6-5 End of Day: Grains Edge Higher Following Positive Talks Between US and China

All Prices as of 2:00 pm Central Time

| Corn | ||

| JUL ’25 | 439.5 | 0.75 |

| DEC ’25 | 448.25 | 4.5 |

| DEC ’26 | 475 | 3.5 |

| Soybeans | ||

| JUL ’25 | 1051.75 | 6.75 |

| NOV ’25 | 1033.25 | 8.25 |

| NOV ’26 | 1056.5 | 11 |

| Chicago Wheat | ||

| JUL ’25 | 545.5 | 2.25 |

| SEP ’25 | 559.75 | 2.5 |

| JUL ’26 | 617 | 2 |

| K.C. Wheat | ||

| JUL ’25 | 542.5 | 2 |

| SEP ’25 | 555.5 | 1.5 |

| JUL ’26 | 614.75 | 2.5 |

| Mpls Wheat | ||

| JUL ’25 | 625.25 | 1.75 |

| SEP ’25 | 636 | -0.5 |

| SEP ’26 | 676 | 0 |

| S&P 500 | ||

| SEP ’25 | 6027.75 | -7 |

| Crude Oil | ||

| AUG ’25 | 62.48 | 0.59 |

| Gold | ||

| AUG ’25 | 3377.9 | -21.3 |

Grain Market Highlights

- 🌽 Corn: Corn futures finished mostly higher on the day thanks to strong export sales and flow over support from high ethanol output data yesterday.

- 🌱 Soybeans: Soybeans got a boost on Thursday after confirmation of positive trade war talks between the U.S. and China.

- 🌾 Wheat: Wheat futures closed higher across all three classes, supported by global production cuts and a slightly weaker dollar.

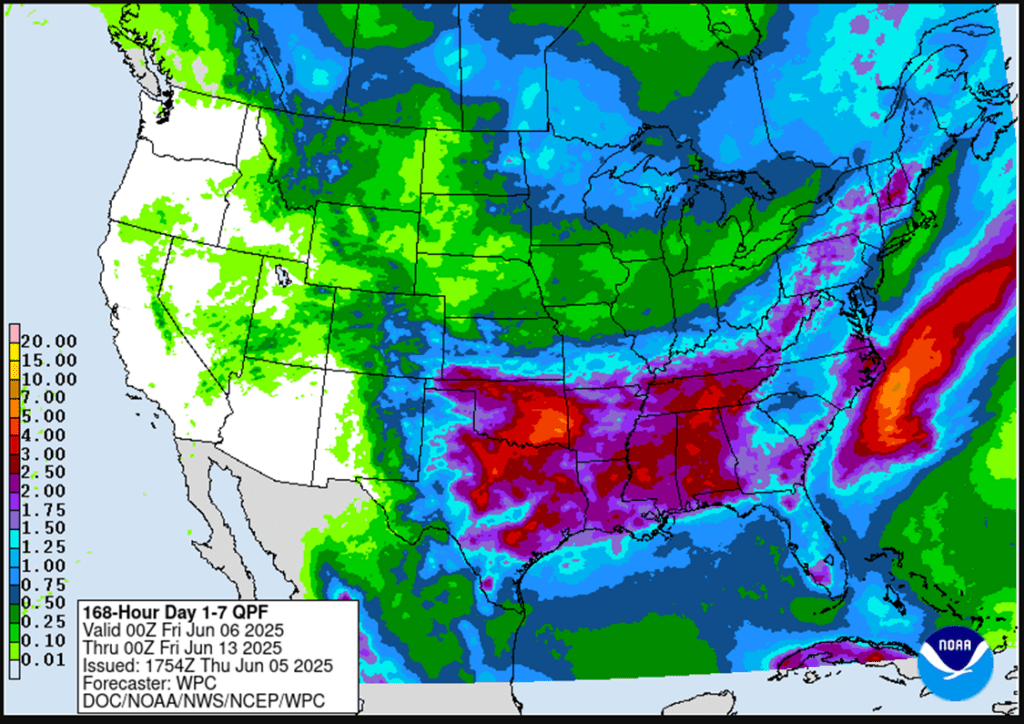

- To see updated U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Wheat section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

