3-25 End of Day: Soybean Oil Supports Beans; While Corn and Wheat Settle Near Unchanged

All prices as of 2:00 pm Central Time

| Corn | ||

| MAY ’24 | 437.75 | -1.5 |

| JUL ’24 | 451.25 | -0.75 |

| DEC ’24 | 474.75 | -0.5 |

| Soybeans | ||

| MAY ’24 | 1209.25 | 16.75 |

| JUL ’24 | 1221.75 | 16.25 |

| NOV ’24 | 1198.75 | 11.75 |

| Chicago Wheat | ||

| MAY ’24 | 555 | 0.25 |

| JUL ’24 | 570.75 | 1.25 |

| JUL ’25 | 640.5 | 1.25 |

| K.C. Wheat | ||

| MAY ’24 | 589.5 | -1 |

| JUL ’24 | 585.5 | 0.75 |

| JUL ’25 | 634 | 2 |

| Mpls Wheat | ||

| MAY ’24 | 659.5 | -1.5 |

| JUL ’24 | 664.25 | -1.5 |

| SEP ’24 | 671.5 | -1 |

| S&P 500 | ||

| JUN ’24 | 5286.25 | -7 |

| Crude Oil | ||

| MAY ’24 | 81.95 | 1.32 |

| Gold | ||

| JUN ’24 | 2196.5 | 14.9 |

Grain Market Highlights

- The corn market continues to drift sideways ahead of Thursday’s USDA Planting Intentions and Quarterly Stocks report. Today, May corn saw a quiet 4 ¼ cent range, while weekly corn export intentions came in as expected, and ahead of the pace needed to reach the USDA’s export forecast.

- May soybeans traded both sides of unchanged in the overnight session before taking off after this morning’s open with support coming from both soybean oil and meal. The 20-day moving average held for all three legs of the soybean complex which supported technical buying off the lows. Malaysian palm oil lent extra support to soybean oil, which saw the largest gains in the complex at 1.38 cents (2.90%.)

- All three classes of wheat traded both sides of unchanged before settling mixed on the day and well off the day’s highs. Early support came from the forecast of cold weather that could hit the HRW crop as far south as Kansas and Oklahoma, with additional support from the escalation of war and restrictions on a major Russian wheat exporter.

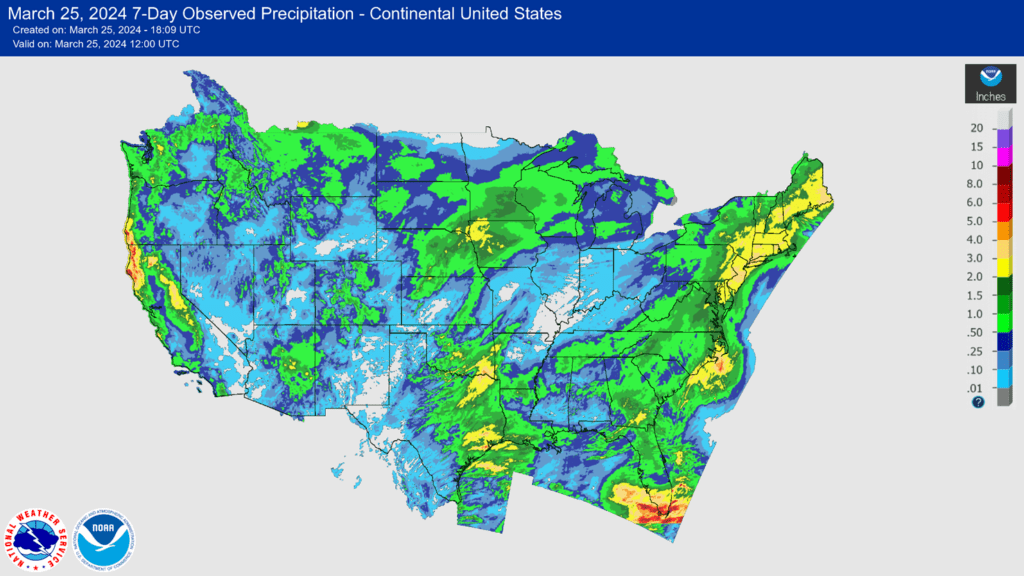

- To see the updated US 7-day observed precipitation, 7-day precipitation forecast, and the 1-week precipitation forecast for Brazil and N. Argentina, courtesy of the NWS, CPC, and NOAA, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

