6-13 End of Day: Grains Rally on Geopolitical Tensions and Biofuel Boost

All Prices as of 2:00 pm Central Time

| Corn | ||

| JUL ’25 | 444.5 | 6 |

| DEC ’25 | 443 | 2.5 |

| DEC ’26 | 471.5 | 1 |

| Soybeans | ||

| JUL ’25 | 1069.75 | 27.5 |

| NOV ’25 | 1054.75 | 27.5 |

| NOV ’26 | 1072.25 | 21 |

| Chicago Wheat | ||

| JUL ’25 | 543.75 | 17.25 |

| SEP ’25 | 559.25 | 17.5 |

| JUL ’26 | 616.25 | 15.25 |

| K.C. Wheat | ||

| JUL ’25 | 540.75 | 18 |

| SEP ’25 | 555 | 17.5 |

| JUL ’26 | 613 | 15.75 |

| Mpls Wheat | ||

| JUL ’25 | 634.25 | 13.5 |

| SEP ’25 | 645.25 | 13.5 |

| SEP ’26 | 682.25 | 9.75 |

| S&P 500 | ||

| SEP ’25 | 6037.5 | -65.5 |

| Crude Oil | ||

| AUG ’25 | 71.88 | 5.24 |

| Gold | ||

| AUG ’25 | 3456.7 | 54.3 |

Grain Market Highlights

- 🌽 Corn: Corn futures ended the week mixed as geopolitical tensions in the Middle East and a surge in crude oil triggered short covering, while strong export demand and bullish biofuel blending targets added support. However, favorable crop weather and anticipation of the upcoming Planted Acreage report provide upside resistance.

- 🌱 Soybeans: Soybeans rallied sharply into the weekend, driven by stronger-than-expected biomass diesel quotas that lifted biofuel demand prospects and pushed prices toward key resistance levels. Support also came from expectations for a solid NOPA crush report, while upcoming Midwest rainfall added upside resistance.

- 🌾 Wheat: Wheat futures surged to end the week, fueled by spillover strength from soybeans and geopolitical tensions after Israel’s reported strike on Iran, prompting short covering and risk-driven buying. Rising drought concerns in U.S. wheat regions and ongoing planting progress in Argentina also added underlying support.

- To see the updated U.S. weather outlook maps, scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Eight sales recommendations made to date, with an average price of 494.

- Changes:

- None.

2025 Crop:

- Plan A:

- Exit all 510 December calls @ 43-5/8 cents.

- Exit half of the December 420 puts @ 43-3/4 cents.

- Exit one-quarter of the December 420 puts if December closes at 411 or lower.

- Roll-down 510 & 550 December calls if December drops to 399.

- Plan B: No active targets.

- Details:

- Sales Recs: Seven sales recommendations have been made to date, with an average price of 461.25.

- Changes:

- None.

- Volatility-Ready: Positioned well for potential market swings, with a solid base of sales and open call and put option positions in place. Active targets remain set to begin legging out of options and roll down call options to lower strikes as conditions warrant.

2026 Crop:

- CONTINUED OPPORTUNITY – Sell a fourth portion of your 2026 corn. The December ‘26 contract has reached the upside target of 474.

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Now four sales recommendations have been made to date, with an average price of 462.

- Changes:

- None.

