4-26 End of Day: Mixed Close as Wheat Continues Higher with Corn and Beans Lower

All prices as of 2:00 pm Central Time

| Corn | ||

| MAY ’24 | 440 | -1 |

| JUL ’24 | 450 | -2 |

| DEC ’24 | 473.5 | -2.75 |

| Soybeans | ||

| MAY ’24 | 1159.5 | -3.25 |

| JUL ’24 | 1177.25 | -2.5 |

| NOV ’24 | 1174.75 | -0.75 |

| Chicago Wheat | ||

| MAY ’24 | 603.25 | 1 |

| JUL ’24 | 622.25 | 1.75 |

| JUL ’25 | 687.5 | 5 |

| K.C. Wheat | ||

| MAY ’24 | 646.25 | 14.25 |

| JUL ’24 | 654.25 | 13.75 |

| JUL ’25 | 687.25 | 11.25 |

| Mpls Wheat | ||

| MAY ’24 | 697.25 | 6.25 |

| JUL ’24 | 703.5 | 5.25 |

| SEP ’24 | 710 | 5.25 |

| S&P 500 | ||

| JUN ’24 | 5136.5 | 54.25 |

| Crude Oil | ||

| JUN ’24 | 83.69 | 0.12 |

| Gold | ||

| JUN ’24 | 2352 | 9.5 |

Grain Market Highlights

- Corn closed just off the day’s low following choppy two sided trade that continued to consolidate in narrow range from Tuesday, with today’s May options expiration possibly contributing to the late day weakness.

- Soybeans also saw choppy back and forth trade in a rather tight 8 ½ cent range that closed just above the 20-day moving average. Weakness in soybean meal with likely profit taking from the week added resistance.

- The wheat complex ended the week strong with gains seen across the board for the sixth consecutive day. Overbought conditions and strength in the US dollar may have contributed to the weakness in the Chicago contracts, which closed the day well off their highs. While concerns for further dryness in the HRW growing areas helped support KC into the close.