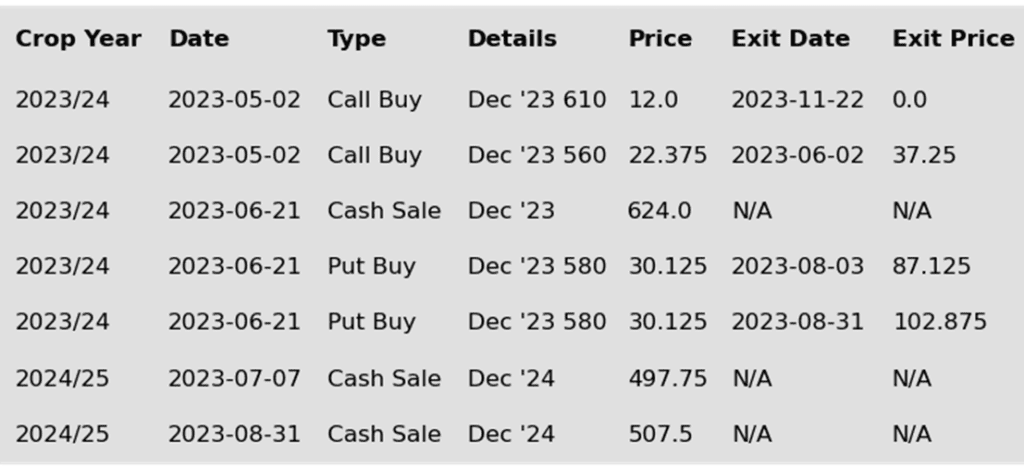

In late February, after languishing in a downtrend that began last October and managed funds posting a record net short position exceeding 340,000 contracts, corn posted a bullish key reversal. Since that time, the market has rallied as the funds covered some of their short positions, though they remain heavily short the market, which could fuel an extended rally as we head into the uncertainty of the spring planting window.

- No new action is recommended for 2023 corn. The recommendation for now is to hold off on additional sales until May corn recovers back toward the 500 level. If you need to move bushels for cash or logistics reasons, consider re-owning any sold bushels with September call options.

- No new action is recommended for 2024 corn. Given the amount of time and uncertainty that remains to market the 2024 crop, we will consider recommending additional sales on a retracement toward the low to mid 500 level.

- No Action is currently recommended for 2025 corn. For now, we aren’t considering any recommendations at this time for the 2025 crop that will be planted next year. It will probably be spring or summer of 2024 before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- The corn market is still looking for direction as daily trade remains quiet with two-sided trade inside a narrow trading range. May corn moved 4 ¼ cents from high to low during the session. Prices still seem tied to the 440-price level.

