4-9 End of Day: Markets Close Mostly Lower, but Remain Largely Rangebound

All prices as of 2:00 pm Central Time

| Corn | ||

| MAY ’24 | 431.25 | -4.25 |

| JUL ’24 | 442.5 | -5 |

| DEC ’24 | 468.25 | -4.75 |

| Soybeans | ||

| MAY ’24 | 1174.5 | -7 |

| JUL ’24 | 1187.75 | -6.5 |

| NOV ’24 | 1178.25 | -6 |

| Chicago Wheat | ||

| MAY ’24 | 557.75 | -8 |

| JUL ’24 | 572 | -8.5 |

| JUL ’25 | 642.75 | -7.5 |

| K.C. Wheat | ||

| MAY ’24 | 577.25 | -8 |

| JUL ’24 | 574.25 | -10.25 |

| JUL ’25 | 628 | -11.5 |

| Mpls Wheat | ||

| MAY ’24 | 651.25 | 1 |

| JUL ’24 | 657.75 | -1.25 |

| SEP ’24 | 666 | -2.5 |

| S&P 500 | ||

| JUN ’24 | 5233.5 | -19.75 |

| Crude Oil | ||

| JUN ’24 | 84.41 | -1.12 |

| Gold | ||

| JUN ’24 | 2366.8 | 15.8 |

Grain Market Highlights

- The corn market remains in a sideways trend as traders anticipate Thursday’s USDA WASDE report, which led to volatile two-sided trading. Weakness from neighboring corn and wheat markets, coupled with additional selling pressure near the 50-day moving average, added to the market’s negative tone.

- The soybean market drifted from its 50-day moving average amid choppy two-sided trade and weakness from both soybean meal and oil, despite a flash sale to unknown destinations. It remains in a sideways trend with limited market-moving news as traders await Thursday’s USDA report.

- Soybean oil traded toward the lower end of the current 47.00 – 50.00 cent range, influenced by declines in crude oil and lower Chinese palm and soybean oil prices. Additionally, meal settled lower for the first time in five sessions, as it faced selling pressure near its 50-day moving average.

- Softer Matif wheat futures, combined with better-than-expected winter wheat conditions, weighed down the wheat complex, resulting in mostly lower closings across the board. While both Chicago and KC contracts retreated from their respective 50-day moving averages and settled well below their highs, Minneapolis contracts managed to recover much of the day’s losses and settled near session highs.