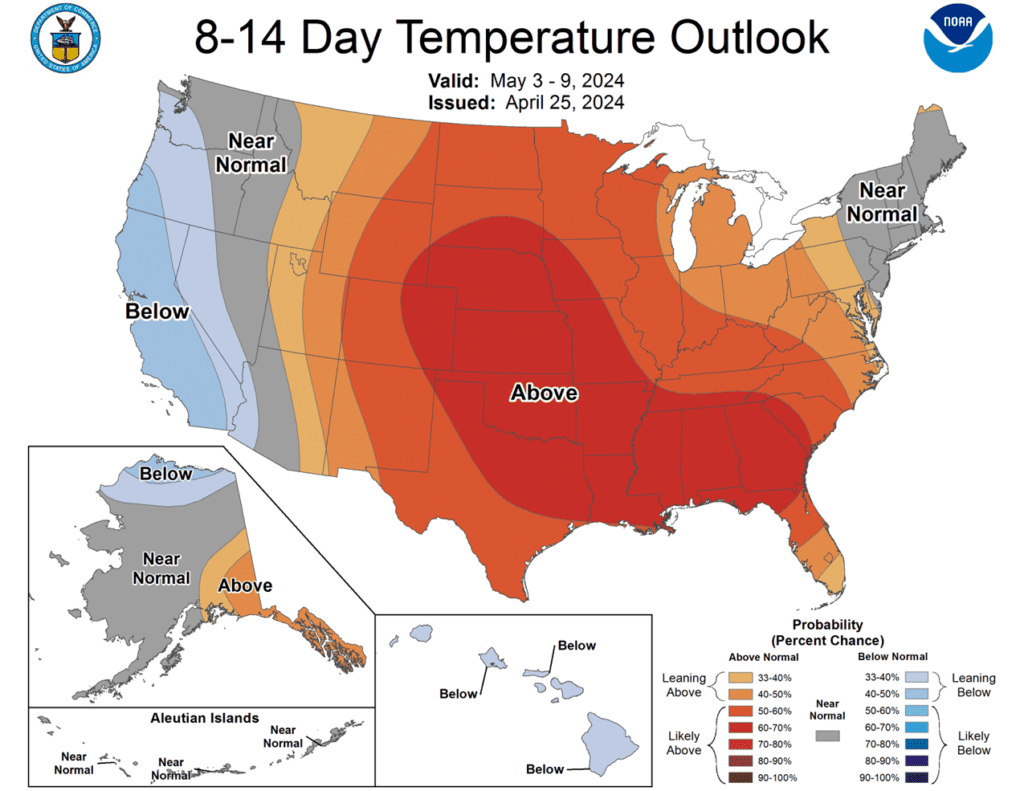

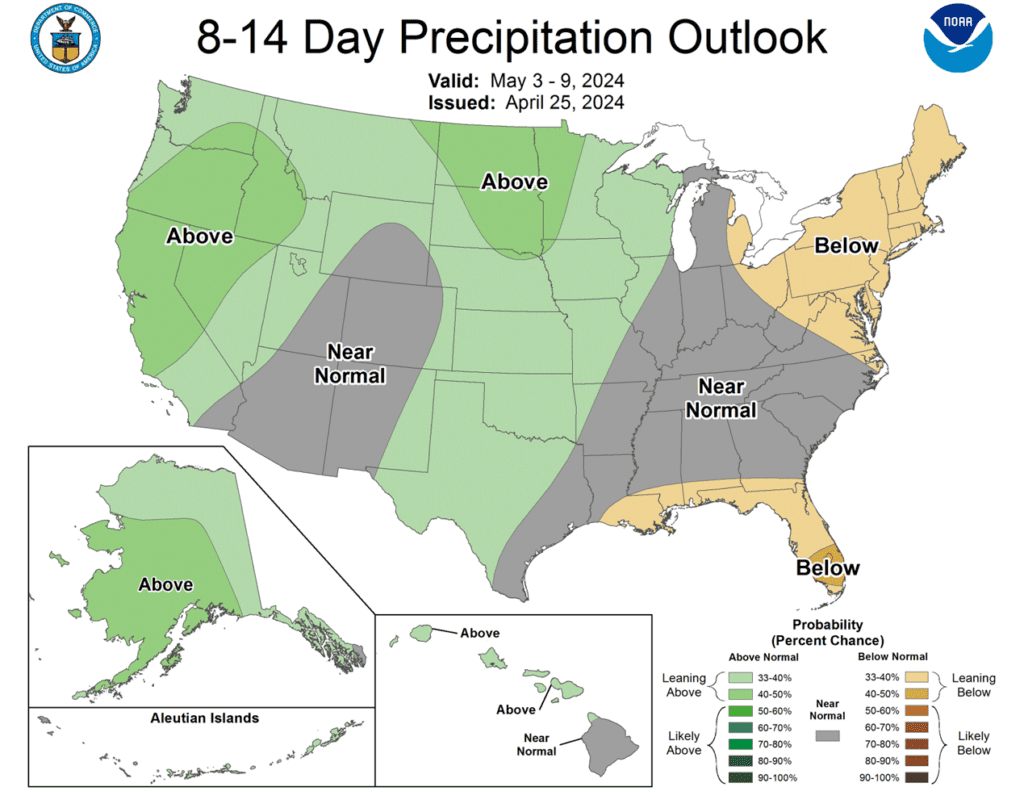

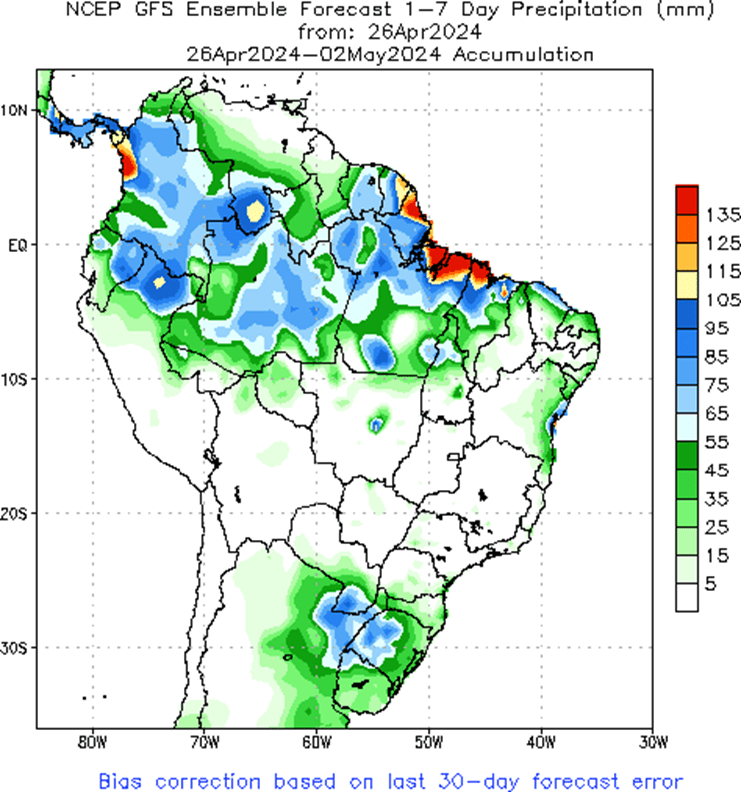

- To see the updated US 7-day precipitation forecast, US 8 – 14 day Temperature and Precipitation Outlooks, and 1-week precipitation forecast for Brazil and N. Argentina courtesy of NOAA and The Climate Prediction Center scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

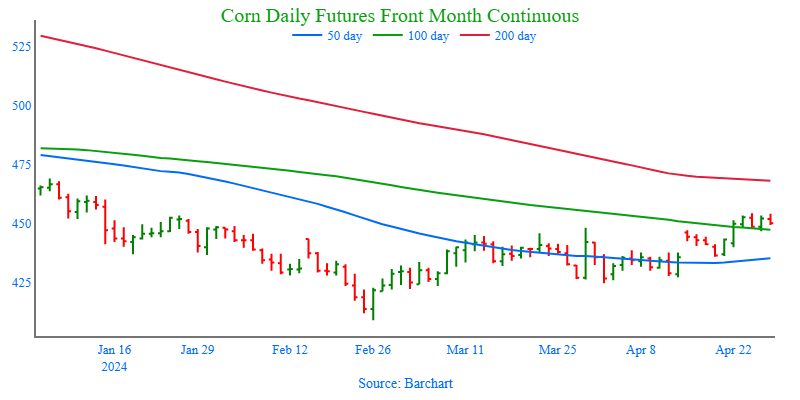

Although July ’24 corn has rallied beyond the congestion range on the front month continuous charts, it remains below its high of 460 that was posted on March 28. With little fresh bullish fundamental news, managed funds have maintained a significant net short position. While the fund’s large net short position likely sparked the recent rise in prices and could fuel a more significant upside move as we move through planting and into the growing season, the market now shows signs of being overbought. Despite potential obstacles along the way, overall market conditions and seasonal tendencies remain conducive to a continued price recovery into May and June.

- No new action is recommended for 2023 corn. The target range to make additional sales is 480 – 520 versus May ’24 futures. If you need to move bushels for cash or logistics reasons, consider re-owning any sold bushels with September call options.

- No new action is recommended for 2024 corn. We are targeting 520 – 560 to recommend making additional sales versus Dec ‘24 futures. For put option hedges, we are looking for 500 – 520 versus Dec ‘24 before recommending buying put options on production that cannot be forward priced prior to harvest.

- No Action is currently recommended for 2025 corn. At the beginning of the year, Dec ’25 corn futures left a gap between 502 ½ and 504 on the daily chart. Considering the tendency for markets to fill price gaps like these, we are targeting the 495 – 510 area to recommend making additional sales.