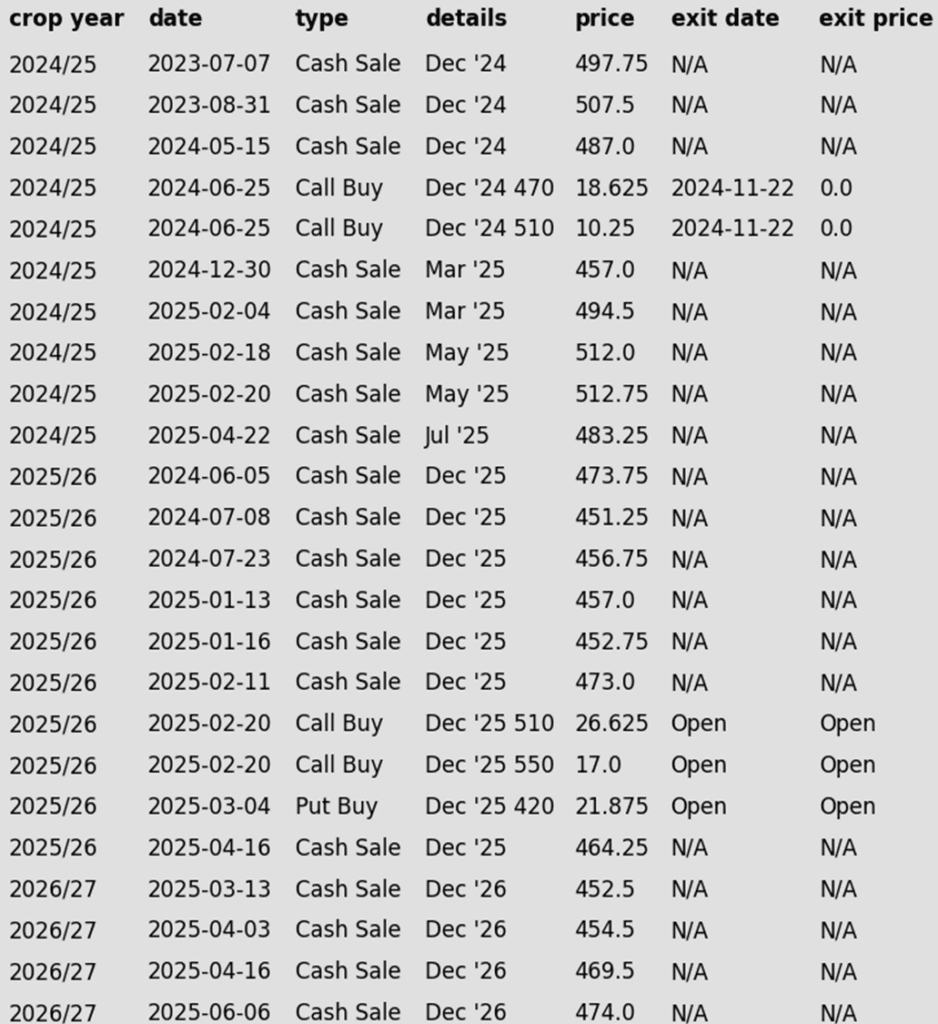

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Money flowed into the grain markets to end the week, and corn futures followed as futures traded higher to end the week. July futures traded 2 cents higher on the week, breaking a two-week losing streak. December corn finished the week 6 ¼ cents lower.

- Geopolitical tensions added uncertainty to the markets as Israel launched an attack against Iranian nuclear sites during the overnight. The crude oil market traded sharply higher and helped trigger some short covering in the corn market. Traders will be watching the headlines closely over the weekend to see if there will be any escalation in the conflict.

- July futures saw additional short covering and follow-through buying after Thursday’s close and supportive USDA report. Old crop corn carryover is at 1.365 BB, supported by strong export demand for U.S. corn. Expectations are for the carryout number to be tightened in future reports as current export sales are at 96% of the market year total on the day of the June report.

- Strong buying in the soybean market helped support corn futures with the announcement of the EPA on the biofuels blending mandate targets. The blending target came in higher than expected at 5.6 billion gallons for 2026 and 5.86 billion gallons for 2027. This is up significantly from the current target of 3.35 billion gallons for 2025. Soybean oil traded the price limit higher on the session, fueling the soybean rally.

- The corn market will be focused on global headlines and weather going into the end of June. Forecasts are staying favorable for crops during this time frame, limiting the corn rally potential. The June Planted Acreage report is 17 days away and will be the report likely to set the direction of the corn market into the summer months.

Corn Futures Finish at the Top End of a Nine-Day Trading Range

The front-month July contract continues to trade within a tight range, mostly between 434 and 446. A close above 446 would open the door to the next upside opportunity at 465. On the downside, support sits at the June 10 bullish reversal low of 429.25. A close below that level would make 408 the next downside risk to watch.

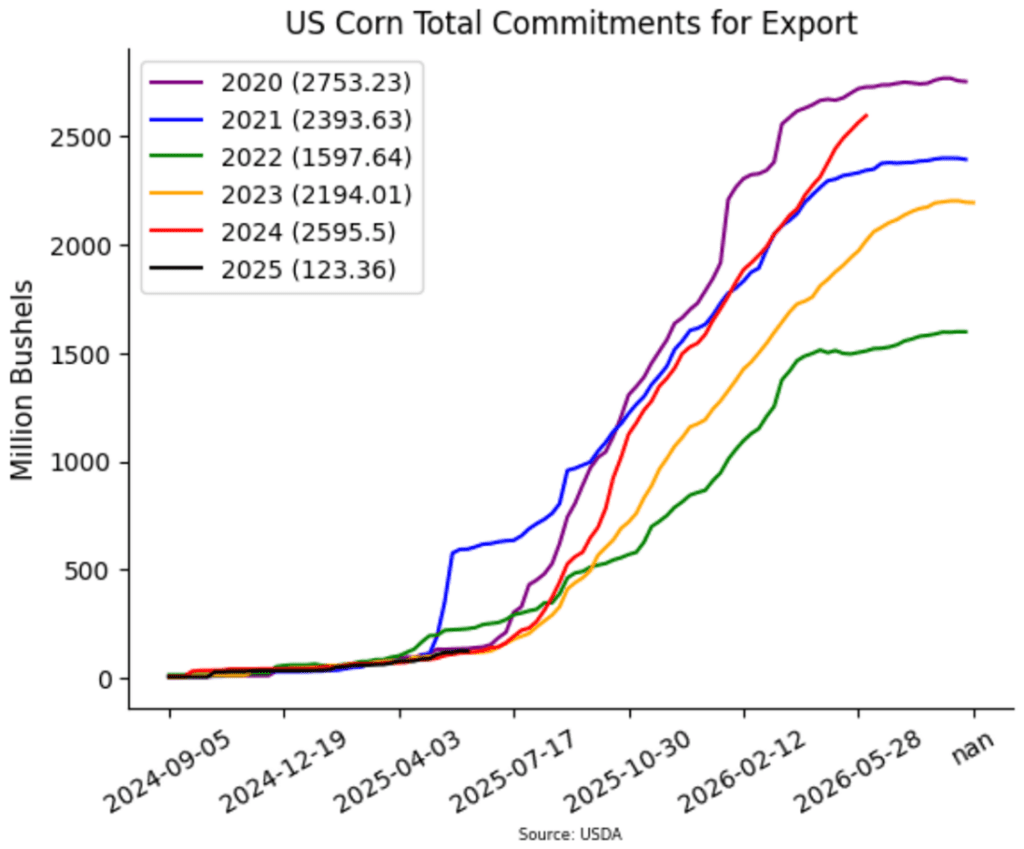

Above: From USDA – US corn total export commitments for 2020 (purple), 2021 (blue), 2022 (green), 2023 (orange), 2024 (red), and 2025 (black).

