4-8 End of Day: Bull Spreading Continues in Corn and Soybeans

All Prices as of 2:00 pm Central Time

| Corn | ||

| MAY ’25 | 469 | 4.5 |

| JUL ’25 | 474.75 | 4 |

| DEC ’25 | 445.75 | -0.25 |

| Soybeans | ||

| MAY ’25 | 992.75 | 9.75 |

| JUL ’25 | 1004 | 7 |

| NOV ’25 | 977.75 | -3.25 |

| Chicago Wheat | ||

| MAY ’25 | 540 | 3.5 |

| JUL ’25 | 554 | 3.5 |

| JUL ’26 | 621.25 | 3 |

| K.C. Wheat | ||

| MAY ’25 | 561.5 | 2.25 |

| JUL ’25 | 575 | 2.25 |

| JUL ’26 | 637 | 1.25 |

| Mpls Wheat | ||

| MAY ’25 | 601 | 7 |

| JUL ’25 | 614.5 | 6.25 |

| SEP ’25 | 625.25 | 5.75 |

| S&P 500 | ||

| JUN ’25 | 5084.5 | -12.75 |

| Crude Oil | ||

| JUN ’25 | 59.22 | -1.22 |

| Gold | ||

| JUN ’25 | 3004.6 | 31 |

Grain Market Highlights

- Corn: The corn market remained bull-spread on Tuesday, with front-end contracts showing strength while the deferred months stayed under pressure.

- Soybeans: Soybeans ended mixed again, with the front three months posting gains while deferred contracts slipped, signaling continued bull spreading.

- Wheat: Wheat finished in the green across all classes, buoyed by a weaker U.S. Dollar Index, a stronger close in Paris futures, and lower crop ratings compared to last year.

