5-15 End of Day: Soybeans Slammed Lower on RFS Headline; Corn Ends Mixed

All Prices as of 2:00 pm Central Time

| Corn | ||

| JUL ’25 | 448.5 | 3 |

| DEC ’25 | 438.75 | -1.75 |

| DEC ’26 | 458 | -1.5 |

| Soybeans | ||

| JUL ’25 | 1051.25 | -26.5 |

| NOV ’25 | 1035.25 | -26 |

| NOV ’26 | 1038.75 | -20.25 |

| Chicago Wheat | ||

| JUL ’25 | 532.75 | 8 |

| SEP ’25 | 546.5 | 7.5 |

| JUL ’26 | 605 | 7.25 |

| K.C. Wheat | ||

| JUL ’25 | 528.25 | 5.25 |

| SEP ’25 | 542 | 5 |

| JUL ’26 | 600.75 | 4.5 |

| Mpls Wheat | ||

| JUL ’25 | 580 | 3 |

| SEP ’25 | 593 | 2.25 |

| SEP ’26 | 657.75 | 3.75 |

| S&P 500 | ||

| JUN ’25 | 5935.5 | 27 |

| Crude Oil | ||

| JUL ’25 | 61.17 | -1.51 |

| Gold | ||

| AUG ’25 | 3254.4 | 38.4 |

Grain Market Highlights

- 🌽 Corn: Corn futures finished mixed on the day. Strong weekly export sales supported old crop contracts, but overall gains were limited by concerns over biofuel demand and favorable weather forecasts.

- 🌱 Soybeans: Soybeans ended the day sharply lower, driven by a limit-down move in soybean oil. The pressure came from bearish news tied to the Renewable Fuel Standard and renewable volume obligations.

- 🌾 Wheat: Wheat futures ended higher across all three classes today, showing relative strength despite heavy pressure in the soy complex.

- To see the updated drought monitor and the updated monthly temperature and precipitation outlooks for the U.S. scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

