3-5 End of Day: Markets Reverse Some of Monday’s Gains

All prices as of 2:00 pm Central Time

| Corn | ||

| MAY ’24 | 426.25 | -3.75 |

| JUL ’24 | 437.5 | -3.75 |

| DEC ’24 | 459.25 | -3.75 |

| Soybeans | ||

| MAY ’24 | 1149 | -6 |

| JUL ’24 | 1159 | -6.25 |

| NOV ’24 | 1144.25 | -2 |

| Chicago Wheat | ||

| MAY ’24 | 551 | -13 |

| JUL ’24 | 555.75 | -11.5 |

| JUL ’25 | 609.25 | -8.25 |

| K.C. Wheat | ||

| MAY ’24 | 569.25 | -11 |

| JUL ’24 | 557.75 | -9.25 |

| JUL ’25 | 602.5 | -7.25 |

| Mpls Wheat | ||

| MAY ’24 | 655.5 | -4 |

| JUL ’24 | 657.5 | -5.25 |

| SEP ’24 | 663.5 | -5 |

| S&P 500 | ||

| JUN ’24 | 5140.5 | -60.25 |

| Crude Oil | ||

| MAY ’24 | 77.41 | -0.76 |

| Gold | ||

| JUN ’24 | 2161.3 | 14.5 |

Grain Market Highlights

- A quick planting pace for Brazil’s safrinha corn crop, and weakness in the wheat complex with May Chicago wheat hitting a new contract low added negativity to the corn market which continued to consolidate for the 6th day in a row.

- After a lower opening to the day session, soybeans rallied briefly to a 3 ¾ cent gain on strength from soybean oil, but that strength quickly faded amid weaker soybean meal and fading soybean oil. With Brazil’s ongoing harvest, their export prices are running about 100 cents cheaper than the US offers, hindering US exports and prices.

- Technical selling resumed in the soybean meal after it failed to hold midday gains, and choppy two-sided trade dominated soybean oil in today’s trade as it continues to consolidate. Meal importing countries remain largely hand to mouth in anticipation of cheaper Argentine supplies, while palm and bean oil demand in India slowed considerably last month in favor of less expensive alternatives like sunflower oil.

- Declining export offers out of the Black Sea region and Russia continue to weigh on the wheat complex, which saw closing prices in the red for all three classes. Open interest in the complex has also risen over the past few days, suggesting that managed funds may be adding to their net short positions.

- To see the updated US 5-day precipitation forecast, and the 1-week precipitation forecast and 7-day total accumulated precipitation for Brazil, courtesy of the NWS, CPC, and NOAA, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

- No new action is recommended for 2023 corn. With a general lack of bullish news and an estimated US carryout nearing 2.2 billion bushels, front month corn has languished in a sideways to lower trend since printing a high last October. While the lack of a bullish catalyst has been disappointing, the market is in a significantly oversold condition, and managed funds continue to hold a substantial net short position. Either or both could trigger a short covering rally at any time heading into the spring planting window. As planting nears, and uncertainties increase, Grain Market Insider will consider recommending additional sales if prices recover back toward the 500 level.

- No new action is recommended for 2024 corn. In January, Dec ’24 broke through the bottom end of the 485 ¾ to 602 range that had been in place since February ’22. While this was a disappointing development, bear spreading has allowed Dec ’24 to maintain more of its value versus old crop as traders attempt to price in a larger 2023 carryout with more uncertainty ahead for the 2024 crop. Additionally, Dec ’24 is significantly oversold on the weekly chart, which is supportive for a technical rally to begin at any time as the spring planting window quickly approaches. Given the amount of time and uncertainty that remains for the 2024 crop, Grain Market Insider will consider recommending additional sales on a retracement toward the low to mid 500 level.

- No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next year. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

