4-29 End of Day: Midwestern Rains Pressure Chicago Wheat and Corn; Soybean Meal Supports Beans

All prices as of 2:00 pm Central Time

| Corn | ||

| MAY ’24 | 439.25 | -0.75 |

| JUL ’24 | 449.25 | -0.75 |

| DEC ’24 | 472.75 | -0.75 |

| Soybeans | ||

| MAY ’24 | 1160.75 | 1.25 |

| JUL ’24 | 1182 | 4.75 |

| NOV ’24 | 1178 | 3.25 |

| Chicago Wheat | ||

| MAY ’24 | 590.25 | -13 |

| JUL ’24 | 608.5 | -13.75 |

| JUL ’25 | 681.25 | -6.25 |

| K.C. Wheat | ||

| MAY ’24 | 643.75 | -2.5 |

| JUL ’24 | 650.5 | -3.75 |

| JUL ’25 | 687.75 | 0.5 |

| Mpls Wheat | ||

| MAY ’24 | 715.25 | 18 |

| JUL ’24 | 707.75 | 4.25 |

| SEP ’24 | 714 | 4 |

| S&P 500 | ||

| JUN ’24 | 5135.5 | 4 |

| Crude Oil | ||

| JUN ’24 | 82.65 | -1.2 |

| Gold | ||

| JUN ’24 | 2350.6 | 3.4 |

Grain Market Highlights

- Weakness in Chicago wheat and the potential effect of First Notice Day kept the corn market in a choppy 4 ¼ cent range that limited any potential upside influence from the soybean market.

- Soybeans also saw choppy two sided trade as they were caught between sharply higher soybean meal and sharply lower soybean oil. The overall gain in meal not only supported soybeans, but also expressed itself in a 3 ½ cent gain in July Board crush.

- A Bloomberg report noting a surge of alternative feedstocks for biofuel use may have been the catalyst for the sharply lower trade in soybean oil today, as it points to potentially much lower soybean oil demand than previously thought. Conversely, a strike in one of Argentina’s largest ag export ports likely led to today’s surge in soybean meal, as it could lead to higher US soybean meal demand.

- Chicago wheat, influenced by recent rains in the Midwest and in the dry areas of southern Russian, led the winter wheats lower, while potential spring wheat planting delays lent support to Minneapolis contracts.

