5-8 End of Day: Markets Close Lower Across the Board as They Consolidate Ahead of Friday’s Report

All prices as of 2:00 pm Central Time

| Corn | ||

| JUL ’24 | 458.5 | -8.5 |

| DEC ’24 | 481.25 | -7.25 |

| DEC ’25 | 492.75 | -4 |

| Soybeans | ||

| JUL ’24 | 1227.75 | -18.75 |

| NOV ’24 | 1213 | -15 |

| NOV ’25 | 1192.5 | -10.75 |

| Chicago Wheat | ||

| JUL ’24 | 634 | -8.75 |

| SEP ’24 | 655 | -8.75 |

| JUL ’25 | 707.25 | -8.25 |

| K.C. Wheat | ||

| JUL ’24 | 648.5 | -15.5 |

| SEP ’24 | 661.5 | -14.75 |

| JUL ’25 | 701.25 | -11 |

| Mpls Wheat | ||

| JUL ’24 | 702.75 | -16.25 |

| SEP ’24 | 708.75 | -16 |

| SEP ’25 | 711 | -5.25 |

| S&P 500 | ||

| JUN ’24 | 5211.5 | -2.25 |

| Crude Oil | ||

| JUL ’24 | 78.71 | 0.65 |

| Gold | ||

| AUG ’24 | 2343.2 | -3.4 |

Grain Market Highlights

- Talk of heavy farmer selling in both the US and South America weighed on the corn market which saw follow through selling on Monday’s loss of upward momentum. July corn futures retraced lower to settle at its 100-day moving average.

- The soybean market closed lower across the board, as traders took profits and squared positions from the recent rally ahead of Friday’s WASDE report.

- Both soybean products also settled lower today. July soybean oil reversed lower as it hit resistance at its 20-day moving average, following the sharp decline in Malaysian palm oil. Soybean meal saw another day of profit-taking, with traders likely exiting long positions ahead of Friday’s report.

- Lower Matif wheat, a stronger US Dollar, and a report from SovEcon putting Russia’s April wheat stocks 65% ahead of the historical average likely triggered a round of profit taking the wheat complex, pressuring prices lower in all three classes.

