4-24 End of Day: Grains Finish Strong Despite Early Session Weakness

All Prices as of 2:00 pm Central Time

| Corn | ||

| MAY ’25 | 477.25 | 5.25 |

| JUL ’25 | 484 | 4.75 |

| DEC ’25 | 456.5 | 2 |

| Soybeans | ||

| MAY ’25 | 1053 | 12.75 |

| JUL ’25 | 1062 | 11.75 |

| NOV ’25 | 1035.5 | 8 |

| Chicago Wheat | ||

| MAY ’25 | 529.25 | 1 |

| JUL ’25 | 544.5 | 1 |

| JUL ’26 | 617 | 1.75 |

| K.C. Wheat | ||

| MAY ’25 | 537.75 | 0 |

| JUL ’25 | 550.75 | 0.5 |

| JUL ’26 | 622 | 0.75 |

| Mpls Wheat | ||

| MAY ’25 | 592.5 | 1 |

| JUL ’25 | 607.75 | 0.75 |

| SEP ’25 | 623 | 0.75 |

| S&P 500 | ||

| JUN ’25 | 5507.75 | 106 |

| Crude Oil | ||

| JUN ’25 | 62.79 | 0.52 |

| Gold | ||

| JUN ’25 | 3348.5 | 54.4 |

Grain Market Highlights

- Corn: After a choppy start to the week, corn futures managed to end with modest gains, supported by strong export performance.

- Soybeans: Supported by ongoing optimism over a trade deal with China, soybeans gained throughout the day and ultimately settled higher.

- Wheat: Despite a weaker start, wheat futures managed to close higher, as the market continued to show signs of being oversold.

- To see the updated U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Wheat section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

Active

Sell JUL ’25 Cash

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

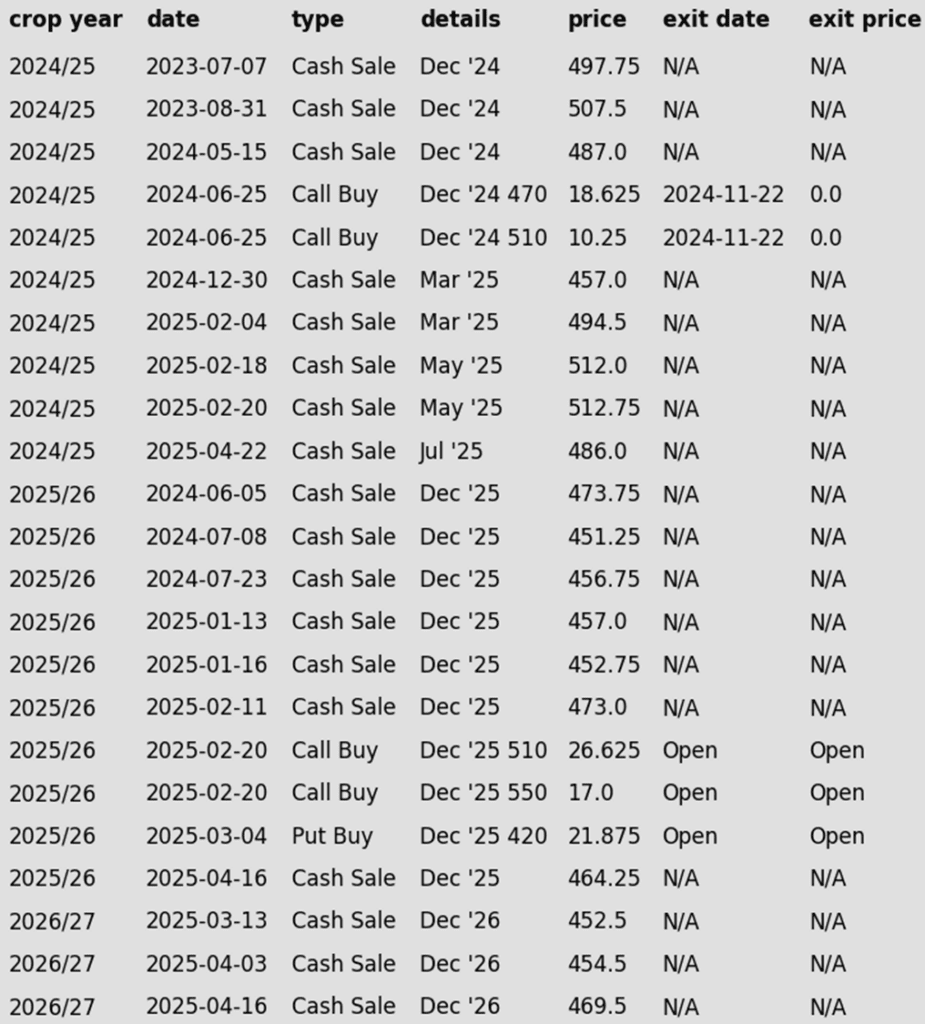

2024 Crop:

- CONTINUED OPPORTUNITY – Sell another portion of your 2024 corn crop. This should be the eighth sale for your 2024 corn crop.