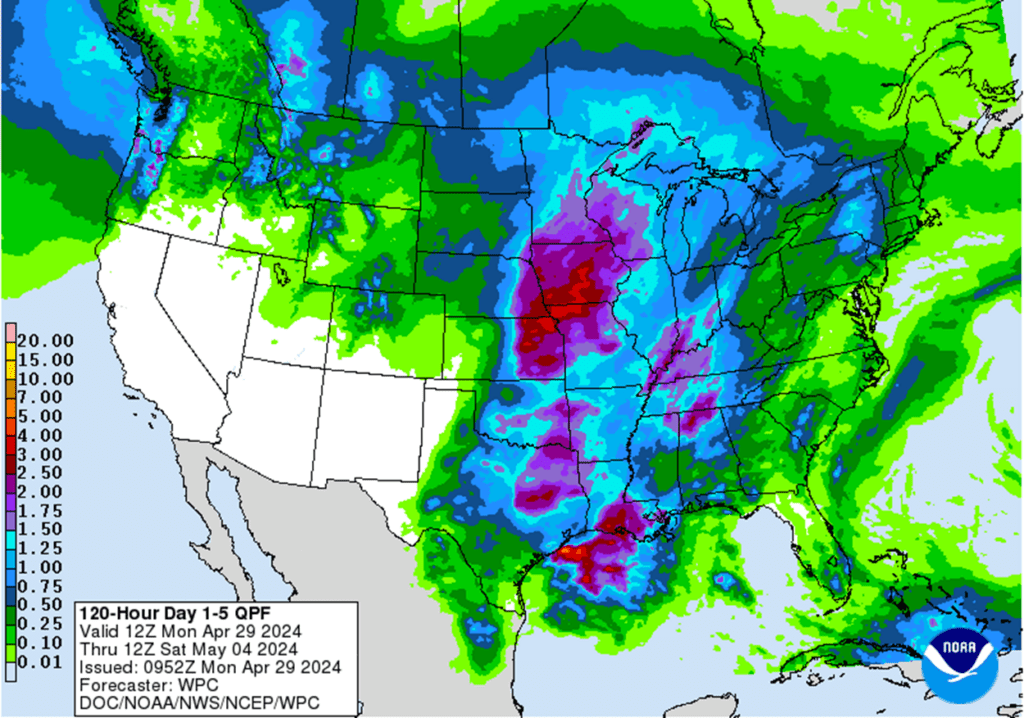

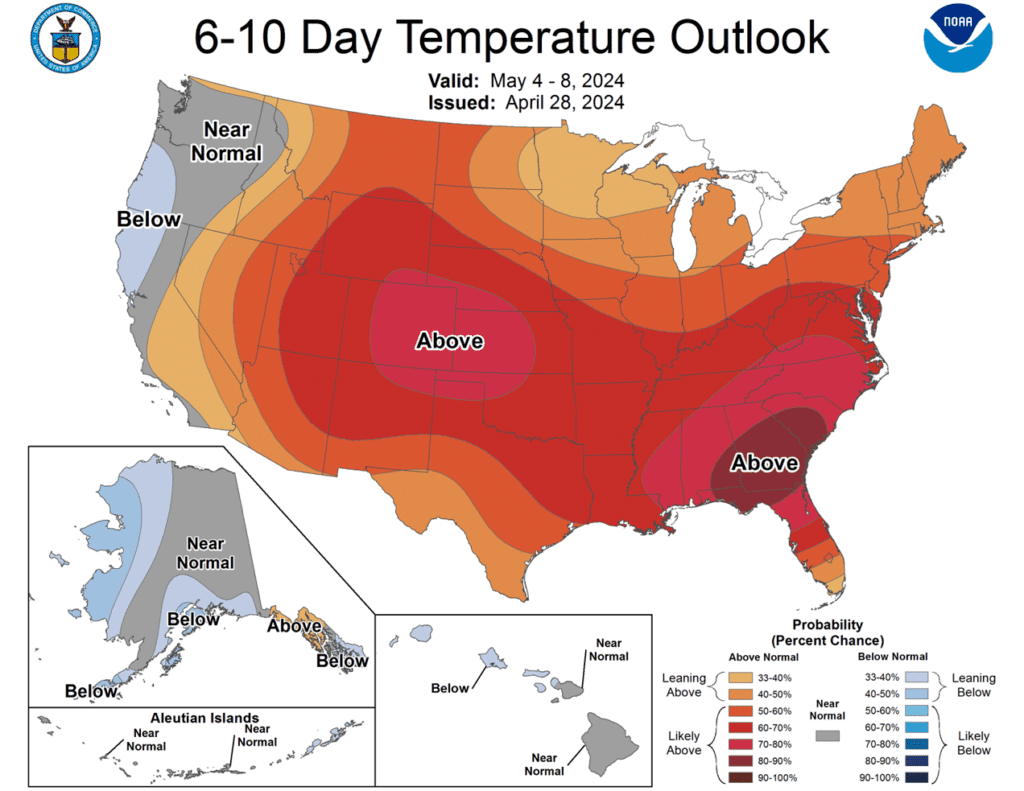

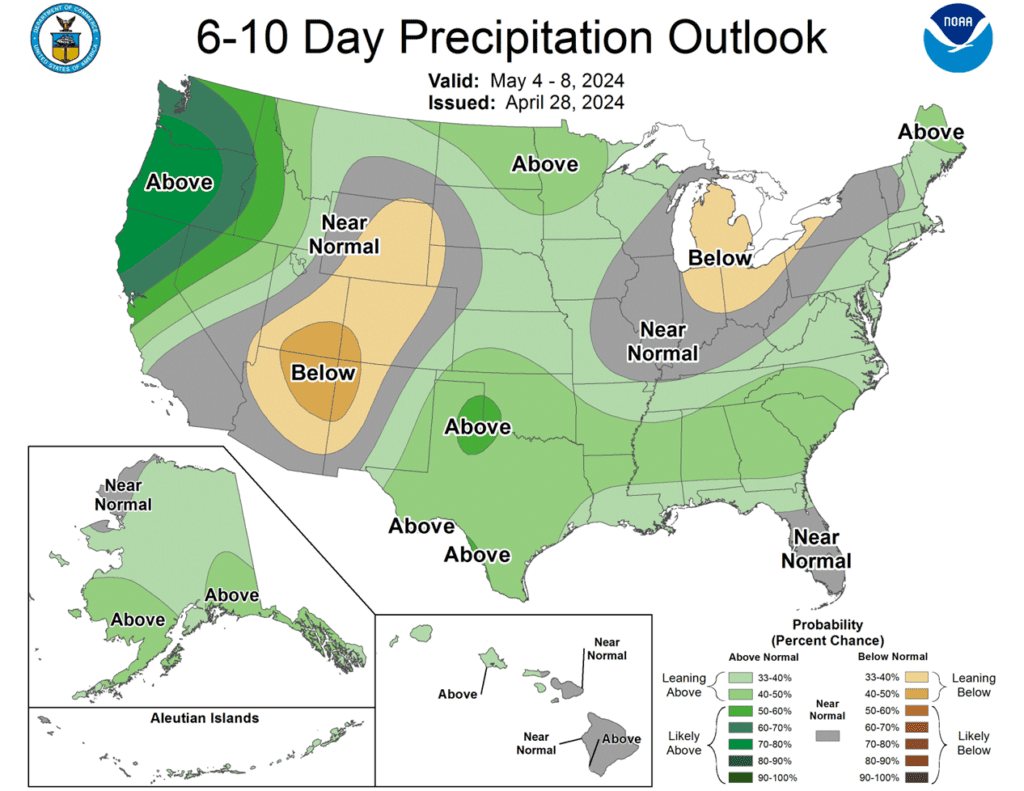

- To see the updated US 5-day precipitation forecast, US 6 – 10 day Temperature and Precipitation Outlooks, and 1-week precipitation forecast for Brazil and N. Argentina courtesy of NOAA and The Climate Prediction Center scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

Although July ’24 corn has rallied beyond the congestion range on the front month continuous charts, it remains below its high of 460 that was posted on March 28. With little fresh bullish fundamental news, managed funds have maintained a significant net short position. While the fund’s large net short position likely sparked the recent rise in prices and could fuel a more significant upside move as we move through planting and into the growing season, the market now shows signs of being overbought, which could add resistance to higher prices. Despite potential obstacles along the way, overall market conditions and seasonal tendencies remain conducive to a continued price recovery into May and June.

- No new action is recommended for 2023 corn. The target range to make additional sales is 480 – 520 versus May ’24 futures. If you need to move bushels for cash or logistics reasons, consider re-owning any sold bushels with September call options.

- No new action is recommended for 2024 corn. We are targeting 520 – 560 to recommend making additional sales versus Dec ‘24 futures. For put option hedges, we are looking for 500 – 520 versus Dec ‘24 before recommending buying put options on production that cannot be forward priced prior to harvest.

- No Action is currently recommended for 2025 corn. At the beginning of the year, Dec ’25 corn futures left a gap between 502 ½ and 504 on the daily chart. Considering the tendency for markets to fill price gaps like these, we are targeting the 495 – 510 area to recommend making additional sales.