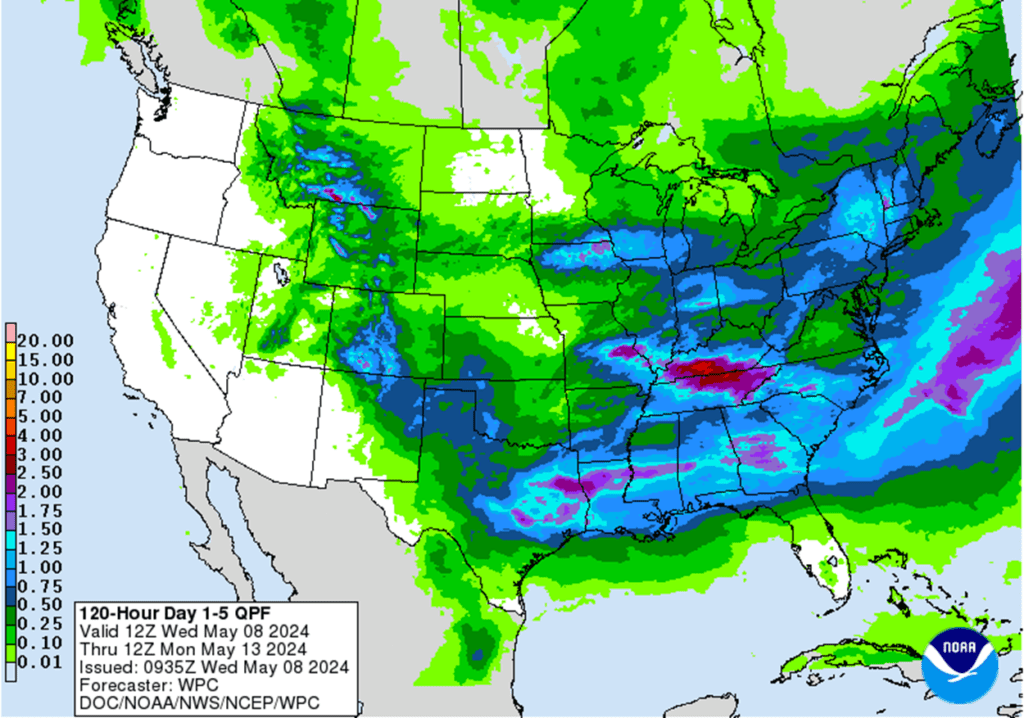

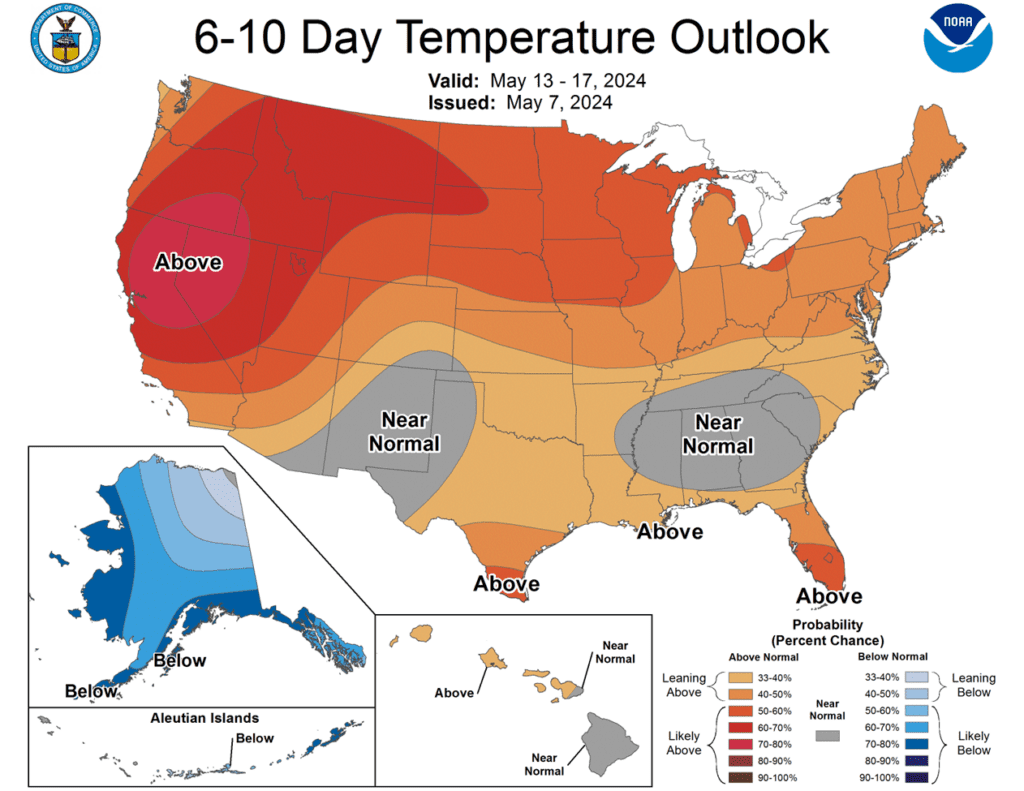

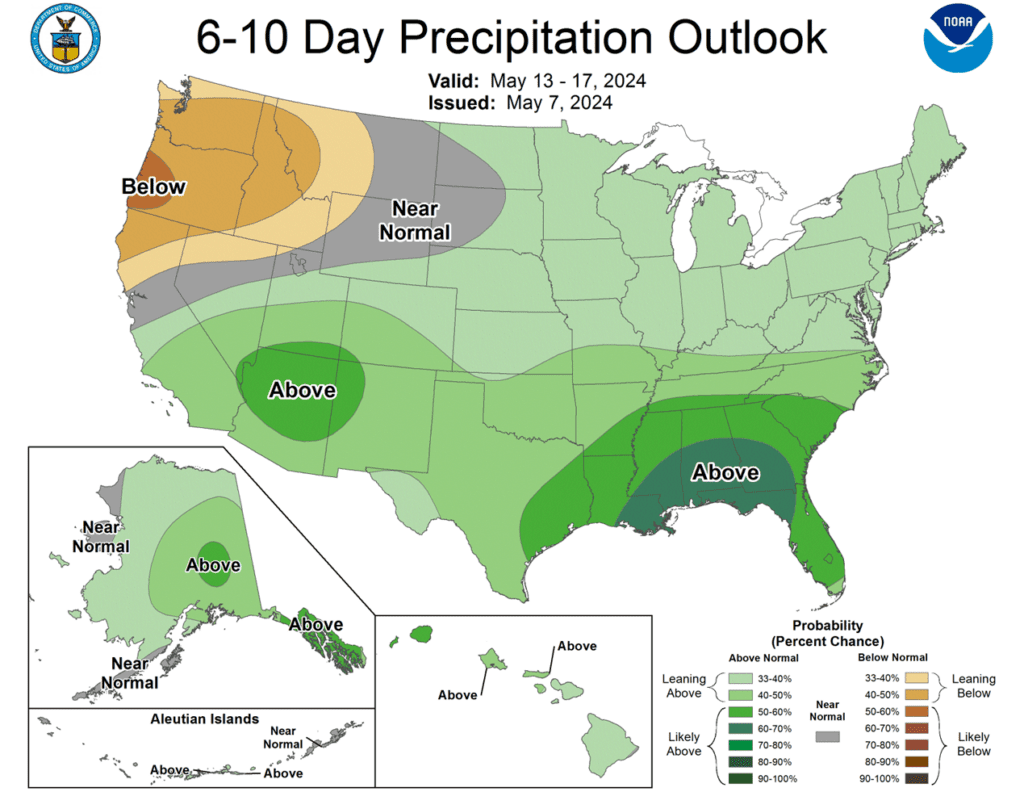

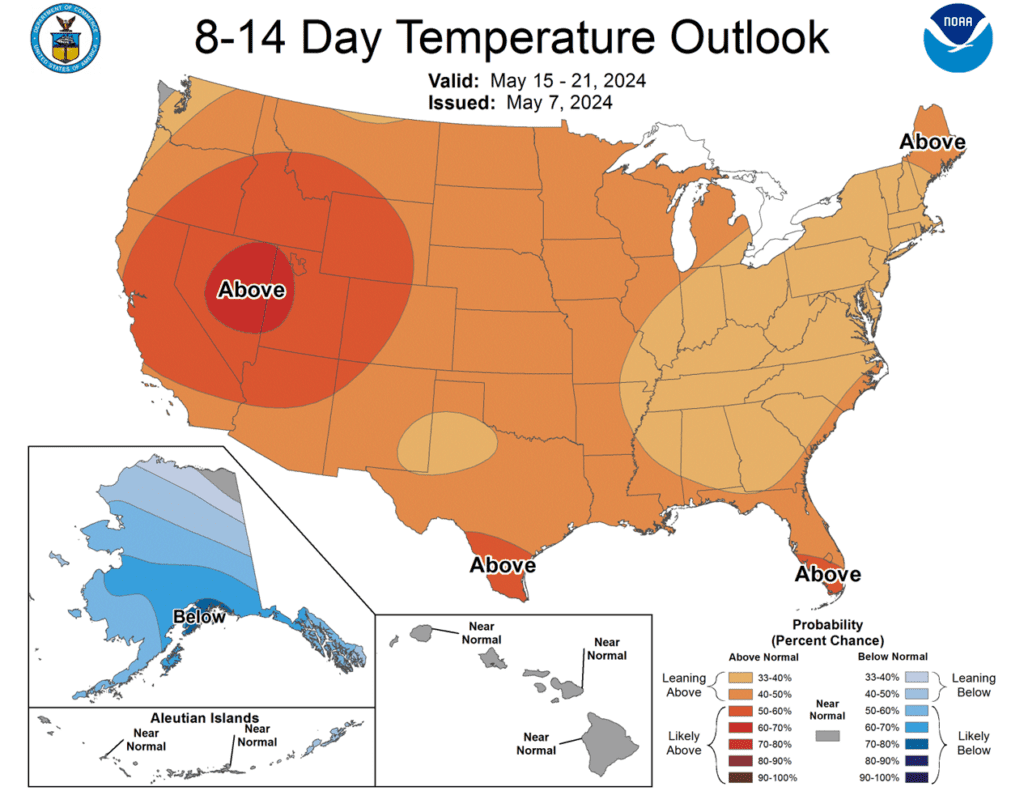

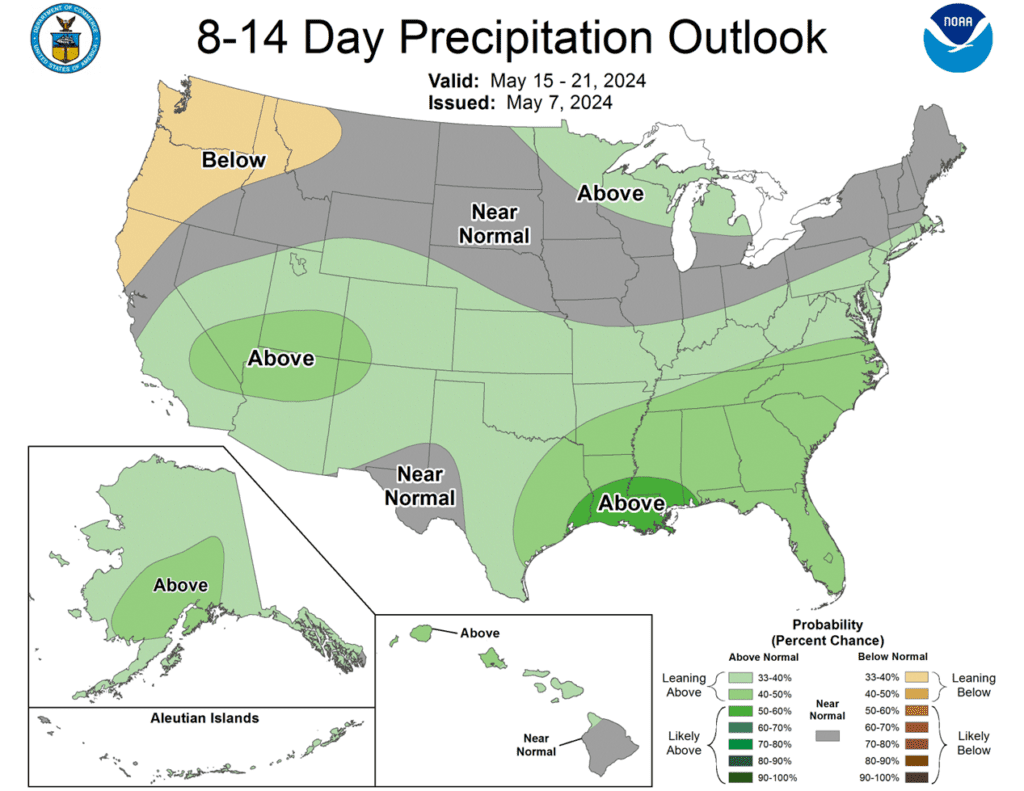

- To see the updated US 5-day precipitation forecast, the US 6 – 10 and 8 – 14 day Temperature and Precipitation Outlooks, as well as the 1-week total precipitation for Brazil and N. Argentina, courtesy of NOAA, NWS, and CPC scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

Despite July ’24 corn rallying beyond the congestion range on the front-month continuous charts, the market exhibits signs of being overbought, potentially adding resistance to higher prices. However, managed funds have retained a significant net short position, likely sparking the recent rally which could fuel a more substantial upside move as we progress through planting and into the growing season. Despite potential obstacles, overall market conditions and seasonal tendencies continue to support a sustained price recovery into May and June.