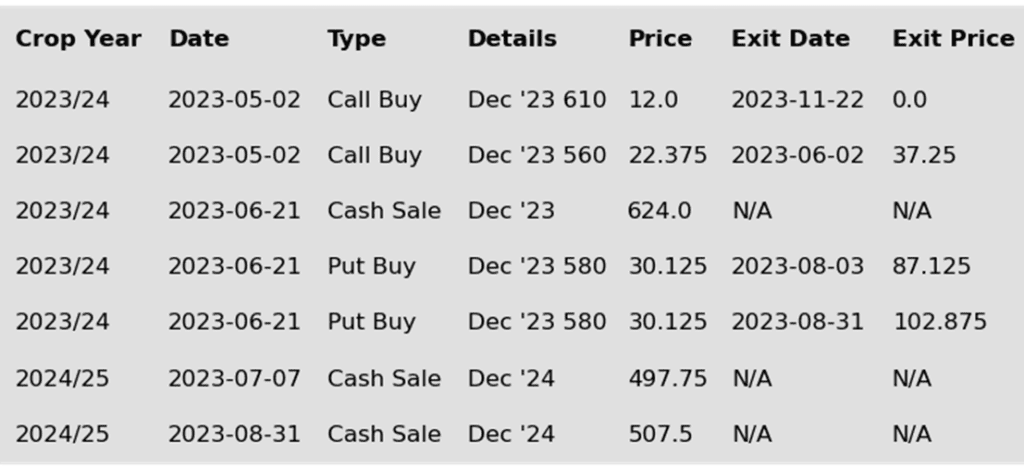

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn futures finished lower on the session, pressured by selling pressure in the wheat market as Chicago wheat prices broke to new lows in the May contract. May corn futures lost 3 ¾ cents during the session.

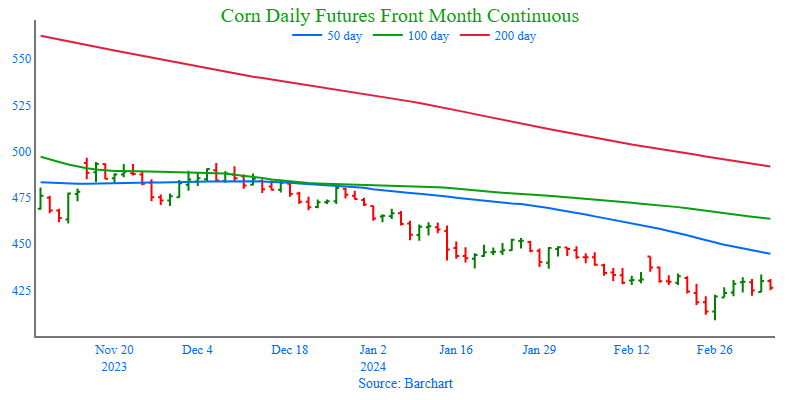

- The corn market consolidated for the sixth consecutive day with a trading range from 420 – 430 on the May futures. Today’s session saw a narrow trading range of six cents from high to low, and prices traded within yesterday’s trading range as the corn market is looking for some near-term direction.

- Brazil’s second crop corn planting is running well ahead of schedule, promoted by a rapid soybean harvest. Brazil consulting group AgRural estimates that 86% of the corn planting is complete versus 70% last year.

- Demand remains the focus of the US corn market. Demand news has been improved in recent weeks for US corn as export sales and inspections have trended well above last year’s disappointing total. Export sales are looking to approach the 5-year average, as the corn export window for US corn is open and prices are competitive. Both sales and shipments will need to stay consistently strong in the weeks ahead to reach USDA export targets.

- Price moves in the corn market are likely to stay choppy the remainder of the week until Friday’s USDA WASDE report. The market could see additional short covering. The report is expecting to see slight changes on US carryout projections, but the market may focus more on the USDA’s path with the Argentina and Brazil production estimates.

Above: The corn market continues to consolidate following the bullish key reversal on February 26. Overhead resistance remains between 435 and 445. If the prices close below 421, the bottom of the recent range, then they may slide to test downside support between 400 and 410 unless a positive input enters the scene to turn prices back higher.

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

- No new action is recommended for 2023 soybeans. Old crop soybeans continue to be in a downtrend that began with the early January breakout of the 1290 – 1400 range that had been in place since last fall. While South American weather has improved, questions remain regarding the crop size, and US planting season is now not that far off with its own potential concerns that could turn prices back higher. Given the potential of a downside breakout back in December, Grain Market Insider recommended adding to sales as prices remained historically good, and Grain Market Insider will continue to look at additional sales opportunities heading into spring.

- No new action is recommended for the 2024 crop. Since the beginning of the year, Nov ’24 has continued to recede alongside the 2023 old crop contracts as South American weather stabilized and the market deals with bourgeoning domestic supplies and slow demand. While this decline in prices is disappointing, planting season is not far off, and plenty of time remains to market this crop, with many unknowns that can rally prices yet ahead. Considering the amount of uncertainty that lies ahead with the 2024 soybean crop, Grain Market Insider recommended back in December buying Nov ’24 1280 and 1360 calls to give you confidence to make sales against anticipated production, and to protect any sales in an extended rally. Based on our research, the possibility remains that prices could retest the 2022 highs in the upper 1300s going into spring/summer, at which point Grain Market Insider would consider recommending additional sales.