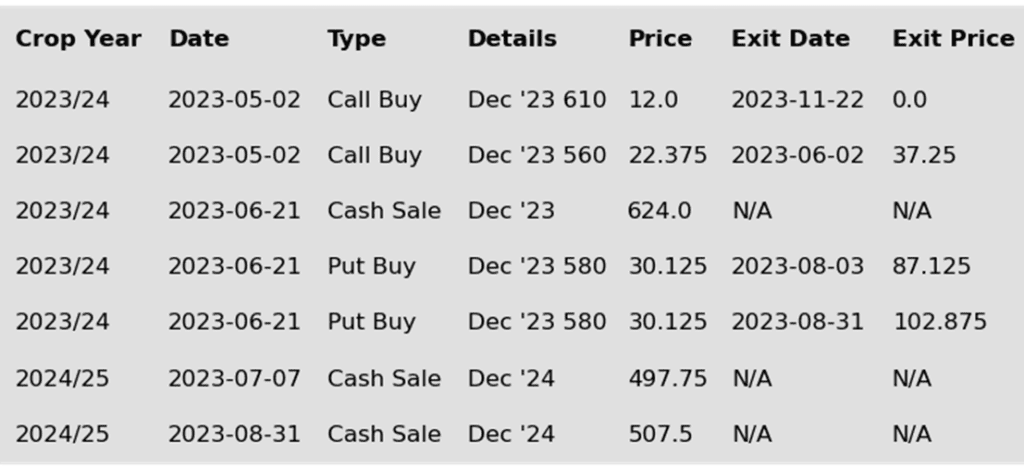

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- The influence of First Notice Day for the May contract and selling in the SRW wheat market limited gains in the corn market, as it remains rangebound with choppy trade.

- The USDA will release the latest round of crop progress numbers this afternoon, with expectations for corn planting to be 27% complete, up 15% from last week. This will keep the planting pace head of the 5-year average. Expectations are for a large jump in planting progress to have occurred in western and southern areas.

- Planting pace is expected to slow over the next couple weeks. Weather models are forecasting rounds of precipitation to push through the corn belt, which could limit planting until the middle of May.

- This morning, the USDA released weekly export inspections. Last week US exporters inspected 48.3 mb (1.226 mmt) of corn for export, below the previous week’s total. Cumulative export inspections now total 1.245 billion bushels, which is 32% ahead of last year’s pace.

- On Friday’s Commitment of Traders Report, managed funds reduced their net short position in the corn market to 238,546 net short corn contracts as of April 23, a reduction of 41,024 from the previous week.

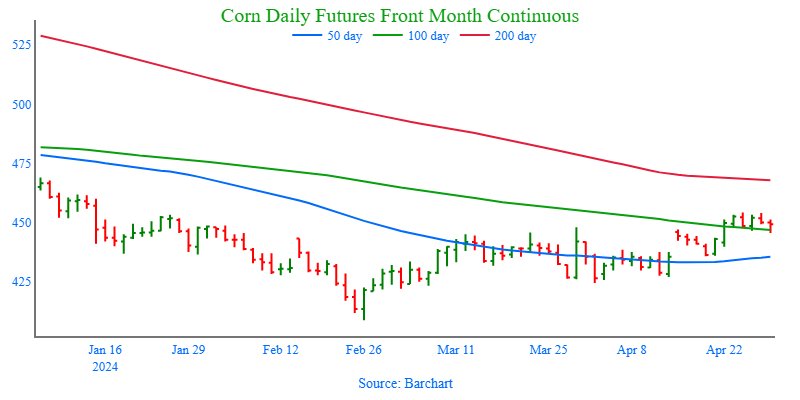

Above: The corn market continues to struggle to rally with overhead resistance remaining around 460 in the July contract. A breakout above there could allow prices to test the 495 – 510 area. If prices break to the downside and close below 421, they could slide further to test 400 – 410 support.

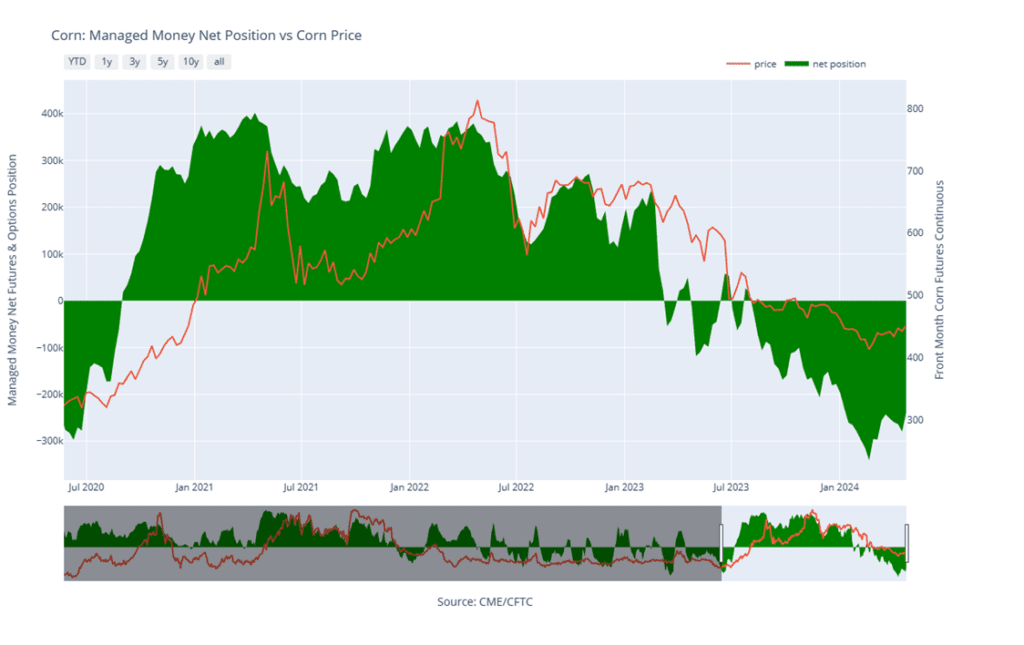

Corn Managed Money Funds net position as of Tuesday, Apr. 23. Net position in Green versus price in Red. Managers net bought 41,024 contracts between Apr. 17 – 23, bringing their total position to a net short 238,546 contracts.