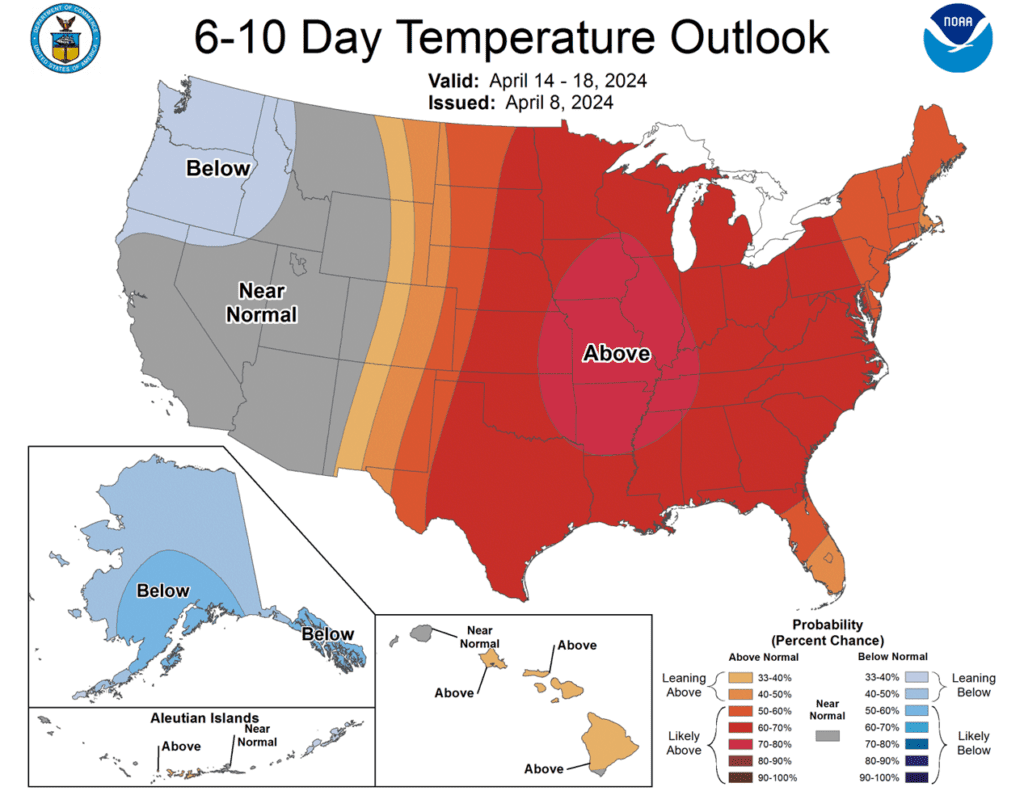

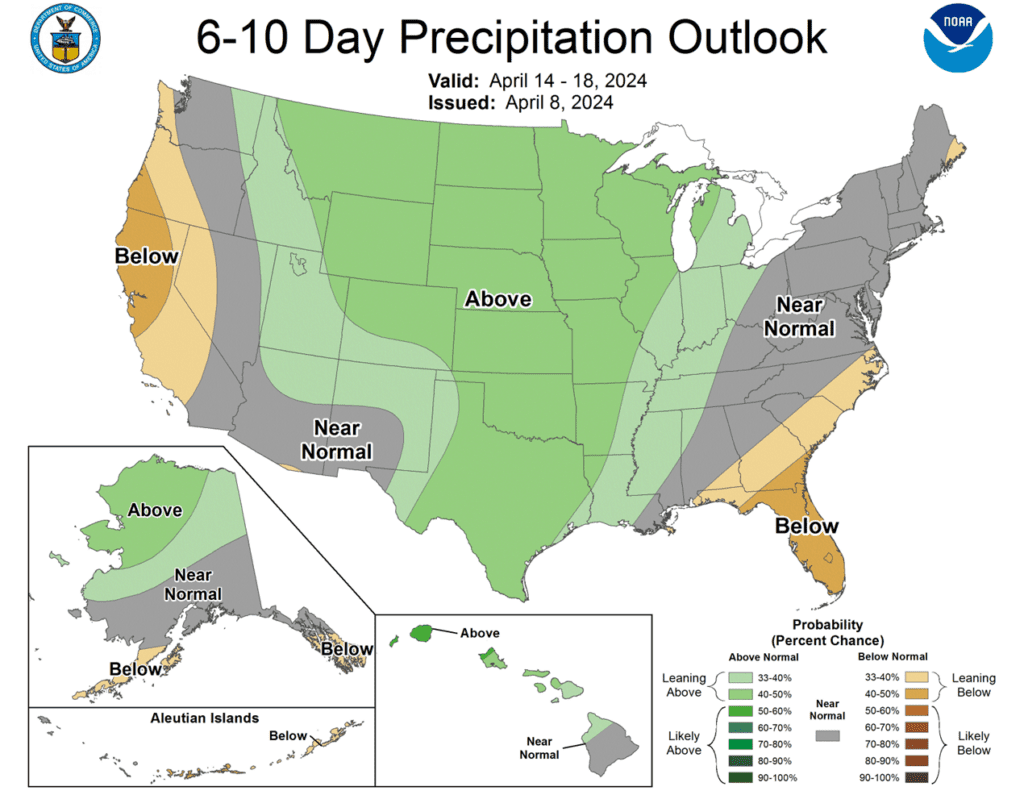

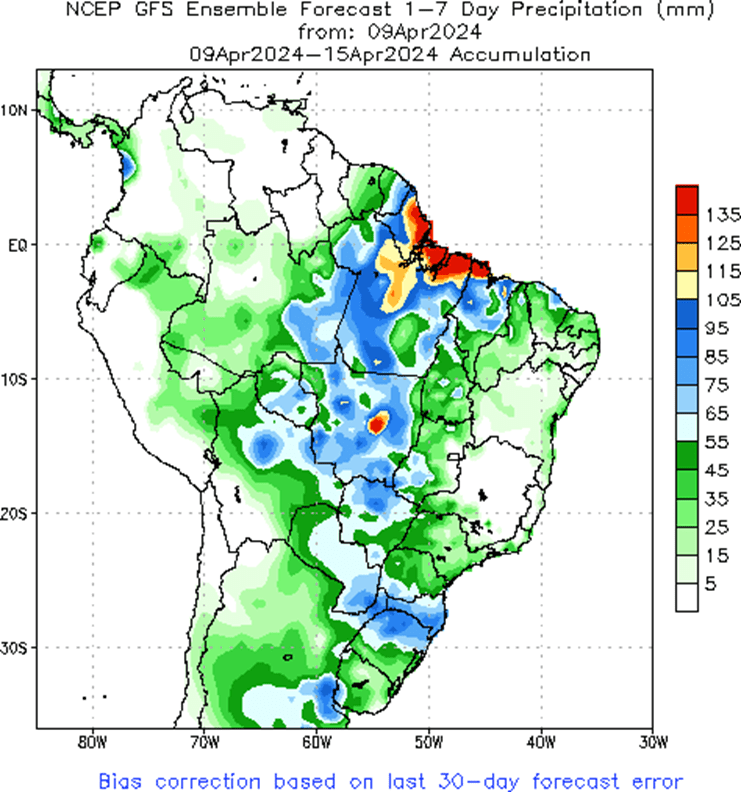

- To see the updated US 6 – 10 day temperature and precipitation outlooks, and 1-week precipitation forecast for Brazil and N. Argentina, courtesy of the NWS and NOAA.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

From the low on February 26 to the high on March 12, May corn experienced a significant rally of nearly 40 cents. However, since then, it has consolidated within a narrow trading range, fluctuating mostly between 430 and 445. During this period, Managed Money has reduced its net short position by approximately 53,000 contracts, although it still holds a historically large short position of around 252,000 contracts. The size of Managed Money’s net short position, coupled with prevailing macro oversold conditions, suggests potential for further upside as we head into spring planting. While the recovery in corn prices may encounter obstacles, overall market conditions remain conducive to a continued price recovery into May and June.

- No new action is recommended for 2023 corn. The target range to make additional sales is 480 – 520 versus May ’24 futures. If you need to move bushels for cash or logistics reasons, consider re-owning any sold bushels with September call options.