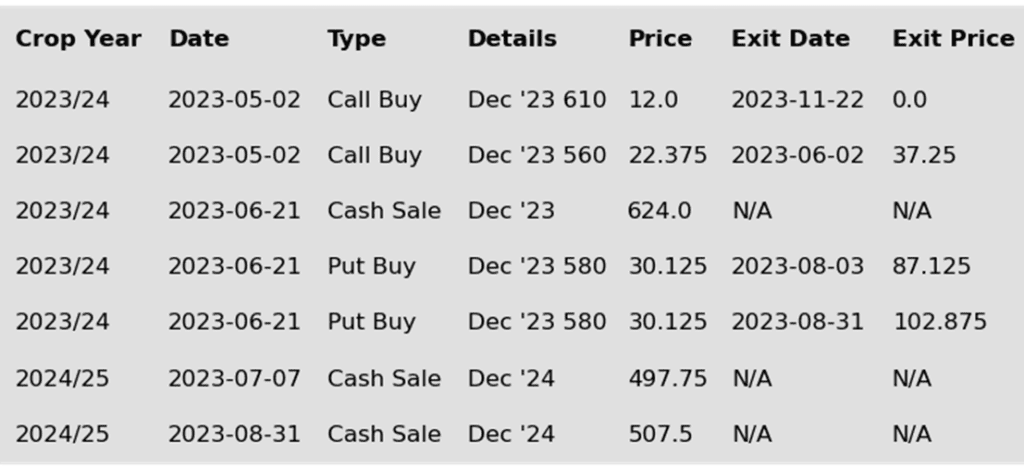

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Choppy, two-sided trade in the corn market to end the week. Overall strength in the wheat market helped support corn futures, but prices failed to push through resistance before turning softer into the close. For the week, July corn futures closed 7 cents higher.

- May options expired today, and that may have accounted for the end of session selling pressure. Price volatility may continue Monday with First Notice Day for May grain contracts on Tuesday, May 30.

- Weather models are shifting to a warmer and more active pattern going into early May. The western corn belt likely showed good planting activity and progress, but the eastern corn belt saw limited progress. Last week, corn planting reached 12% complete nationally.

- Recent rainfall has proven beneficial for areas experiencing moisture deficits, as evidenced by Thursday’s drought monitor maps, which indicated a contraction of the drought area. Moreover, forecasted rainfall for the upcoming week is expected to contribute to further moisture recovery. Presently, approximately 23% of corn acres are affected by some form of drought.

- Cash market have likely helped support corn futures this week. The average US corn basis levels have firmed in most cash markets. End users are trying to pull bushels in to meet demand, as producers are focused on planting this year’s crop.

Above: The corn market continues to struggle to rally with overhead resistance remaining around 460 in the July contract. A breakout above there could allow prices to test the 495 – 510 area. If prices break to the downside and close below 421, they could slide further to test 400 – 410 support.

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

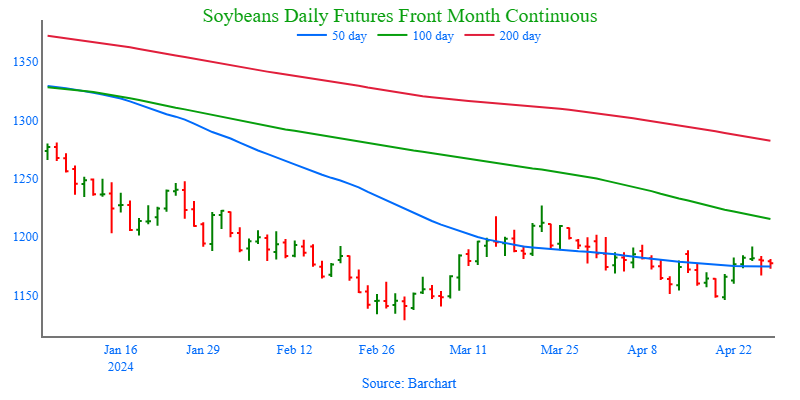

The USDA’s April Supply and Demand report failed to provide significant bullish data to prompt substantial short covering, as it mainly reflected recent demand challenges and an increase in ending stocks that aligned with the market’s expectations. However, managed money retains a considerable net short position near 168,000 contracts, as of the latest Commitment of Traders report. This could still fuel a short covering rally should complications arise during planting season, which has just begun. Otherwise, if weather conditions cooperate and planting progresses without major issues, prices could remain susceptible to revisiting recent lows throughout the spring.

- No new action is recommended for 2023 soybeans. We are currently targeting a rebound to the 1275 – 1325 area versus May ’24 futures to recommend making further sales. If you need to move inventory for cash or logistics reasons, consider re-owning any sold bushels with September call options.

- No new action is recommended for the 2024 crop. Considering the amount of uncertainty that lies ahead with the 2024 soybean crop, we recommended back in December buying Nov ’24 1280 and 1360 calls to give you confidence to make sales against anticipated production and to protect any sales in an extended rally. We are currently targeting the 1280 – 1320 range versus Nov ’24 futures, which is a modest retracement toward the 2022 highs, to recommend making additional sales.