- No new action is recommended for 2023 corn. The target range to make additional sales is 480 – 520 versus July ’24 futures. If you need to move bushels for cash or logistics reasons, consider re-owning any sold bushels with September call options.

- No new action is recommended for 2024 corn. We are targeting 520 – 560 to recommend making additional sales versus Dec ‘24 futures. For put option hedges, we are looking for 500 – 520 versus Dec ‘24 before recommending buying put options on production that cannot be forward priced prior to harvest.

- No Action is currently recommended for 2025 corn. At the beginning of the year, Dec ’25 corn futures left a gap between 502 ½ and 504 on the daily chart. Considering the tendency for markets to fill price gaps like these, we are targeting the 495 – 510 area to recommend making additional sales.

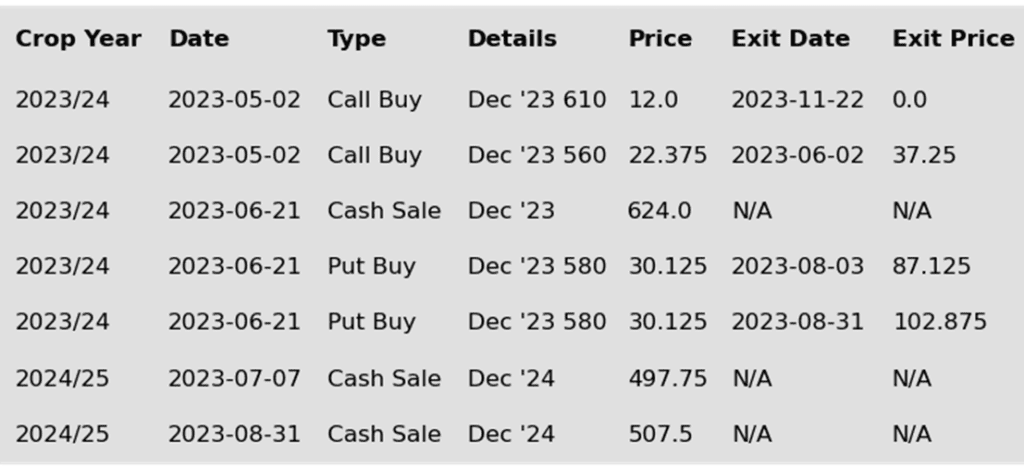

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Strong selling hit the grain markets, pulling corn lower on the day as the recent rally’s momentum seemed to lose steam on Tuesday, and saw follow through selling on Wednesday. July corn futures fell back to test support at the 100-day moving average. This will likely be a key support level for Thursday’s session.

- Talk of strong producer selling of corn in the US, Brazil, and Argentina likely weighed on corn markets as the recent price rally provided opportunities for producers to get caught up on sales for both old and new crop bushels. The movement of corn has been reflected in a widening basis in some areas of the Corn Belt. South American sales moved more bushels to ports for export, creating competition against US corn.

- The USDA will release weekly export sales on Thursday morning. Expectations are for new sales from last week to be near the 700,000 mt – 1.0 mmt levels. On last week’s report, US exporters reported new sales of 759,000 mt.

- The USDA will release the next WASDE report on Friday morning. The May report will give the market its first estimates for the 24/25 marketing year and updates for the current marketing year. Old crop corn carryout is expected to decrease slightly, but 24/25 will likely show the potential for large production and increased carryout year over year.

- After the release of Friday’s USDA report, the planting pace will move back into focus for the market. Planting will continue to struggle as another weather system is moving across the Corn Belt this week. The forecast is showing a break in the weather in the middle of the month, but expectations are for a warm and wetter forecast into the end of May.

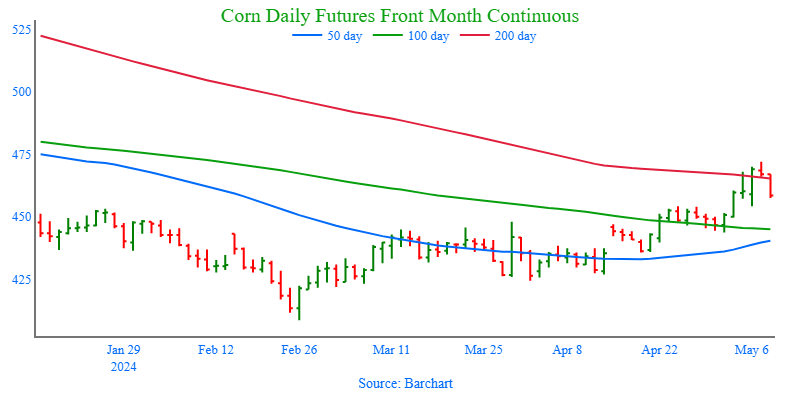

Above: The recent move up took July corn into overbought status and to a high of 472, just above the 200-day moving average. Being overbought makes the market more vulnerable to a downturn. Should that occur, support may be found down near 445 to 440. If prices turn back higher, initial resistance remains near the 472 high, and then again around 495 – 510.

