between 550 and 520.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

KC Wheat Action Plan Summary

Since the end of May the wheat market has been trending lower as concerns regarding Russia’s shrinking wheat crop have waned, along with US HRW harvest yields being higher than expected. During this time the market has become extremely oversold, and managed funds have begun reestablishing their short positions. While harvest pressure and falling Black Sea export prices continue to weigh on US prices, the funds’ short position and oversold conditions could culminate in a short covering rally on any increase in demand as world wheat ending stocks are expected to fall yet again this year.

- No new action is recommended for 2023 KC wheat. Any remaining 2023 hard red winter wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 KC wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 KC wheat. Considering the recent upside breakout in KC wheat, we recommended buying upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 780 – 810 versus Sept ’24 to recommend further sales and to target a selling price of about 71 cents on the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is currently recommended for 2025 KC Wheat. We recently recommended exiting half of the previously recommended July ’25 620 puts once they reached 60 cents (double the original approximate cost) to realize gains in case the market rallies back, while still holding the remaining 620 puts at, or near, a net neutral cost for continued downside coverage on any unsold bushels. Looking ahead, our strategy is to target the 700 – 725 range to recommend making additional sales.

To date, Grain Market Insider has issued the following KC recommendations:

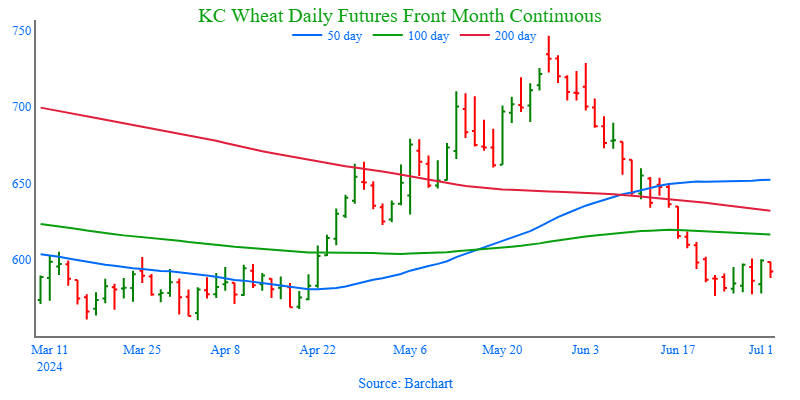

Above: It appears that support has been found around 576. If this area holds and prices turn back higher, initial resistance could be found near 620 with heavier resistance up towards 650 – 660. If the 576 area doesn’t hold, they may find further support between 560 – 550.