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

In mid to late April soybeans posted an intermediate low and a bullish reversal with some subsequent short covering which rallied the market back toward early April’s congestion area. While that initial rally was limited, and the current supply/demand situation remains somewhat bearish, Managed funds remain short about 149,000 contracts according to the latest Commitment of Traders report. This could still fuel an extended short covering rally should any production concerns arise in the coming weeks. Otherwise, if weather conditions cooperate and planting progresses without major issues, prices could remain susceptible to revisiting recent lows throughout the spring.

- No new action is recommended for 2023 soybeans. We are currently targeting a rebound to the 1275 – 1325 area versus May ’24 futures to recommend making further sales. If you need to move inventory for cash or logistics reasons, consider re-owning any sold bushels with September call options.

- No new action is recommended for the 2024 crop. Considering the amount of uncertainty that lies ahead with the 2024 soybean crop, we recommended back in December buying Nov ’24 1280 and 1360 calls to give you confidence to make sales against anticipated production and to protect any sales in an extended rally. We are currently targeting the 1280 – 1320 range versus Nov ’24 futures, which is a modest retracement toward the 2022 highs, to recommend making additional sales.

- No Action is currently recommended for 2025 Soybeans. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

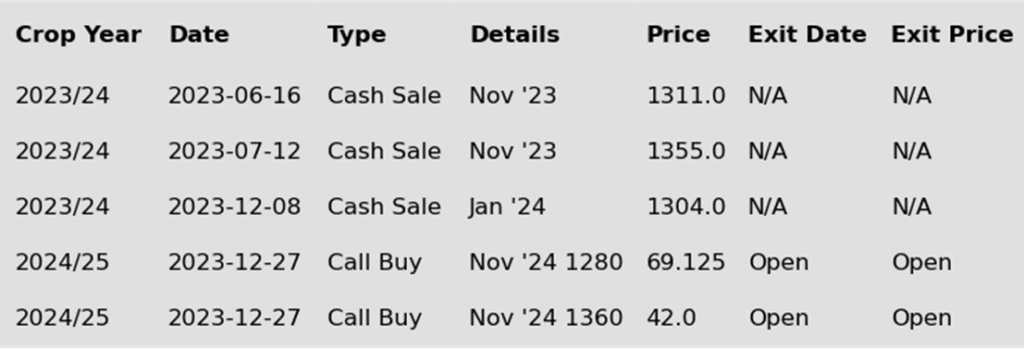

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day higher thanks to an impressive showing from soybean meal which saw the July futures up $9.60 which was a gain of 2.79%. July soybean futures once again rallied up to their 40-day moving average but failed and drifted lower into the day. Soybean oil was sharply lower.

- A bearish factor for soybean oil and other veg oils has been a surge in imports of used cooking oil for the use of biofuel production in the US. Bringing in this cheap imported oil has reduced profits for soybean processors which has caused crushing to slow and may cause a change in plans to expand processing plants. There has been a lot of optimism that the increased use of biodiesels would support the soy complex, but this development may exert an adverse effect.

- For the week ending Thursday, April 18, the USDA reported that soybean inspections totaled 9.2 mb. This was within the range of trade expectations but below last week’s, which were 16.3 mb. Total inspections for 23/24 are now at 1.424 billion bushels, which is down 18% from the previous year.

- The US share of Chinese imports has significantly fallen as both Argentina and Brazil continue to put out larger crops each year lessening the need for US purchases. Chinese imports from the US are expected to fall by 24% with Argentina picking up that business.

- In Argentina, the world’s largest soybean meal exporter, a strike was called by the oilseed workers’ union at the country’s largest agricultural export port to begin today. The strike is to protest against the government’s labor reforms and new taxes. It is said that the strike would also affect 80% of the companies that use the port.

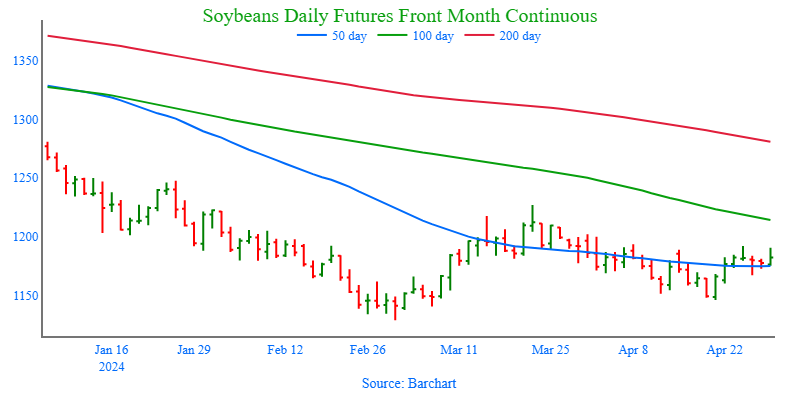

Above: Since posting a bullish reversal on April 19, the market has struggled to stay above 1190. A close above the April 24, 1191 ¾ high could allow the market to run and test the 1227 March high. Otherwise, support below the market remains between 1145 and 1140, if prices slide back toward key support and the February low of 1128 ½.