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: Next cash sale at 1107 vs July.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made to date, with an average price of 1089.

- Changes:

- No Changes (for Now): Despite last week’s break of 1036.50 support, the 1107 target remains active to recommend making the next sale.

2025 Crop:

- CONTINUED OPPORTUNITIES – Buy January ‘26 1040 put options for approximately 49 cents in premium, plus fees and commission.

- Plan A:

- No active sales targets.

- Exit one-third of 1100 call options at 1085 vs November.

- Exit remaining two-thirds of 1100 November call options at 88 cents.

- Plan B:

- No active targets.

- Details:

- Sales Recs: Now two sales recommendations made to date, with an average price of 1040.25.

- Changes:

- None.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- Changes:

- None.

- We’re now in the seasonal window where first sales targets for next year’s crop could post at any time. Stay tuned.

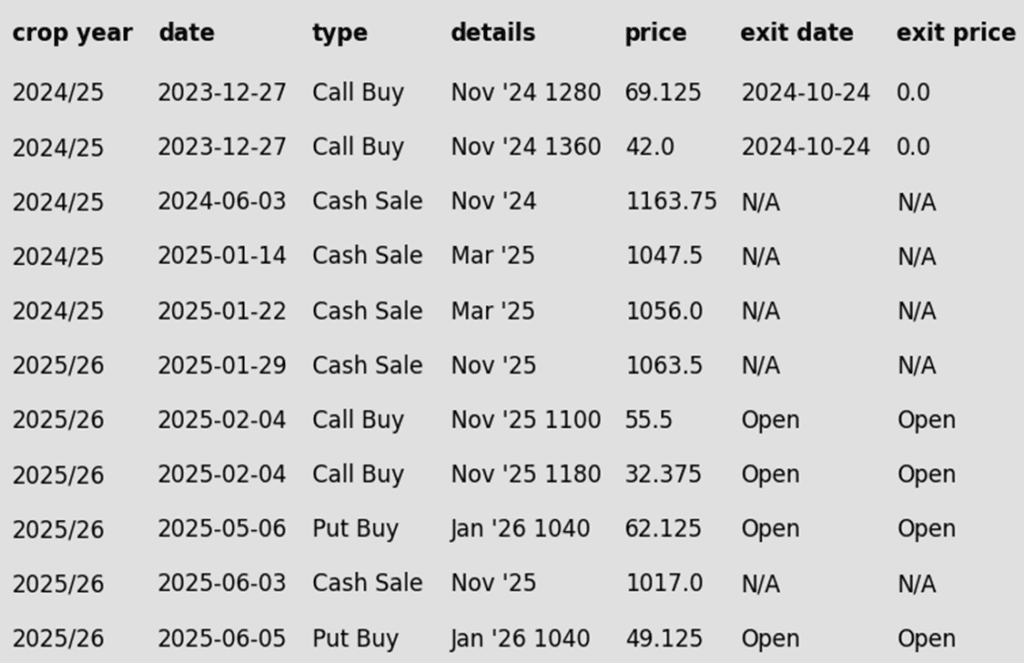

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans closed substantially higher heading into the weekend after new biomass diesel quotas came in higher than previously rumored. The November contract will now look to break above the first resistance level around $10.60 with the second resistance around $10.65 after today’s newfound strength.

- The Renewable Fuels Association released the new biomass quotas today, which now stand to be 3.35 billion gallons for 2025, 5.61 billion gallons for 2026, and 5.86 billion gallons for 2027.

- The Buenos Aires Grain Exchange slightly bumped their soybean production estimate for Argentina to 50.3 mmt, up from their previous estimate of 50 mb. The group also pegged soybean harvest in the country at 93.2% done.

- Monday will be the release of the May NOPA Crush report. Average analyst guesses are at 193.519 mb, which if realized, would be up 1.7% from the month prior and 5.4% higher than May of last year.

- Rainfall is expected over the next 7 days, with a majority of the soybean belt seeing anywhere from 0.25” to 4”. Higher totals are expected South of the I-80 line into Missouri and the Delta region.

July soybeans posts highest close since May 14

Strong weekly close, yet July still has major resistance to clear before broader upside opportunities can become more immediate possibilities. Macro trend remains sideways with resistance at the May high of 1082. A close over that resistance and the first upside objective could be the open gap on the front-month continuous chart from last June. The gap starts at 1161 and ends at 1177. If July cannot clear 1082 then rangebound to lower trade remains the risk. First support is now at 1032.50. A close below that support and the April low of 970.25 would be the next risk.