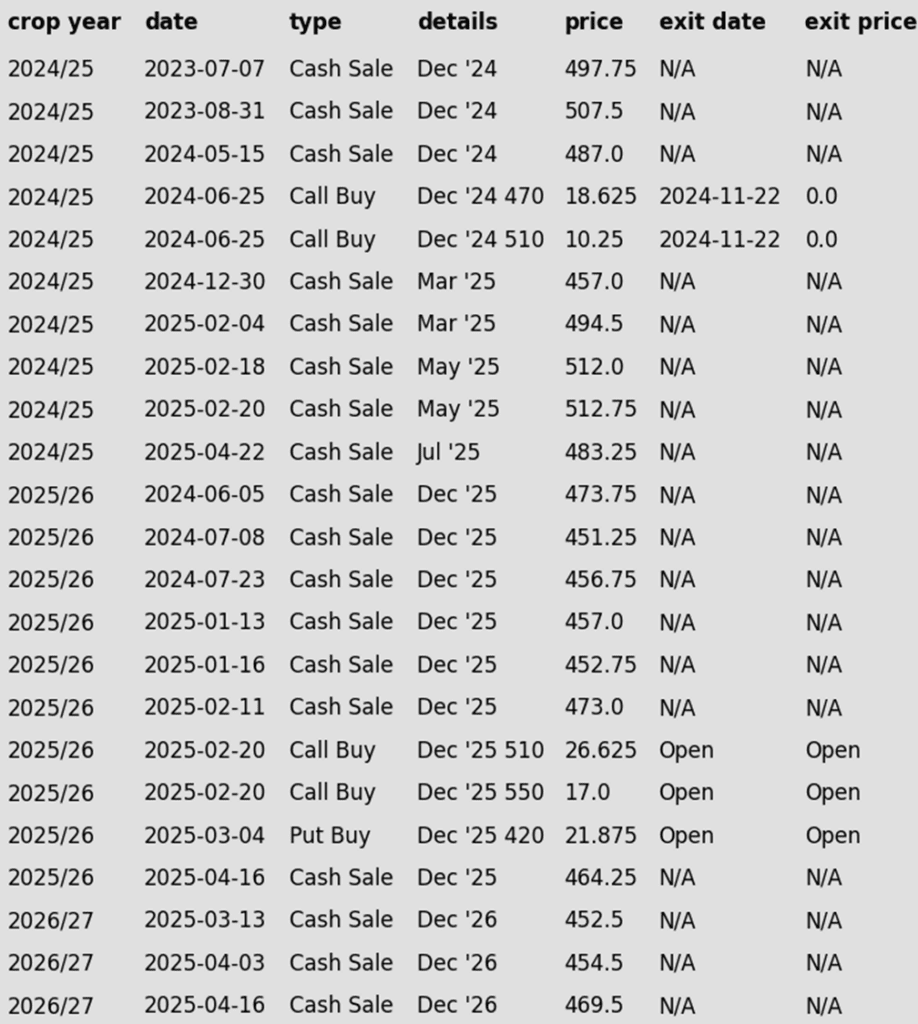

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Eight sales recommendations made to date, with an average price of 494.

- Changes:

- A Plan B downside stop could be added within the next few trading days. The front-month contract hasn’t closed below 440 since mid-December, and the July contract is currently testing that area. If support fails to hold here, the next downside risk could be a move toward 400.

2025 Crop:

- Plan A:

- Exit all 510 December calls @ 43-5/8 cents.

- Exit half of the December 420 puts @ 43-3/4 cents.

- Exit one-quarter of the December 420 puts if December closes at 411 or lower.

- Roll-down 510 & 550 December calls if December drops to 399.

- Plan B: No active targets.

- Details:

- Sales Recs: Seven sales recommendations have been made to date, with an average price of 461.25.

- Changes:

- None. Prepped for growing season volatility with upside and downside targets to start legging out of open options positions.

2026 Crop:

- Plan A: Next cash sale at 474 vs December ‘26.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations have been made to date, with an average price of 460.

- Changes:

- None.

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn futures finished mixed on the day. Strong weekly export sales supported old crop contracts, but overall gains were limited by concerns over biofuel demand and favorable weather forecasts.

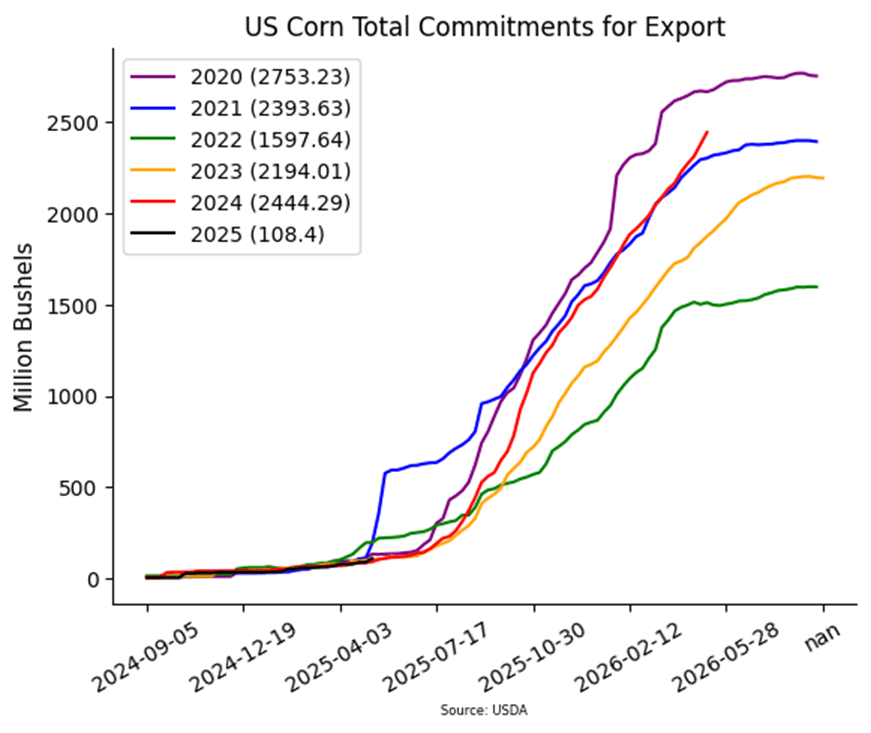

- The USDA released its weekly export sales report on Thursday morning. For the week ending May 8, new sales totaled 1.677 million metric tons (66 million bushels) for old crop and 509,000 metric tons (20 million bushels) for new crop. Old crop sales exceeded analysts’ expectations, with South Korea emerging as the largest buyer last week.