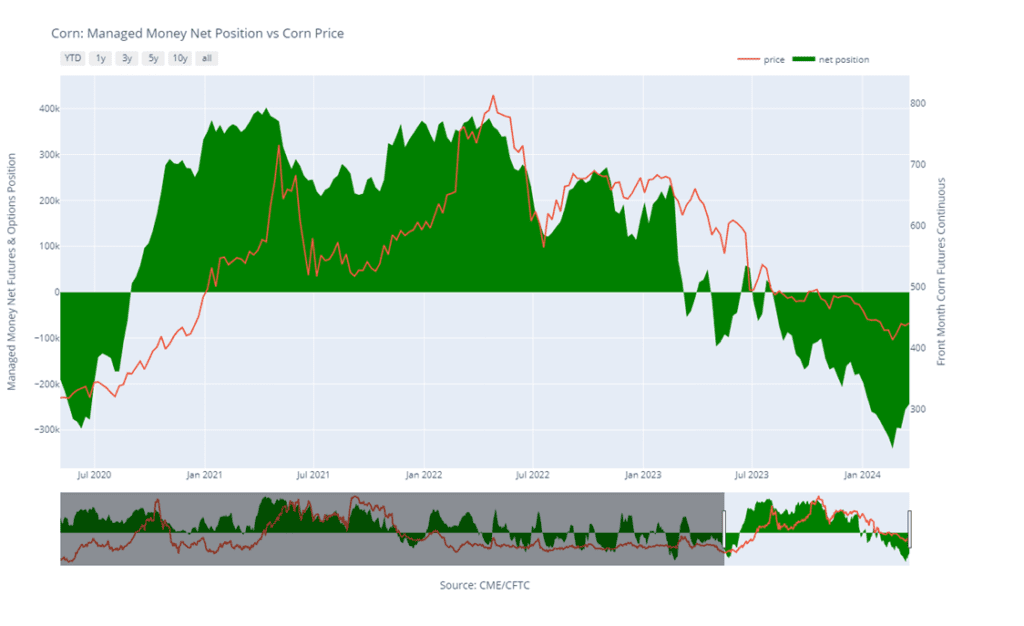

- Managed funds have been moving out of their net short position in the corn market during this recent price rally. Last week’s Commitment of Traders report released on Friday showed that funds were still net short 242,988 contracts, reduced by 12,940 contracts from the previous week. Funds are still holding a historically large net short position given the current fundamental market scenario.

- Weekly corn export inspections for corn totaled 48.3 mb (1.228 mmt) last week. Total inspections for 23/24 are at 961 mb, up 34% over last year. The USDA is targeting a 26% rise in US corn exports.

- A strong weather system is moving through the western and northern Corn Belt, providing a mixture of snow and rain to areas in need. The precipitation should help build some soil moisture levels in those areas to help promote spring planting.

- The grain markets may stay choppy going into Thursday’s USDA Planting Intentions and Grain Stocks report. With the market holding short positions, additional position squaring could bring some volatility as the market moves closer to Thursday’s report.

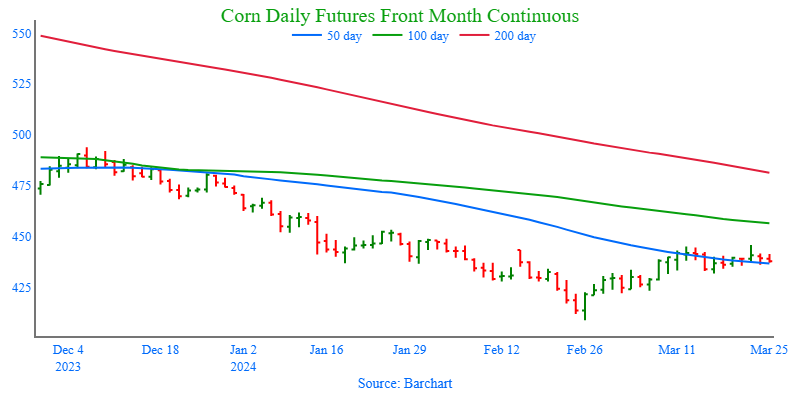

Above: The corn market continues to battle the 50-day moving average and the 435 – 445 resistance area. If it can close above 445, the market could then test the January high of 452 ¼. If prices fall back, and close below 421, then they may slide to test downside support between 400 and 410.

Above: Corn Managed Money Funds net position as of Tuesday, March 19. Net position in Green versus price in Red. Managers net bought 12,940 contracts between March 13 – 19 , bringing their total position to a net short 242,988 contracts.

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

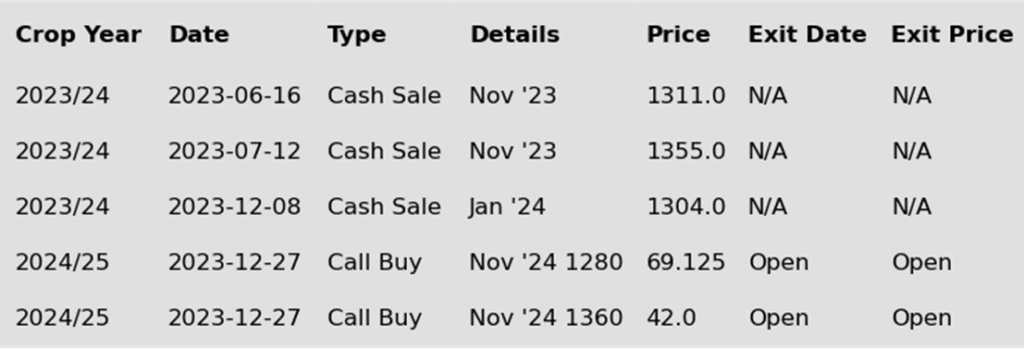

Since old crop soybeans broke out of the 1290 – 1400 range in January, prices appear to have made a near term low. Managed funds have also established a record net short position for this time of year, and world carryout has dropped according to the USDA. While new lows could still be made, US planting is not far off, and the funds current short position could fuel an extended short covering rally on a smaller South American crop, lower world soybean carryout, and potential US weather concerns.