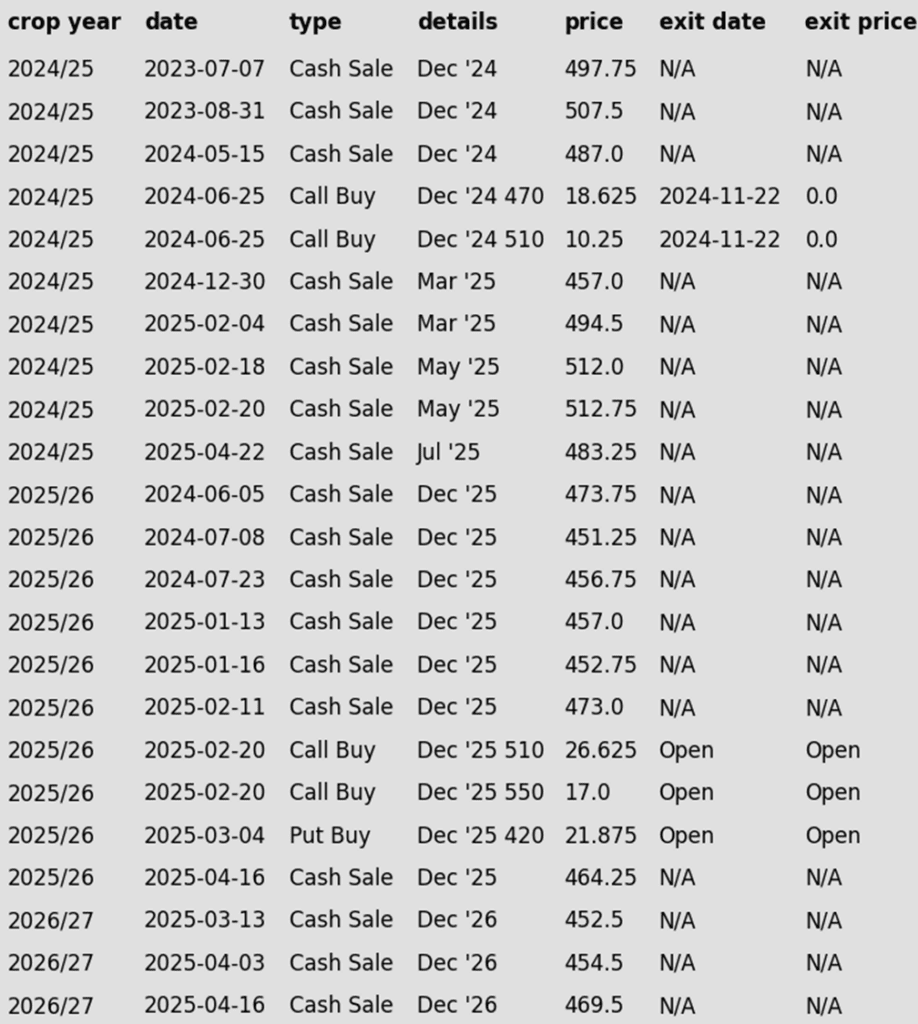

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Eight sales recommendations made to date, with an average price of 494.

- Changes:

- None.

- Continuing to hold out for potential upside volatility during the growing season before issuing the next sales recommendations.

2025 Crop:

- Plan A:

- Exit all 510 December calls @ 43-5/8 cents.

- Exit half of the December 420 puts @ 43-3/4 cents.

- Exit one-quarter of the December 420 puts if December closes at 411 or lower.

- Roll-down 510 & 550 December calls if December drops to 399.

- Plan B: No active targets.

- Details:

- Sales Recs: Seven sales recommendations have been made to date, with an average price of 461.25.

- Changes:

- None.

- Well positioned for growing season volatility, with a solid base of sales already in place. Both upside and downside targets remain active — ready to begin legging out of open options positions and to roll down call options as market conditions warrant.

2026 Crop:

- Plan A: Next cash sale at 474 vs December ‘26.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations have been made to date, with an average price of 460.

- Changes:

- None.

- Be prepared for the next sales recommendation at any time as sales need to be systematically and incrementally progressed based on the calendar throughout the growing season.

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Short covering and value buying helped lift the corn markets for the second consecutive session as new corn crop prices led the market higher. December corn futures are trading 9 ¾ cents higher going into Friday trade.

- Despite the strong tone of demand in both export sales and ethanol usage, the corn market remained bear-spread with limited gains or extended selling pressure in the July contract. The strong planting pace, prospects of large Brazil corn crop, and crop-friendly weather forecast have seen end users comfortable with front end supplies, limited upside currently on old crop corn prices. July corn futures are 4 ½ cents lower on the week going into Friday trade.