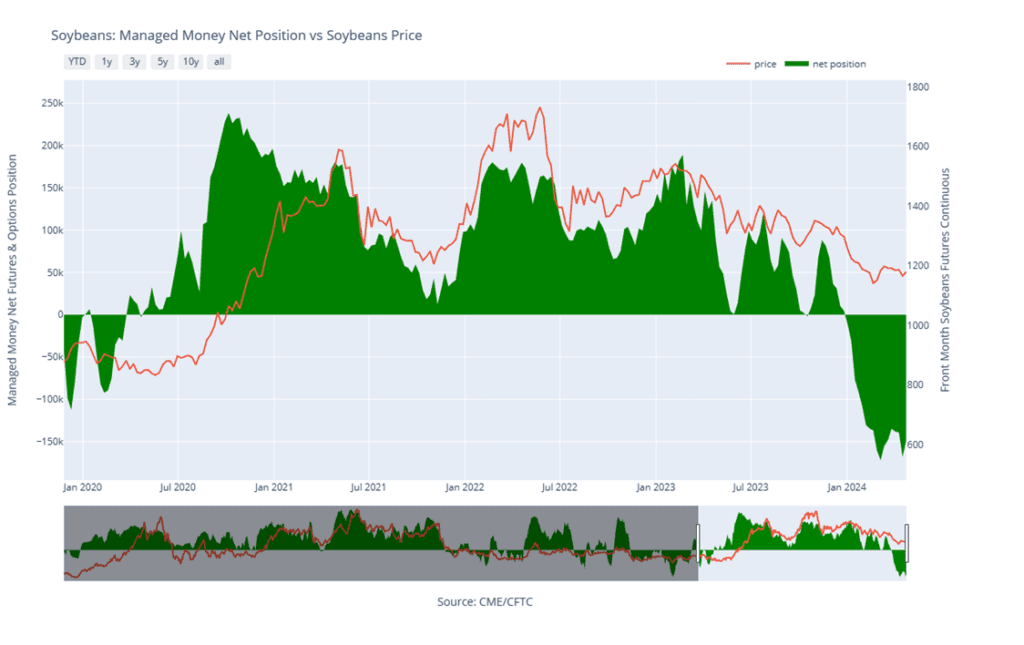

Soybean Managed Money Funds net position as of Tuesday, Apr. 23. Net position in Green versus price in Red. Money Managers net bought 18,891 contracts between Apr. 17 – 23, bringing their total position to a net short 149,014 contracts.

Wheat

Market Notes: Wheat

- Wheat closed mixed, with pressure on Chicago and KC futures, but gains in Minneapolis. Weakness for the SRW wheat stemmed from recent rains in the US Midwest, as well as the potential for some of the drier areas of southern Russia to receive limited moisture this week. A lower close in Matif wheat also weighed on the US market.

- Weekly wheat export inspections of 17.7 mb bring the 23/24 total to 622 mb. Inspections are slightly ahead of the pace needed to meet the USDA’s goal.

- Australia was mostly dry over the weekend, but eastern areas may see storms later this week and into the weekend. While their wheat planting continues to move forward, more moisture is needed, so this system will be beneficial if rain does develop.

- Russia’s state weather forecaster indicates the potential continuation of drought conditions in some of their vital wheat-growing regions until mid-May. While conditions are projected to be relatively average for most of the European part of Russia, concerns arise for the eastern part of the Southern Federal District, where a lack of moisture may impact winter crops.

- The New Zealand National Institute for Water and Atmospheric Research has said they expect El Nino to ease by June, with La Nina expected to form between July and September. Some forecasters have already said that El Nino is fading, but most are in agreement that La Nina weather conditions will develop in mid to late summer in the northern hemisphere.

Action Plan: Chicago Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Chicago Wheat Action Plan Summary

After holding downside support near 550, Chicago wheat staged a rally, likely fueled by Managed fund short covering and HRW crop concerns, that has taken it through the major moving averages on the continuous chart, and towards last Decembers highs. Although bearish fundamentals remain, and the market shows signs of being overbought which adds downside risk, Managed funds quite possibly still hold a large net short position that has the potential to drive an extended short covering rally should any crop more concerns arise as we enter the more dynamic part of the growing season.

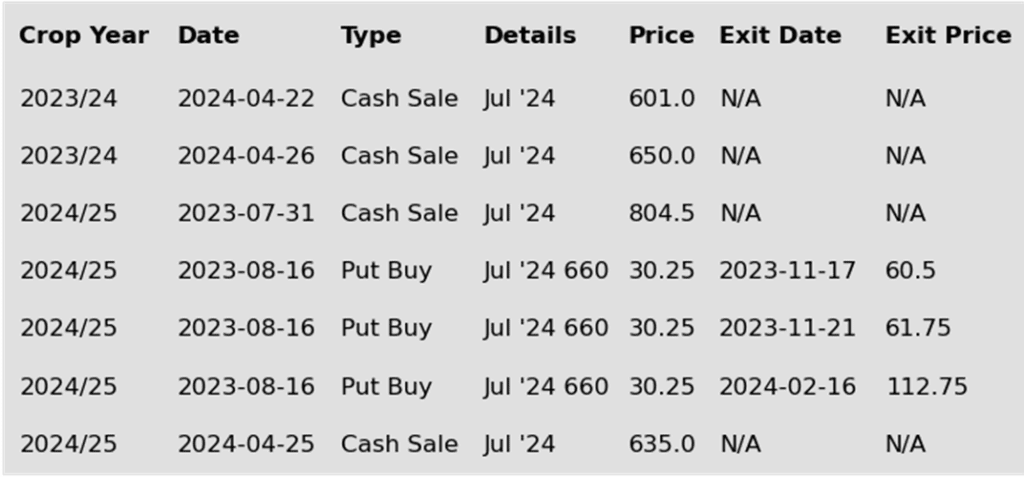

- No new action is currently recommended for 2023 Chicago wheat. Any remaining 2023 soft red winter wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 Chicago wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