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Now, eight sales recommendations made to date, with an average price of 494.

- Current Rec: The July contract has recently stalled, encountering strong selling pressure in the 494–496 range. Monday’s Crop Progress report showed U.S. corn planting moving ahead of the five-year average — a trend that, if it continues, could reduce the market’s urgency to bid aggressively for old crop supplies. Additionally, a key Plan B technical indicator that Grain Market Insider closely tracks turned lower on Tuesday, issuing a sell signal. Given the rally from the March low and the seasonal timing, this remains a timely opportunity to make an eighth sale of the 2024 corn crop.

2025 Crop:

- Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

- Plan B: No active targets.

- Details:

- Sales Recs: Seven sales recommendations have been made to date, with an average price of 461.25.

- Nothing New: Exit targets for December options remain unchanged, and no new sales targets posted today.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations have been made to date, with an average price of 460.

- Nothing New: Following the recent recommendation to make a third sale, no new sales targets posted today.

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn futures broke a three-session losing strength to finish with moderate gains on Thursday. Strong export performance, buying in the soybean market and the volatility of options expiration helped triggered buying in the corn market on the session.

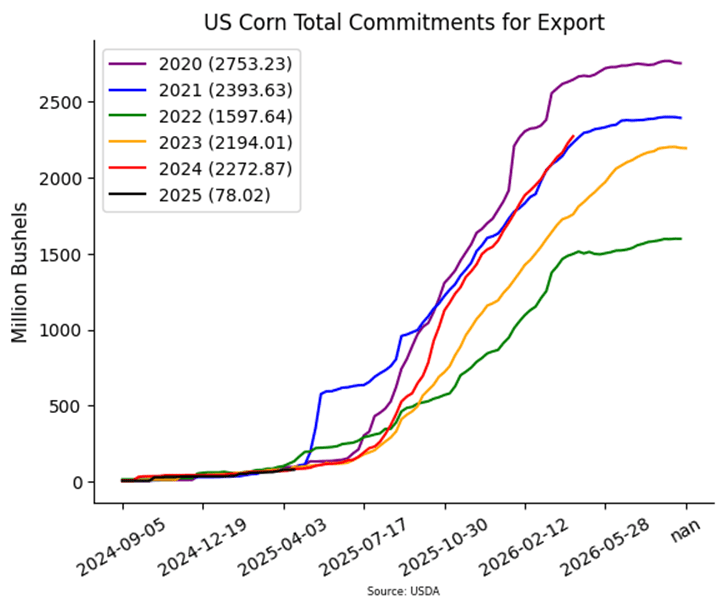

- USDA released weekly export sales on Thursday morning. For the week ending April 17, USDA reported new crop sales of 1.152 MMT (45.4 mb). Japan was the largest buyer of US corn on the week. Corn export sales are up 26% over last year and still ahead of the USDA pace to reach the marketing year export target.

- New crop export sales for the 2025-26 marketing year are starting slowly at 458,377 MT (18.04 mb). These total trails last year’s sale pace by approximately 400,000MT for the same time period. The market will be watching 2025-26 sales as the US is expected to plant a record number of acres, strong South American crops, and the impacts of tariffs on corn exports in the future.

- May corn options expire on Friday, and prices tend to be more volatile in the expiration window. This is followed by First Notice Day on April 30. These events can trigger volatility in the front end of the corn market.