- No Action is currently recommended for 2025 Soybeans. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

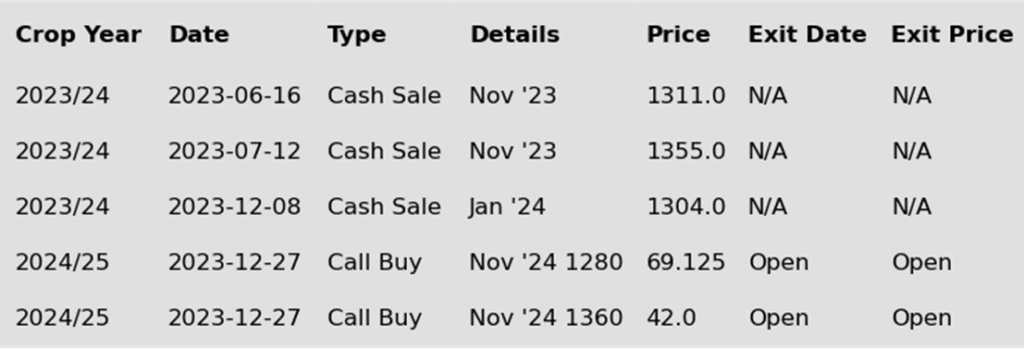

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans closed lower for the day with this being the third consecutive lower close in the July contract after three days in a row of gains. Prices have faltered and been unable to close above the July 20-day moving average for the past two days. Soybean meal ended the day lower while soybean oil was higher along with both palm and crude oil.

- For the week, July soybeans gained 11 ½ cents at 1177 ¼, November soybeans gained 13 ¾ at 1174 ¾, July soybean meal gained $1.50 at $344.70, and July soybean oil gained 0.60 cents at 45.54 cents. While soybeans bounced well off their recent lows, there was less bullish news regarding them than in corn and wheat.

- The Brazilian harvest is essentially complete, whereas Argentina’s crop is in good shape with harvest underway. Meanwhile, US soybean planting is moving along with wet conditions. This compares to corn which is struggling in South America and may see production revisions lower.

- In Argentina, the 23/24 corn harvest is now called at 19.8% complete which compares to 17.2% the previous week. Prices may have found some support with leaf hopper insects transmitting a disease among the Argentine crop that will cause yields to drop. Additionally, the corn crop is dealing with dryness and heat.

Above: Since posting a bullish reversal on April 19, the market has struggled to stay above 1190. A close above the April 24, 1191 ¾ high could allow the market to run and test the 1227 March high. Otherwise, support below the market remains between 1145 and 1140, if prices slide back toward key support and the February low of 1128 ½.

Wheat

Market Notes: Wheat

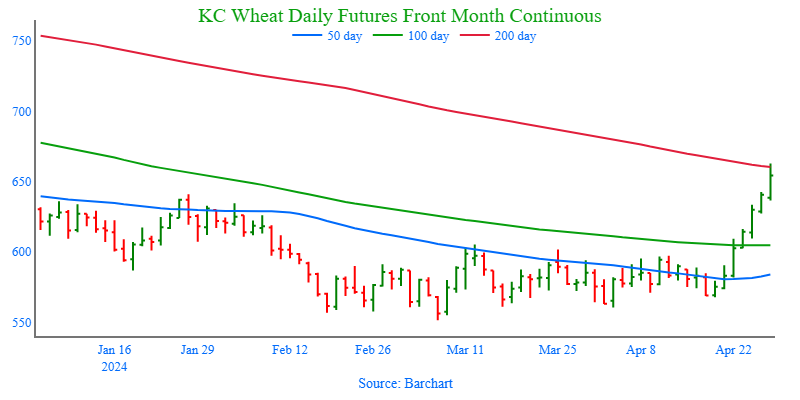

- Wheat managed to eke out another positive close in Chicago futures, although they finished well below the daily highs. Conversely, KC and Minneapolis contracts displayed more strength, with July Chicago rallying above the 200-day moving average for the first time since July 2023. However, the rally encountered strong resistance as it retreated below the 628 level by the close.