- No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

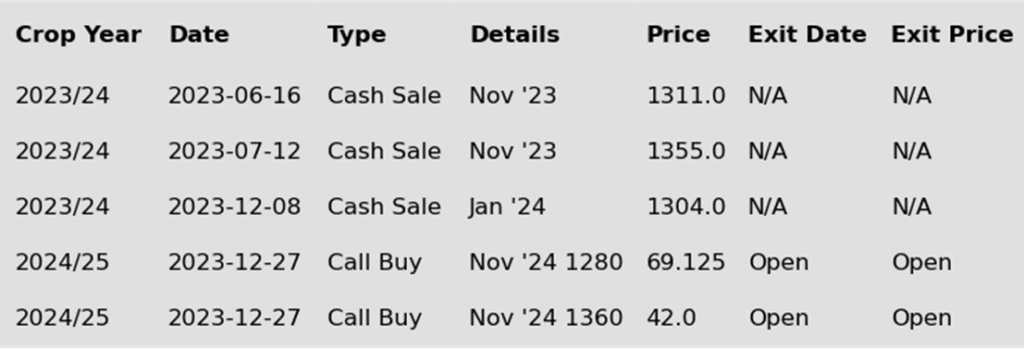

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day lower and though they managed to remain off the contract lows, they have also been met with selling pressure following any rallies. Export demand has been sluggish, and the US has a greater disadvantage with the ongoing Brazilian harvest. Both soybean meal and oil ended the day lower as well.

- Friday’s WASDE report isn’t expected to include any major surprises, but analysts expect that the US soybean carryout will be slightly increased due to a decrease in exports. The world carryout is expected to fall, and estimated Argentine soybean production is expected to increase slightly to 50.3 mmt, while Brazil’s is expected to decrease to 152.8 mmt, from last month’s 156 mmt forecast.

- The Brazilian soybean harvest is now 48% complete, which compares to 40% a week earlier and 43% the previous year. Cash prices in the country have recently begun to rise, which has brought about more farmer selling, although export prices remain about 100 cents/bu. below US offers.

- In China, soybeans on the Dalian Exchange rose by 0.6% and are trading at the equivalent of $13.68. China has bought US soybeans but will likely lean more heavily on Brazil’s cheaper beans as harvest progresses. There continue to be concerns that China and other countries will cancel previous US purchases in favor of Brazil.

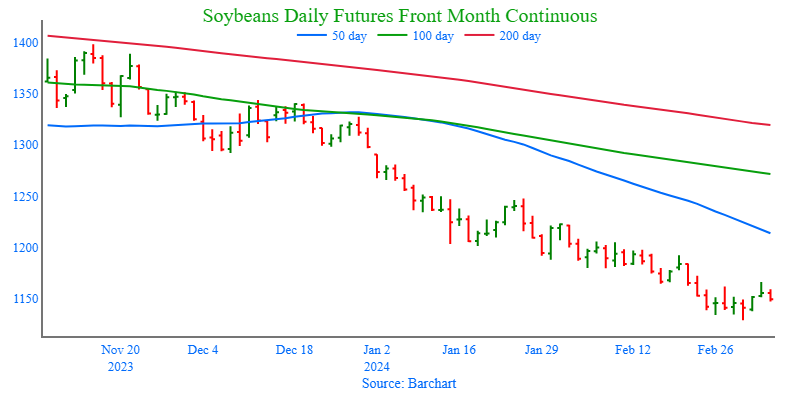

Above: After posting a low of 1128 ½ on February 29, soybeans rallied back higher on short covering. The market remains oversold on the weekly chart and continues to provide underlying support. For now, resistance above the market remains between 1190 and 1205, with initial support still just below 1130. If prices were to decline further, major support below the market may enter in around 1040 – 1050.

Wheat

Market Notes: Wheat

- In a reversal from yesterday’s trend, all three US wheats posted losses, led by Chicago futures. This comes despite winter wheat crop good to excellent conditions declining in Texas by 3%, Kansas by 4%, and Oklahoma by 5%. Offering pressure to the wheat trade today are reports that Black Sea wheat FOB values dropped below $200 per mt, with Russia just above that level; this keeps the US uncompetitive in terms of exports.