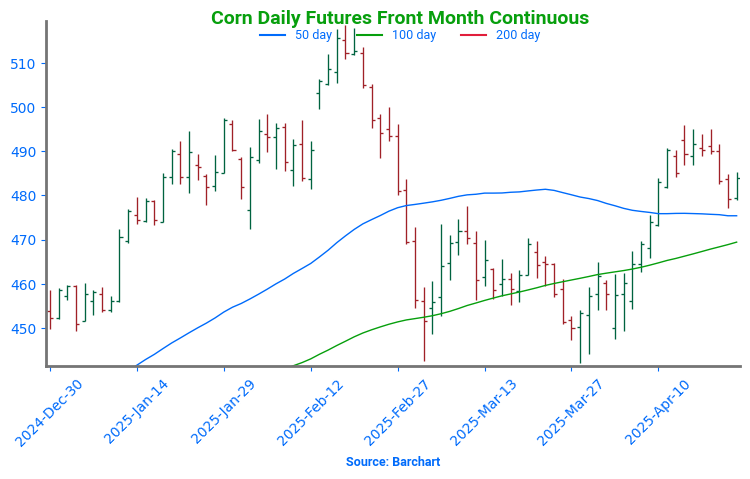

Corn on the Move: Bulls Eye 510+ After Breakout

Corn futures broke out in April after holding key support near 450 through much of March. A bullish April WASDE report highlighting stronger demand sparked the rally, with prices pushing through the 50-day moving average. All eyes now turn to planting progress and demand trends to drive the next move. The February highs just above 510 are the next upside target, while support is firming near 470 at the top of the previous range.

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: Next cash sale at 1107 vs July.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made to date, with an average price of 1089.

- Nothing New: With three sales recommendations made to date, continue targeting a move to 1107 to make a fourth sale.

2025 Crop:

- Plan A: Next cash sales at 1093 & 1114 vs November. Exit all 1100 November call options at 88 cents.

- Plan B: Make a cash sale if November closes below 1016.75 support.

- Details:

- Sales Recs: One sales recommendation made so far to date, at 1063.50.

- Catch-Up Target: If you didn’t make the one sale, aim for 1063 vs November as your catch-up target. This price level aligns with the Grain Market Insider sale recommendation issued back on January 29.

- Nothing New: Plan A and Plan B targets remain unchanged – ready to pull the trigger on additional sales if November can rally to 1093 & 1114, while simultaneously prepared to advance another sale if 1016.75 support is broken.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- Nothing New: The expectation is still for targets to begin posting in a month or two.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day higher, gaining throughout the day and finally managing to close above the 200-day moving average for the first time since February. Support came from continued hopes for a trade negotiation with China along with a breakout higher in soybean oil. Soybean meal finished the day lower.

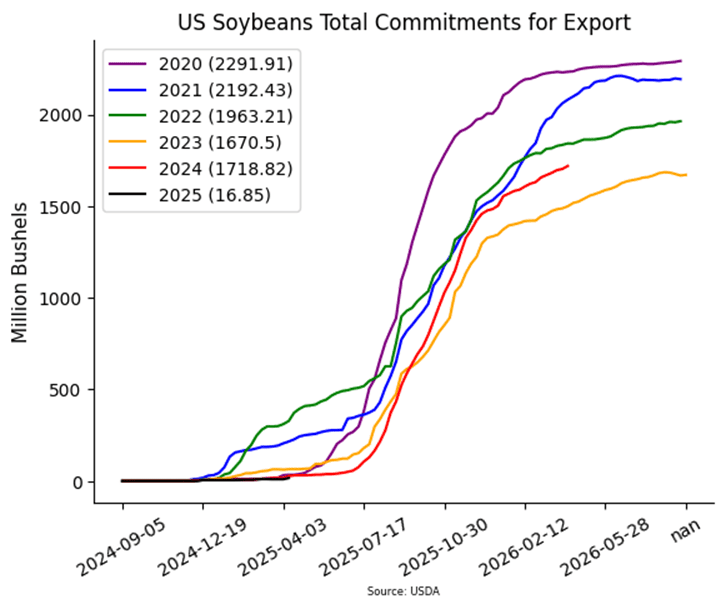

- Today’s export inspections report was on the poor side for soybeans. The USDA reported an increase of 10.2 million bushels of export sales for 24/25 and a decrease of 3,700 bushels for 25/26. This was on the low end of analyst estimates. Primary destinations were to Mexico, the Netherlands, and unknown destinations.

- Last week’s export shipments of 18.2 million bushels were above the 11.8 mb needed each week to meet the USDA’s export estimate of 1.825 bb in 24/25. Soybean sales commitments are now up 13% from a year ago. China was not an active buyer this week.

- U.S. soybean planting is off to a strong start, with 8% of the crop planted — ahead of the five-year average. Near-term rains are expected, but longer-range forecasts show a drier May across North America, raising concerns about summer drought potential and adding weather premium to prices.