- No new action is recommended for 2024 corn. We are targeting 520 – 560 to recommend making additional sales versus Dec ‘24 futures. For put option hedges, we are looking for 500 – 520 versus Dec ‘24 before recommending buying put options on production that cannot be forward priced prior to harvest.

- No Action is currently recommended for 2025 corn. At the beginning of the year, Dec ’25 corn futures left a gap between 502 ½ and 504 on the daily chart. Considering the tendency for markets to fill price gaps like these, we are targeting the 495 – 510 area to recommend making additional sales.

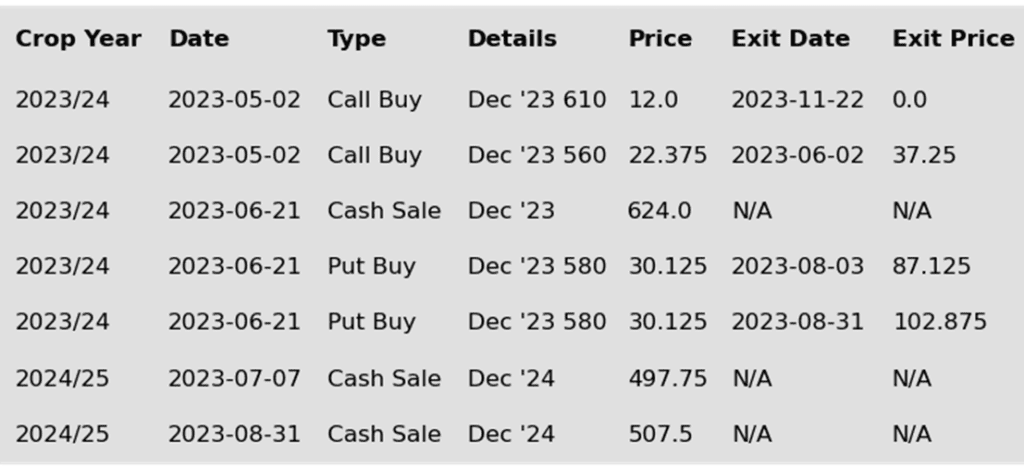

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Selling pressure across the grain complex weighed on corn futures during the session. The weak price action leaves the corn market vulnerable to further downside pressure and liquidation as the May contract is looking to test the low for the month of April at 424 ½ from April 2.

- Seasonality may be working against the corn market with potential price weakness into the end of the month. Producers who hold May basis contracts will need to decide to price or roll these positions before the month’s end. This market structure can lead to selling pressure.