- On Friday’s USDA report, not much change is expected for wheat in terms of the US numbers. The average pre-report estimate of US wheat carryout is pegged at 658 mb, which would be unchanged from last month. The world ending stocks estimate comes in at 259.2 mmt versus 259.4 last month. There is a chance that the USDA could lower US wheat exports from the current 725 mb.

- In Brazil, wheat imports are on the rise due to low supply from last season. According to Secex, Brazil imported about 439,000 mt of wheat up to the fourth week in February. For reference, February of last year saw just over 291,000 mt of wheat imported. In addition, Brazil’s wheat exports of roughly 131,000 mt were well below the 533,000 mt exported last year.

- According to China’s Minister of Agricultural and Rural Affairs, Chinese grain output was a record 695.4 mmt in 2023. This marks the ninth year in a row that they have recorded a harvest of over 650 mmt. As they work to become less reliant on other nations for their food security, there is also news that China has pledged to protect farmland. The government will work towards developing high quality land as well as restoring degraded land.

- The north African country of Morocco will reportedly need to increase their wheat imports. They struggled with a lack of rain in the fall and officials have stated that the wheat crop could be substantially below the 4mm crop last year. They are said to have their hands tied, in that they have no choice but to increase their imports.

Action Plan: Chicago Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Chicago Wheat Action Plan Summary

- No new action is currently recommended for 2023 Chicago wheat. The wheat market has continued to be dominated by lower world export prices that have stymied US export sales and depressed US prices. In early December, Grain Market Insider recommended taking advantage and making a sale on a short covering rally which was sparked by several Chinese purchases of US wheat. Since then, China has been silent in the US wheat export market, and prices remain somewhat elevated. Any remaining 2023 soft red winter wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 Chicago wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Chicago wheat. Since the early December runup on Chinese buying, the July ’24 contract has gradually stair stepped its way lower and erased those gains. In the meantime, managed funds continue to hold a sizeable, short position that could trigger another short covering rally if a bullish impetus enters the market. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for further price erosion. Although, if the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset much of the original cost and move toward a net neutral cost for the remaining position.

- No action is currently recommended for 2025 Chicago Wheat. In mid-February, July ’25 Chicago wheat broke through the bottom of the long established 632 – 685 trading range to a new low just below 600. For now, that new low is holding, and the market is correcting its oversold condition. So far, Grain Market Insider’s strategy for the 2025 crop year has been to sit tight. However, if prices rally toward the mid-600s, we will consider taking advantage of the still historically good prices to make sales recommendations.