- An announcement from the EPA on Thursday added pressure to the grain markets. Instead of a near-term update on blending volumes, EPA Administrator Lee Zeldin stated that the agency will complete a new rulemaking process “over the next few months.” The delay disappointed traders hoping for clarity on Renewable Fuel Standard volumes and triggered a limit-down move in soybean oil. The spillover weighed on new crop corn futures, reflecting concerns about long-term ethanol demand.

- Planting conditions across the U.S. remain favorable, with most areas seeing an open window for fieldwork. Forecasts show increasing chances for beneficial precipitation across key growing regions next week, supporting early crop development and helping cap market rallies.

- Mexico remains the largest buyer of U.S. corn on the export market. Current weather and drought conditions there could become a quiet but supportive factor for U.S. corn. Mexico’s primary planting window runs from April through August, accounting for about 70% of its total production. Drought in key growing areas could reduce yields, potentially boosting U.S. corn exports next winter.

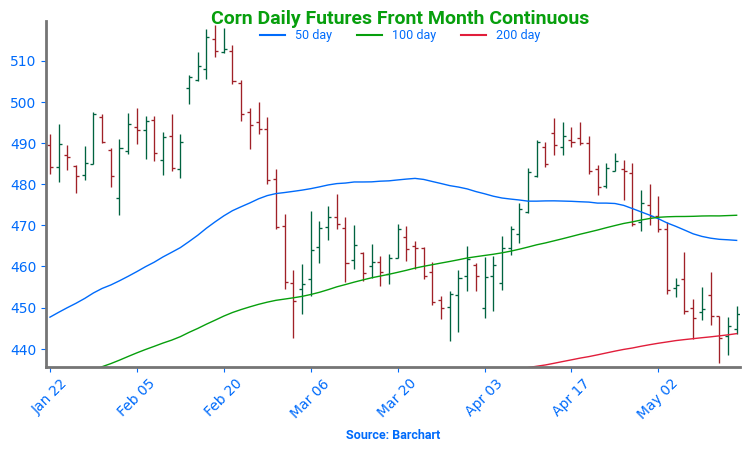

Corn Back Near Calendar Year Lows

Corn futures broke higher in April after repeatedly holding support near 450, with a bullish April WASDE — highlighting stronger demand — fueling the move through the 50-day moving average. As May begins, traders are watching weather developments and demand signals to guide the next leg. February highs above 510 are the next upside target. However, early May weakness has taken out support at 470, setting up a potential retest of the critical 445-450 zone — the early 2025 low and a key technical floor.

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: Next cash sale at 1107 vs July.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made to date, with an average price of 1089.

- Changes:

- None.

2025 Crop:

- Plan A:

- Next cash sales at 1114 vs November.

- Exit one-third of 1100 call options at 1085 vs November.

- Exit remaining two-thirds of 1100 November call options at 88 cents.

- Plan B:

- Make a cash sale if November closes below 1016.75 support.

- Details:

- Sales Recs: One sales recommendation made so far to date, at 1063.50.

- Changes:

- None. Thinking sub-1000 vs November to potentially begin legging out of recently recommended 1040 January put options. More details to come once an official target is posted.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- Changes:

- None.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day sharply lower due to a limit down move in soybean oil, and July soybeans gave up all of their gains from earlier this week. While soybean export sales were within expectations, the bearish news concerning soybean oil was an announcement last night regarding Renewable Fuel Standard renewable volume obligations.

- On Wednesday evening, EPA Administrator Lee Zeldin confirmed that the agency will initiate a new rulemaking process over the coming months to set updated volume obligations. Traders are concerned the delay could signal lower-than-expected biofuel mandates, potentially below the anticipated 4.6 billion gallons, though this remains speculative.