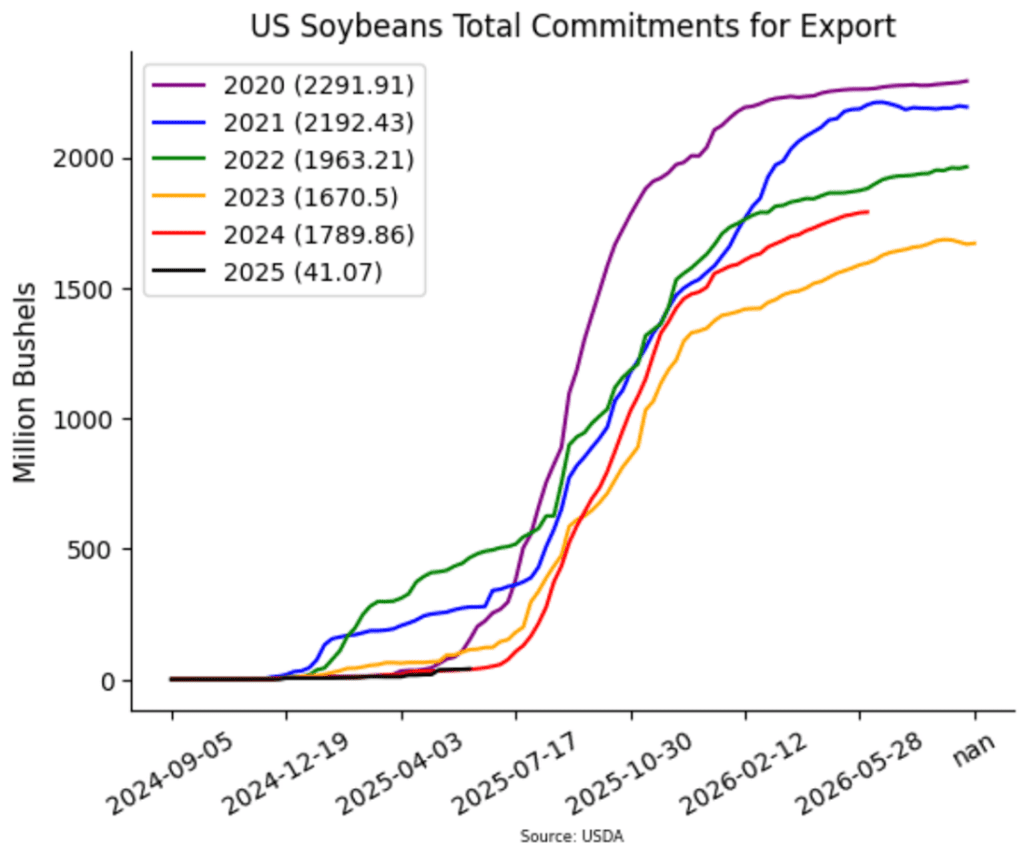

Above: From USDA – US soybean total export commitments for 2020 (purple), 2021 (blue), 2022 (green), 2023 (orange), 2024 (red), and 2025 (black).

Wheat

Market Notes: Wheat

- Wheat closed out the week sharply higher as it followed strong gains in the soy complex. Israel is reported to have launched attacks on Iran overnight, targeting their nuclear infrastructure. This led to a mix of short covering and speculative buying interest as war premium was factored back into the trade.

- As reported by the USDA, as of June 10, an estimated 15% of winter wheat acres are experiencing drought conditions, up from 12% a week ago. Drought also expanded in spring wheat areas by 1% to 20% for the same time period. At this time last year, only 3% of spring wheat acres were in drought.

- According to the Buenos Aires Grain Exchange, wheat planting in Argentina advanced 15% last week to 38.5% complete. A storm system moving across northeastern Argentina today and tomorrow should bring beneficial moisture to the newly planted wheat, but will likely delay harvest of corn and soybeans as well.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Four sales recommendations made to date, with an average price of 690.

- Changes:

- None.

- This week will likely be the final week that Grain Market Insider provides guidance on the 2024 crop before fully shifting focus to the 2025 and 2026 crops.

2025 Crop:

- Plan A: No active targets.

- Plan B:

- Buy call options if July closes over 633.50 macro resistance.

- Details:

- Sales Recs: Five sales recommendations made to date, with an average price of 646.

- Changes:

- None.

2026 Crop:

- Plan A:

- Target 675 vs July ‘26 for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: One sales recommendation made to date, at 624.

- Changes:

- New put options target added.

- Put option coverage is leveraged for early downside protection in the event of a break of support.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Finishes the Week with a Bullish Daily Reversal

The July ended a four-day losing streak, erased three days of losses, and closed back above the 50-day on the front month continuous following today’s outside bullish daily reversal. That reversal now establishes first downside support at today’s low of 522.25. A close below that support and the next downside risk would be 506.25. A lot of resistance remains above the market, yet with the recent high and 200-day at 558. A close over 558 and that could provide fuel for a bigger move towards the winter high of 621.75.