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

In early May the soybean market rallied out of its congestion range and above the March highs as Managed funds likely covered some of their net short positions. While the current supply/demand situation remains somewhat bearish, Managed funds remain net short the market and this breakout opens the door for a run towards the 1290 ¾ – 1296 ¾ chart gap and resistance area just above there if further production concerns arise in the coming weeks. Otherwise, if weather conditions cooperate and planting progresses without major issues, prices could remain susceptible to a reversal from the recent highs.

- No new action is recommended for 2023 soybeans. We are currently targeting a rebound to the 1275 – 1325 area versus July ’24 futures to recommend making further sales. If you need to move inventory for cash or logistics reasons, consider re-owning any sold bushels with September call options.

- No new action is recommended for the 2024 crop. Considering the amount of uncertainty that lies ahead with the 2024 soybean crop, we recommended back in December buying Nov ’24 1280 and 1360 calls to give you confidence to make sales against anticipated production and to protect any sales in an extended rally. We are currently targeting the 1280 – 1320 range versus Nov ’24 futures, which is a modest retracement toward the 2022 highs, to recommend making additional sales.

- No Action is currently recommended for 2025 Soybeans. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

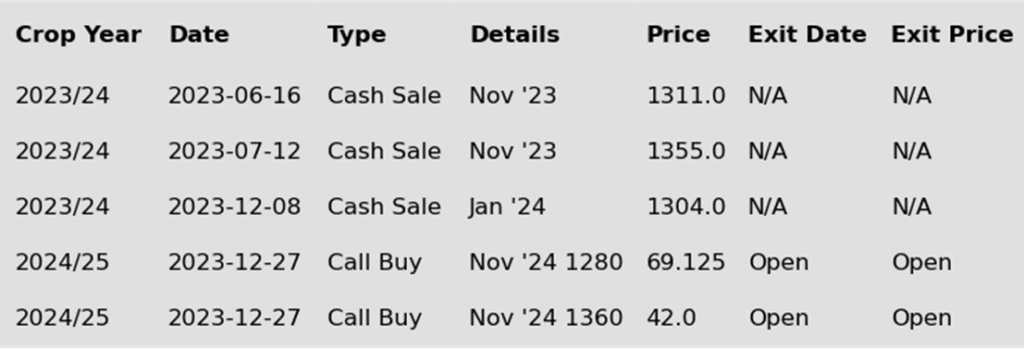

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans finished the day significantly lower along with lower closes in both soybean meal and oil. Much of today’s downward pressure was likely due to profit taking following the recent rally along with positioning ahead of Friday’s WASDE report. Planting delays in the US along with flooding in South America has been supportive to this rally.

- Early trade estimates for Friday’s USDA report have the 23/24 soybean ending stocks relatively unchanged, and the ending stocks for 24/25 are estimated at 439 mb, using a soybean yield of 52.0 bpa. The Argentinian bean crop is expected to be revised lower to 49.7 mmt from 50 mmt, and Brazil’s production is expected to be lowered to 152.5 mmt from 155 mmt last month.

- In Argentina, there is a big problem with leaf hopper insects spreading disease among the corn crop, and there is a possibility that this could continue into further seasons, especially with warmer weather. As a result, many Argentinian producers are reporting that they will plant more soybeans than corn in the future in order to mitigate potential yield losses in corn.

- The flooding in Rio Grande do Sul has been a large impact on this rally and specifically has benefitted soybean meal as Brazil typically exports a portion of its bean crop to Argentina to be crushed. The flooding comes after a season that suffered through drought conditions as well further impacting yields in those areas.

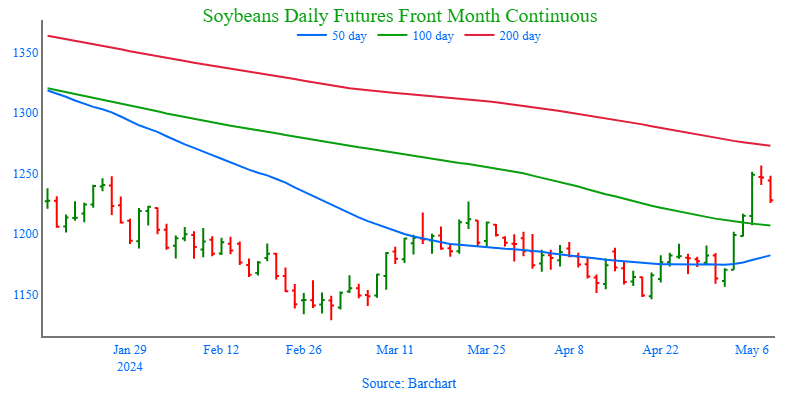

Above: While the close above the 1248 January high on May 6 set the market up to target the 1290 ¾ – 1296 ¾ gap and the subsequent 1328 – 1352 resistance area, it also left the market overbought and vulnerable to a decline. Initial support could be found between 1227 and 1207, with further support between 1192 and 1146 if the market slides further.

Wheat

Market Notes: Wheat

- Wheat finished with losses in all three classes today. The US Dollar Index has been trending higher the past two days, putting pressure on the market. Additionally, Matif wheat was down again today, offering weakness. Profit taking after the recent strong uptrend may also be considered a culprit for the lower trade today.