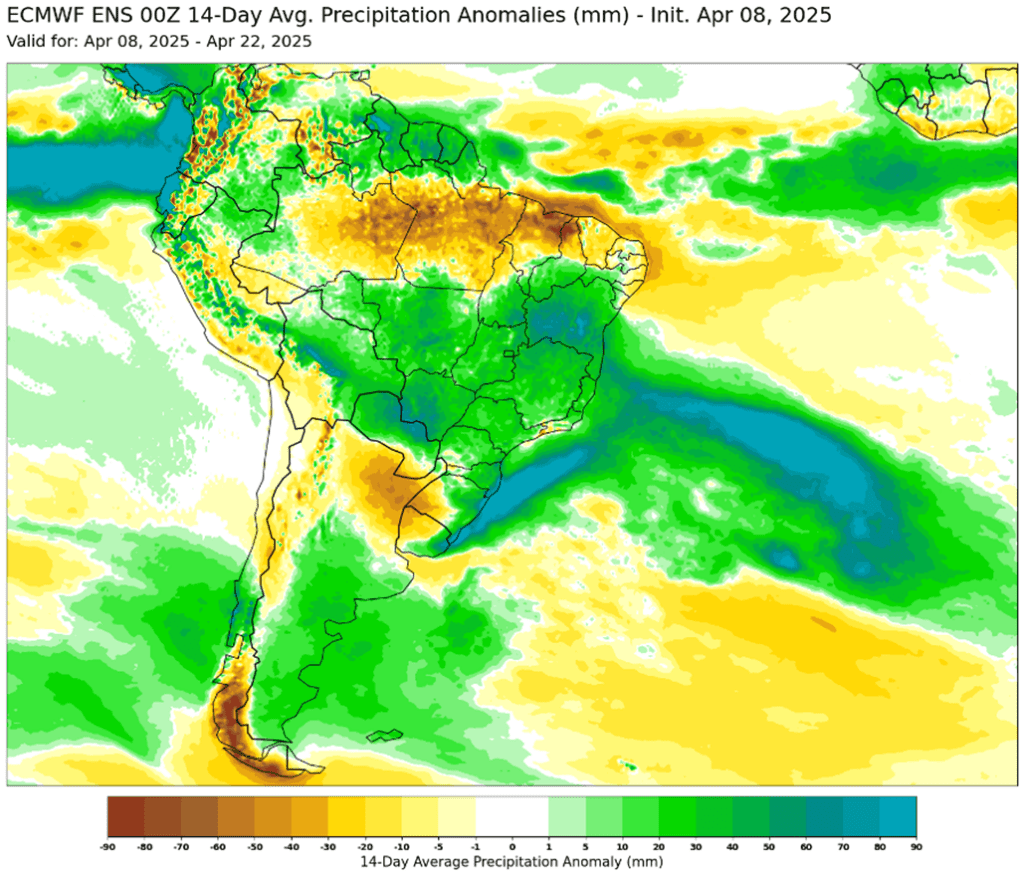

- Too see the updated 14-day ECMWF precipitation anomalies for South America, as well as the 7-day precipitation outlook for the U.S., scroll down to the other charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

Active

Sell DEC ’26 Cash

Puts

2024

No New Action

2025

No New Action

2026

No New Action

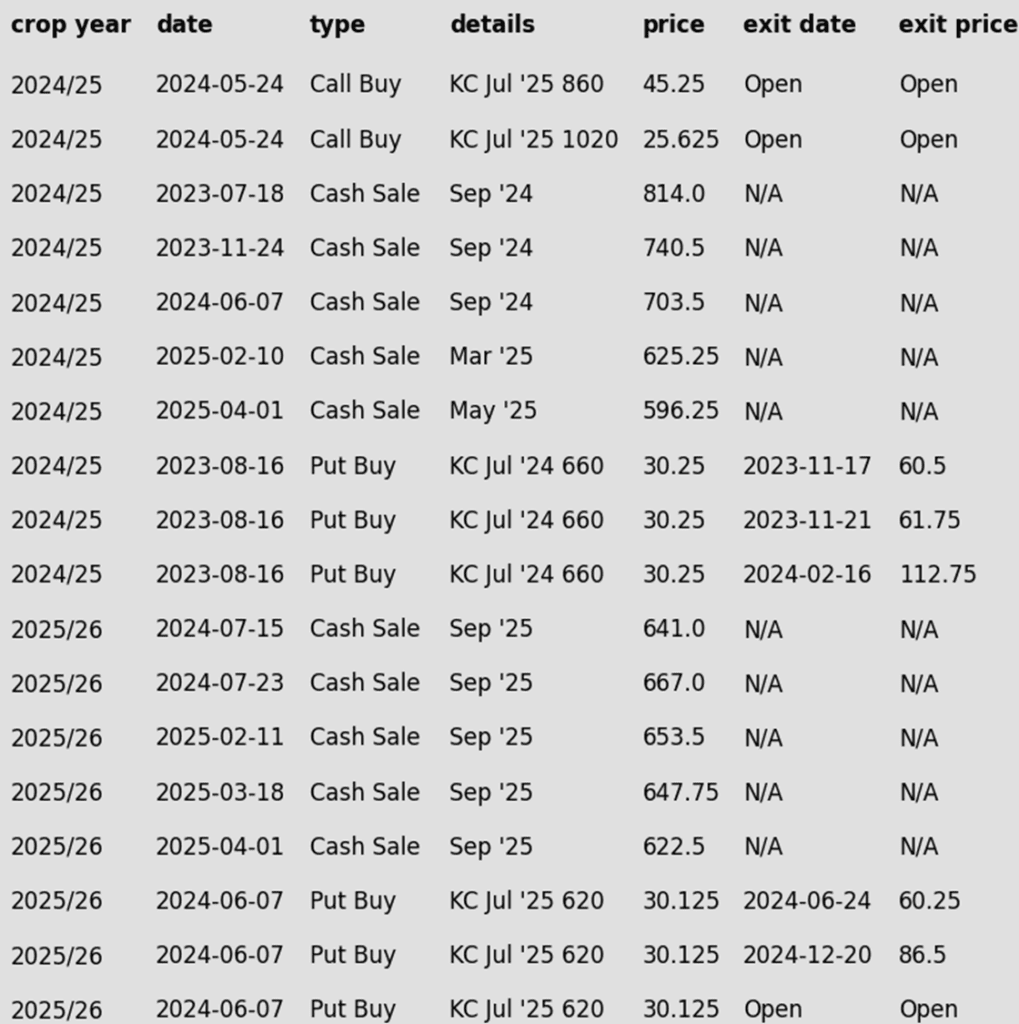

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Seven sales recommendations made so far to date.

