6-20 End of Day: Markets Fall Sharply Thursday

All prices as of 2:00 pm Central Time

| Corn | ||

| JUL ’24 | 439.75 | -10.25 |

| DEC ’24 | 456.75 | -11 |

| DEC ’25 | 469.25 | -6.75 |

| Soybeans | ||

| JUL ’24 | 1155.25 | -18.75 |

| NOV ’24 | 1116.75 | -15.25 |

| NOV ’25 | 1114.25 | -6.25 |

| Chicago Wheat | ||

| JUL ’24 | 572.75 | -9.25 |

| SEP ’24 | 586 | -13 |

| JUL ’25 | 639.25 | -13 |

| K.C. Wheat | ||

| JUL ’24 | 592 | -8.75 |

| SEP ’24 | 598.25 | -11.5 |

| JUL ’25 | 633.75 | -9 |

| Mpls Wheat | ||

| JUL ’24 | 618.75 | -14 |

| SEP ’24 | 625.75 | -14.5 |

| SEP ’25 | 671.25 | -8.75 |

| S&P 500 | ||

| SEP ’24 | 5546.75 | -13 |

| Crude Oil | ||

| AUG ’24 | 81.41 | 0.7 |

| Gold | ||

| AUG ’24 | 2373.4 | 26.5 |

Grain Market Highlights

- The corn market broke lower on Thursday following the midweek Juneteenth pause. Continuous corn futures broke through trendline support dating back to February as well as the 100-day moving average, spurring further technical selling pressure.

- Soybeans were not immune to the commodity wide sell off on Thursday. November futures fell to their lowest level since August of 2021. Soybean meal and oil futures were lower on the day as well.

- Wheat futures fell once again on Thursday across all three classes. July Chicago wheat has closed lower in 15 of the last 17 trading sessions as all three wheats remain in severely oversold territory.