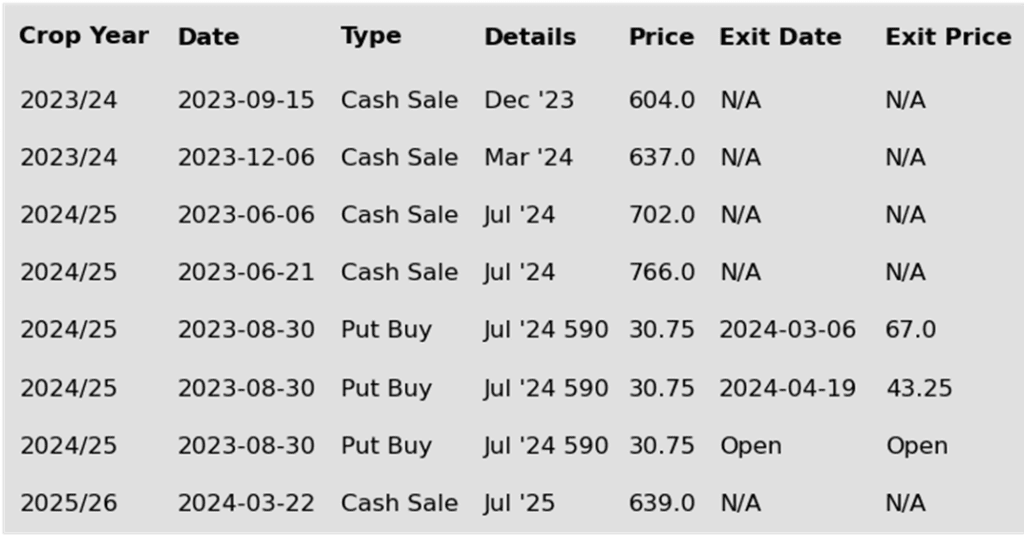

- No new action is recommended for 2024 Chicago wheat. Back in August we recommended buying July ’24 590 puts to prepare for further price erosion. Since then, we recommended exiting half of the original position to get closer to a net neutral cost, and then most recently, we recommended exiting another half of the remaining position to lock in further gains in case prices continue higher, leaving 25% of the original position in place. We continue to target a market rebound back towards 675 – 715 versus July ’24 futures before recommending any additional sales. As for the open July ’24 590 put position, we are looking for prices between 475 – 500 versus July ’24 futures to before we recommend exiting any of the last 25%.

- No new action is currently recommended for 2025 Chicago Wheat. We recently recommended initiating your first sales for the 2025 SRW crop year as prices pressed back toward the mid-600 range to take advantage of historically good prices for next year’s crop. Since plenty of time remains to market this crop, we are looking for further price appreciation and are currently targeting the 690 – 725 area to recommend making additional sales.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

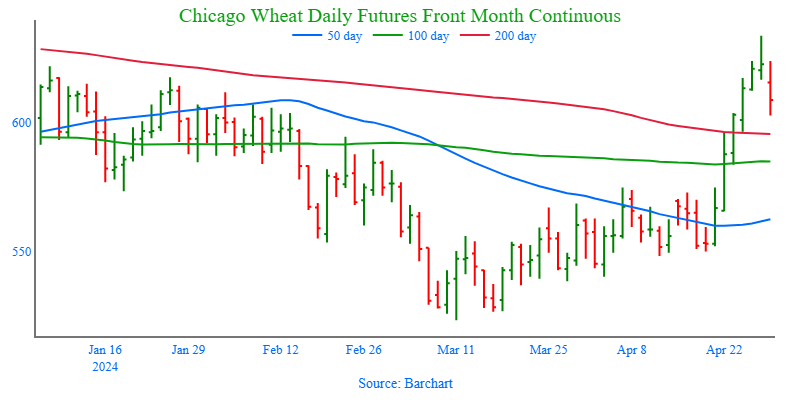

Above: July Chicago’s close above the 200-day MA opens the door to test the December high of 630. On the downside, if prices retreat, initial support is likely around 575 and the 50-day moving average (currently 562).

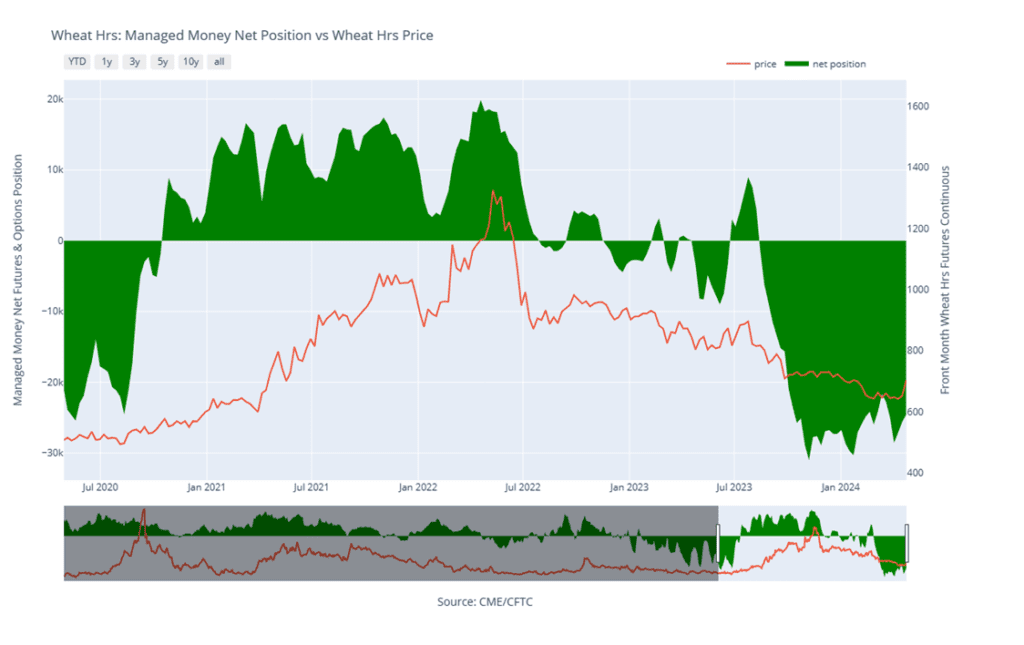

Chicago Wheat Managed Money Funds net position as of Tuesday, Apr. 23. Net position in Green versus price in Red. Money Managers net bought 20,219 contracts between Apr. 17 – 23, bringing their total position to a net short 76,184 contracts.