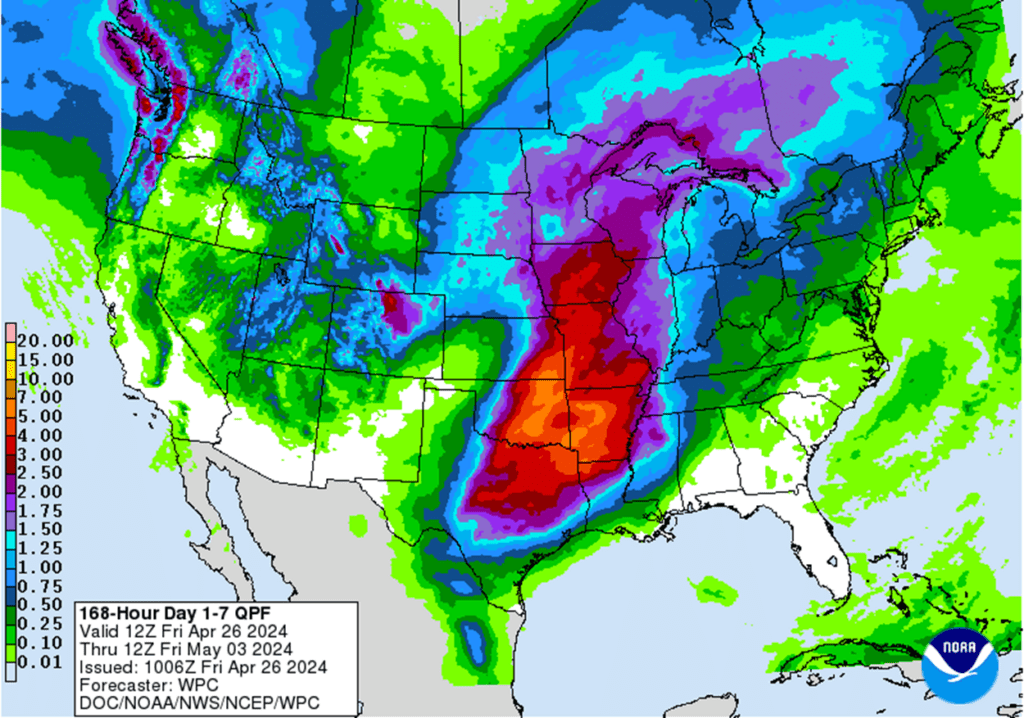

- Storms sweeping across the central Midwest are expected to bring drought relief to many areas, although regions such as southwest Kansas and the panhandles of Oklahoma and Texas were largely unaffected. This discrepancy may result in further declines to the HRW crop rating next week and could explain why KC wheat closed notably stronger than Chicago wheat today.

- The US Dollar Index continues to chop around with back-and-forth action. Despite being in a downtrend since mid-April, its strength today may have contributed to the decline in Chicago futures by the close. Moreover, technical indicators suggesting that Chicago wheat is overbought may have added to the weakness.

- The International Grains Council forecasts a US wheat crop of 1.94 billion bushels for 24/25, potentially the largest in eight years. This projection could limit long-term upside movement for futures from a fundamental perspective.

- The European Commission has revised down its estimate of Europe’s 24/25 soft wheat crop to 102.2 mmt, compared to 120.8 mmt in March. Additionally, exports are forecasted at 31 mmt, with stocks at 12.2 mmt. This decline may be attributed to excessive wet weather in certain areas, with the French wheat crop now rated at just 63% good to excellent, the lowest in four years.

Action Plan: Chicago Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Chicago Wheat Action Plan Summary

After holding downside support near 550, Chicago wheat staged a rally, likely fueled by Managed fund short covering and HRW crop concerns, that has taken it through the major moving averages on the continuous chart, and towards last Decembers highs. Although bearish fundamentals remain, and the market shows signs of being overbought which adds downside risk, Managed funds quite possibly still hold a large net short position that has the potential to drive an extended short covering rally should any crop more concerns arise as we enter the more dynamic part of the growing season.