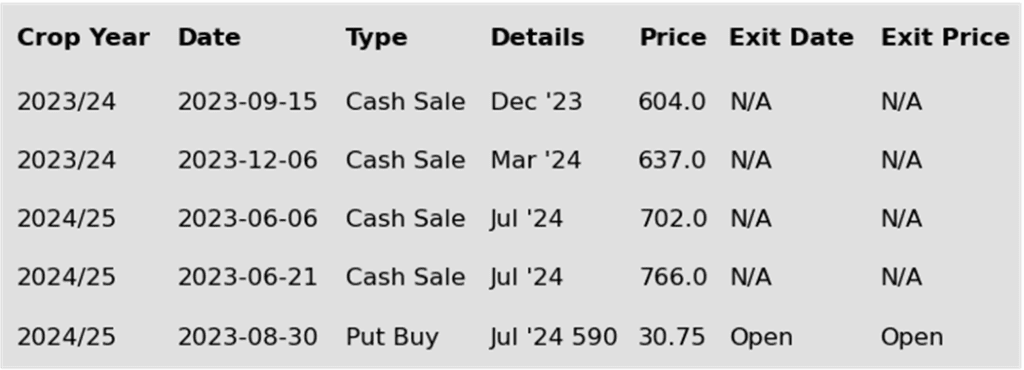

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

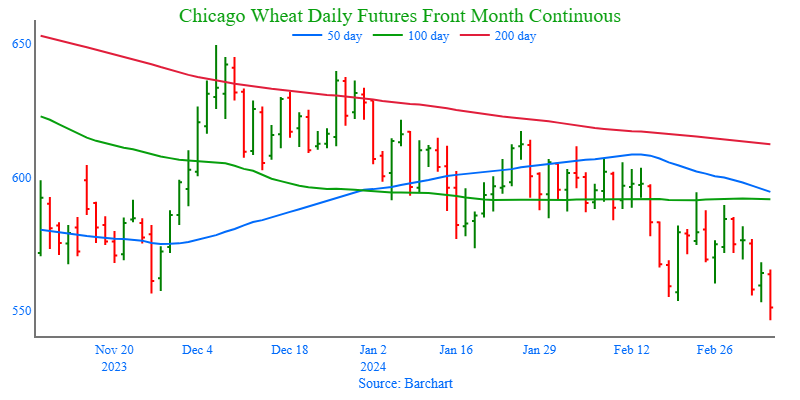

Above: With falling Russian and Black Sea export prices still pressuring the wheat market, it appears that May Chicago wheat has fallen below 555 support. Managed funds continue to hold a significant short position which is supportive and could move prices toward the 584 – 618 resistance area if they choose to cover. For now, if prices continue to retreat, the next support level below the market remains between 533 and 540.

Action Plan: KC Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

KC Wheat Action Plan Summary

- No new action is recommended for 2023 KC wheat crop. Since December’s brief runup, prices have continued to erode as US exports continue to suffer from lower world export prices. Although fundamentals remain weak, considering the market is at levels not seen since spring of 2021, and funds continue to hold a considerable net short position, these factors could trigger a return to higher prices if any unforeseen risks enter the market. Grain Market Insider’s strategy is to look for price appreciation as weather becomes a more prominent market mover and may consider suggesting additional sales if prices make a modest 20% retracement of the 2022 highs back toward 700.

- No new action is recommended for 2024 KC wheat. Since the beginning of the year, the July ’24 contract has been in a downtrend alongside the front month contracts, while also setting new contract lows and becoming very oversold. During this time, managed funds have maintained a net short position in the front month of around 35,000 contracts. While this net short position is about 15,000 contracts smaller than it was at the end of November, it is still large enough to trigger a short covering rally, much like the one that began in late November, and could easily translate to higher prices for July ’24 as well as the front months. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside, and as the market got further extended into oversold territory, Grain Market Insider recommended exiting 75% of the originally recommended position. Recently, Grain Market Insider also recommended exiting the remaining 660 puts to protect any gains that have been made. Considering bullish headwinds remain, and the equity gained from the closed July 660 put position, Grain Market Insider is prepared to consider recommending additional sales for the 2024 crop if July ‘24 retraces back toward the January highs in the mid-640s.

- No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

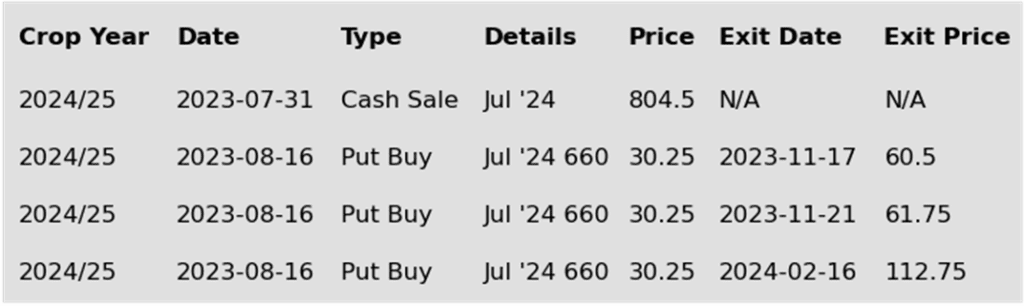

To date, Grain Market Insider has issued the following KC recommendations:

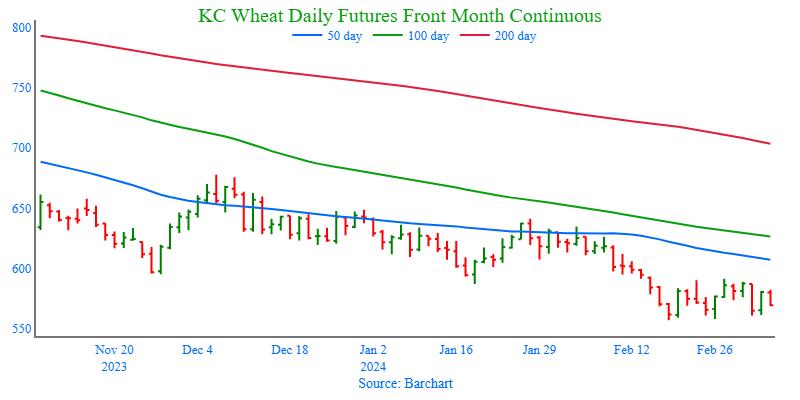

Above: May KC wheat is correcting from being oversold as it consolidates after making a 556 ¾ low on Feb. 16, with nearby resistance just overhead between 590 and 600. So far, this support level is holding, and if prices break out to the upside, further resistance may come in around 610. If they break out to the downside, then the next major support area may be found around 530.