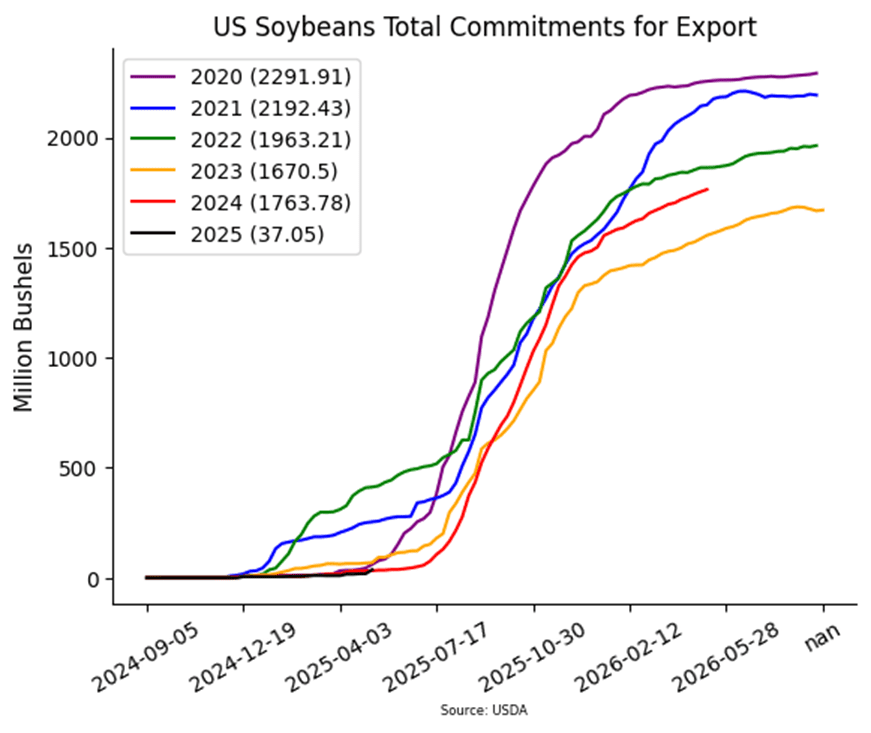

- Today’s export sales report saw soybean sales with an increase of 10.4 mb for 24/25 and an increase of 18.0 mb for 25/26. Top destinations were to Egypt, Indonesia, and Mexico. Last week’s export shipments of 15.8 mb were below the 33.4 mb needed each week to mee the USDA’s export estimates.

- Projections for the U.S. soybean crush in April average 183.8 million bushels. This compares to 194.6 million bushels in March and 169.5 million bushels in April of last year.

Soybean Futures Drift Near Upper End of Yearly Range

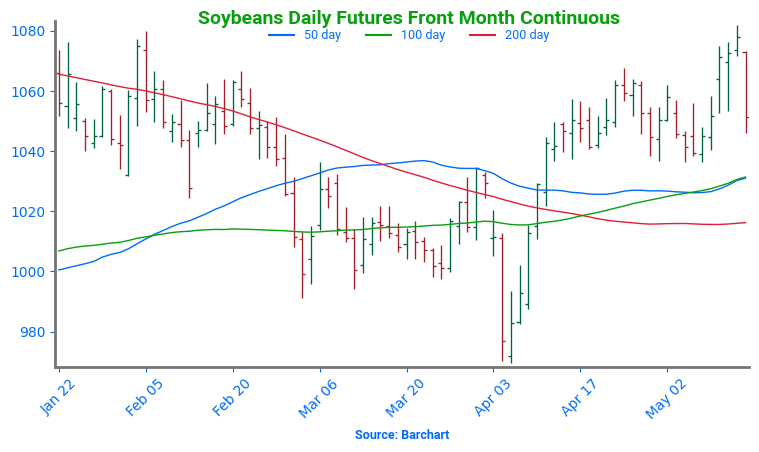

Soybean futures plunged below the critical 1000 level in early April on tariff news, triggering technical selling after a firm March floor gave way. But the drop was short-lived — strong buying quickly reversed the slide, lifting prices back above 1000 and reclaiming major moving averages. Most notably, the 200-day moving average — long a ceiling — was decisively cleared. With momentum shifting higher, the market is eyeing a retest of February’s highs near 1080, while the 200-day average now serves as a key layer of support on any pullbacks.

Wheat

Market Notes: Wheat

- Wheat futures ended higher across all three classes today, showing relative strength despite heavy pressure in the soy complex. Soybean oil closed down its three-cent limit, and soybean futures lost 25 to 27 cents on the day. Support for U.S. wheat may be coming from the upward trend in Paris milling wheat futures, though domestic strength appears largely driven by continued technical buying and short covering, as fresh fundamental news remains limited.