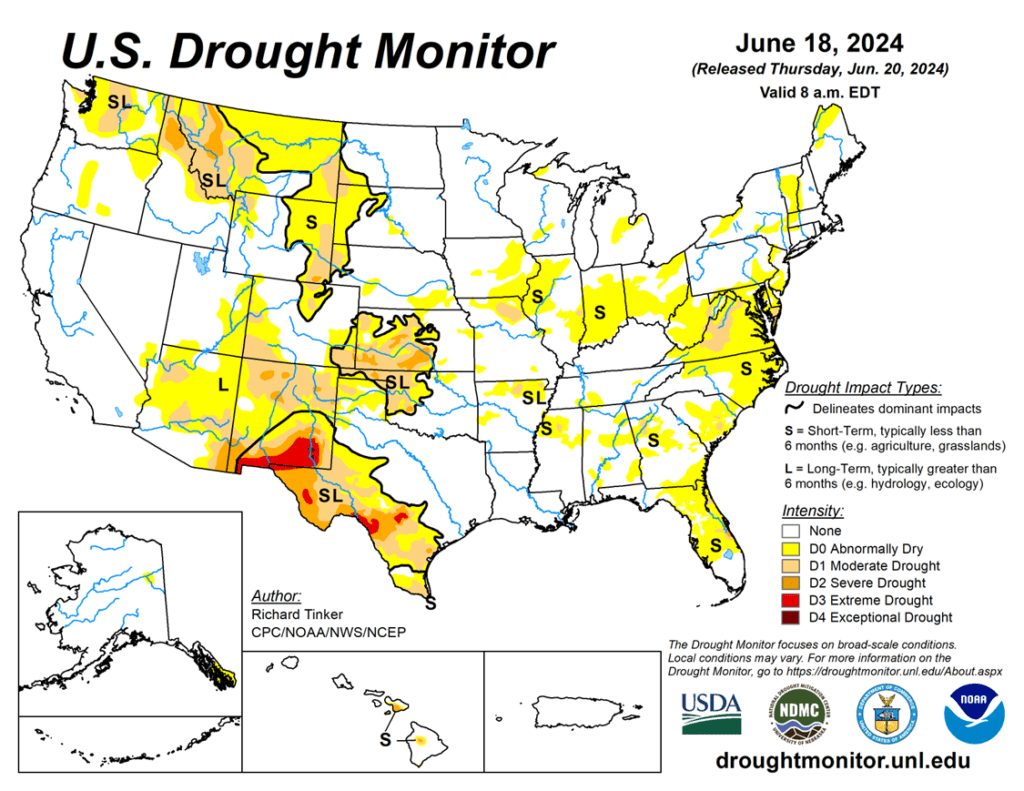

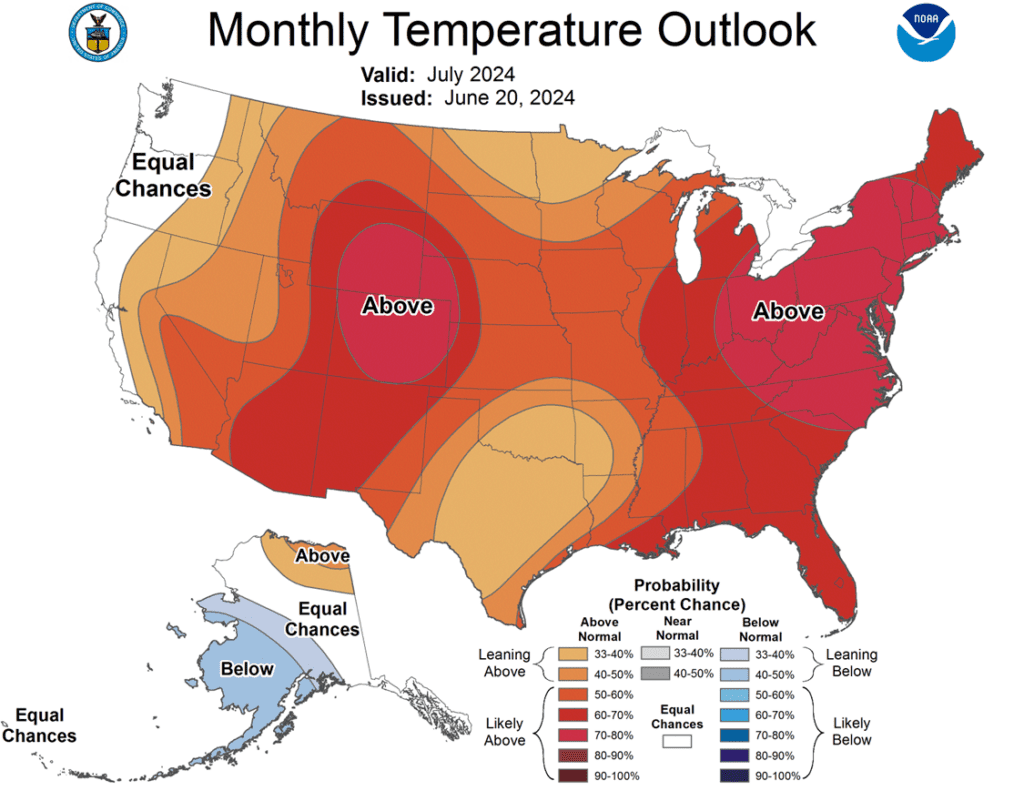

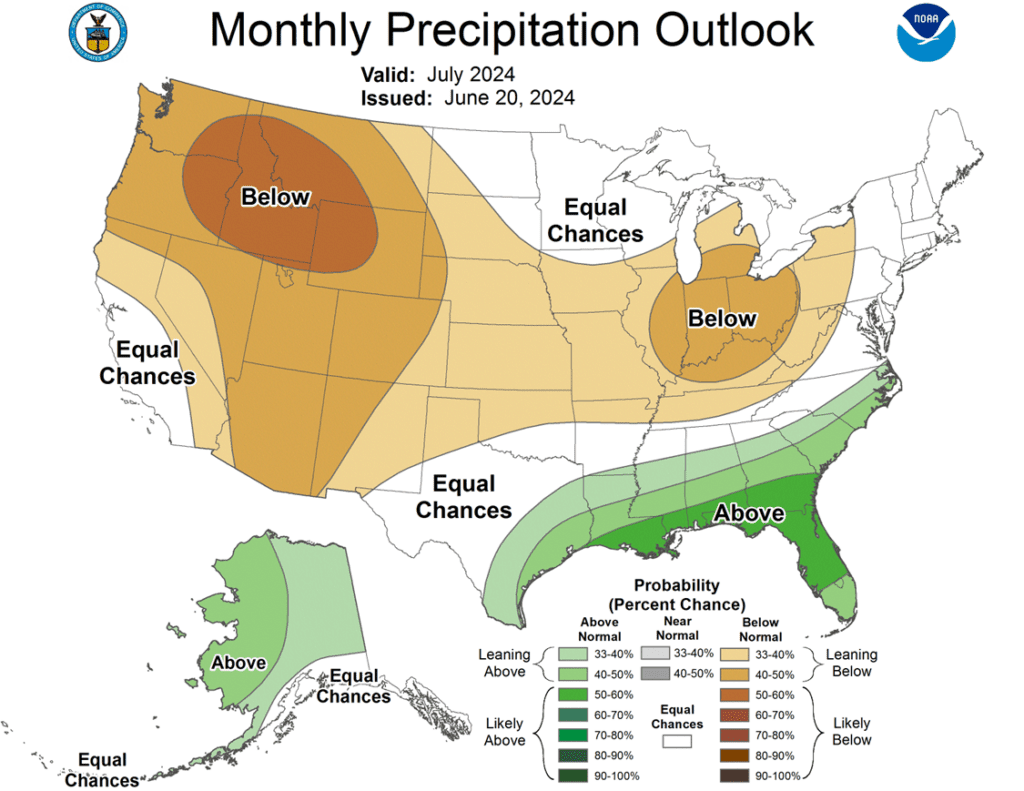

- To see the updated US Drought Monitor, and the updated US July Monthly Temperature and Precipitation Outlooks, courtesy of NOAA and the Weather Prediction Center, and UNL scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

New Alert

Sell SEP ’24 Cash

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

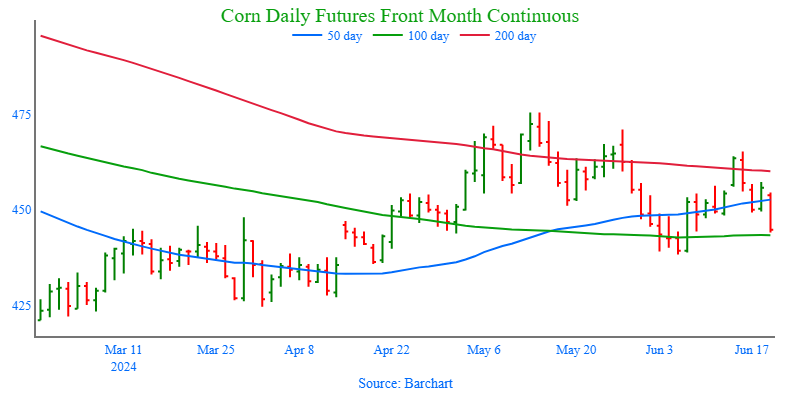

Since mid-April, the front month corn market has been in a broad trading range bound mostly by 435 on the bottom and 475 up top. While solid demand has been a prominent supportive feature of the market along with US and South American weather, an old crop carryout near 2.0 billion bushels and the prospect of an even higher carryout number for new crop, has kept upside rallies in check. The 2024 growing season is still young with lots of potential ahead as weather remains the dominant market mover.