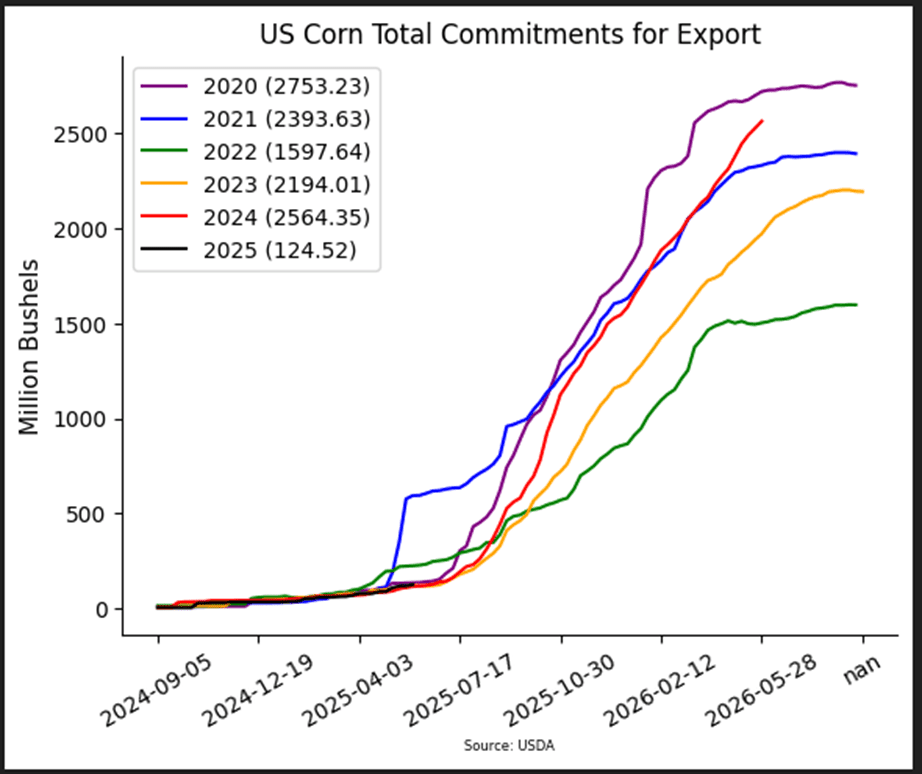

- USDA released corn export sales on Thursday morning. For the week ending May 29, the USDA reported new sales of 942,000 MT (37.1 mb) for 2024-25, and 160,000 MT (6.3 mb) for 2025-26. This was within analysts’ expectations. Mexico was the top buyer of U.S. corn last week. Total export sales commitments for 2024-25 marketing year now total 2.564 bb, up 27% from a year ago, and within 36 mb of the USDA target for the year.

- Commodity markets were supported by comments by President Trump regarding his phone conversation with President Xi of China. The possibility of more dialogue eased some of the trade tensions fears that may have limited the corn market over recent sessions.

- Weather forecast into the middle of June remains supportive for good crop growth, and a limiting gain in the corn market. Longer range models reflect a drier and warm pattern going into the end of the month, but long-range forecast lack reliability and can change daily.

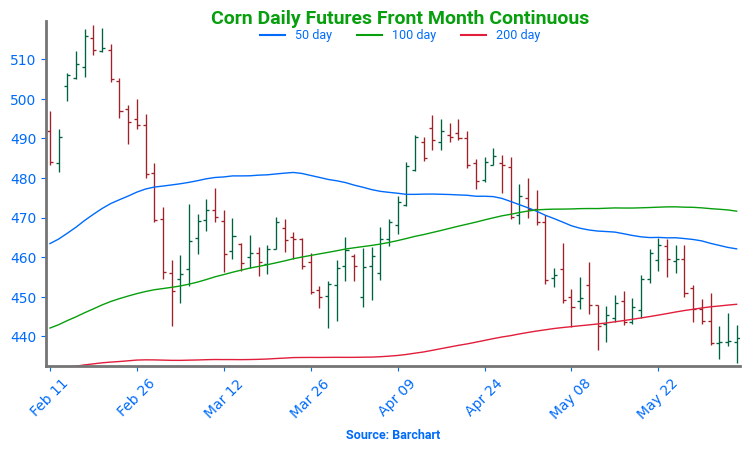

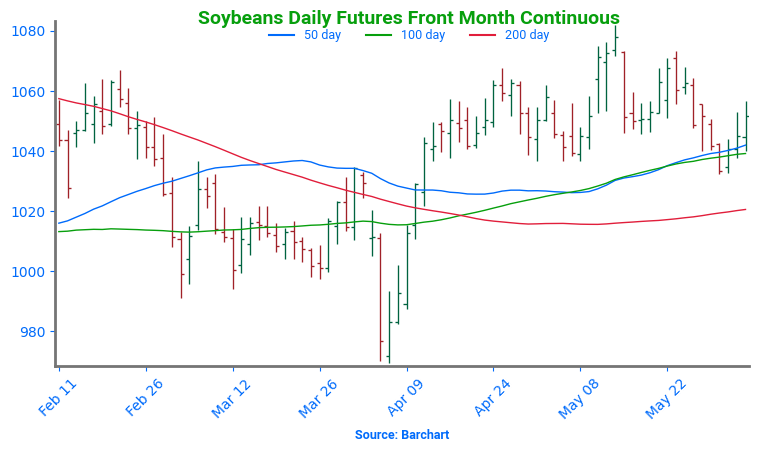

Corn Futures Eye Weather Risks After May Pullback

After bouncing off the key $4.50 level in April following a bullish WASDE and a break above the 50-day moving average, corn futures faced renewed pressure through May. Rapid planting progress and lingering demand concerns dragged prices back below $4.70. So far, the $4.45–$4.50 support zone — reinforced by the 200-day moving average — has held firm. With planting nearing completion, market focus is quickly shifting to summer weather. NOAA’s extended outlook for a warmer, drier Western Corn Belt could revive risk premium and set the stage for weather-driven rallies. Resistance emerges near $4.70, with stronger resistance around the April highs at $4.90.