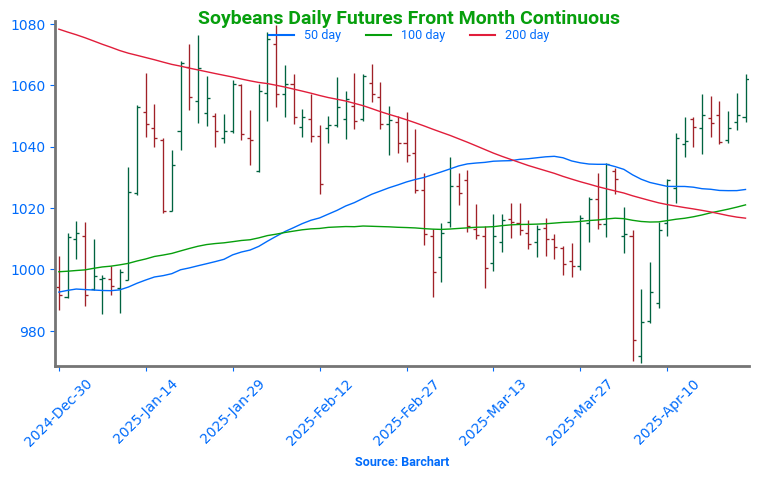

Soybean Futures Rebound: Momentum Builds Above Key Support

Soybean futures dropped sharply in early April after newly announced tariffs triggered a break below key support near 1000, a level that had held firm through March. However, strong buying interest fueled a swift rebound, pushing futures back above the pivotal 1000 mark and reclaiming major moving averages — especially the 200-day, which had capped rallies for the past two years. With momentum rebuilding, the market is now eyeing the February highs near 1080, while the 200-day moving average is expected to provide support on any spring pullbacks.

Wheat

Market Notes: Wheat

- Despite a weaker start to the day, wheat managed to eke out a positive close across all three classes. Managed funds are estimated to hold a net short position of around 145,000 contracts heading into the session, and Kansas City futures remain technically oversold. Both factors could set the stage for a short-covering rally—if a catalyst emerges to spark it.

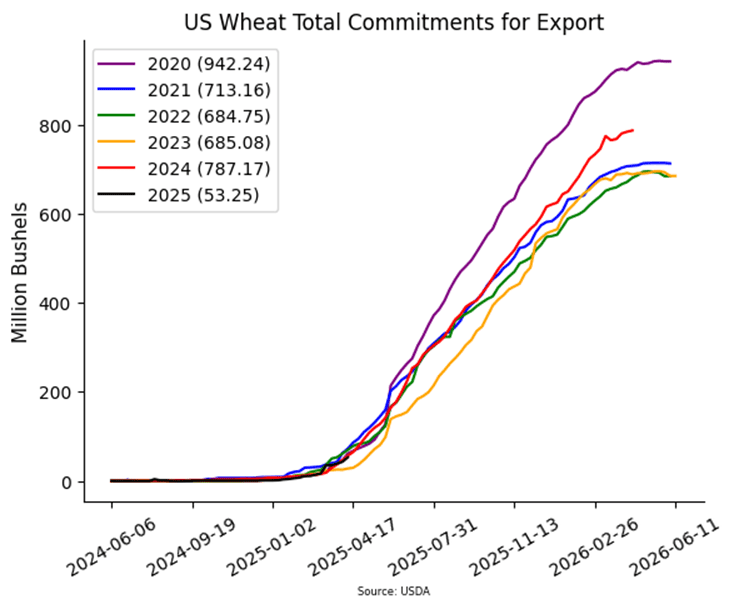

- The USDA reported a decrease of 5.3 mb of wheat export sales for 24/25, and an increase of 13.7 mb for 25/26. Shipments last week at 17.6 mb fell under the 21.9 mb pace needed per week to reach the USDA’s export goal of 820 mb. Total 24/25 sales commitments have reached 782 mb, up 13% from last year.

- According to the USDA, as of April 22, an estimated 33% of US winter wheat acres are experiencing drought conditions. This is down 1% from last week, as recent rains have fallen across much of the central and southern US. During the same timeframe, however, spring wheat acres in drought increased by 6% to 49%.

- According to their supply minister, Egypt is expected to import 4.5 mmt of wheat during the 25/26 season (which begins in July). This would be below the 4.8 mmt estimated so far this year. Additionally, they stated that current wheat stockpiles are expected to be sufficient through late July.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: Target 701 against July for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Four sales recommendations made to date, with an average price of 690.