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

- No new action is currently recommended for 2023 Minneapolis wheat. Since last summer, front month Minneapolis wheat has slowly stair-stepped lower with weaker world prices and little bullish news to move markets higher. During this time, the 50-day moving average has acted as resistance, above which the market has not been able to hold for very long. Managed funds have also established and maintained a record (or near record) short position for much of the same time. Although bullish headwinds remain, the market has become very oversold, and the large fund net short position continues to leave the market susceptible to a short-covering rally at any time here. Grain Market Insider’s strategy is to look for a modest retracement of the July high and consider additional sales in the neighborhood of 675 – 700.

- No new action is recommended for 2024 Minneapolis wheat. Much like the front month contracts, Sep ’24 has been in a downward trend since last summer. And just as Sep ’24 has been influenced to the downside by the front months, it could be similarly influenced to the upside by the front months if a bullish impetus enters the scene and triggers an extended short covering rally due to the fund’s large short position. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside (due to their higher liquidity and correlation to Minneapolis), and as the market got further extended into oversold territory, Grain Market Insider recommended exiting 75% of the originally recommended position. Recently, Grain Market Insider recommended exiting the remaining 660 puts to protect the gains that have been made. From here, Grain Market Insider is prepared to consider recommending additional sales for the 2024 crop if Sep ‘24 posts a modest 22% retracement back toward the 2022 highs of 1400.

- No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted in the spring of next year. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: May Minneapolis wheat appears to be consolidating after posting a bullish reversal on February 26. If prices continue higher, they may run into resistance around 675 – 680. If prices turn back lower, the next major support level below 640 may come in near 600.