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

Active

Sell NOV ’25 Cash

2026

No New Action

Puts

2024

No New Action

2025

New Alert

Enter(Buy) JAN ’26 Puts:

1040 @ ~ 49c

2026

No New Action

2024 Crop:

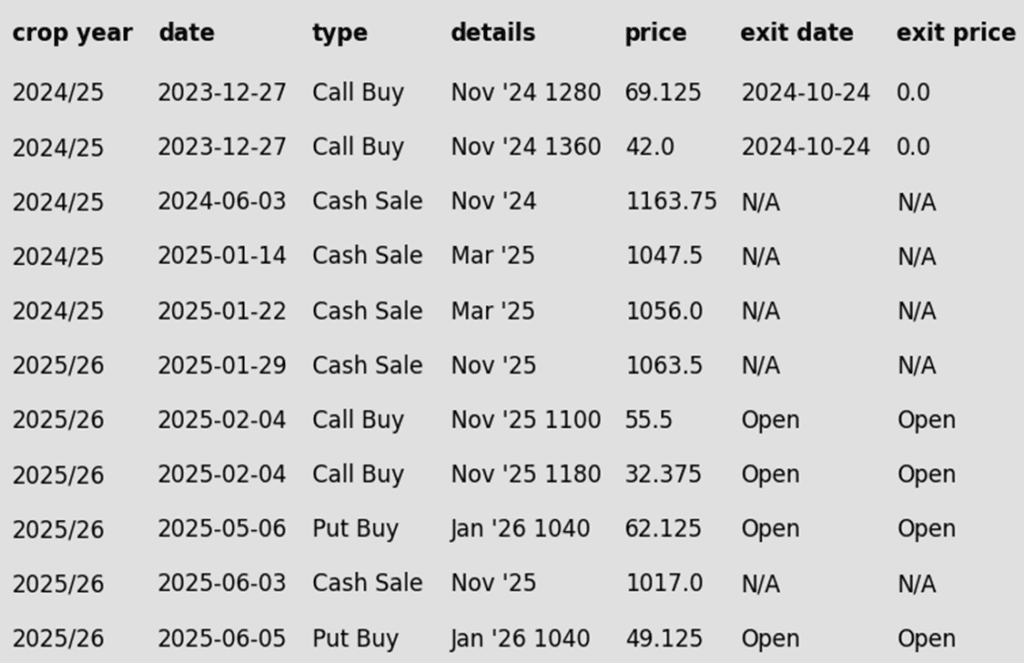

- Plan A: Next cash sale at 1107 vs July.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made to date, with an average price of 1089.

- Changes:

- None.

- No Changes (for Now): While there are no adjustments at the moment, Monday’s close below 1036 support could prompt a revision to Plan A in the near future. Stay alert for potential updates.

2025 Crop:

- NEW ACTION – Buy January ‘26 1040 put options for approximately 49 cents in premium, plus fees and commission. This is a recommendation to purchase a second round of 1040 puts, following the first round advised on May 6. Seasonally, May and June are key months to secure downside price protection. Adding this second layer provides additional coverage against lower prices while preserving upside potential and avoiding any further commitment of physical bushels.

- CONTINUED OPPORTUNITY – Sell another portion of your 2025 soybean crop. The November contract closed below key 1018.50 support Monday, triggering Grain Market Insider’s Plan B strategy, which recommends selling a second portion of your 2025 soybean crop. Bigger picture, the soybean market continues to trade within a broader range — roughly 1060 on the topside and 960 on the bottom. Monday’s break of support shifts the short-term trend within this sideways range to down, increasing the risk of a move back toward 960.

- Plan A:

- No active sales targets.

- Exit one-third of 1100 call options at 1085 vs November.

- Exit remaining two-thirds of 1100 November call options at 88 cents.

- Plan B:

- No active targets.

- Details:

- Sales Recs: Now two sales recommendations made to date, with an average price of 1040.25.

- Changes:

- None.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- Changes:

- None.

- We’re now in the seasonal window where first sales targets for next year’s crop could post at any time. Stay tuned.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans closed higher today following positive trade talks between President Trump and China’s Xi, which will hopefully lead to further negotiations. Today’s export sales report fell within trade expectations but were not very strong. Soybean meal was slightly higher, while bean oil was mixed in bear spreading action.