- Russia has reportedly reduced their wheat export tax by 3% to 3,171 rubles per mt, for the time period ending May 21. In other news, Russia is said to have been the lowest offer for Egypt’s wheat tender, at $255 per mt FOB. In a final note about Russia, Sov Econ has reported their wheat stocks at the end of April to be 27.5 mmt, which is 65% above the average.

- The flooding in Rio Grande do Sul in southern Brazil has caused damage to the soybean crop in addition to transportation and logistics issues. As it relates to wheat, the wet weather is also causing major delays to winter wheat planting in the region.

- A crop tour in Oklahoma has come up with a projected 2024 wheat crop at just over 89 mb, with an average yield of 33.68 bpa. These estimates were the result of field assessments led by educators from Oklahoma State University Extension, as well as crop consultants and agronomists.

- China has reportedly approved the safety of genetically edited wheat for the first time. Over the past year or so they have approved the use of certain GMO soybean and corn seeds as well. The key difference is that genetic editing involves altering the plant’s existing genes, while genetic modification involves the implementation of foreign genes into the plant’s DNA. This is a step forward for China as they work to become more self-sufficient with their agriculture.

- Later this week, record cold temperatures may hit parts of Russia and Ukraine, which may affect spring crops. However, damage to winter wheat is not expected to be much of an issue, as is evident by a lack of response from the market at this time.

Action Plan: Chicago Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

Active

Sell JUL ’25 Cash

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Chicago Wheat Action Plan Summary

After holding downside support near 550, Chicago wheat staged a rally, fueled mostly by Managed fund short covering, HRW crop concerns, and dryness in southern Russia, that took it through the major moving averages on the continuous chart, and towards last December highs. Although bearish fundamentals remain, and the market shows signs of being overbought which adds downside risk, Managed funds still hold a net short position that has the potential to drive an extended short covering rally should these concerns linger or intensify.

- No new action is currently recommended for 2023 Chicago wheat. Any remaining 2023 soft red winter wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 Chicago wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Chicago wheat. Since weather became a much more dominant story for the wheat market, it appears that Chicago wheat may have established a springtime low. In light of this, Grain Market Insider has issued two separate recommendations to exit the second half of the July ’24 Chicago wheat 590 puts that were recommended for purchase last August. Considering that the crop is still developing, and weather remains a factor, we are aiming to recommend further sales within the 685 – 715 range versus July ’24 futures.

- Grain Market Insider sees a continued opportunity to sell another portion of your estimated 2025 SRW wheat production. Since our last sales recommendation for next year’s SRW wheat crop, July ’25 Chicago has rallied over 70 cents and is approaching the 62% retracement level from the March low back to contract highs, as Managed funds cover their extensive net short positions on world production concerns for this year’s crop. While plenty of time remains for other bullish factors to enter the scene that could push prices further, this rally may primarily be weather driven and short-lived, and we advise you to take advantage of these elevated prices to sell another portion of your estimated 2025 SRW production.