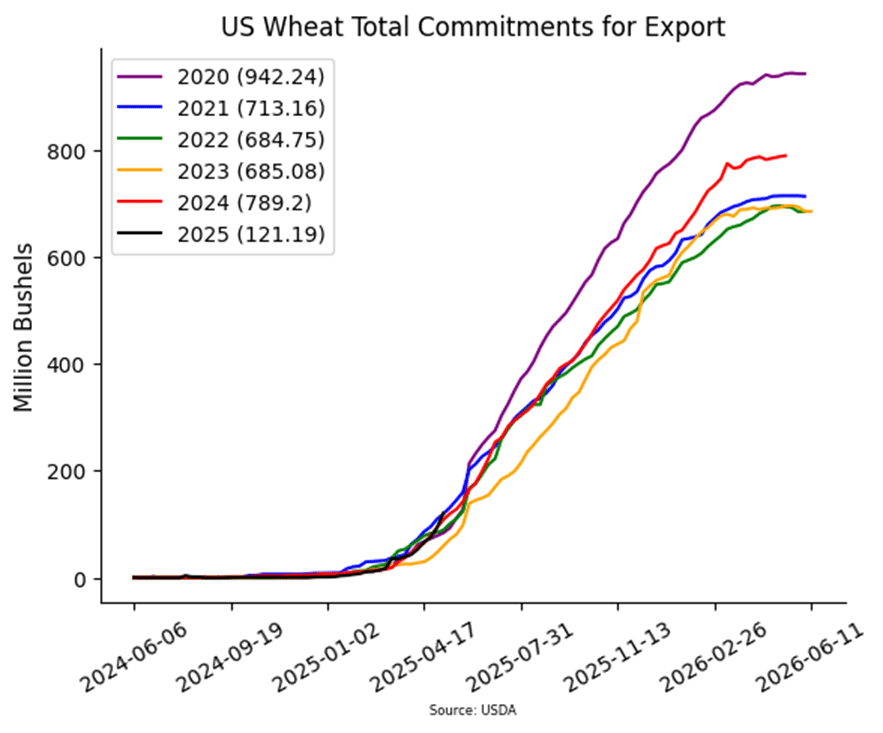

- The USDA reported an increase of 2.2 million bushels (mb) in wheat export sales for 2024/25 and 27.4 mb for 2025/26. Shipments last week totaled 13.6 mb, falling short of the 15.3 mb weekly pace needed to reach the USDA’s 2024/25 export goal of 820 mb. However, total sales commitments for 2024/25 now stand at 798 mb, up 14% from a year ago.

- On day two of the Kansas Wheat Quality Council tour, scouts estimated an average yield of 53.3 bushels per acre (bpa), 2.8 bpa above day one and well above last year’s 42.4 bpa. While there is some concern about wheat curl mite and related disease, impacts appear limited at this point in the season.

- Brazil’s CONAB released updated crop estimates, trimming its wheat production forecast slightly by 0.22 million metric tons (mmt) to 8.25 mmt. For comparison, the USDA currently projects Brazilian wheat output at 8.0 mmt.

- The Rosario Grain Exchange in Argentina is estimating their 25/26 wheat crop at 21 mmt. If realized, this would be an increase from the 20.1 mmt harvested in 24/25. Wheat planting is just getting started there, but the RGE is anticipating a planted area of 7.2 million hectares which would be the largest in 15 years.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A:

- Target 699.25 vs July for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Four sales recommendations made to date, with an average price of 690.

- Changes:

- None. Still waiting for a bottom to form.

2025 Crop:

- Plan A:

- Target 693.75 against July for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made to date, with an average price of 646.

- Changes:

- None. Still waiting for a bottom to form.

2026 Crop:

- Plan A:

- Target 675 vs July ‘26 for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: One sales recommendation made to date, at 624.

- Changes:

- The 688 target was lowered to 675.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Looking for Support