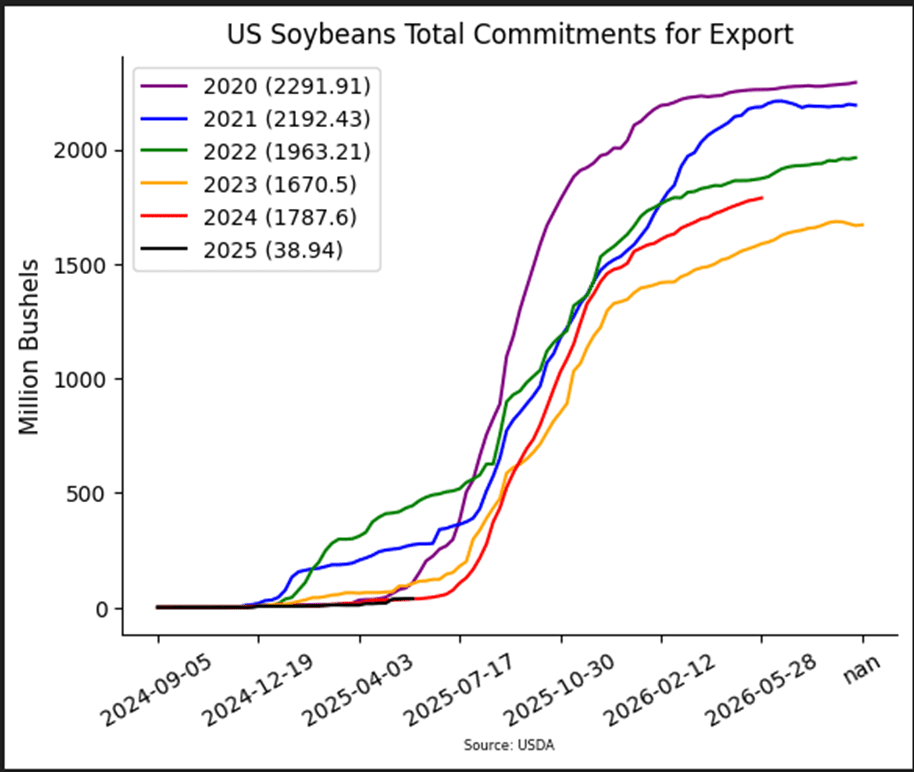

- Today’s export sales report saw an increase of 7.1 million bushels of soybean sales for 24/25 and 0.1 mb for 25/26. This was up 33% from last week but down 30% from the prior 4-week average. Top buyers were Bangladesh, Norway, and Taiwan. Last week’s export shipments of 11.3 mb were below the 13.4 mb needed each week to meet USDA estimates.

- Today, Presidents Trump and Xi spoke on the phone and, according to Trum,p had a very good conversation regarding the countries’ trade truce. More meetings are expected to follow and will ideally end with a trade agreement.

- The soybean meal market could provide some support for soybean futures in the near future. Managed hedge funds are holding a near-record short position in the soybean meal market, but demand for U.S. soybean meal has been improving. Soybean meal exports for the current marketing year are at a record pace and up 5% over last year. With the prospects of tighter acres for next crop year, soybean meal could see buying strength from value buyers at these price levels.

Soybean Futures Remain Range-Bound into June

Soybean futures tumbled below the key $10.00 mark in early April on tariff-related headlines, triggering technical selling after breaking the March low. However, the decline was short-lived as buyers stepped in, lifting prices back above $10.00 and reclaiming key moving averages, including a clean break above the 200-day moving average — a level that now serves as solid support. With no fresh bullish catalyst and favorable weather weighing on sentiment, futures remain range-bound. The 200-day should continue to offer support, while resistance holds near the May high of $10.82.

Wheat

Market Notes: Wheat

- With the exception of Minneapolis futures, wheat closed marginally higher today. Ongoing concerns about global production, along with anticipation of better U.S. and world trade relations helped keep the wheat settlements mostly positive. However, U.S. winter wheat harvest pressure may somewhat limit upside potential for now.

- Grain markets may have received a boost today in part due to the phone call between President Trump and Chinese President Xi. It appears to have been constructive; news outlets report that Trump stated it was a “very good phone call” and this may have given traders some optimism that a trade deal is near.