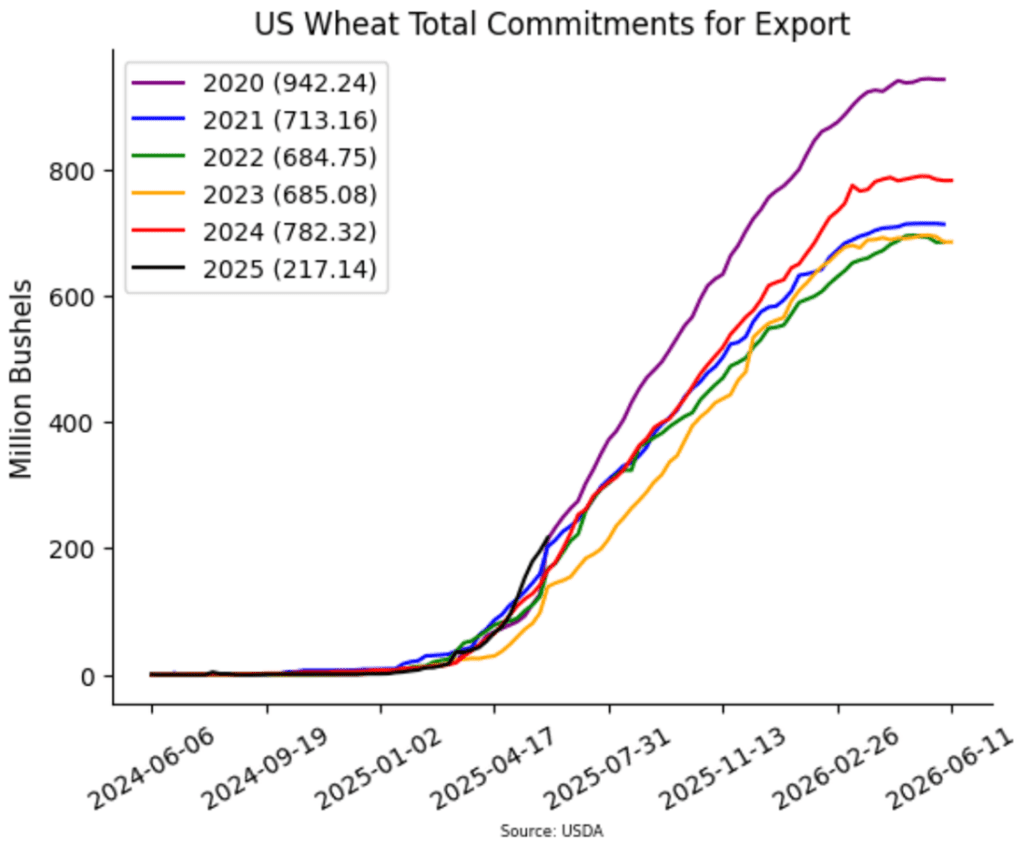

Above: From USDA – US wheat total export commitments for 2020 (purple), 2021 (blue), 2022 (green), 2023 (orange), 2024 (red), and 2025 (black).

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made to date, with an average price of 677.

- Changes:

- None.

- This week will likely be the final week that Grain Market Insider provides guidance on the 2024 crop before fully shifting focus to the 2025 and 2026 crops.

2025 Crop:

- Plan A: No active targets.

- Plan B:

- Buy call options if July closes over 653 macro resistance.

- Details:

- Sales Recs: Four sales recommendations made to date, with an average price of 639.

- Changes:

- None.

2026 Crop:

- Plan A: Target 697 vs July ‘26 to make the first cash sale.

- Plan B:

- Close below 584 support and buy July ‘26 put options (strikes TBD).

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- Changes:

- New cash sale target and new put option target.

- Given the high yield variability from year to year in Hard Red Winter wheat, put option coverage is leveraged for early downside protection in the event of a break of support.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Finds Resistance at the 50-Day

July closed right at the 50-day moving average today following a strong bullish reversal off today’s low. Closing over today’s high would make the 200-day at 567 the next immediate target.