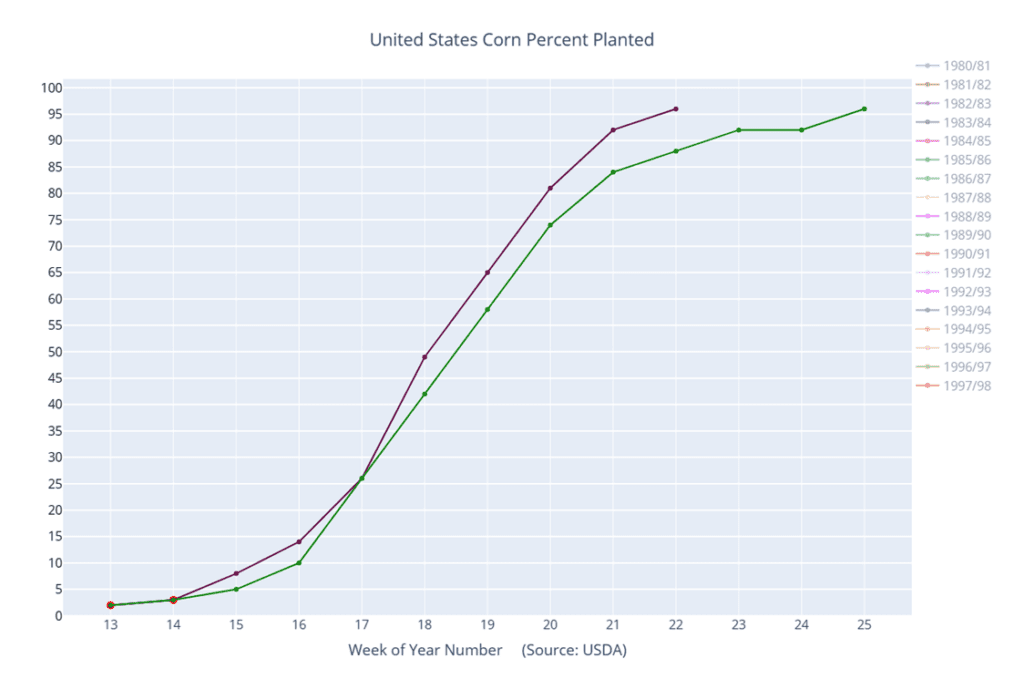

- The USDA Crop Progress report released on Monday afternoon showed corn planting in its beginning stages nationally at 3% complete. This was even with last year, and 1% ahead of the 5-year average.

- Weather forecast for temperatures into the end of April are predicted to stay above normal, which could allow for planting progress to pick up speed for this year’s US corn crop.

- The USDA will release the April WASDE report on Thursday, April 11. Expectations are for corn ending stocks to be reduced to 2.102 billion bushels, down 70 mb from last month. This should reflect the strong first quarter corn usage as reflected in last month’s Quarterly Grain Stocks report.

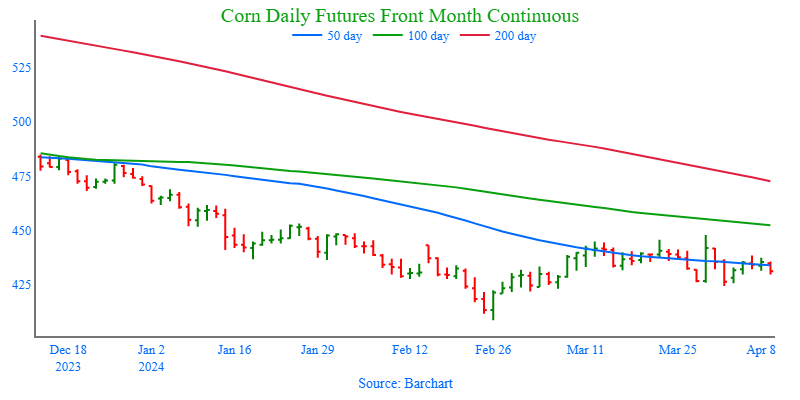

Above: Since the beginning of March, the corn market has been trading sideways, bound mostly by 445 up top and 430 down below. If prices can breakout and close above resistance between the recent high of 448 and the January high of 452 ¼, they could run toward the next major resistance level of 495 – 510. If they break out to the downside and close below 421, they could slide further to test 400 – 410 support.

Above: 24/25 corn percent planted seen at 3% (red) versus the 5-year average (green) and last year (purple).