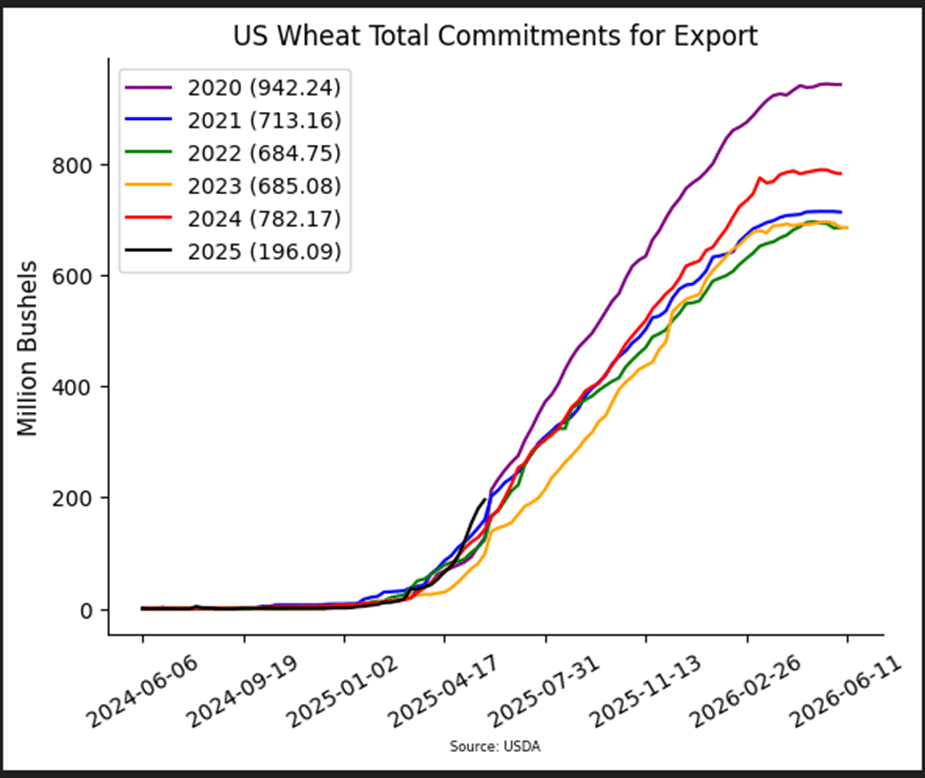

- The USDA reported a decrease of 1.8 mb of wheat export sales for 24/25, but an increase of 16.3 mb for 25/26. Shipments last week reached 19.8 mb, which is well below the 50.5 mb pace needed per week to reach the USDA’s 820 mb export goal for 24/25. Total 24/25 shipments at 768 mb are up 13% from last year.

- Recent rains have improved the drought situation for both winter and spring wheat areas. According to the USDA, as of June 3, an estimated 12% of winter wheat acres are experiencing drought conditions – this is down 4% from last week. Meanwhile, spring wheat areas in drought dropped from 29% to 19% during the same time period.

- LSEG sees Chinese wheat production at 141.7 mmt in their latest estimate. This would be down 1% from the last update and the decrease is due to the impact of ongoing drought. Other private estimates range as low as 133-135 mmt. For reference, last year China’s wheat crop was a record 140 mmt.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A:

- Target 699.25 vs July for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Four sales recommendations made to date, with an average price of 690.

- Changes:

- None.

2025 Crop:

- Plan A:

- Target 693.75 against July for the next sale.

- Plan B:

- Buy call options if July closes over 633.50 macro resistance.

- Details:

- Sales Recs: Five sales recommendations made to date, with an average price of 646.

- Changes:

- None.

2026 Crop:

- Plan A:

- Target 675 vs July ‘26 for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: One sales recommendation made to date, at 624.

- Changes:

- None.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Potentially Finds Support

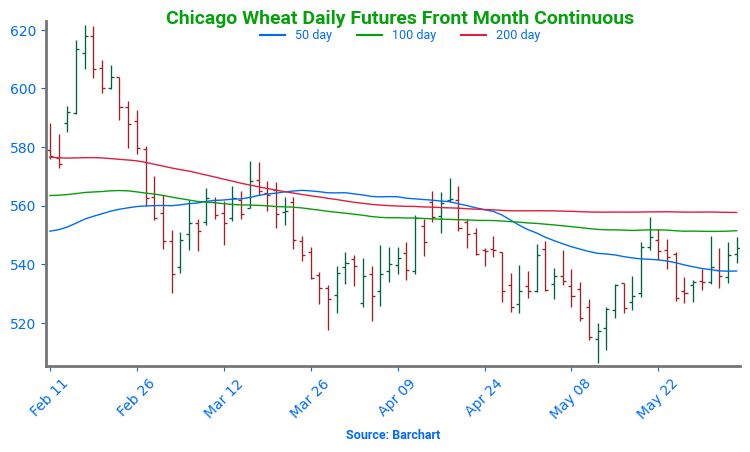

After months of range-bound trade, Chicago wheat futures broke out in February, reaching October highs above $6.15 before quickly retreating back into their 2024 range. By mid-May, prices slipped below key support near $5.30 but have since stabilized around $5.20. The next major resistance is the 200-day moving average — a firm weekly close above it could signal a trend reversal and open the door to broader gains.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made to date, with an average price of 677.

- Changes:

- None.

2025 Crop:

- Plan A: No active targets.

- Plan B:

- Buy call options if July closes over 653 macro resistance.

- Details:

- Sales Recs: Four sales recommendations made to date, with an average price of 639.

- Changes:

- None.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- Changes:

- None.

- The first sales targets could post this week — keep checking back for updates.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Finds Support

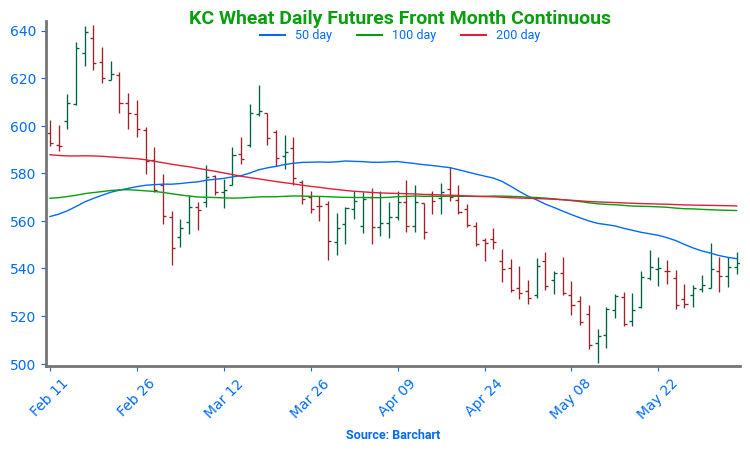

With ample spring moisture across the Plains and sluggish demand, wheat futures have lacked bullish momentum, recently touching multi-year lows near $5.00 in early May—a level that has since held. A recovery above $5.40 would suggest a potential bottom is in place. On a rebound, the 200-day moving average marks initial resistance, with a stronger ceiling at the February highs near $6.40.