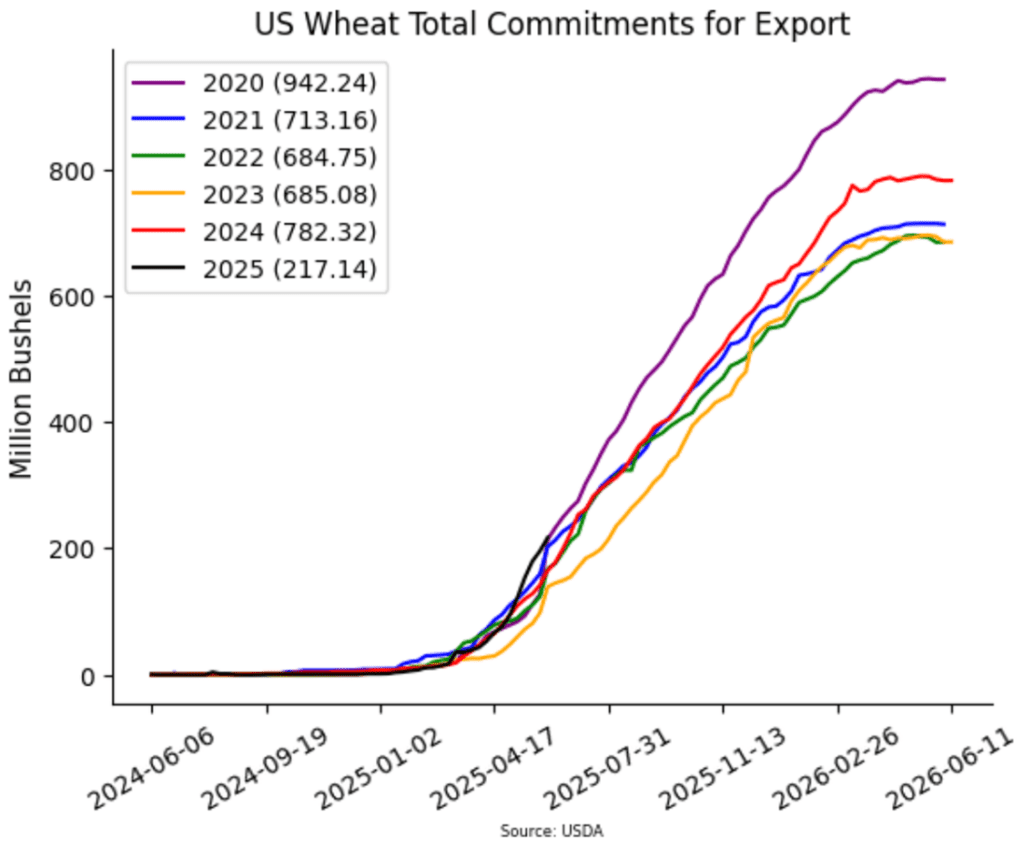

Above: From USDA – US wheat total export commitments for 2020 (purple), 2021 (blue), 2022 (green), 2023 (orange), 2024 (red), and 2025 (black).

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Now six sales recommendations made to date, with an average price of 684.

- Changes:

- None.

- This week will likely be the final week that Grain Market Insider provides guidance on the 2024 crop before fully shifting focus to the 2025 and 2026 crops.

2025 Crop:

- Plan A: No active targets.

- Plan B:

- Buy KC call options if July KC closes over 653 macro resistance.

- Details:

- Sales Recs: Five sales recommendations made to date, with an average price of 646.

- Changes:

- None.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Changes:

- None.

- None. Another few weeks before price targets may post.

- Changes:

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Retests Last Week’s High

July spring wheat futures closed just below last Friday’s close of 635.25. A close over that resistance would make 660 the next first upside target. Downside support is at this week’s low and the 200-day in the 607 area. A close below that support and the May low of 572.50 would be the first downside risk.

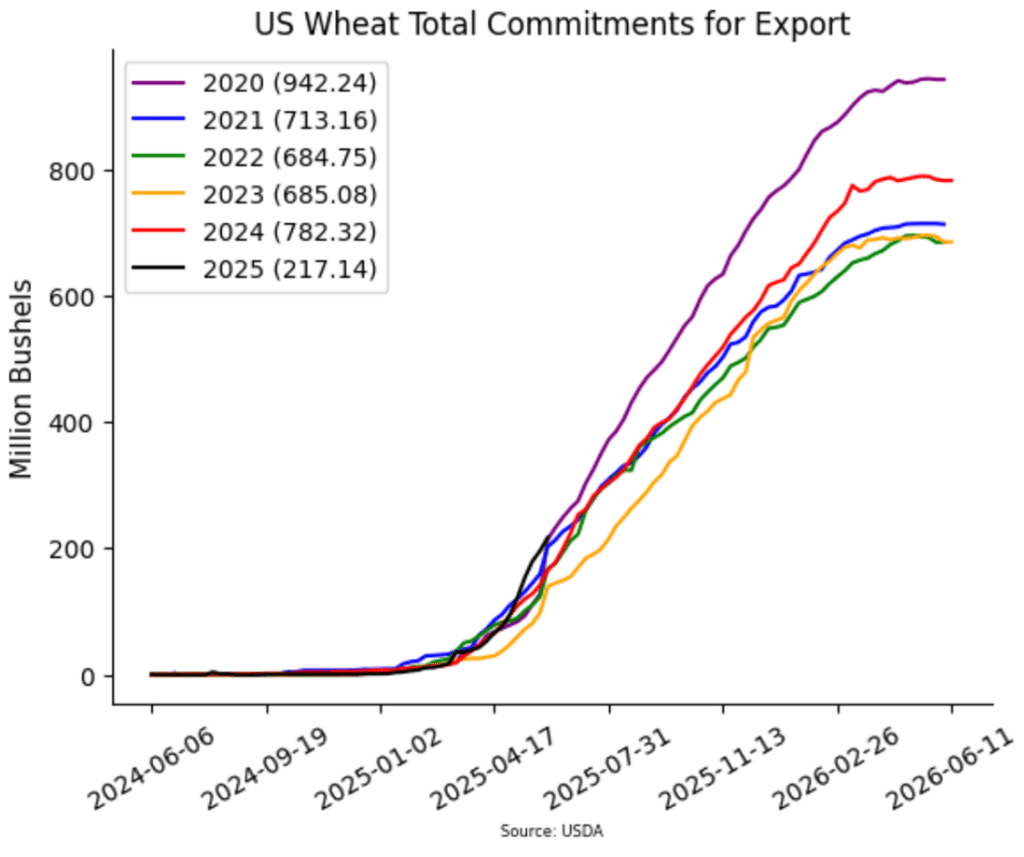

Above: From USDA – US wheat total export commitments for 2020 (purple), 2021 (blue), 2022 (green), 2023 (orange), 2024 (red), and 2025 (black).