- Catch-Up Target: If you haven’t made all seven sales to date, aim for 477 vs May as your catch-up target.

- No New Targets: Still no new recommendations for making an eighth sale. Old crop contracts continue to lead, and we’re content to remain patient for another day.

2025 Crop:

- Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

- Plan B: No active targets.

- Details:

- Sales Recs: Six sales recommendations made so far to date.

- Catch-Up Target: If you haven’t made all six sales to date, aim for 459 vs December as your first catch-up target.

- No Changes: No new sales targets have posted to trigger a seventh sale for the new crop.

2026 Crop:

- CONTINUED OPPORTUNITY – Sell a second portion of your 2026 corn crop.

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Target Hit: The move to 456 vs December ’26 triggered the current sales recommendation.

- Sales Recs: Now two sales recommendations made to date.

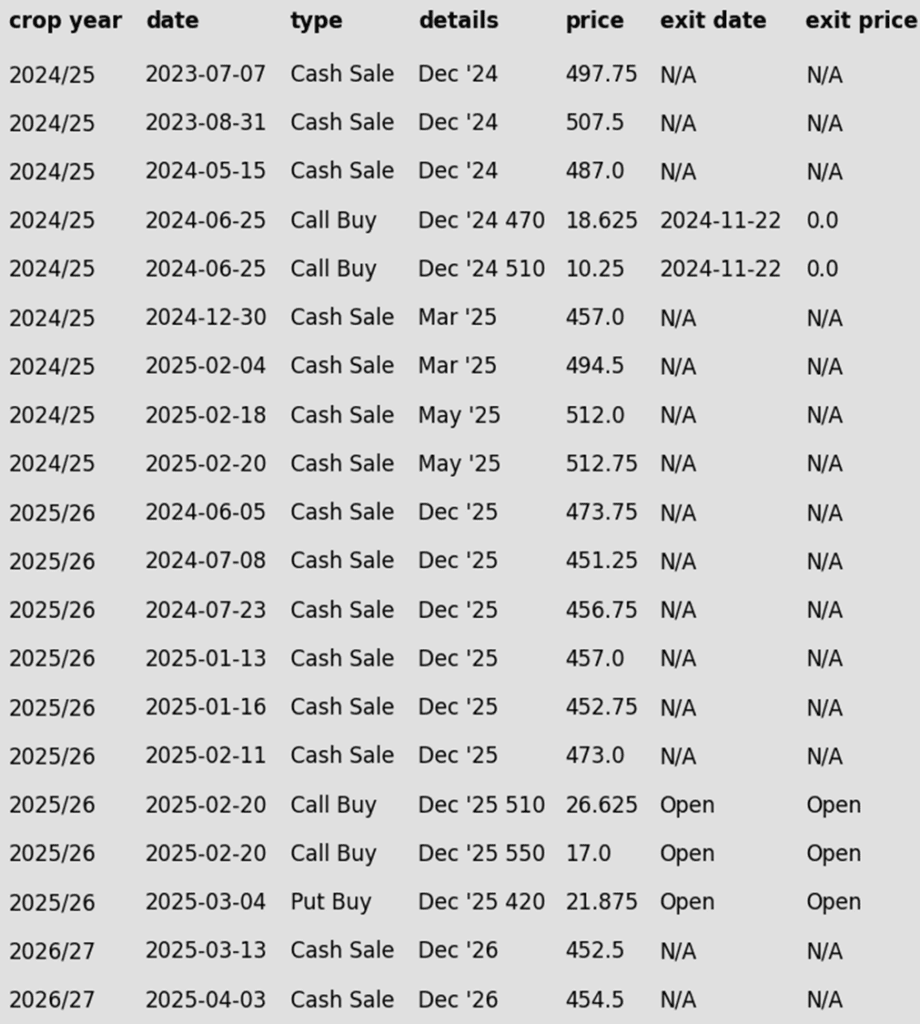

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- The corn market remained bull-spread in the Tuesday session as front-end contracts saw buying strength as deferred contracts stayed under pressure. The market is caught between robust old crop demand and uncertainty over long-term demand, driven by tariff concerns and projections for a large corn acreage this spring.