Action Plan: KC Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

Active

Sell JUL ’24 Cash

2024

Active

Sell JUL ’24 Cash

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

KC Wheat Action Plan Summary

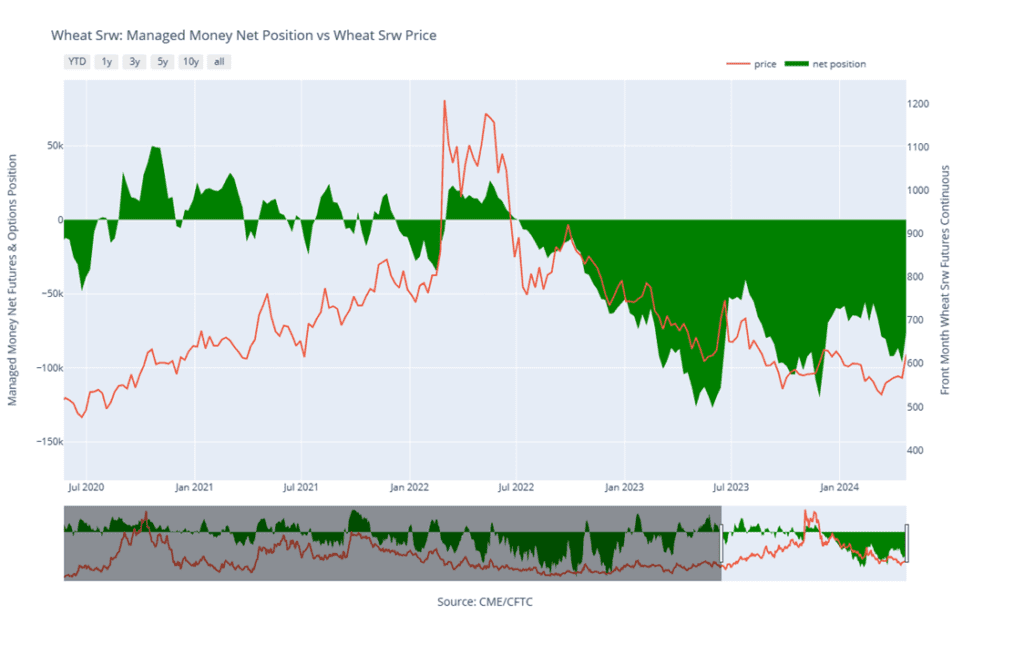

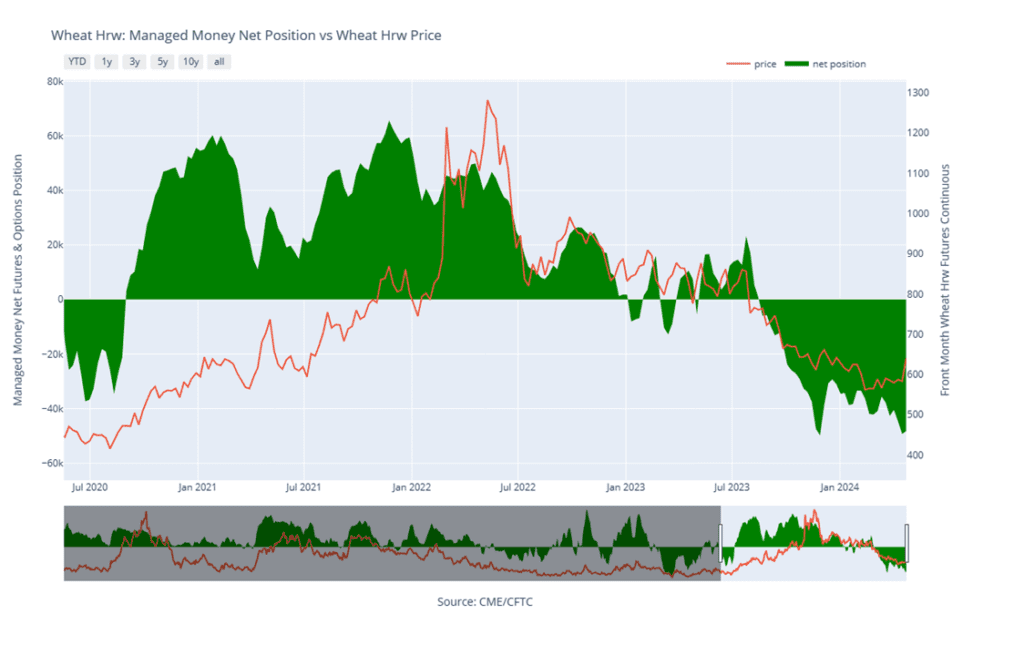

Between the end of February and the middle of April, KC wheat was mostly rangebound between the mid 590’s on the topside and mid 550’s down low, with little to move prices higher. All the while Managed funds continued adding to their large net short positions. Toward the end of April, dryness in the Black Sea region and the US HRW growing areas started becoming more concerning and triggered a short covering rally across the wheat complex, driving prices to levels not seen since last December. While low world export prices continue to be a drag on US demand and prices, and it is likely that Managed funds covered a significant portion of their net short positions, it is also quite possible that they remain short the market. Which could still push prices higher if production concerns persist.

- Grain Market Insider sees a continued opportunity to sell a portion of your 2023 HRW wheat production. Dryness in the Southwestern Plains and Russia, along with elevated geopolitical tensions in the Middle East and Black Sea spurred Managed funds to cover some of their extensive short positions in the wheat complex. As a result, the July ’24 KC wheat futures contract is about 50 cents higher than our previous old crop sales recommendation, and near both the 200-day moving average and the resistance area of last December’s highs. Considering this rally may primarily be weather driven and could be short-lived, as well as being limited on time before the 2024 crop is harvested, we advise you to take advantage of these elevated prices to sell another portion of your 2023 HRW wheat inventory.

- Grain Market Insider sees a continued opportunity to sell a portion of your 2024 HRW wheat production. Since the end of July, the wheat market has been in a downtrend with no significant selling opportunities, while many uncertainties remain that could drive prices even higher. The market is now approximately 90 cents off the March low and entering an area of heavy resistance that coincides with a 25% retracement of the recent downtrend back toward the July high. Grain Market Insider recommends taking advantage of this rally to make an additional sale on your 2024 crop.