- No new action is currently recommended for 2023 Chicago wheat. Any remaining 2023 soft red winter wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 Chicago wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Chicago wheat. Back in August we recommended buying July ’24 590 puts to prepare for further price erosion. Since then, we recommended exiting half of the original position to get closer to a net neutral cost, and then most recently, we recommended exiting another half of the remaining position to lock in further gains in case prices continue higher, leaving 25% of the original position in place. We continue to target a market rebound back towards 675 – 715 versus July ’24 futures before recommending any additional sales. As for the open July ’24 590 put position, we are looking for prices between 475 – 500 versus July ’24 futures to before we recommend exiting any of the last 25%.

- No new action is currently recommended for 2025 Chicago Wheat. We recently recommended initiating your first sales for the 2025 SRW crop year as prices pressed back toward the mid-600 range to take advantage of historically good prices for next year’s crop. Since plenty of time remains to market this crop, we are looking for further price appreciation and are currently targeting the 690 – 725 area to recommend making additional sales.

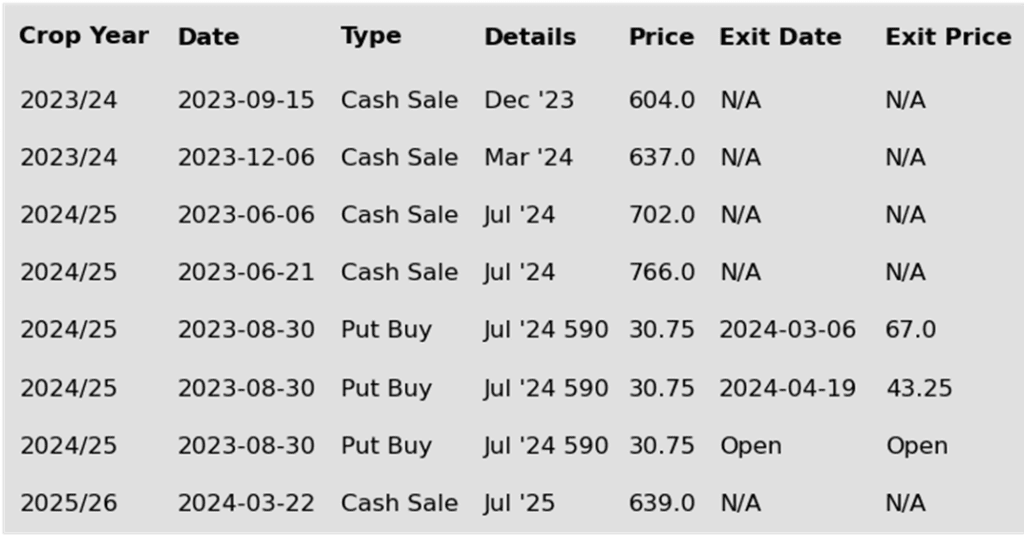

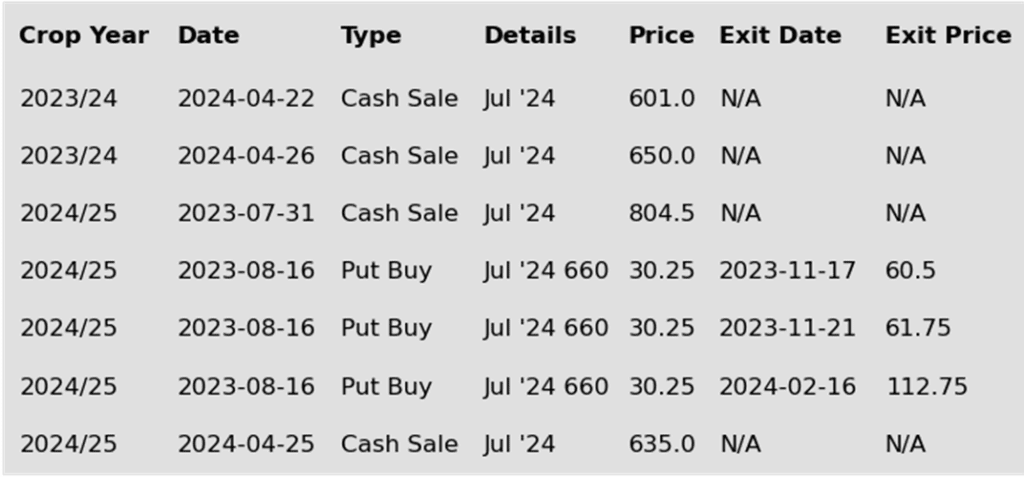

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: July Chicago’s close above the 200-day MA opens the door to test the December high of 630. On the downside, if prices retreat, initial support is likely around 575 and the 50-day moving average (currently 561).