- Volatility continues to dominate trade across all markets. On Monday, the Trump administration announced a new 50% tariff on Chinese goods in response to China’s retaliatory tariff issued last Friday. The new measure is set to take effect at midnight tonight.

- USDA announced a flash sale of corn on the export market. Spain purchased 240,000MT (9.45 mb) of U.S. corn for the 2024-25 marketing year. This was the first announced flash sale of corn since March 14.

- The April WASDE report, due Thursday, could show reduced corn carryout if USDA raises export demand. However, adjustments to feed use and tariff impacts may delay major changes until later reports. Current analyst expectations are for corn carryout to be reduced to 1.510 mb, down 30 mb from the March report.

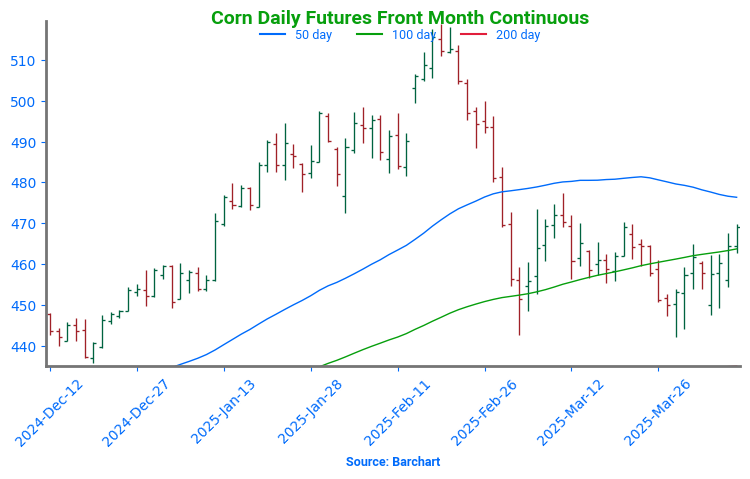

Corn Finds Support Ahead of Growing Season

After surging to 16-month highs in late February, corn futures experienced a sharp pullback, spending much of March testing key technical support levels. As spring planting approaches in earnest, futures have stabilized around the 450 level — a zone that’s likely to continue acting as near-term support into the early part of the growing season. If this area fails to hold, stronger support is expected near the 200-day moving average, currently around 430. On the upside, the first resistance comes at the 100-day moving average, followed by the March highs and the 50-day moving average near the 470 level.

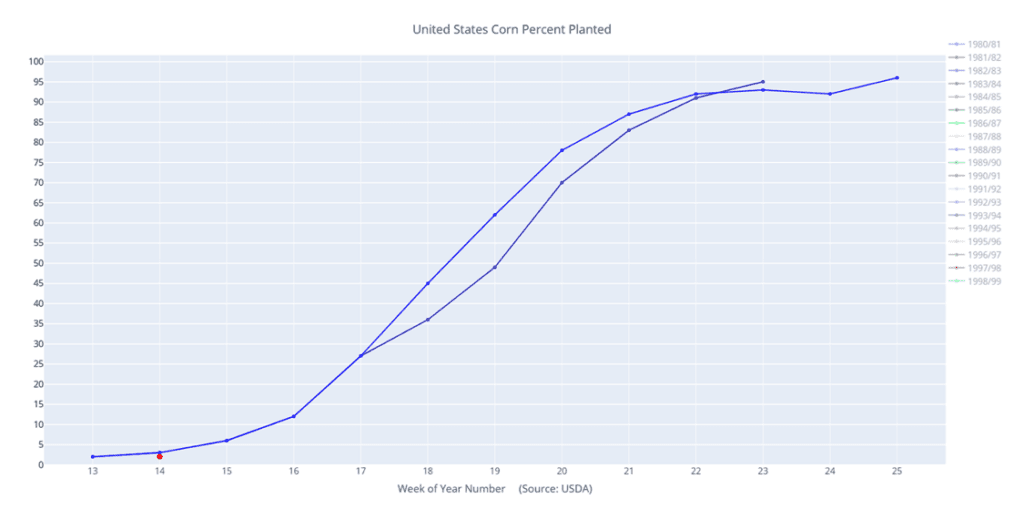

Corn percent planted (red) versus the 10-year average (blue) and last year (purple).