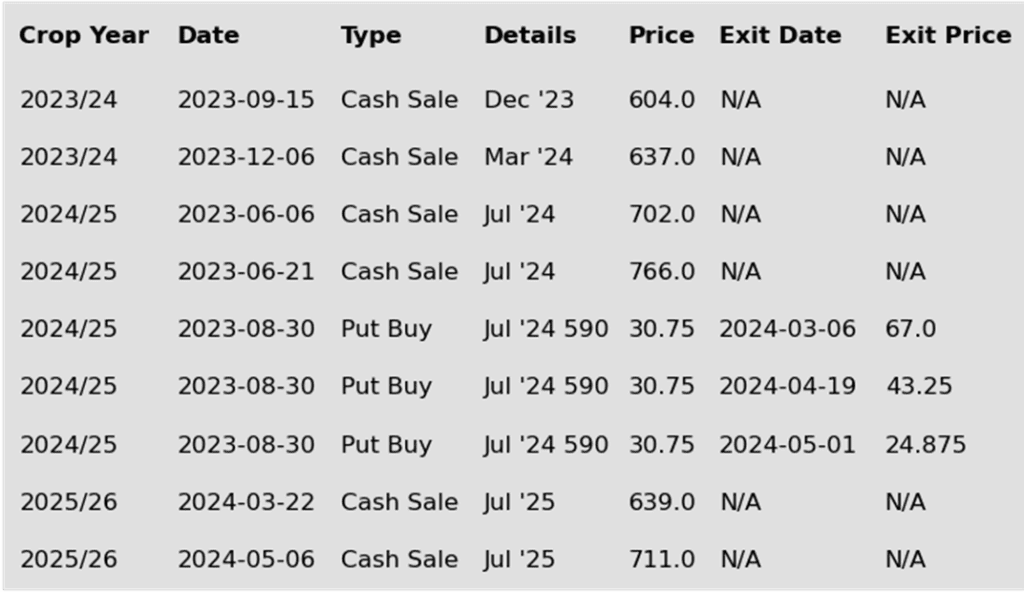

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

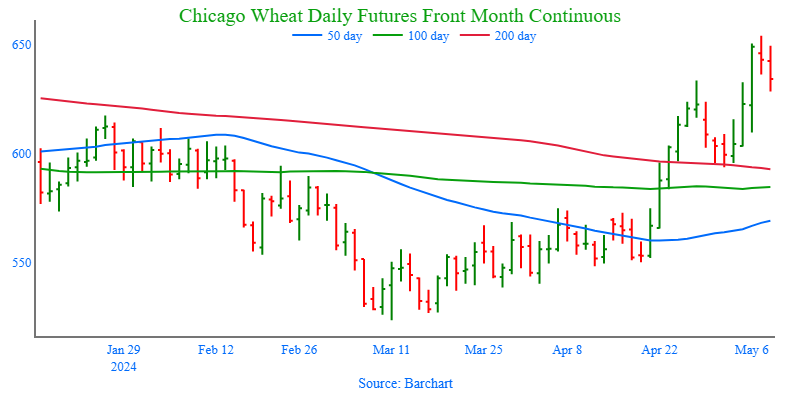

Above: Support near the 200-day moving average has held, and the close above 633 ¼ opens the door for the market to test the area of 664 and then 684 as it moves toward the July high of 777 ¼. A slide lower and close below 593 ½ may encounter support around the 50-day moving average (568) with 548 support below that.

Action Plan: KC Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

KC Wheat Action Plan Summary

Between the end of February and the middle of April, KC wheat was mostly rangebound between the mid 590s on the topside and mid 550s down low, with little to move prices higher, all the while Managed funds continued adding to their large net short positions. Toward the end of April, dryness in the Black Sea region and the US HRW growing areas started becoming more concerning and triggered a short covering rally across the wheat complex, driving prices to levels not seen since last December. Although US wheat exports continue to struggle to compete on the world market, which can keep a lid on US prices, and while Managed funds covered a significant portion of their net short positions, they remain short the market, which could still push prices higher if production concerns persist.

- No new action is recommended for 2023 KC wheat. Considering time is getting limited before the ’24 crop harvest, we recommended two sales on this most recent runup in prices to get old crop HRW wheat marketed. With that said, we are currently evaluating the market situation before setting a target for what will likely be our last sales recommendation for the 2023 HRW crop year.

- No new action is recommended for 2024 KC wheat. Since weather has become a much more dominant driver, marked by the market breaking out of its 2-month long 552 – 605 trading range, we recently recommended making a sale for the 2024 crop considering weather rallies can be short lived. Seeing that the crop is still developing, and weather has become a larger factor, we are currently targeting the 760 – 780 range versus July ’24 futures to recommend additional sales.

- No action is currently recommended for 2025 KC Wheat. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

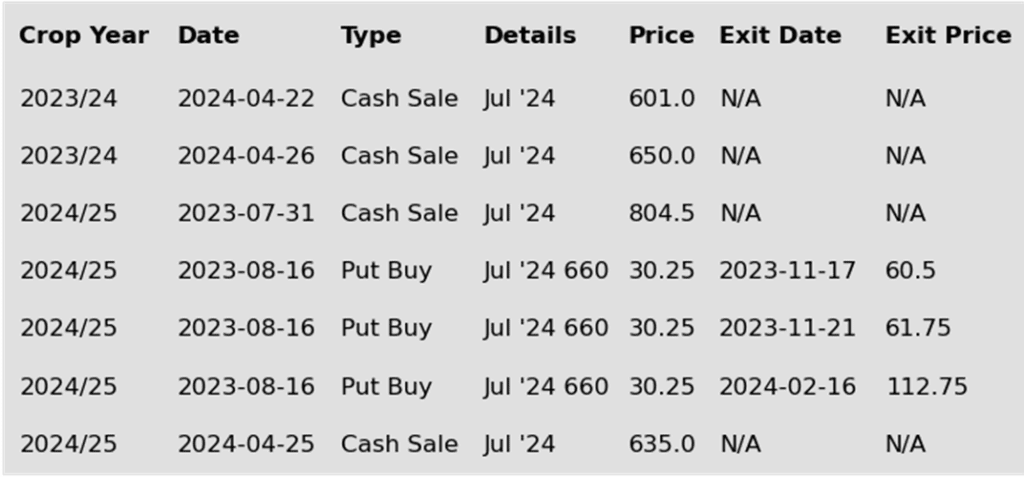

To date, Grain Market Insider has issued the following KC recommendations:

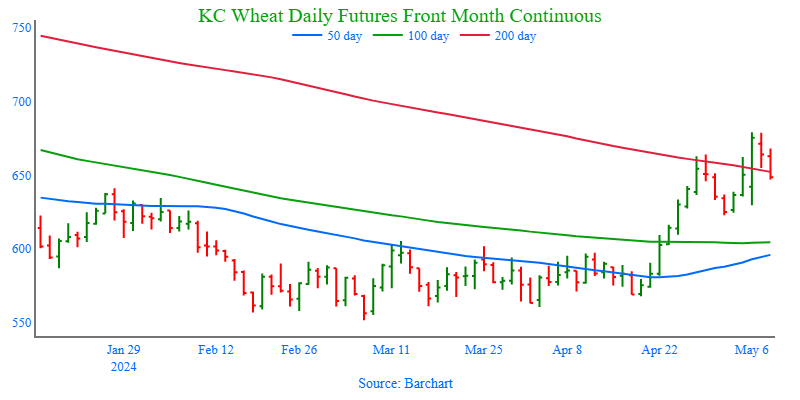

Above: Front-month KC wheat appears to be consolidating following the recent rally. Nearby support below the market sits near 623, with nearby resistance just overhead near the recent 679 high. A close above 679 should be supportive for a run towards 700 psychological resistance, while a close below 623 could open the door for a slide toward 600 support.