Action Plan: KC Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

New Alert

Sell JUL ’24 Cash

2024

Active

Sell JUL ’24 Cash

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

KC Wheat Action Plan Summary

Between the end of February and the middle of April, KC wheat was mostly rangebound between the mid 590’s on the topside and mid 550’s down low, with little to move prices higher. All the while Managed funds continued adding to their large net short positions. Toward the end of April, dryness in the Black Sea region and the US HRW growing areas started becoming more concerning and triggered a short covering rally across the wheat complex, driving prices to levels not seen since last December. While low world export prices continue to be a drag on US demand and prices, and it is likely that Managed funds covered a significant portion of their net short positions, it is also quite possible that they remain short the market. Which could still push prices higher if production concerns persist.

- Grain Market Insider recommends selling a portion of your 2023 HRW wheat production. Dryness in the Southwestern Plains and Russia, along with elevated geopolitical tensions in the Middle East and Black Sea spurred Managed funds to cover some of their extensive short positions in the wheat complex. As a result, the July ’24 KC wheat futures contract is about 50 cents higher than our previous old crop sales recommendation, and near both the 200-day moving average and the resistance area of last December’s highs. Considering this rally may primarily be weather driven and could be short-lived, as well as being limited on time before the 2024 crop is harvested, we advise you to take advantage of these elevated prices to sell another portion of your 2023 HRW wheat inventory.

- Grain Market Insider sees a continued opportunity to sell a portion of your 2024 HRW wheat production. Since the end of July, the wheat market has been in a downtrend with no significant selling opportunities, while many uncertainties remain that could drive prices even higher. The market is now approximately 90 cents off the March low and entering an area of heavy resistance that coincides with a 25% retracement of the recent downtrend back toward the July high. Grain Market Insider recommends taking advantage of this rally to make an additional sale on your 2024 crop.

- No action is currently recommended for 2025 KC Wheat. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

Above: The market’s ability to close above the 610 – 640 congestion area puts it on track to further test overhead resistance in the 678 – 700 area. Should the market fall back, initial support may be found near 640 and again between 605 and 551 ½.

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

Active

Sell JUL ’24 Cash

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

Between mid-February and much of April Minneapolis wheat traded mostly sideways to lower with little bullish fundamental news to drive prices higher. In late April, driven by world wheat crop concerns and dryness in the HRW growing areas, and fueled by likely Managed fund short covering, Minneapolis wheat rallied back toward the January highs. Although bullish fundamentals remain scarce, and the market shows signs of being overbought, historical seasonal trends typically strengthen as we approach late spring and early summer. Furthermore, Managed funds quite possibly still hold a net short position, that could fuel an extended rally if more production concerns arise.

- Grain Market Insider sees a continued opportunity to sell a portion of your 2023 Spring wheat crop. Since the end of July, the wheat market has been in a downtrend due to lower world prices, with no significant rallies to take advantage of. While many unknowns remain that could move prices even higher, the market is now more than 50 cents off its low and entering an area of heavy resistance that coincides with a 23% retracement back to the July high. Grain Market Insider advises taking advantage of this rally, and these still historically good prices, to make an additional sale on your 2023 crop.

- No new action is recommended for 2024 Minneapolis wheat. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts (due to their higher liquidity and correlation to Minneapolis), to protect the downside, and recommended exiting the original position in three separate tranches as the market got further extended into oversold territory to protect any gains that were made. The current strategy is targeting the 775 – 815 area versus Sept ’24 to recommend making additional sales. We are also targeting the 850 – 900 area to recommend buying upside calls to help protect any sales that would have been made.

- No action is currently recommended for the 2025 Minneapolis wheat crop. We are currently not considering any recommendations at this time for the 2025 crop that will be planted in the spring of next year. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: The market’s test of the 700 – 712 area has put it into overbought territory and is at risk of falling back. If that happens, initial support may come between 675 and 660, with further support down toward 632 and 625 ¼.

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Brazil and N. Argentina 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.