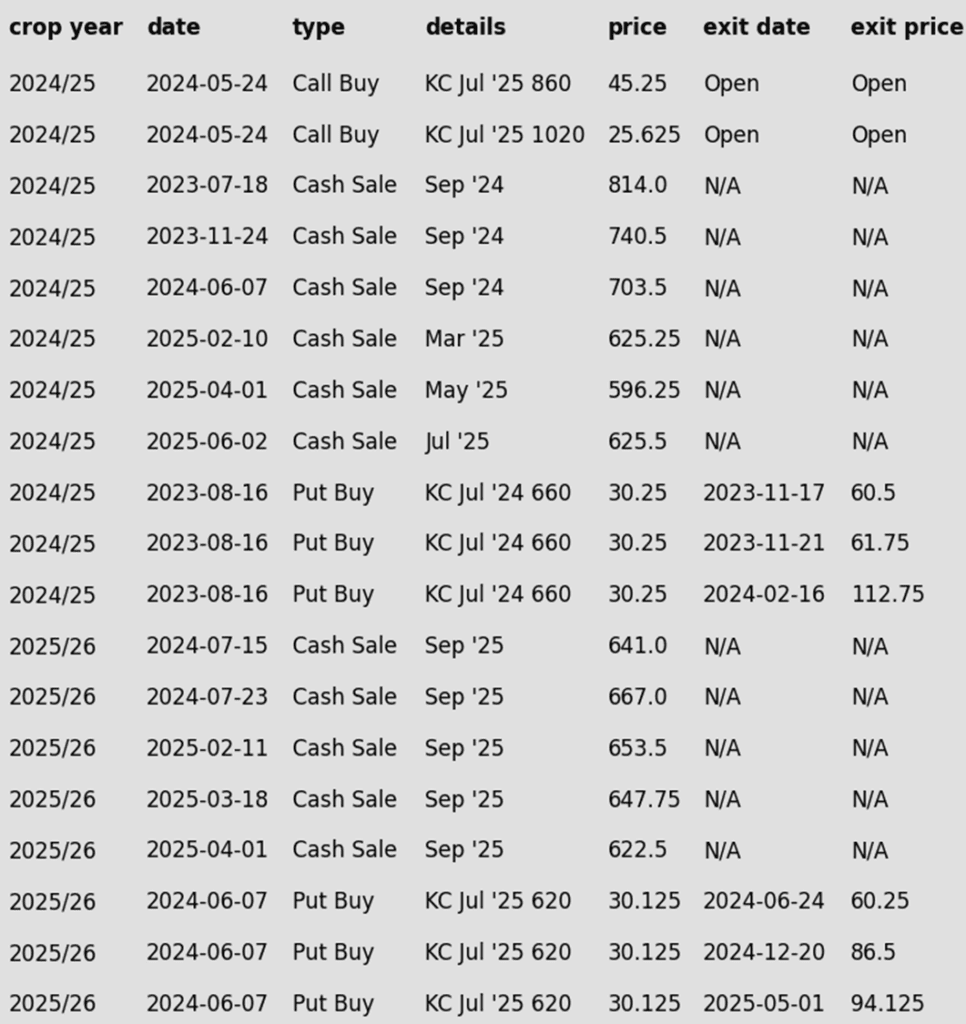

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

Active

Sell JUL ’25 Cash

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- CONTINUED OPPORTUNITY – Sell another portion of your 2024 Minneapolis wheat crop. This marks the sixth sale for the 2024 crop and may well be the final sales recommendation for this marketing year, as Grain Market Insider shifts focus to the 2025 and 2026 crops moving forward. Use this rally as an opportunity to consider pricing any remaining unsold bushels.

- Plan A: Sell more cash now.

- Plan B: No active targets.

- Details:

- Sales Recs: Now six sales recommendations made to date, with an average price of 684.

- Changes:

- None.

2025 Crop:

- Plan A: No active targets.

- Plan B:

- Buy KC call options if July KC closes over 653 macro resistance.

- Details:

- Sales Recs: Five sales recommendations made to date, with an average price of 646.

- Changes:

- None.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Changes:

- None.

- First sales targets are expected to post after July 1.