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

From mid-February through most of April, Minneapolis wheat traded mostly sideways to lower, lacking significant bullish fundamental news to drive prices upward. However, in late April, spurred by concerns over the world wheat crop and dry conditions in the HRW growing regions, Minneapolis wheat experienced a rally back towards last fall’s highs. Despite lingering obstacles for the US wheat market and indications of overbought conditions, historical seasonal trends typically strengthen in late spring and early summer. Moreover, the fact that Managed funds still maintain a net short position suggests the potential for an extended rally if further production concerns emerge.

- No new action is recommended for 2023 Minneapolis wheat. Following the recent breakout to the upside and the subsequent rally off the April lows, we recommended making a sale to take advantage of the elevated prices. The current strategy is to look for an extension of the rally toward last December’s highs and target 725 – 750 to recommend additional sales.

- No new action is recommended for 2024 Minneapolis wheat. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts (due to their higher liquidity and correlation to Minneapolis), to protect the downside, and recommended exiting the original position in three separate tranches as the market got further extended into oversold territory to protect any gains that were made. The current strategy is targeting the 775 – 815 area versus Sept ’24 to recommend making additional sales. We are also targeting the 850 – 900 area to recommend buying upside calls to help protect any sales that would have been made.

- No action is currently recommended for the 2025 Minneapolis wheat crop. We are currently not considering any recommendations at this time for the 2025 crop that will be planted in the spring of next year. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

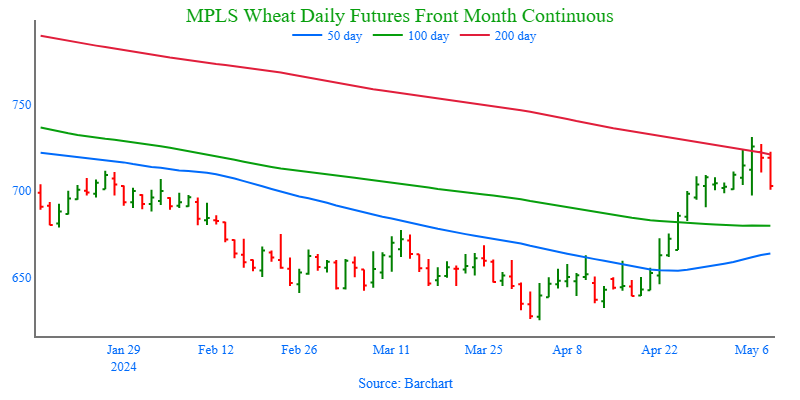

Above: After reaching a high of 731 in July Minneapolis wheat, the market seems to be consolidating after becoming overbought. Nearby support is around 697 – 690 ½, and a close below this range could signal a further decline toward support levels at 675 and 660. Conversely, a close above 731 could pave the way for prices to advance toward the November high of 752, although resistance may be encountered in the 725 – 735 area.

Other Charts / Weather

Above: US 5-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

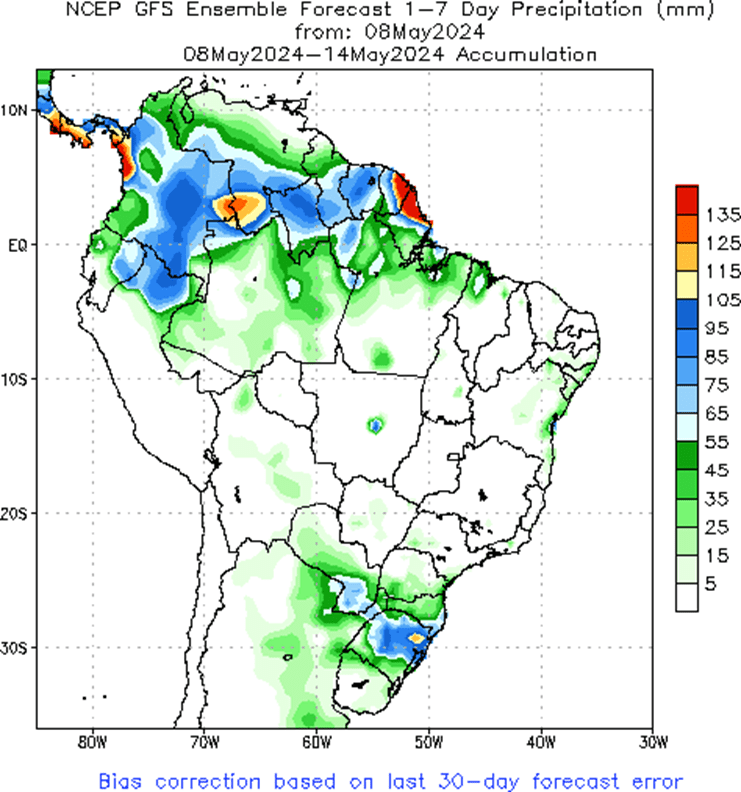

Above: Brazil and N. Argentina 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.