Other Charts / Weather

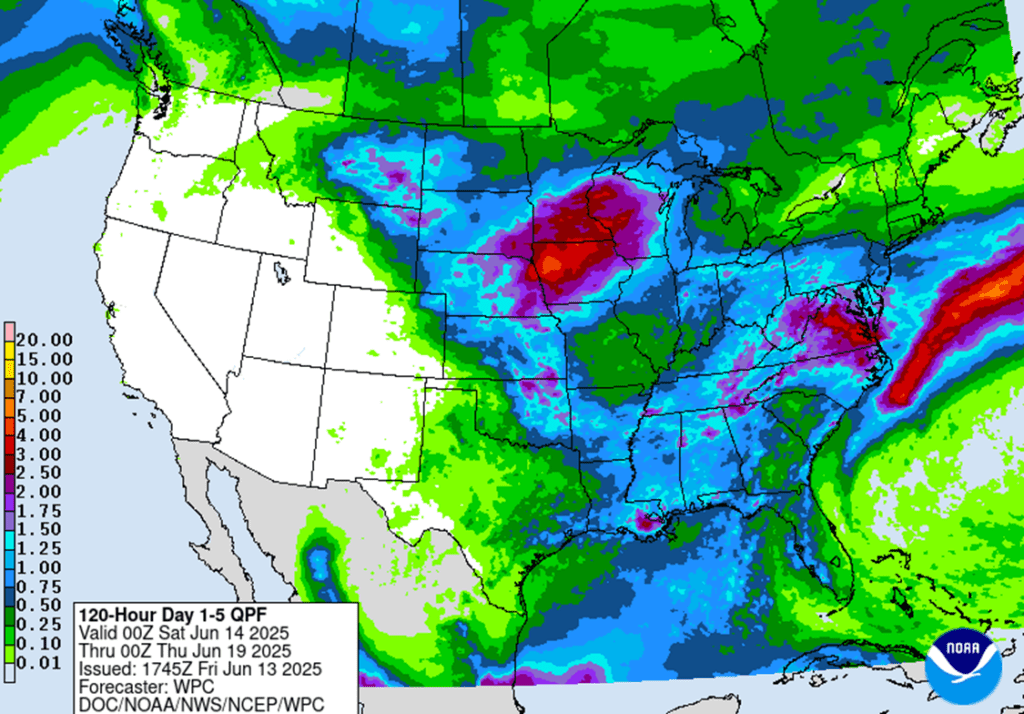

Above: US 5-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

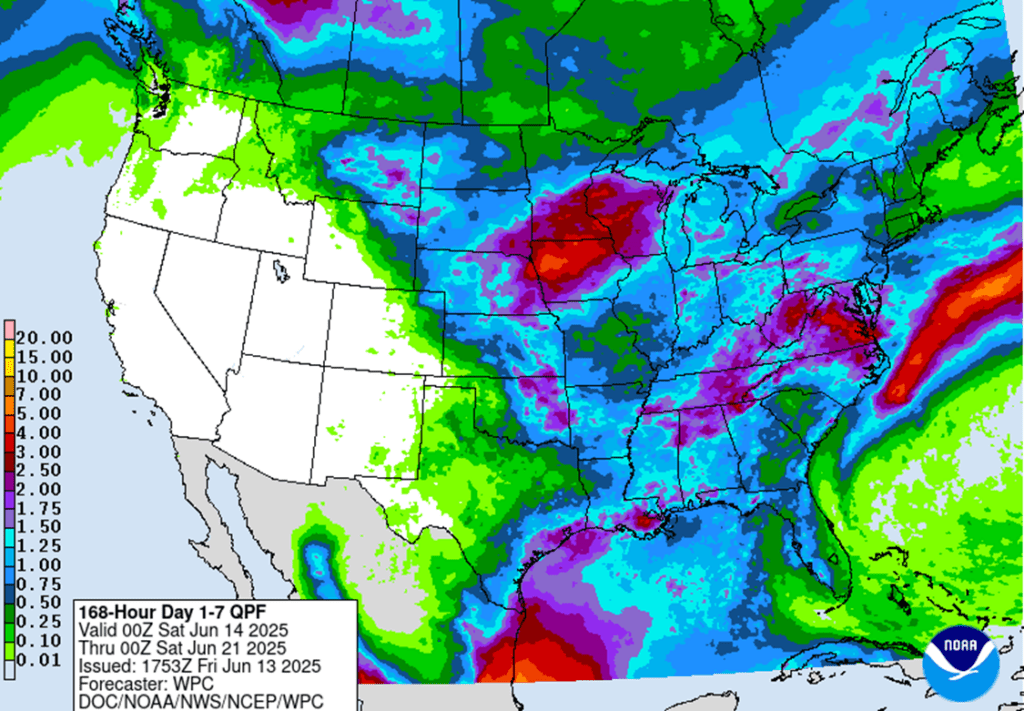

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