- Nothing New: 701 is still the price target to trigger a fifth sales recommendation.

2025 Crop:

- Plan A: Target 705.50 against July for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made to date, with an average price of 646.

- Nothing New: Still targeting 705.50 to trigger the sixth sales recommendation.

2026 Crop:

- Plan A: Target 704 against July ‘26 for the next sale

- Plan B: No active targets.

- Details:

- Sales Recs: One sales recommendation made to date, at 624.

- Nothing New: 704 is still the price target to trigger a second sales recommendation.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Futures Eye Key Breakout Above 200-Day Moving Average

After months of sideways action, Chicago wheat futures broke higher in February, rallying to early October highs just above 615. However, that mid-month peak quickly turned into a reversal point, sending futures back into the late 2024 trading range. Support near 530 held firm through March, and prices are building upward again this April. The next key test is the 200-day moving average — a decisive weekly close above it could signal a shift in momentum and potentially kickstart a broader upside trend.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Three sales recommendations made to date, with an average price of 677.

- Nothing New: Still no active price targets, as the July contract continues to chop around in the 560–580 range.

2025 Crop:

- Plan A: Target 677 against July for the next sale.

- Plan B: No active targets.

- Details:

- Sales Recs: Four sales recommendations made to date, with an average price of 639.

- Nothing New: 677 is still the price target to trigger a fifth sales recommendation.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Zero sales recommendations made so far to date.

- Nothing New: The expectation is still for targets to begin posting in the May – June timeframe.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Holding Support, Watching 200-Day Resistance

February was a volatile month for Kansas City wheat, with prices surging higher before tumbling back and ending the month little changed. March brought additional weakness, dragging prices near recent lows, but the ability to hold trendline support so far in April is encouraging. On a rebound, the 200-day moving average will be the first resistance level to watch, with February highs near 640 serving as a more significant upside barrier. On the downside, support near the December lows around 540 should provide a strong floor if selling pressure continues.

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made to date, with an average price of 696.

- Nothing New: No active targets for a sixth sales recommendation at this time.

2025 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Sales Recs: Five sales recommendations made to date, with an average price of 646.

- Nothing New: No active targets for a sixth sales recommendation at this time.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Nothing New: The expectation is still for targets to begin posting in the June – July timeframe.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

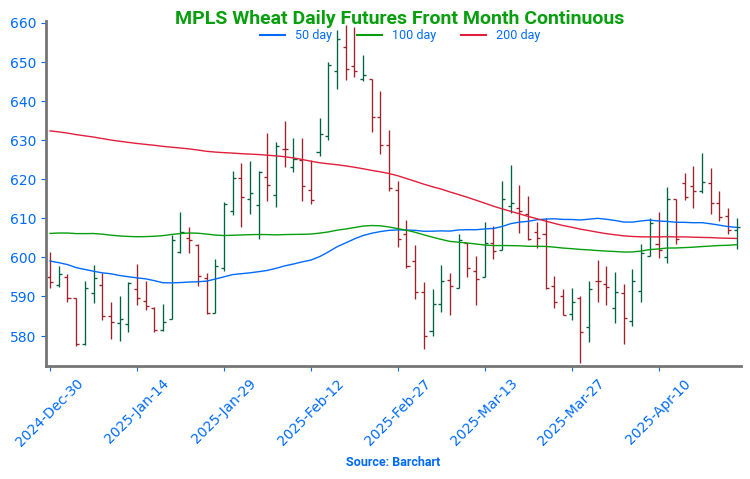

Spring Wheat Holds Above 200-Day

Spring wheat broke out of its long-standing sideways range in late January, triggering a surge of bullish momentum. The rally gained traction in mid-February with a close above the 200-day moving average, though late-month weakness briefly pushed futures back below key technical levels. Unlike winter wheats, spring wheat’s ability to stay above the 200-day remains encouraging, with this level now expected to act as support on any growing season pullbacks. The next upside target is the February highs near 660. With spring wheat acreage projected to be the lowest in 55 years, weather volatility is likely to play a major role in driving price action this season.