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: Next cash sale at 1107 vs May. Buy calls with a close over 1079.75 vs May.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made so far to date.

- No Changes: 1107 remains the target to trigger a fourth sales recommendation.

2025 Crop:

- Plan A: Next cash sales at 1093 & 1114 vs November. Exit all 1100 November call options at 88 cents.

- Plan B: No active targets.

- Details:

- Sales Recs: One sales recommendation made so far to date.

- No Changes: With one sales recommendation made to date, a move to 1093 would trigger the second, and 1114 would trigger the third.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- No Changes: The expectation is still for targets to begin posting in a month or two.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans were mixed again to end the day with the three front months higher but deferred contracts lower in more bull spreading. Equity markets initially rebounded today, which lifted all grains and livestock, but both faded into the end of the day. Soybean meal ended higher while soybean oil was lower.

- Today, the White House press secretary said that President Trump’s tariffs on China would go into effect just after midnight tonight. With the initial 20% tariffs he placed on China at the start of his term combined with the new 34% tariffs and now additional 50% tariffs as a result of China’s retaliation, this would bring China’s total tariff rate to 104%. There is optimism that an agreement can be made soon with China and all other countries.

- Yesterday’s export inspections report saw soybean inspections at 804k tons which compared to 813k the previous week and 492k tons a year ago. Primary destinations were to China, Egypt, and Mexico.

- In Brazil, a key Amazon shipping route has been disrupted by Indigenous protests and deteriorating road conditions. Global grain giants like Cargill and Bunge, which have significant operations in the region, are experiencing delays at the river port of Miritituba as a result.

Soybeans Break Lower on Tariff News

The newly announced tariffs in early April caused soybean futures to drop sharply, breaking previously held support near the 1000 level that had sustained the market throughout March. Should the decline persist, support is expected to emerge around the December lows at 950. Conversely, if prices rally, initial resistance will be encountered at the 1000 level, followed by a confluence of major moving averages between 1020 and 1030. Of these, the 200-day moving average has proven particularly challenging for the soybean market to break above, restricting gains for nearly the last year and a half.

Wheat

Market Notes: Wheat

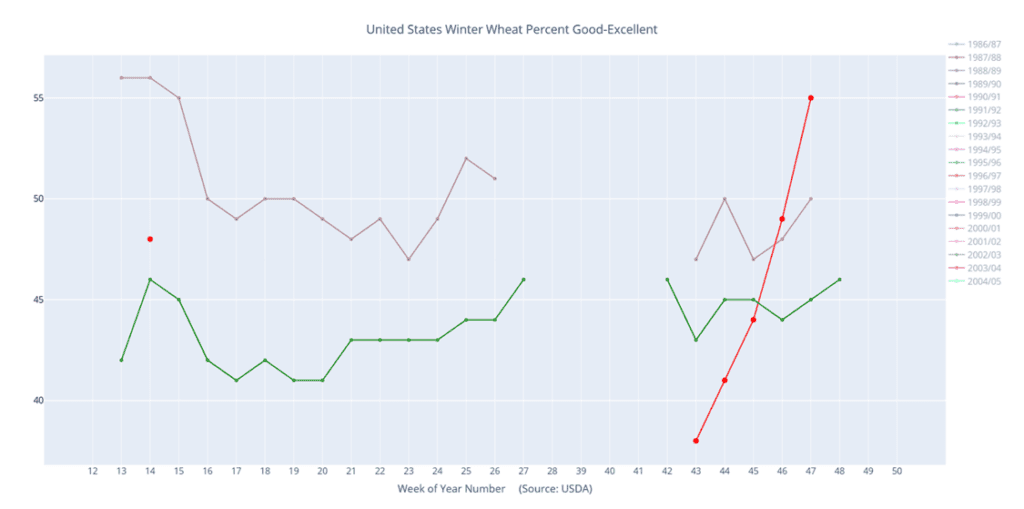

- Wheat closed with green on the screen for each class, supported by a lower US Dollar Index, higher close for Paris futures, and lower crop ratings compared with a year ago. Nationally, US winter wheat was rated 48% good to excellent, compared to 56% at this time last year, and 55% in the final November report.