- No new action is recommended for 2023 soybeans. The current recommendation is to refrain from making further sales until the market rebounds towards the 1300 level, which represents a modest 30% retracement from the 2022 high.

- No new action is recommended for the 2024 crop. Considering the amount of uncertainty that lies ahead with the 2024 soybean crop, we recommended back in December buying Nov ’24 1280 and 1360 calls to give you confidence to make sales against anticipated production and to protect any sales in an extended rally. Based on our research, the possibility remains that prices could retest the upper 1300 range near the 2022 highs going into spring/summer, at which point we would consider recommending additional sales.

- No Action is currently recommended for 2025 Soybeans. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

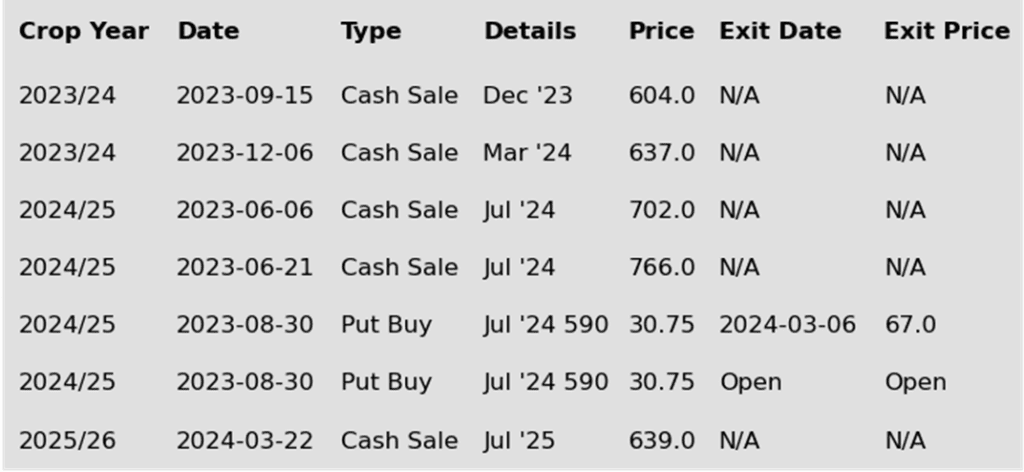

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day higher to start the week despite weakness in both corn and wheat. Prices were lower overnight but rallied into the close, closing just off the high of the day and just below yesterday’s high. Main support came from higher soybean oil which was helped by Malaysian palm oil, while soybean meal closed higher but not by as much.

- In Brazil, the soybean harvest is nearly complete with key growing state Mato Grosso finished and the rest of the country at 70% done. The USDA attaché in Brazil has lowered its estimates for Brazilian production in 23/24 to 152.6 mmt from 157.5 mmt. This change will likely be included in the USDA’s next WASDE report.