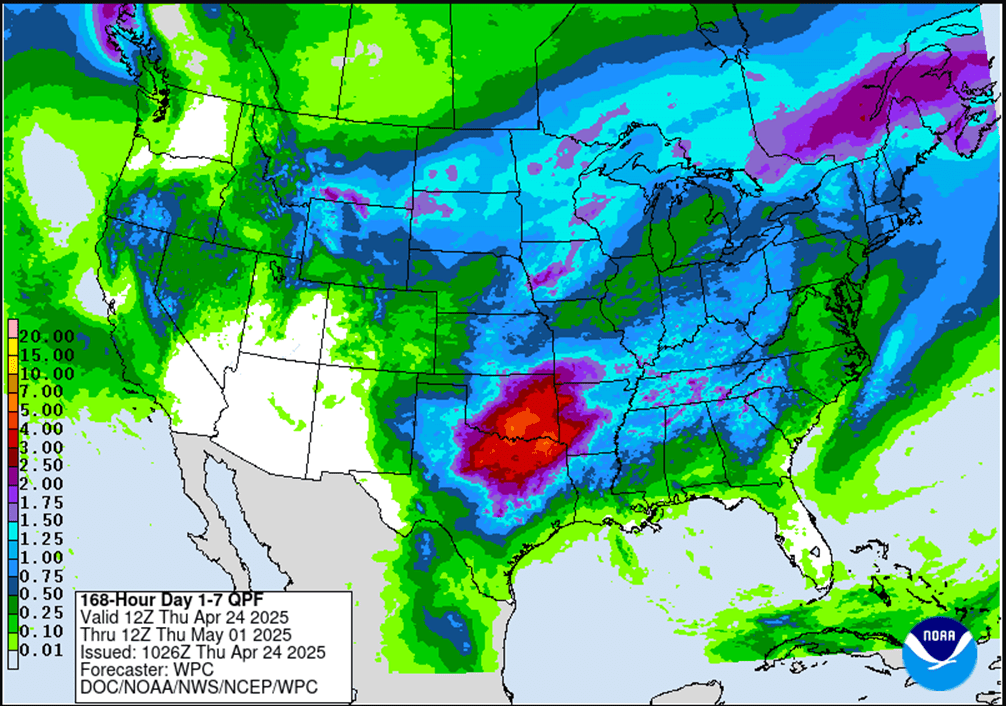

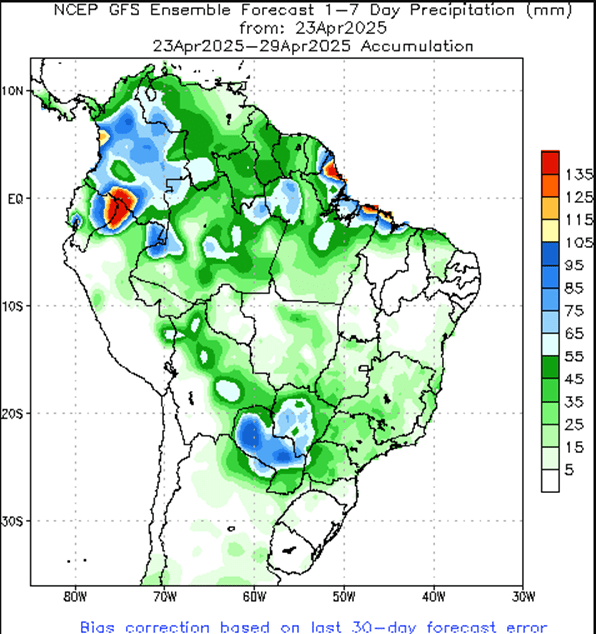

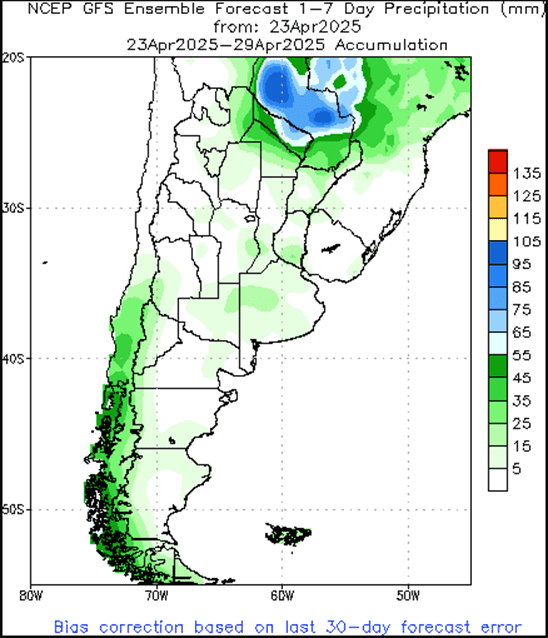

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above: Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.