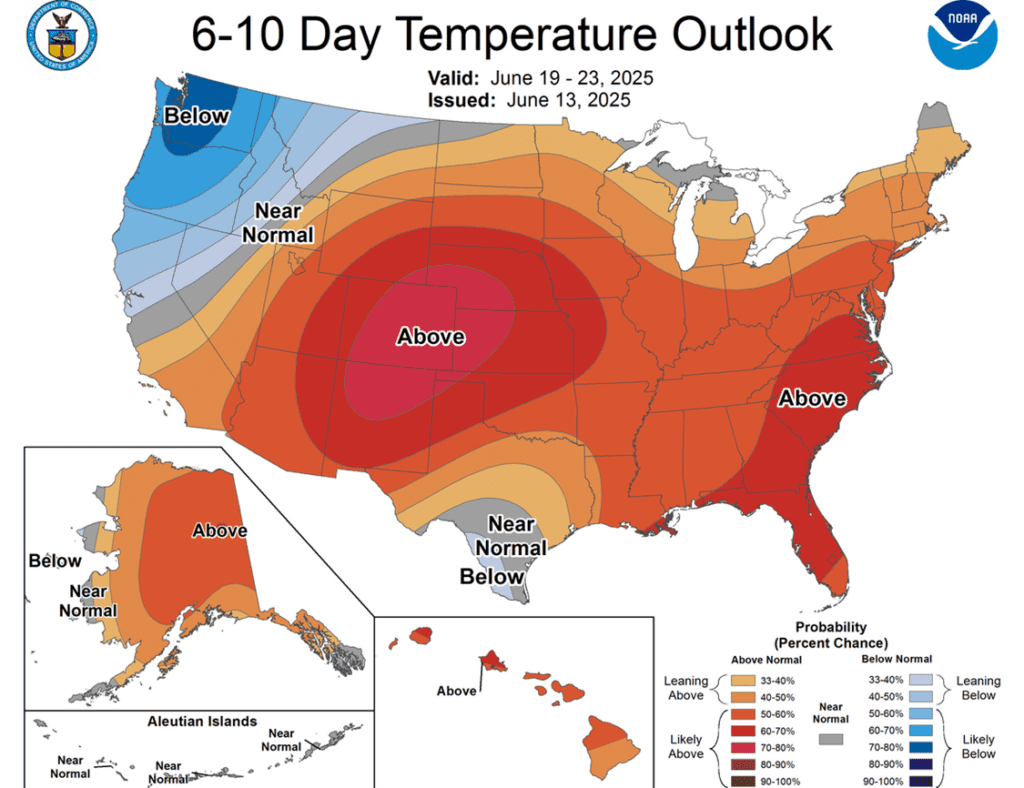

Above: US 6-10 day temperature outlook courtesy of NOAA.

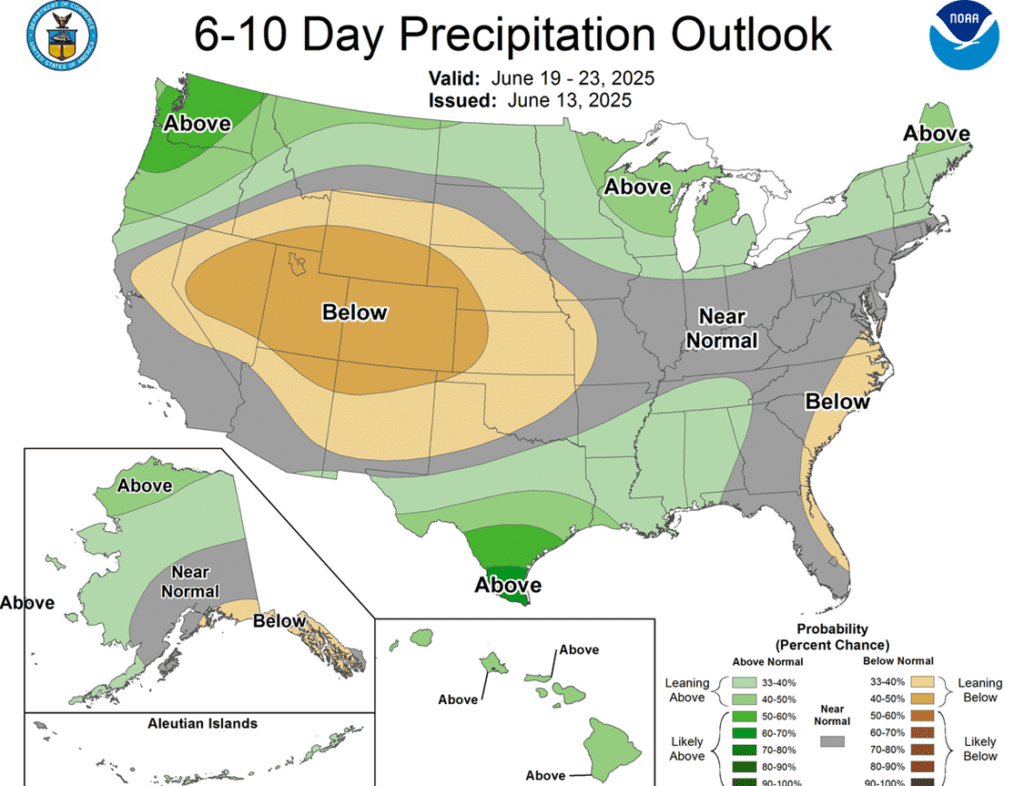

Above: US 6-10 day precipitation outlook courtesy of NOAA.