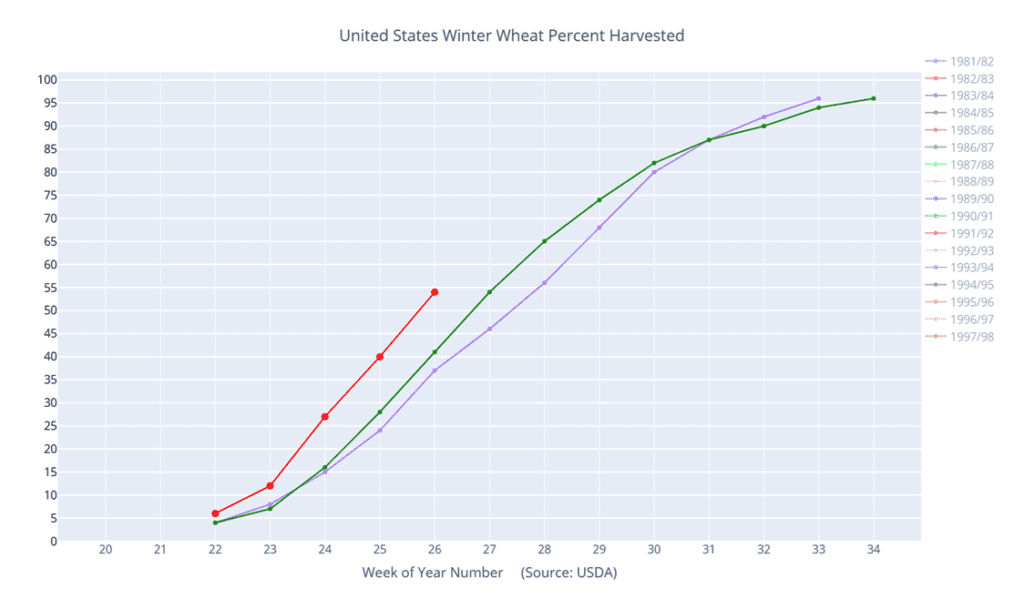

Above: Winter wheat percent harvested (red) versus the 5-year average (green) and last year (purple).

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

Since the end of May, the wheat market has been trending lower as concerns about Russia’s shrinking wheat crop have eased and US HRW harvest yields have exceeded expectations. During this period, the market has become extremely oversold, leading managed funds to reestablish their short positions in Minneapolis wheat. Although declining Black Sea export prices and slow world demand continue to depress US prices, the funds’ short positions and oversold conditions could trigger a short-covering rally with any increase in demand, especially as global wheat ending stocks are projected to decline again this year.

- No new action is recommended for 2023 Minneapolis wheat. Any remaining 2023 spring wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 Minneapolis wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Minneapolis wheat. With the recent close below the 712 support level, Grain Market Insider implemented its Plan B stop strategy, recommending additional sales for the 2024 crop due to waning upside momentum and an increased likelihood of a downward trend. Given the heightened volatility and the amount of time that remains to market this crop, we will maintain the current July ’25 KC wheat 860 and 1020 call options. Our target is a selling price of about 71 cents for the 860 calls to achieve a net neutral cost on the remaining 1020 calls. These 1020 calls will continue to protect existing sales and provide confidence to make additional sales at higher prices.

- No new action is currently recommended for the 2025 Minneapolis wheat crop. We recently recommended exiting half of the previously recommended July ’25 KC 620 puts once they reached 60 cents (double their original approximate cost), to lock in gains in case the market rallies back, while still holding the remaining 620 puts at, or near, a net neutral cost for continued downside coverage on any unsold bushels. Grain Market Insider is continuing to monitor the markets and may begin considering the first sales targets after July 8.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

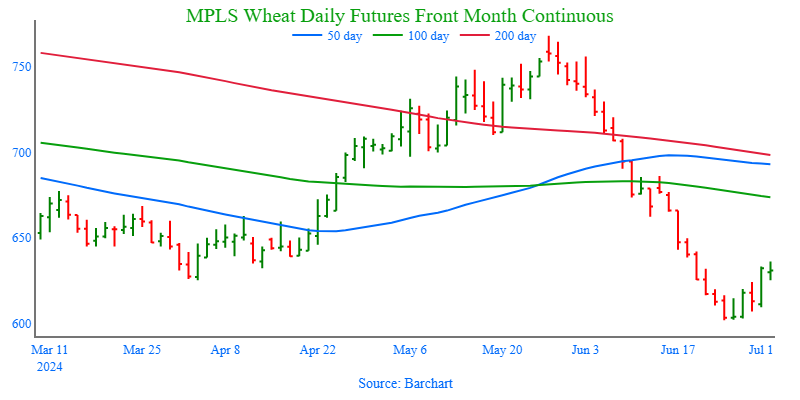

Above: Sept ’24 Minneapolis wheat appears to have found support around 600, and considering the oversold conditions of the market, a rally back towards the 662 – 686 resistance area may be possible. Otherwise, a market close below 596 support could suggest a further decline towards 542.

Above: Spring wheat condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Other Charts / Weather

Above: US 5-day precipitation forecast courtesy of NOAA, Weather Prediction Center.