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

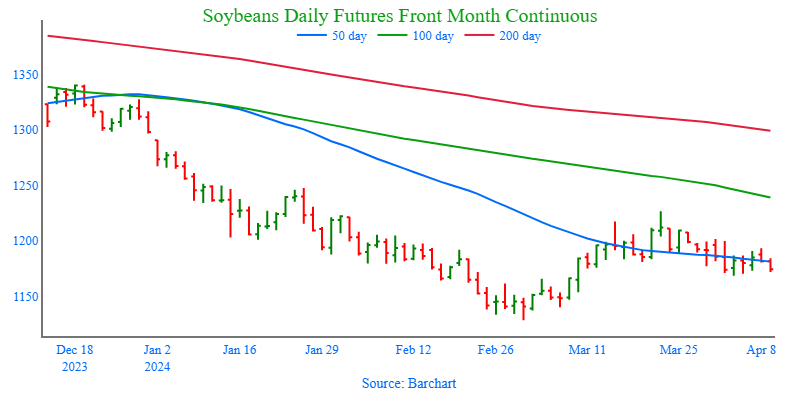

The USDA gave little in the way of outright bullish information to trigger great amounts of short covering as their March 1 stocks and prospective soybean plantings estimates were relatively neutral and came in as expected by the market. That said, Managed Money still held a sizable 135,000 contract net short position in the most recent Commitment of Traders report, which can still fuel a short covering rally if issues come up this season, with planting not that far off. Otherwise, prices may still be at risk of retesting the recent lows this spring if weather stays benign and planting goes smoothly.

- No new action is recommended for 2023 soybeans. We are currently targeting a rebound to the 1275 – 1325 area versus May ’24 futures to recommend making further sales. If you need to move inventory for cash or logistics reasons, consider re-owning any sold bushels with September call options.

- No new action is recommended for the 2024 crop. Considering the amount of uncertainty that lies ahead with the 2024 soybean crop, we recommended back in December buying Nov ’24 1280 and 1360 calls to give you confidence to make sales against anticipated production and to protect any sales in an extended rally. We are currently targeting the 1280 – 1320 range versus Nov ’24 futures, which is a modest retracement toward the 2022 highs, to recommend making additional sales.

- No Action is currently recommended for 2025 Soybeans. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

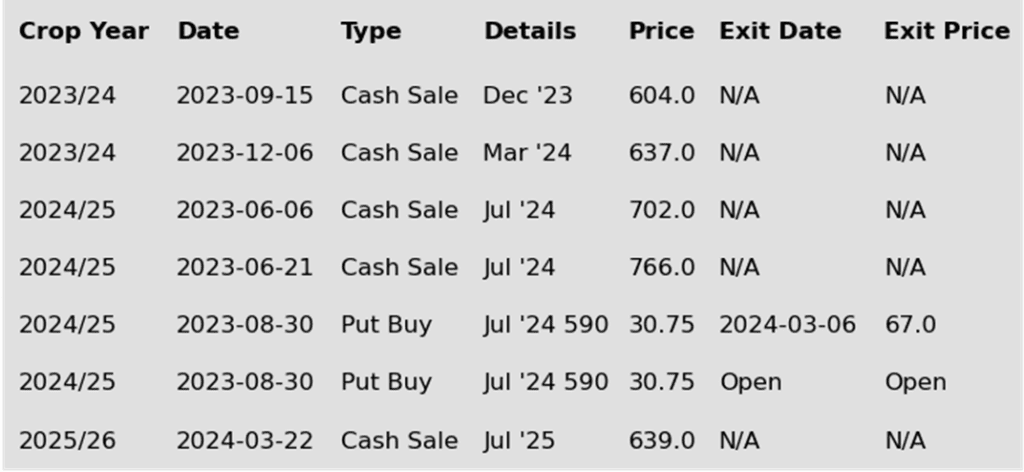

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day lower with the May contract closing below the 40-day moving average. Pressure came from lower soybean oil along with lower soybean meal. Prices got a boost earlier this morning after a flash sale was announced but faded into the end of the day.

- This morning, the USDA reported a flash sale of 124,000 metric tons of soybeans sold to unknown destinations during the 23/24 marketing year. This was the second flash sale announced within two weeks after a long period of no activity. Premiums in Brazil are reportedly rising which could make US soybeans more competitive.

- In South America, the Brazilian soybean harvest is pressing on and is reportedly 79% complete which is slightly below last year’s pace. Some of the beans were planted a bit late and recent rains may have delayed the progress. In Argentina, the growing season is winding down and harvest should begin soon.

- On Thursday, the USDA will release its Supply and Demand report at 11am central time. Early estimates for soybeans are for US ending stocks to increase slightly by 4 mb to 319 mb, and for world ending stocks to decrease slightly. In South America, Argentine soybean production is expected to increase by 0.4 mmt to 50.4 mmt. In Brazil, the USDA is expected to lower their production by 2.7 mmt to 152.3 mmt.