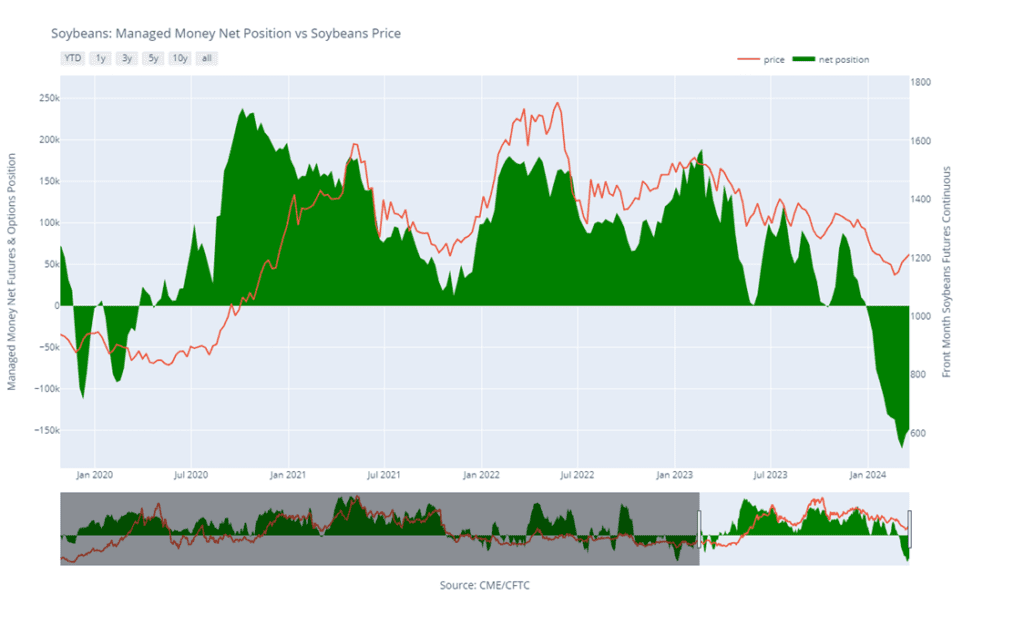

- Friday’s CFTC report showed funds buying back 6,798 contracts of their net short position reducing it to 148,399 contracts. Similar to corn, the short covering hasn’t had a very bullish effect on prices as farmer selling has ramped up to take advantage of any rallies.

- Last Friday, Argentina’s Buenos Aires Grain Exchange cut its estimates for the 23/24 corn crop but kept soybean production unchanged at 52.5 mmt. Argentina is the world’s largest exporter of soybean meal, so any issues in the growing season could be friendly to meal.

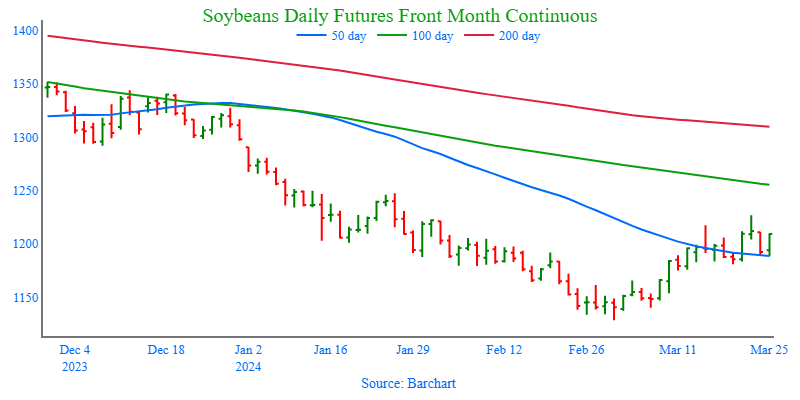

Above: Although May soybeans rejected a rally through the previous high of 1217 ½, they could still test the January high of 1247 ½ if downside support near 1175 continues to hold and if prices close above 1226 ¾. If not, the market runs the risk of retreating down toward the 1130 – 1140 support area.

Above: Soybean Managed Money Funds net position as of Tuesday, March 19. Net position in Green versus price in Red. Money Managers net bought 6,798 contracts between March 13 – 19, bringing their total position to a net short 148,399 contracts.

Wheat

Market Notes: Wheat

- Wheat had a mostly higher close while still closing off session highs. Early support came from a lower US Dollar Index, as well as the forecast of a cold snap this week that could hit as far south as Kansas and Oklahoma. This is raising concern that there will be some damage to the HRW crop as it exits dormancy.

- Russian attacks on Odesa power plants gave wheat a boost today, with concern that port operations would be disrupted. Additionally, the second largest Russian wheat exporter was forced to keep vessels in port for not obtaining the necessary phytosanitary permits.

- Weekly wheat inspections were on the softer side at 11.6 mb and brought total 23/24 export inspections to 521 mb. That is down 15% from last year and inspections and behind the USDA’s estimated pace.

- According to a Bloomberg survey, the average pre-report estimate for wheat acreage in this week’s USDA report is 47.3 million, which compares to 49.6 ma last year. Additionally, quarterly wheat stocks are projected to be up 11.3% at 1.05 bb which compares to 941 mb last year.

Action Plan: Chicago Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

Active

Sell JUL ’25 Cash

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Chicago Wheat Action Plan Summary

Since the early December runup, Chicago wheat has suffered in a lower trend while going on to make new contract lows. Although the lack of any bullish information has been disappointing, the market is in a significantly oversold condition, and managed funds continue to hold a significant net short position. Either or both could fuel a short covering rally at any time as we head into the more active part of the growing season.

- No new action is currently recommended for 2023 Chicago wheat. Any remaining 2023 soft red winter wheat should be getting priced into market strength. Grain Market Insider won’t have any “New Alerts” for 2023 Chicago wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Chicago wheat. At the end of August, we recommended purchasing July ‘24 590 puts to prepare for further price erosion, and recently recommended exiting half of those puts to lock in gains and get closer to a net neutral cost on the remaining position. For now, the current recommendation is to hold off on making any additional sales unless the market moves back toward last summer’s highs. At which point, we are prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the remaining July ‘24 590 put position will add a layer of protection if prices erode further.