- No action is currently recommended for 2025 KC Wheat. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

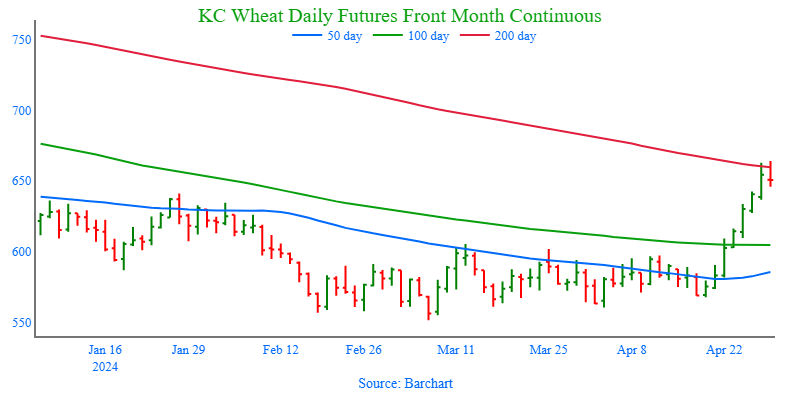

Above: The market’s ability to close above the 610 – 640 congestion area puts it on track to further test overhead resistance in the 678 – 700 area. Should the market fall back, initial support may be found near 640 and again between 605 and 551 ½.

KC Wheat Managed Money Funds net position as of Tuesday, Apr. 23. Net position in Green versus price in Red. Money Managers net bought 1023 contracts between Apr. 17 – 23, bringing their total position to a net short 48,208 contracts.

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

Active

Sell JUL ’24 Cash

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

Between mid-February and much of April Minneapolis wheat traded mostly sideways to lower with little bullish fundamental news to drive prices higher. In late April, driven by world wheat crop concerns and dryness in the HRW growing areas, and fueled by likely Managed fund short covering, Minneapolis wheat rallied back toward the January highs. Although bullish fundamentals remain scarce, and the market shows signs of being overbought, historical seasonal trends typically strengthen as we approach late spring and early summer. Furthermore, Managed funds quite possibly still hold a net short position, that could fuel an extended rally if more production concerns arise.

- Grain Market Insider sees a continued opportunity to sell a portion of your 2023 Spring wheat crop. Since the end of July, the wheat market has been in a downtrend due to lower world prices, with no significant rallies to take advantage of. While many unknowns remain that could move prices even higher, the market is now more than 50 cents off its low and entering an area of heavy resistance that coincides with a 23% retracement back to the July high. Grain Market Insider advises taking advantage of this rally, and these still historically good prices, to make an additional sale on your 2023 crop.

- No new action is recommended for 2024 Minneapolis wheat. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts (due to their higher liquidity and correlation to Minneapolis), to protect the downside, and recommended exiting the original position in three separate tranches as the market got further extended into oversold territory to protect any gains that were made. The current strategy is targeting the 775 – 815 area versus Sept ’24 to recommend making additional sales. We are also targeting the 850 – 900 area to recommend buying upside calls to help protect any sales that would have been made.

- No action is currently recommended for the 2025 Minneapolis wheat crop. We are currently not considering any recommendations at this time for the 2025 crop that will be planted in the spring of next year. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: The market’s test of the 700 – 712 area has put it into overbought territory and is at risk of falling back. Should this occur, initial support may come between 675 and 660, with further support down toward 632 and 625 ¼. Conversely, if prices close above 712 and continue toward the November high of 752, they may encounter more resistance between 725 and 735.

Minneapolis Wheat Managed Money Funds net position as of Tuesday, Apr. 23. Net position in Green versus price in Red. Money Managers net bought 1,042 contracts between Apr. 17 – 23, bringing their total position to a net short 24,556 contracts.

Other Charts / Weather

Above: US 5-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

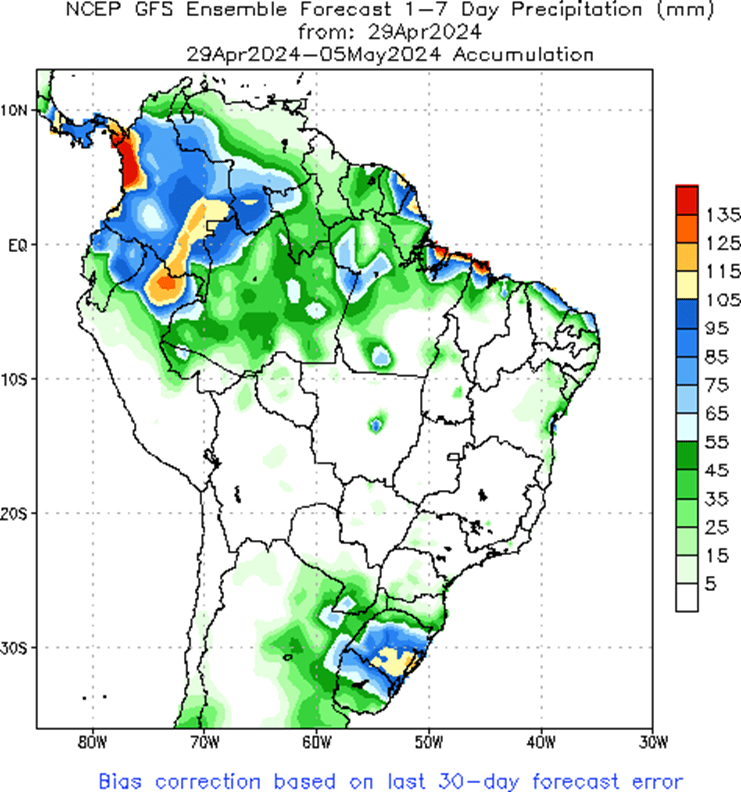

Brazil and N. Argentina 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.