- Changes:

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

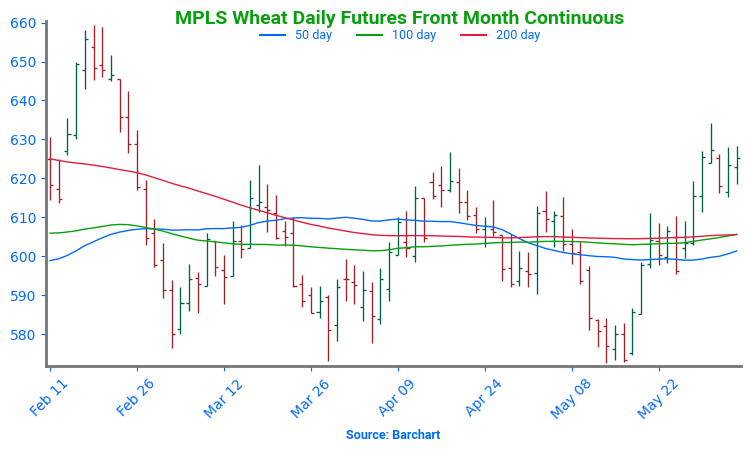

Spring Wheat Runs Higher on Poor Conditions

Spring wheat futures broke out of a prolonged sideways trend in late January, with momentum accelerating in mid-February after a decisive close above the 200-day moving average. Although late-month weakness briefly pulled prices below key support, futures traded mostly sideways through spring. A sharp rally was triggered in late May after crop condition ratings came in at their second lowest in 40 years, sparking short covering. Prices are now back above a confluence of moving averages and nearing the top of the recent range. Key support sits just above $6.00, with the next upside target near February’s highs around $6.60.

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

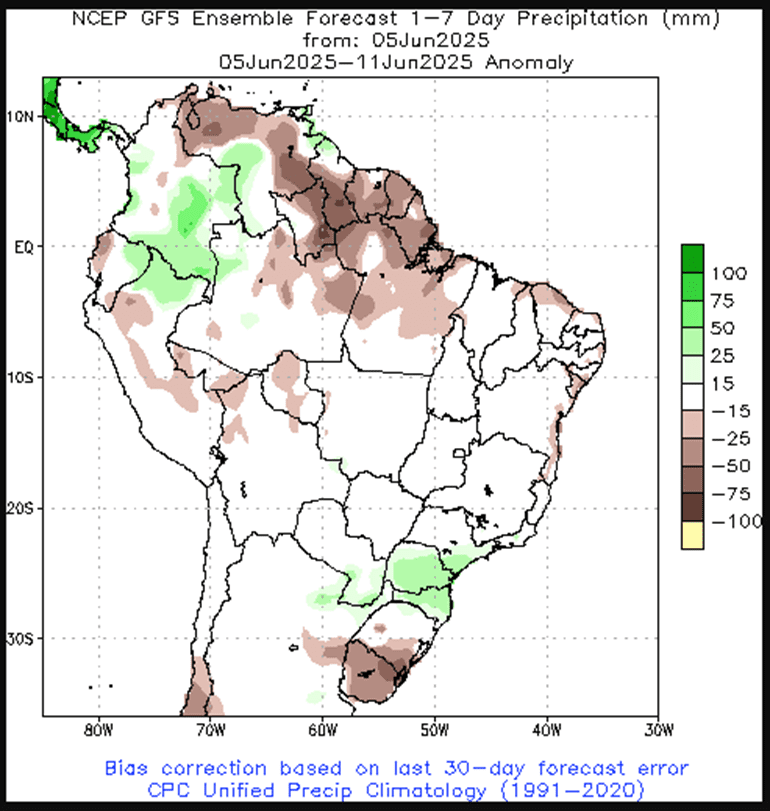

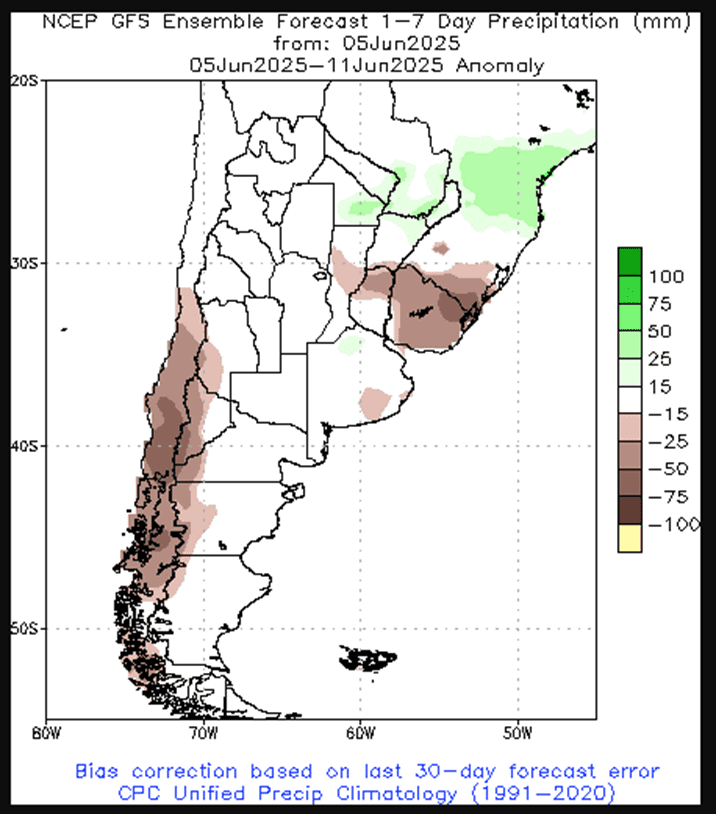

Above: Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.