- Grain Market Insider sees a continued opportunity to sell a portion of your 2025 SRW wheat crop. In mid-February, the July ’25 Chicago wheat contract broke through the bottom of the long standing 640 – 685 trading range and traded down to the 597 ½low. Prices have rallied 50% back toward the high of that range. While a lot of time remains in which many unforeseen circumstances can unfold to move prices even higher, Grain Market Insider recommends taking advantage of this rally, and these historically good prices, to make an early sale and begin marketing your 2025 SRW crop.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

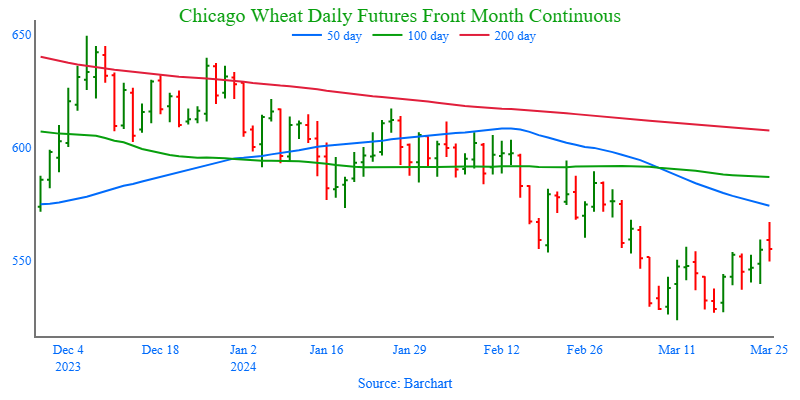

Above: Chicago wheat posted a bearish reversal on March 25, indicating there is significant resistance above the market near the 50-day moving average. Prices could still challenge the 50 and 100-day moving averages and the 585 – 620 congestion area if they rebound and close above 567. Otherwise, if they retreat and close below 523 ½, the next level of major support may come in around 488.