Above: Support around 1168 appears to be holding for now. Should that area continue to hold, and prices close above the recent high around 1227, they could then run toward the 1291 – 1297 chart gap, though resistance might be found near 1250. If prices drop below 1168, they then run the risk of retreating toward 1130 – 1140.

Wheat

Market Notes: Wheat

- Wheat faded into the end of the session, with a lower close across the board, except for a penny gain in May spring wheat. The pressure stemmed from a decline in Matif futures, alongside lower US corn and soybean prices. Moreover, the US Dollar is positioned near the middle of the recent range ahead of tomorrow’s release of key inflation data. The Consumer Price Index (CPI) is anticipated to have risen by 0.3% in March and 3.5% year-over-year. Any deviation from these projections could prompt a market reaction.

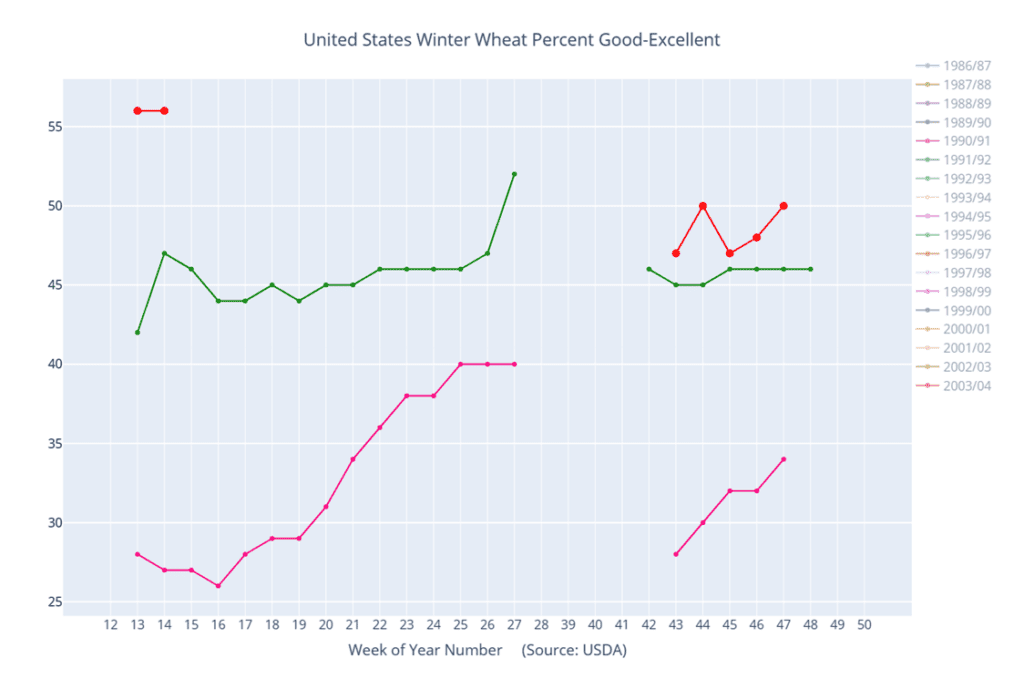

- According to the USDA, the winter wheat crop condition remained steady at 56% rated good to excellent, marking the best condition seen for this time of year since 2020. Additionally, 6% of the crop is currently headed, slightly lower than the 7% reported last year but above the average of 5%. Furthermore, US spring wheat planting progress is at 3%, aligning with the average and surpassing last year’s 1%.

- Argentina’s Economy Minister has announced plans to lower tariffs on certain herbicide imports starting in April, just one month before the start of wheat planting for the 24/25 season. The Buenos Aires Grain Exchange reported a wheat harvest of 15.1 million metric tons last year.

- India’s wheat production for the 23/24 season is forecasted to rise to 105.8 million metric tons, a 2.8% increase from the previous year’s 102.9 million metric tons, as reported by the Roller Flour Miller’s Federation. This increase is attributed to expanded planted acreage, estimated at 34 million hectares compared to last year’s 33.6 million hectares, and improved yields. Additionally, the Indian government is expected to boost wheat buying for reserves to 31-32 million metric tons, up from 26.2 million metric tons last year, according to Agriwatch.