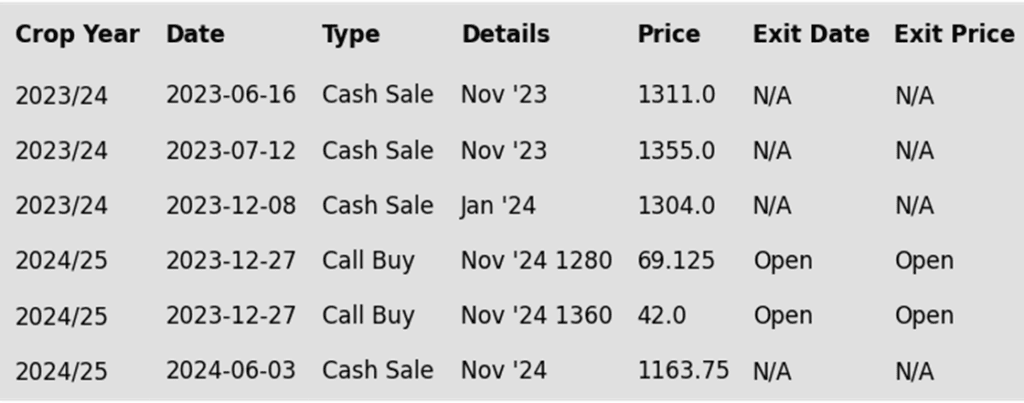

- Grain Market Insider recommends selling a portion of your 2023 corn crop. With no bullish surprises in last week’s WASDE report and a relatively benign 8–14-day weather outlook, we are recommending selling the last of the old crop corn here. The risk of a lower trend into month’s end looks to be increasing. Then on the 28th of June, we have the uncertainty of the Grain Stocks and Acreage reports, which is one of the most volatile report days of the year. If that report day ends up being overall bearish, we’ve seen before where the market can shed 3% or more of its price. So given all these factors, and that we try not to carry old crop bushels past mid-July, we are making what will be our last sales recommendation for the 2023 corn crop at this time.

- No new action is recommended for 2024 corn. After the Dec ’24 contract posted a bearish key reversal in mid-May, we implemented our Plan B stop strategy and advised making additional sales considering we are in the time of year when changes in weather, actual or perceived, can move the market swiftly in either direction. Also considering the volatility that this time of year can bring, our current strategy is to have several targets in place to provide both upside coverage as well as downside. While targeting 520 – 540 to recommend additional sales versus Dec ’24, we are targeting the 510 – 520 area to buy puts on any production that cannot be priced ahead of harvest. We are also targeting a close below 451 in Dec ’24 to buy upside calls for their value to protect any existing or future new crop sales.

- No new action is currently recommended for 2025 corn. As we move through the growing season with its potential for high volatility, we are looking for higher prices and anticipate issuing two more sales recommendations before the beginning of September. Also given the tendency for the growing season to provide some of the best pricing opportunities for the next crop year we will also be watching the calendar along with price action to make additional recommendations.

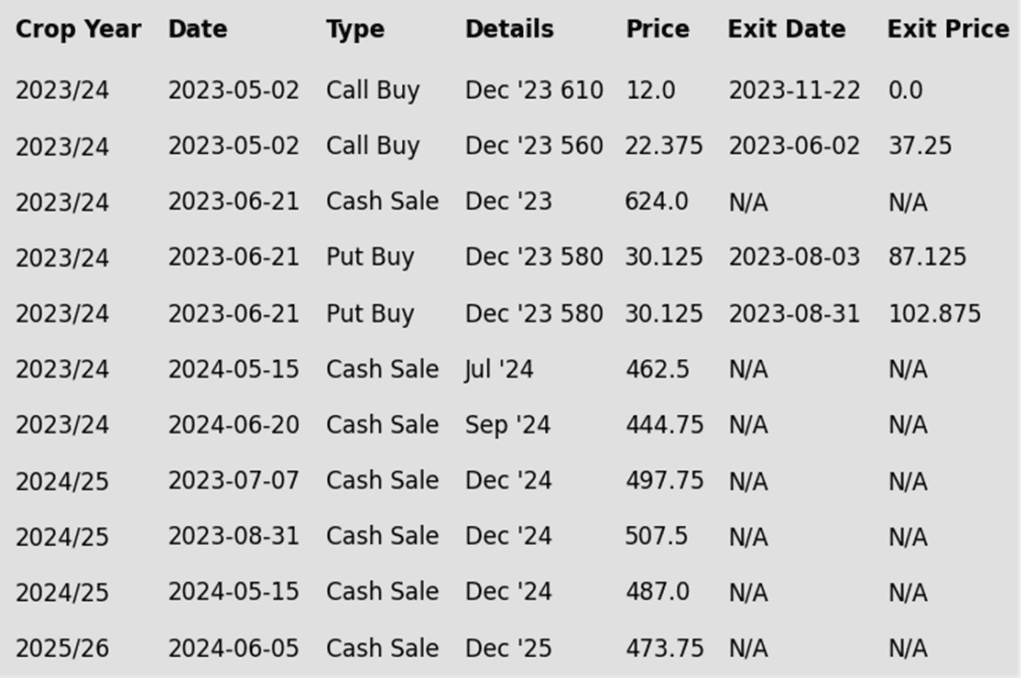

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- The corn market turned sellers following the Juneteenth holiday on prospects of a high yielding crop from a relatively strong start to the growing season. The market also likely saw additional technical selling after breaking support at the 100-day moving average on the daily continuous charts.

- One private group is currently estimating US corn yield for the 2024 crop at 181 bpa, in line with the USDA’s current forecast and ahead of last year’s 177 bpa. While not all states’ yields are estimated to be higher, states like Minnesota and Nebraska are projected to be well above last year’s.