Other Charts / Weather

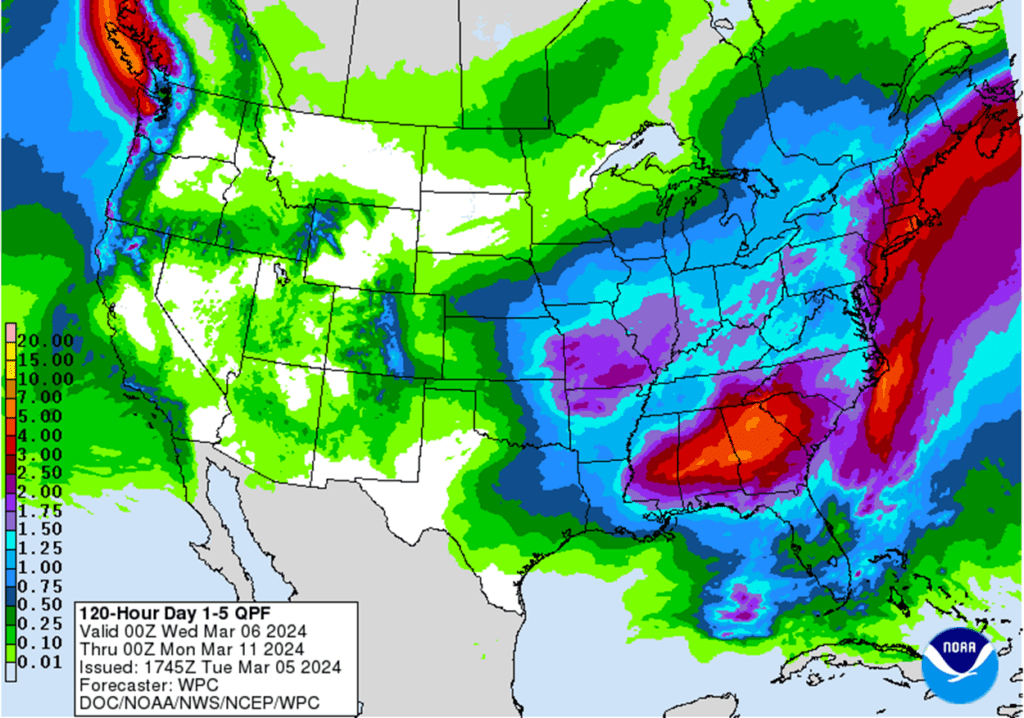

Above: US 5-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

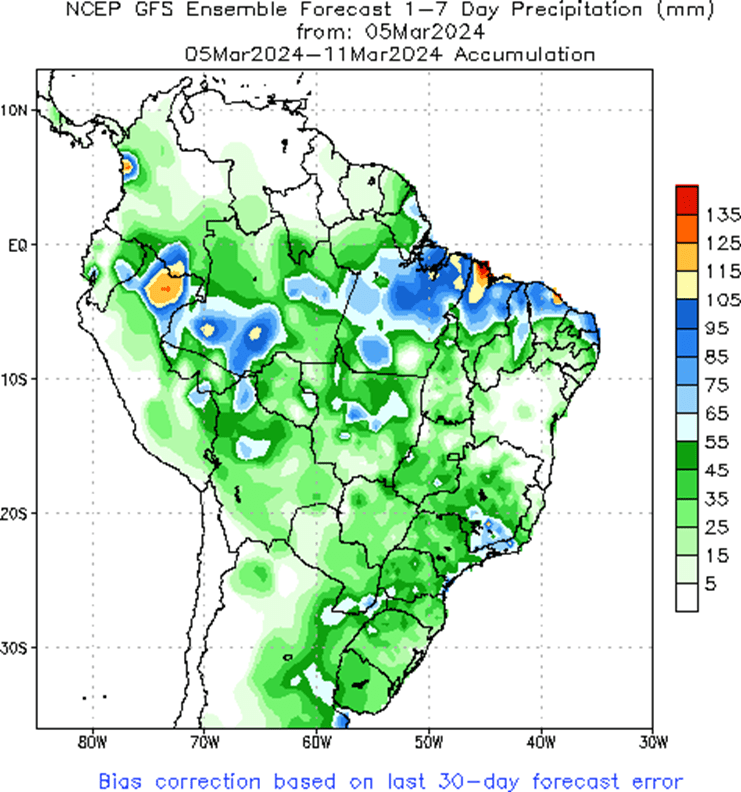

Above: Brazil 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.

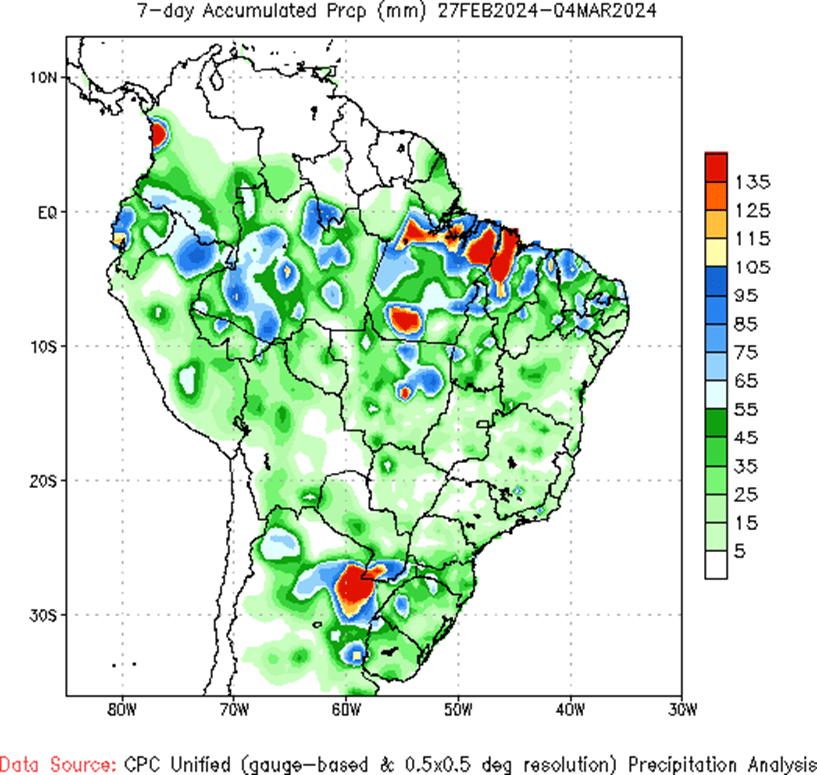

Above: Brazil 7-day total accumulated precipitation courtesy of the National Weather Service, Climate Prediction Center.