- The USDA projects Russian wheat production at 91.5 million metric tons, while Argus has raised their estimate to 92.1 million metric tons from 90 million previously. Despite the recent rise in Russian wheat FOB values to $210 per metric ton, as reported by IKAR, Russian wheat continues to be the world’s most competitively priced offer, keeping pressure on US futures.

Action Plan: Chicago Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Chicago Wheat Action Plan Summary

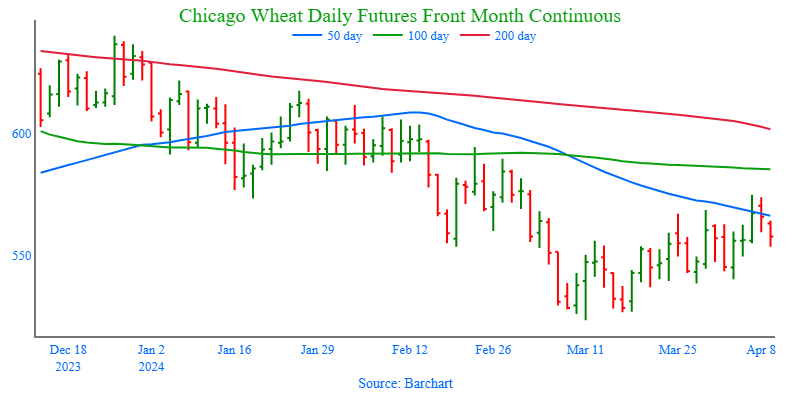

Since making a fresh low in early March, Chicago wheat has traded mostly sideways with relatively small gains capped by overhead resistance. Although the lack of any bullish information has been disappointing, the market remains oversold on a macro level, and managed funds continue to hold a significant net short position. Either or both of these factors could fuel a short covering rally at any time as we head into the more active part of the growing season.

- No new action is currently recommended for 2023 Chicago wheat. Any remaining 2023 soft red winter wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 Chicago wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Chicago wheat. At the end of August, we recommended purchasing July ‘24 590 puts to prepare for further price erosion, and recently recommended exiting half of those puts to lock in gains and get closer to a net neutral cost on the remaining position. For now, we are targeting a market rebound back towards 675 – 715 versus May ’24 futures before recommending any additional sales. As for the open 590 put position, we are looking for prices between 475 – 500 versus July ’24 futures to before we recommend exiting half of the remaining July ’24 590 puts.

- No new action is currently recommended for 2025 Chicago Wheat. We recently recommended initiating your first sales for the 2025 SRW crop year as prices pressed back toward the mid-600 range to take advantage of historically good prices for next year’s crop. Since plenty of time remains to market this crop, we are looking for further price appreciation and are currently targeting the 690 – 725 area to recommend making additional sales.

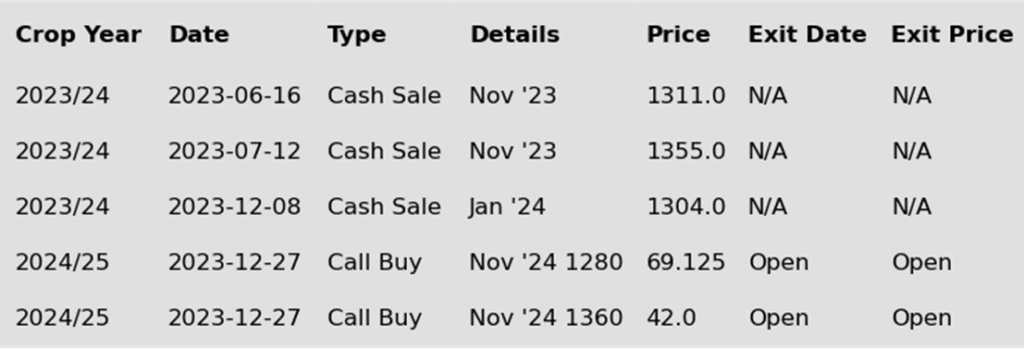

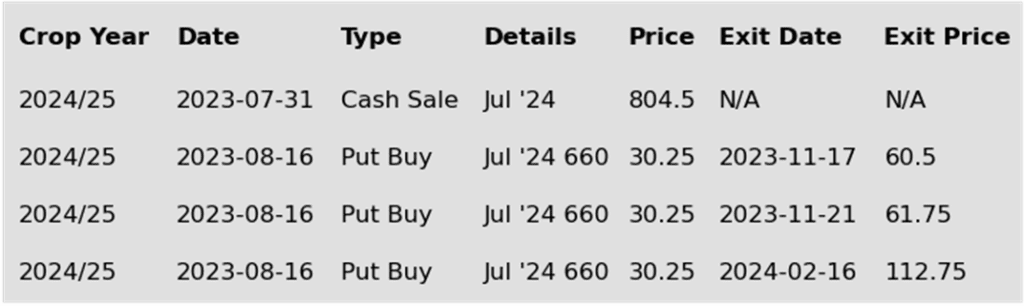

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: The market has fallen away from the 50-day moving average and may be at risk of testing the 523 ½ low if it closes below 537. If prices turn back around and close back above the 50-day moving average, they could still encounter resistance in the 585 – 620 area.