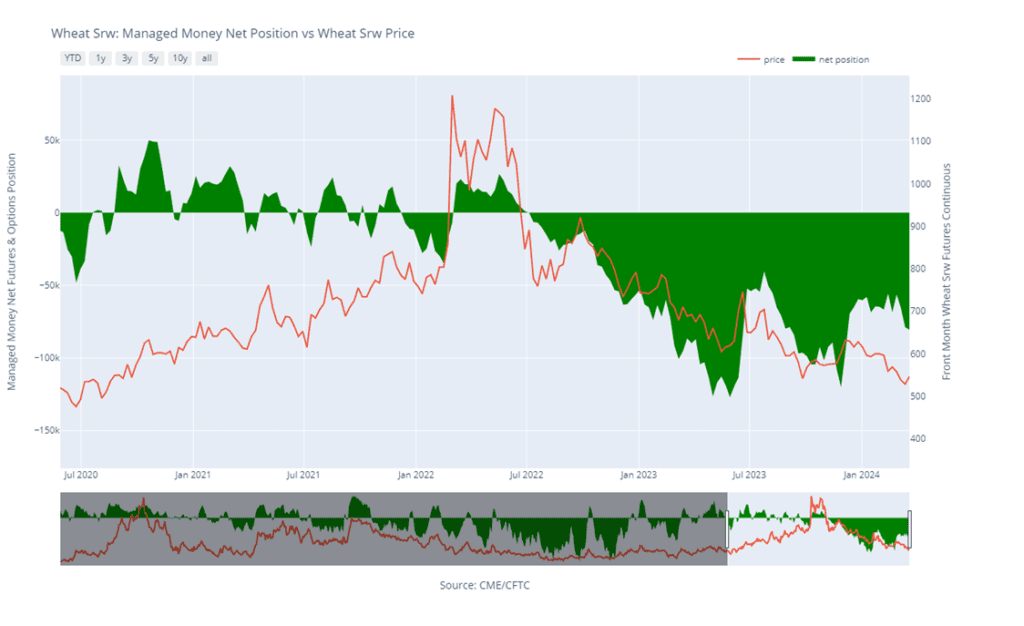

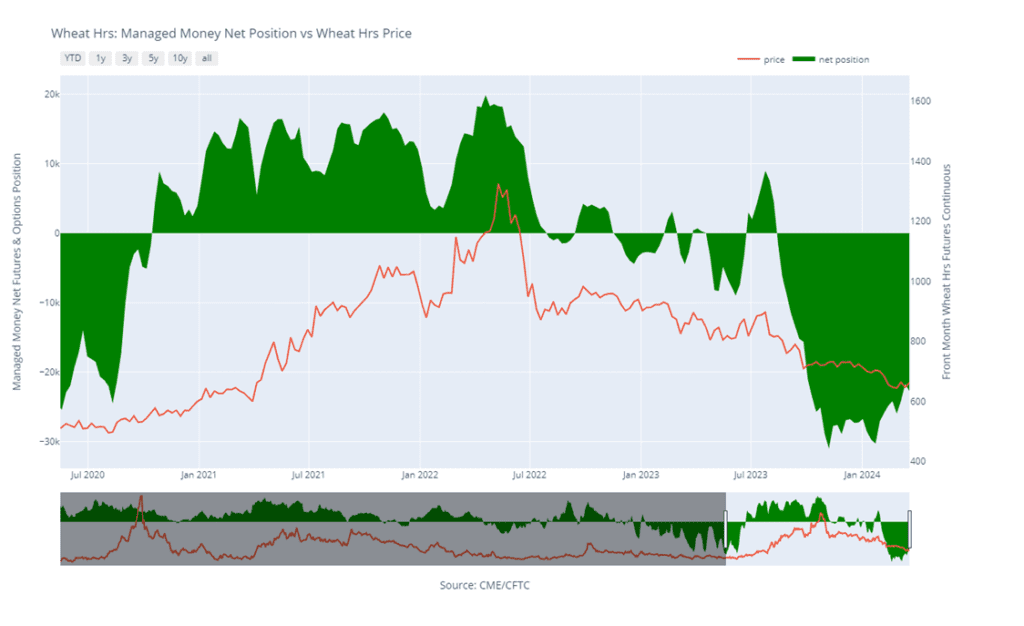

Above: Chicago Wheat Managed Money Funds net position as of Tuesday, March 19. Net position in Green versus price in Red. Money Managers net sold 1,700 contracts between March 13 – 19, bringing their total position to a net short 80,570 contracts.

Action Plan: KC Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

KC Wheat Action Plan Summary

Since December’s brief runup, prices have continued to erode as US exports continue to suffer from lower world export prices. Although fundamentals remain weak. Managed funds continue to hold a considerable net short position, and the market is at levels not seen since spring of 2021, which combined could trigger a return to higher prices if any unforeseen risks enter the market.

- No new action is recommended for 2023 KC wheat crop. The current strategy is to look for price appreciation as weather becomes a more prominent market mover and consider suggesting additional sales if prices make a modest 20% retracement of the 2022 highs back toward the upper 600s

- No new action is recommended for 2024 KC wheat. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside, and recommended exiting the original position in three separate tranches as the market got further extended into oversold territory to protect any gains that were made. Taking the equity gained from the closed July 660 put position into account, the current strategy for the 2024 crop is to wait for better opportunities and consider recommending additional sales if July ‘24 retraces back toward the January highs in the mid-630s.

- No action is currently recommended for 2025 KC Wheat. We currently aren’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

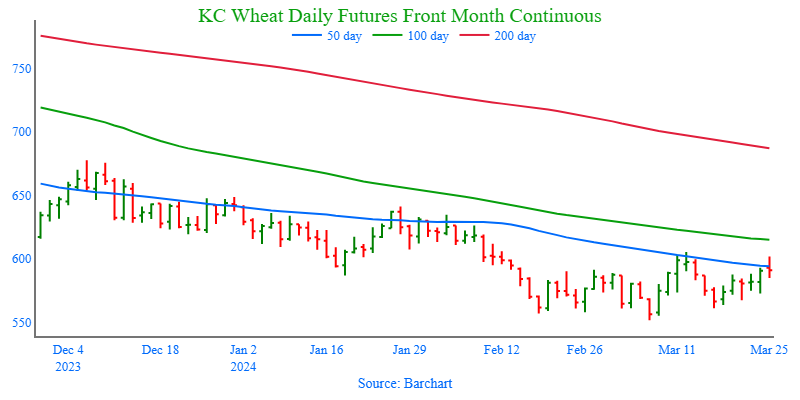

Above: The inability of the market to close above the 50-day moving average (dma) suggests considerable resistance in this area, potentially leading to a test of support near the 551 ½ low if initial support near 575 is broken. However, if prices do manage to close above the 50 dma and the March 10 high of 605 ¼, there’s a possibility of a rally towards the congestion range between 610 and 640. Although with substantial support around 551 ½, a breach below this level could lead to a test of 530.