- For the months of July and August, US corn export FOB premiums are currently an 8 – 10 cent discount versus those from Brazil which could help improve US exports. Though not as large a player, Argentina’s corn export premiums remain the cheapest.

- Localized flooding is likely in areas of Minnesota and parts of the Dakotas, with an additional 3-5 inches of rain expected over the next few days. Meanwhile, the eastern Corn Belt is forecasted to experience highs in the 90s with some areas in the 70s overnight and limited rainfall over the next couple of weeks. Additionally, the European weather model indicates much lower humidity compared to the American model, suggesting less moisture in the air and potentially less rainfall than predicted by the American model.

Above: The corn market appears to be holding support in the 440 – 435 area and could test overhead resistance between 471 and 475 ½ if additional bullish input enters the scene. If prices close below 435 they could then be at risk of trading toward the 427 – 424 support area.

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

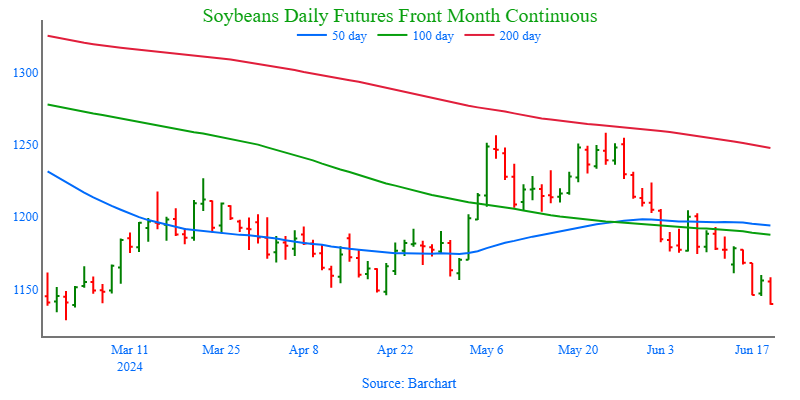

Since trading toward the 200-day moving average and peaking near 1260, front month soybeans have been on the decline and appear on track to test the February low around 1128. Though domestic crush demand has been good, export demand has lagged, and like corn, the prospect of a higher 24/25 carryout looms, adding overhead resistance to prices. With much of the growing season in front of the market, a weather-related issue or surge in demand appear to be the most likely catalysts to push prices back near their recent highs.