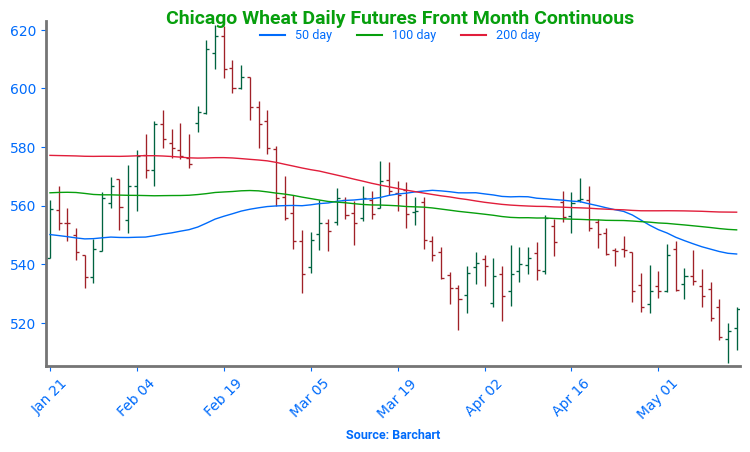

After months of range-bound trading, Chicago wheat futures broke out in February, climbing to October highs just above 615. However, the rally proved short-lived, with prices quickly retreating back into their 2024 range. By mid-May, futures broke below key support near 530 and are now searching for a bottom around the 520 level. The next major technical hurdle is the 200-day moving average — a firm weekly close above this level could signal a potential trend reversal and open the door to a broader uptrend.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made to date, with an average price of 677.

- Changes:

- None. Still waiting for a bottom to form.

2025 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Four sales recommendations made to date, with an average price of 639.

- Changes:

- None. Still waiting for a bottom to form.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- Changes:

- None.

To date, Grain Market Insider has issued the following KC recommendations:

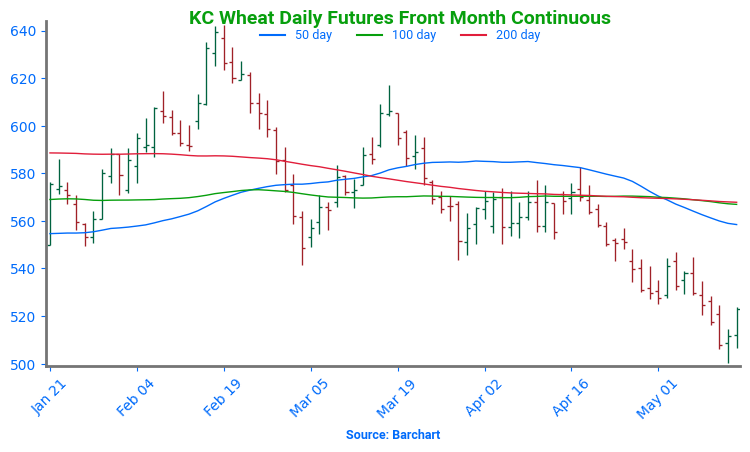

Kansas City Wheat Searching for Support

Kansas City wheat experienced sharp volatility in February, rallying early before settling flat by month’s end. Persistent weakness through March and April pushed prices toward recent lows — and the market broke below that support to start May. A recovery back above the prior 540 level would signal a potential bottom. On a rebound, the 200-day moving average stands as the first resistance, with a more formidable ceiling at the February highs near 640.

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made to date, with an average price of 696.

- Changes:

- None. Still waiting for a bottom to form.

2025 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made to date, with an average price of 646.

- Changes:

- None. Still waiting for a bottom to form.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Changes:

- None.

- Changes:

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Holds Recent Lows

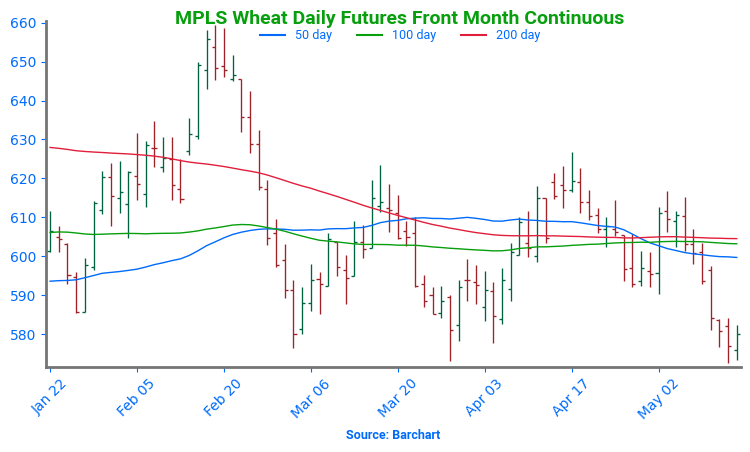

Spring wheat futures broke out of a prolonged sideways trend in late January, sparking a wave of bullish momentum. The rally gained strength in mid-February with a decisive close above the 200-day moving average. However, late-month weakness briefly dragged futures back below key support levels.

Currently, futures are retreating toward recent lows, pressured by strong planting progress and favorable weather conditions across major spring wheat-growing regions. On a potential rebound, initial resistance is expected near the 600 level, where a confluence of moving averages could cap gains.

Other Charts / Weather