Action Plan: KC Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

KC Wheat Action Plan Summary

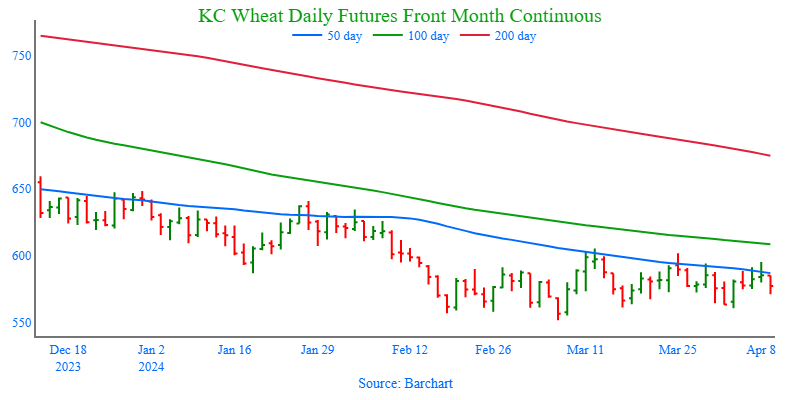

Since the end of February, prices have been trading in a broad range, bound mostly by 555 on the downside and 605 up top, with little fresh bullish news to trade, while US exports continue to suffer from lower world export prices. Although, fundamentals remain weak. Managed funds continue to hold a considerable net short position, and the market is at levels not seen since spring of 2021, which combined could trigger a return to higher prices if unforeseen risks enter the market.

- No new action is recommended for 2023 KC wheat crop. Considering the current US export demand challenges and the sideways nature of the wheat market, we are looking for prices to return to the upper end of the recent range and are targeting the 600 area versus May ’24 to recommend making additional sales.

- No new action is recommended for 2024 KC wheat. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside, and recommended exiting the original position in three separate tranches as the market got further extended into oversold territory to protect any gains that were made. The current strategy is to target 625 – 650 versus July ’24 futures to recommend additional sales.

- No action is currently recommended for 2025 KC Wheat. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

Above: Significant resistance remains within the range bound by the 50-day moving average and the March 10 high of 605 ¼. A close above 605 ¼ might pave the way for further advancement toward the congestion area of 610 – 640. Otherwise, should prices retreat below the initial support level of 561, there’s a possibility of testing the March low of 551 ½.

Above: Winter wheat condition percent good-excellent (red) versus the 5-year average (green) and last year (pink).

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

Minneapolis wheat has primarily traded within a range since last February until a recent breakout below its lower boundary, marking new contract lows and potentially signaling a continuation of the downtrend initiated last summer. Despite facing resistance from the 50-day moving average and a lack of bullish catalysts, seasonal patterns tend to improve heading into early summer. Furthermore, managed funds still maintain a large net short position, which might trigger a short covering rally at any time.

- No new action is currently recommended for 2023 Minneapolis wheat. The current strategy is to look for a modest retracement of the July high and target 675 – 700 to recommend more sales.

- No new action is recommended for 2024 Minneapolis wheat. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts (due to their higher liquidity and correlation to Minneapolis), to protect the downside, and recommended exiting the original position in three separate tranches as the market got further extended into oversold territory to protect any gains that were made. The current strategy is targeting the 775 – 815 area versus Sept ’24 to recommend making additional sales. We are also targeting the 850 – 900 area to recommend buying upside calls to help protect any sales that would have been made.

- No action is currently recommended for the 2025 Minneapolis wheat crop. We are currently not considering any recommendations at this time for the 2025 crop that will be planted in the spring of next year. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: After posting a key bullish reversal on April 3 and with additional support from being oversold, prices may attempt to extend further and challenge the resistance area around 660 – 670. However, if they fail to rally, they may be at risk of drifting back toward psychological support at 600 and the March ’21 low of 596 ¼.

Other Charts / Weather

Above: Brazil and N. Argentina 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.