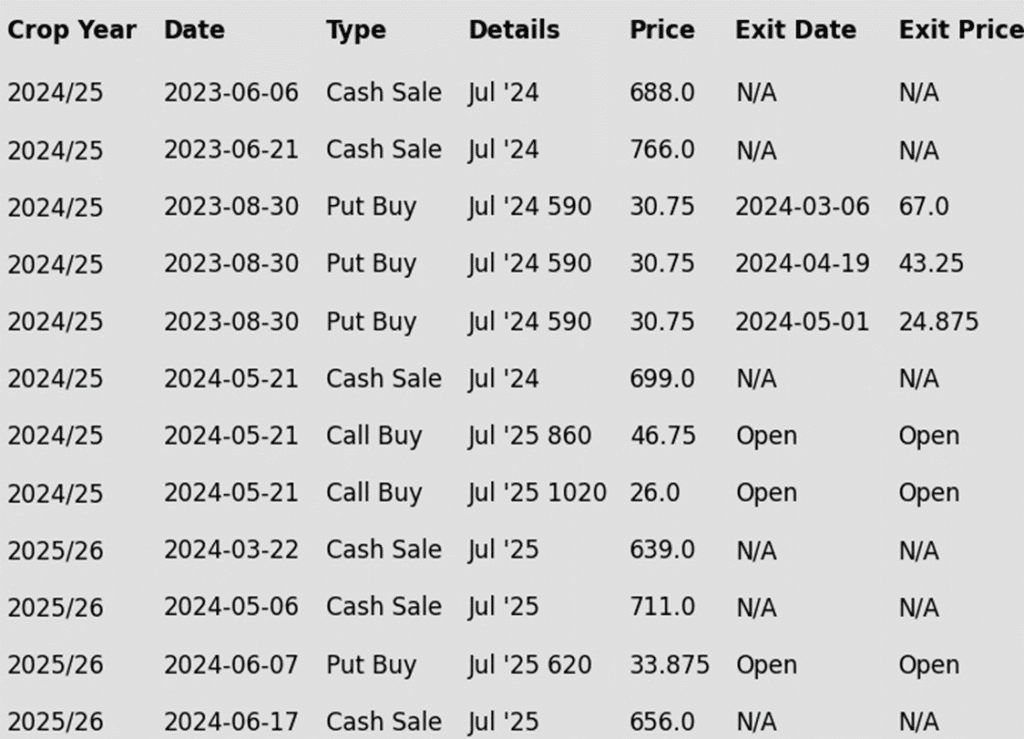

- No new action is recommended for 2023 soybeans. As we progress into the 2024 growing season, time is becoming limited to market the remaining 2023 old crop inventory. Although we are currently targeting a rebound to the 1275 – 1325 area versus Aug ’24 futures as our Plan A strategy, for what will likely be our final sales recommendation for the 2023 crop, we also don’t want to carry old crop inventory past mid-July due to seasonal weakness. Taking this into consideration, if the market does not present the opportunity to make sales at our Plan A target, our Plan B strategy will be to issue our final sales recommendation sometime in mid-July.

- No new action is recommended for the 2024 crop. At the end of December, we recommended buying Nov ’24 1280 and 1360 calls due to the amount of uncertainty in the 2024 soybean crop and to give you confidence to make sales and protect those sales in an extended rally. Given that the market has retreated since that time, we are targeting the mid-1200s versus Nov ’24 futures to exit 1/3 of the 1280 calls to help preserve equity. Most recently we employed our Plan B strategy with the close below 1180 in Nov ’24 and recommended making additional sales due to the potential change in trend. With the growing season still ahead of us, should the market turn back higher, we continue to target the 1280 – 1320 range from our Plan A strategy to make additional sales.

- No Action is currently recommended for 2025 Soybeans. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans closed sharply lower in a day of poor trade across the ag complex. November soybeans took out this past February’s low as well as the low made in May of last year to post the lowest close since August of 2021. Pressure came from rain expected in the nearby forecast despite the extended forecast showing some heat and dryness. Both soybean meal and oil closed lower with meal leading the way down.

- Chinese imports of soybeans from the US jumped in May and were up 156% from the same period a year ago. China purchased 1.27 mmt of soybeans from the US as Brazilian supplies shrink due to the flooding in the southern region of the country. Overall, China has been attempting to become more resource independent which could hurt demand in the future.

- The weekly export sales report will be delayed until tomorrow due to the holiday week, but estimates are for soybean sales to be in between the range of 500k to 750k metric tons. It is likely that China will be a top buyer as they have made multiple purchases recently that have shown up in flash sales.

- Earlier this week, the NOPA crush report showed a crush number that was way above the average trade guesses, but the market did not react which points to trade that is focused on the weather. Crush demand should continue to be strong thanks to crush margins that have become more profitable in the past few weeks.

Above: The sharp drop on June 16 brought the soybean market to test support near 1146. Should this area hold, and prices recover, they could then test the 1190 – 1200 area. Otherwise, they remain at risk of testing the 1130 – 1125 area.

Wheat

Market Notes: Wheat

- Wheat posted double-digit losses in all three US classes with little fresh news to offer bullish support. A higher US Dollar today, and another lower close for Matif wheat futures also did not help the situation, with those contracts at six-week lows.

- Wheat remains technically oversold in all three categories. This could indicate that a bottom is near, but with harvest pressure on the winter crops and falling European values, it may be difficult for US wheat to rally in any significant manner in the near term.

- Sov Econ has estimated Russia’s 2024 grain production at 127.4 mmt, down from 144.9 the year prior. This should be supportive to prices and may reflect the frost damage and drought conditions. However, some analysts are now estimating the Russian wheat crop at 82 mmt (up from 80) which is bearish.

- Monsoon rains in India should bring relief to grain growing regions in the north over the next few days. However, India will still likely need to import wheat to rebuild their reserves. In related news, India is said to have increased their domestic wheat prices in an effort to stimulate more production (which would ultimately reduce their need for imports).

- Ukraine’s 23/24 grain exports have reached 49.3 mmt as of June 19, which is up from 47.5 mmt a year ago. Of that total, 18.1 mmt is wheat, but the majority is corn at 28.2 mmt. In addition, Ukraine’s government has said the 2023 harvest totaled 81 mmt of grains and oilseeds, but the 2024 harvest could fall to 77 mmt.