- In addition to winter wheat ratings, the USDA also reported that 3% of the US spring wheat crop was planted as of April 6. This is steady with the five-year average and also in line with a year ago.

- Russia is expected to remain the top global wheatexporter through the 2024–25 season, according to Rusagrotrans. The country is projected to hold a 22% share of the global market (excluding flour), with total exports reaching 40.8 MMT.

- Argus has estimated Ukraine’s 2025–26 wheat crop at 23.7 MMT, unchanged from their November forecast. If realized, this would mark an increase from 22.3 MMT in 2024–25 and the highest output since the 2021–22 season. Projected yields for 2025–26 are 4.51 tons per hectare, above the five-year average of 4.34.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: Target 701 against May for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Four sales recommendations made so far to date.

- No Changes: 701 is still the price target to trigger a fifth sales recommendation.

2025 Crop:

- Plan A: Target 705.50 against July for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made so far to date.

- No Changes: Still targeting 705.50 to trigger the sixth sales recommendation.

2026 Crop:

- Plan A: Target 704 against July ‘26 for the next sale

- Plan B: No active targets.

- Details:

- Sales Recs: One sales recommendation made so far to date.

- No Changes: 704 is still the price target to trigger a second sales recommendation.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat – Back to Sideways Trend

After months of sideways movement, Chicago wheat broke higher in February, rallying to early October highs just above 615. However, this mid-month peak quickly turned into a reversal point, with futures sliding back into the trading range that defined late 2024. Currently, support near 530 continues to hold firm. The next major resistance is the 200-day moving average, which now represents a critical test. A decisive weekly close above this level could signal a shift in momentum, potentially marking the beginning of a trend reversal and a return to upside momentum.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made so far to date.

- No Changes: Still no active price targets, as the May contract continues to try forming a base in the 550–570 range.

2025 Crop:

- Plan A: Target 677 against July for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made so far to date.

- No Changes: 677 is still the price target to trigger a sixth sales recommendation.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- No Changes: The expectation is still for targets to begin posting in the May – June timeframe.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Seeks Direction After February Whiplash

February was a wild ride for Kansas City wheat, with prices surging higher before tumbling back down, ultimately finishing the month little changed. March ended with weakness, bringing prices back near recent lows, but holding trendline support so far in April remains encouraging. On a rebound, the 200-day moving average is expected to act as initial resistance, with February highs near 640 serving as a more significant barrier. Support near the December lows of 540 should act as stout support on any continued decline.

Winter wheat condition percentage good-excellent (red) versus the 5-year average (green) and last year (purple).

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

Active

Sell MAY ’25 Cash

2025

Active

Sell SEP ’25 Cash

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- CONTINUED OPPORTUNITY – Sell another portion of your 2024 HRS crop. This marks the fifth sales recommendation to date and brings the average sales price to 695.

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Four sales recommendations were made prior to last week. With the current recommendation, this marks the fifth sales recommendation for the 2024 crop.

2025 Crop:

- CONTINUED OPPORTUNITY – Sell another portion of your 2025 HRS crop. This marks the fifth sales recommendation to date and brings the average sales price to 646.

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Four sales recommendations were made prior to last week. With the current recommendation, this marks the fifth sales recommendation for the 2025 crop.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- No Changes: The expectation is still for targets to begin posting in the June – July timeframe.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Hovers Near Support

Spring wheat broke out of its long-standing sideways range in late January, triggering a surge of bullish momentum. The rally gained further traction in mid-February with a close above the 200-day moving average, but late-month weakness wiped out those gains, pushing futures back below key technical levels. Currently, the 200-day moving average acts as a barrier, limiting any rebound attempts, while support near 580 remains crucial in preventing further downside. To reignite the uptrend, futures would need to make a sustained move above the 200-day, with the next upside target at the February highs near 660. With spring wheat acreage expected to be the lowest in the past 55 years, weather volatility is likely to play a significant role in market movements.