Action Plan: Chicago Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

Active

Sell JUL ’25 Cash

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Chicago Wheat Action Plan Summary

Since rallying nearly 200 cents from the March low to the May high, largely on fund short covering from Russian crop concerns and dryness in the southwestern Plains, prices have fallen from their peak with seasonal weakness and the onset of harvest. Although the market is showing signs of weakness, it is also becoming oversold, which can be supportive in the event prices turn back higher, and the recent breakout above the December highs suggests there is potential for a test of the 2023 summer highs post-harvest.

- No new action is currently recommended for 2023 Chicago wheat. Any remaining 2023 soft red winter wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 Chicago wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Chicago wheat. Considering the recent rally in wheat, we recommended taking advantage of the elevated prices to make additional sales and buy upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 740 – 760 versus Sept ’24 to recommend further sales and to target a selling price of about 73 cents in the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- Grain Market Insider sees a continued opportunity to sell a portion of your 2025 SRW wheat crop. Support around 667 in the July ’25 Chicago wheat contract has been broken. Since peaking in May, the market has retraced over 50% back toward the March low, suggesting that our Plan A upside targets are now less likely to be achieved and prices may trend lower. Taking this into consideration, Grain Market Insider is implementing a Plan B Stop strategy and recommends selling another portion of your 2025 SRW wheat crop at this time.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

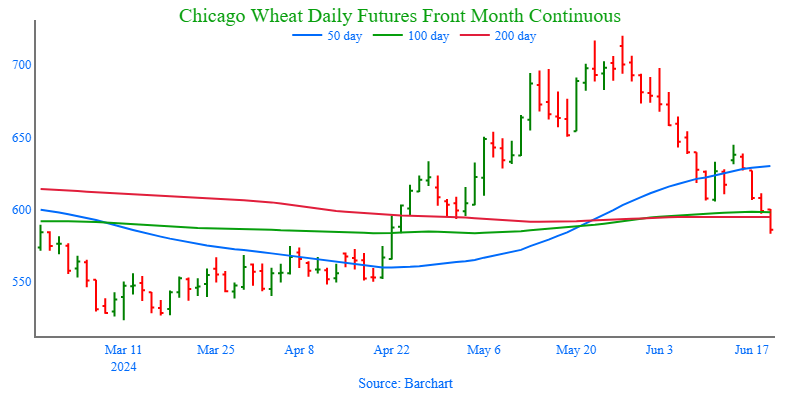

Above: Chicago wheat has been on a slide since late May and is on track to test the 600 – 593 support area from late April, while also showing signs of being oversold. Being oversold can be supportive to a higher move back towards the 650 resistance area if 600 – 593 support holds. If not, the next major support area may come in between 550 and 520.

Action Plan: KC Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

Active

Sell JUL ’25 Cash

Puts

2023

No New Action

2024

No New Action

2025

No New Action

KC Wheat Action Plan Summary

Between the end of February and the middle of April, KC wheat was mostly rangebound between the mid-590s on the topside and mid 550s down low, with little to move prices higher, all the while Managed funds continued adding to their large net short positions. Toward the end of April, dryness in the Black Sea region and the US HRW growing areas started becoming more concerning and triggered a short covering rally across the wheat complex, driving prices to levels not seen in over six months. Although US wheat exports continue to struggle to compete on the world market, which can keep a lid on US prices, the recent breakout above resistance from the December highs suggests there is potential for a test of the highs from last summer.

- No new action is recommended for 2023 KC wheat. Any remaining 2023 hard red winter wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 KC wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 KC wheat. Considering the recent upside breakout in KC wheat, we recommended buying upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 780 – 810 versus Sept ’24 to recommend further sales and to target a selling price of about 71 cents on the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- Grain Market Insider sees a continued opportunity to sell a portion of your 2025 HRW wheat crop. Support near 663 in the July ’25 KC wheat contract has been broken. Since peaking in May, the market has retraced over 50% toward the March low, suggesting that our Plan A upside targets are now less likely to be achieved, and prices may trend lower. Taking this into consideration, Grain Market Insider is implementing a Plan B Stop strategy and recommends selling another portion of your 2025 Hard Red Winter wheat crop at this time.