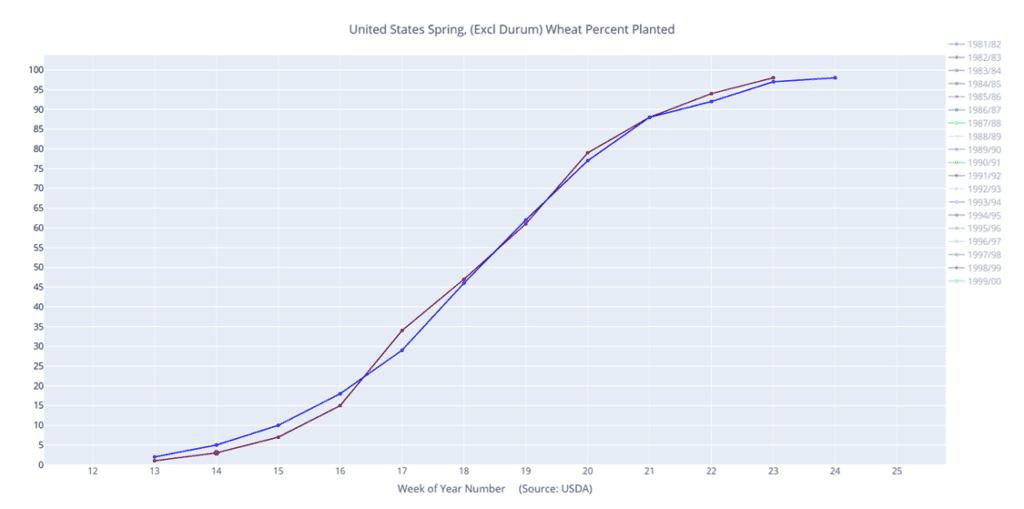

Spring wheat percentage planted (red) versus the 10-year average (blue) and last year (purple).

Other Charts / Weather

Courtesy of ag-wx.com

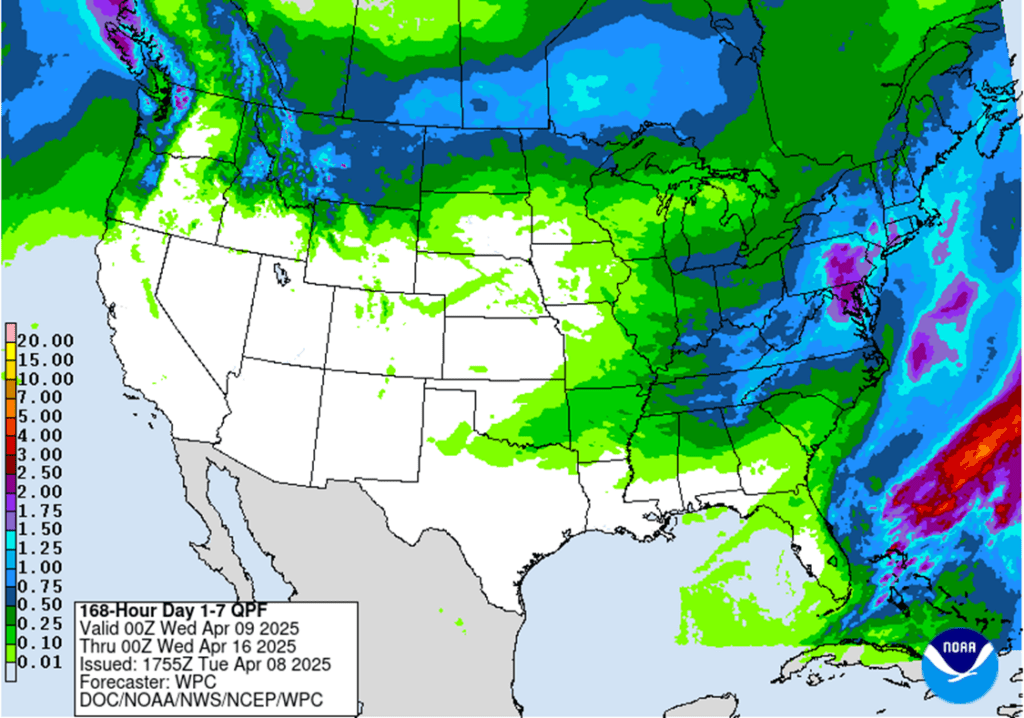

US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Courtesy of ag-wx.com