To date, Grain Market Insider has issued the following KC recommendations:

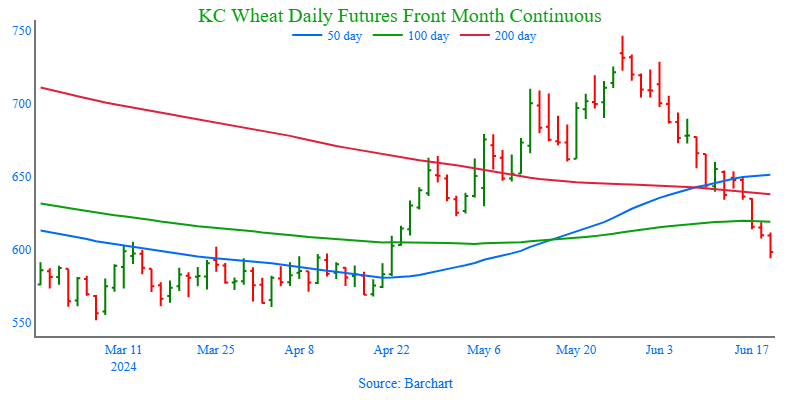

Above: The break through 625 – 620 support suggests that prices may be on track back toward the 570 – 550 support area from earlier this year, though the market may encounter psychological support around 600. If a bullish impetus enters the scene to turn prices back higher, overhead resistance could be found near 650 – 660.

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

From mid-February through most of April, Minneapolis wheat traded mostly sideways to lower, lacking significant bullish fundamental news to drive prices upward. However, in late April, spurred by concerns over the world wheat crop and dry conditions in the HRW growing regions, Minneapolis wheat experienced a rally back towards last fall’s highs. Despite lingering obstacles for the US wheat market, the recent rally above resistance from last winter’s highs suggests there is potential for an extended rally toward summer 2023 highs.

- No new action is recommended for 2023 Minneapolis wheat. Any remaining 2023 spring wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 Minneapolis wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Minneapolis wheat. With the recent close below the 712 support level, Grain Market Insider implemented its Plan B stop strategy, recommending additional sales for the 2024 crop due to waning upside momentum and an increased likelihood of a downward trend. Given the heightened volatility and the amount of time that remains to market this crop, we will maintain the current July ’25 KC wheat 860 and 1020 call options. Our target is a selling price of about 71 cents for the 860 calls to achieve a net neutral cost on the remaining 1020 calls. These 1020 calls will continue to protect existing sales and provide confidence to make additional sales at higher prices.

- No new action is currently recommended for the 2025 Minneapolis wheat crop. Given the volatility in the wheat market, we recently recommended buying July ’25 620 KC wheat puts to provide downside coverage for the 2025 crop due to their greater liquidity and high correlation to Minneapolis wheat. Moving forward, we will target a value of 60 cents (double the original approximate cost) in the July 620 puts to exit half of the original position, leaving the remainder to continue providing downside coverage with a net neutral cost if the market moves higher. Grain Market Insider may also start considering the first sales targets after July 1.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

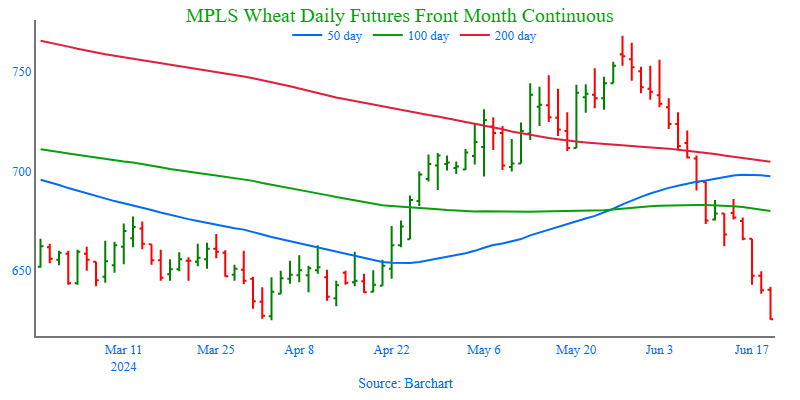

Above: With the recent lower trend, the market appears on track to test support in the 663 – 625 congestion area. Should that level hold with a rebound in prices, overhead resistance could be encountered near 685. If not, further support may be found near 600.

Other Charts / Weather