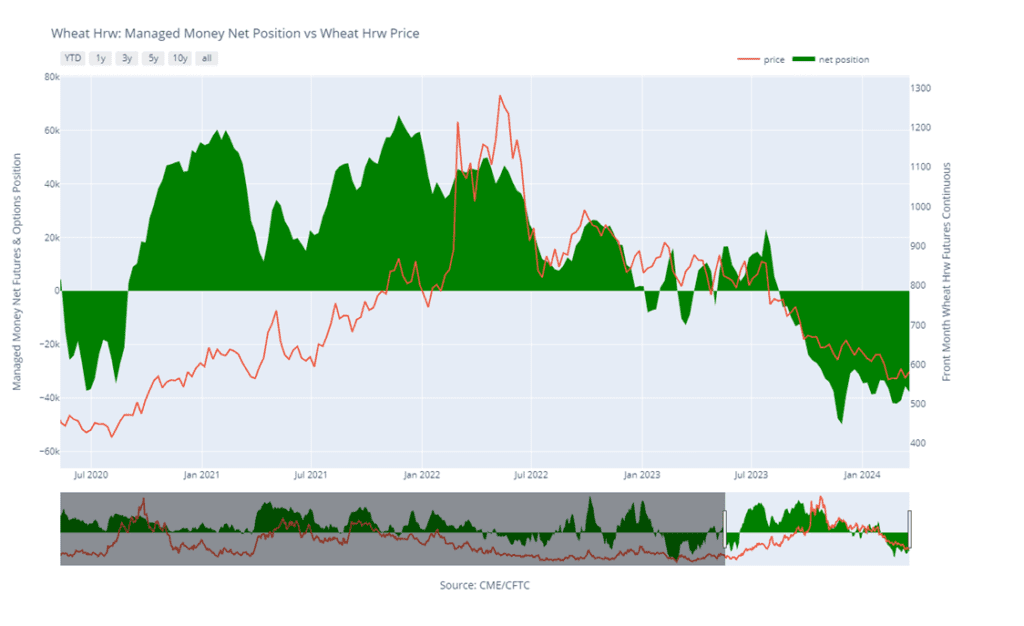

Above: KC Wheat Managed Money Funds net position as of Tuesday, March 19. Net position in Green versus price in Red. Money Managers net sold 2,310 contracts between March 13 – 19, bringing their total position to a net short 37,857 contracts.

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

Since last summer, Minneapolis wheat has slowly stair-stepped lower with weaker world prices and little bullish news to move markets higher. During this time, the 50-day moving average has acted as resistance, above which the market has not been able to hold for very long. Managed funds have also established and maintained a record (or near record) short position for much of the same time. Although bullish headwinds remain, the market has become very oversold, and the large fund net short position continues to leave the market susceptible to a short-covering rally at any time.

- No new action is currently recommended for 2023 Minneapolis wheat. The current strategy is to look for a modest retracement of the July high and consider additional sales in the neighborhood of 675 – 700.

- No new action is recommended for 2024 Minneapolis wheat. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts (due to their higher liquidity and correlation to Minneapolis), to protect the downside, and recommended exiting the original position in three separate tranches as the market got further extended into oversold territory to protect any gains that were made. From here, the strategy for the 2024 crop is to consider recommending additional sales if Sep ‘24 posts a modest 22% retracement back toward the 2022 highs of 1400.

- No action is currently recommended for the 2025 Minneapolis wheat crop. We are currently not considering any recommendations at this time for the 2025 crop that will be planted in the spring of next year. It may be late spring or summer before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: Minneapolis wheat continues to trade in a congestion pattern following the retreat from overhead resistance near the 50-day moving average. Initial support below the market remains near the recent low of 641, with support near 600 if prices fall further. Overhead, if the market reverses and closes above 675 – 680 resistance, they could challenge the 700 – 710 area.

Above: Minneapolis Wheat Managed Money Funds net position as of Tuesday, March 19. Net position in Green versus price in Red. Money Managers net sold 1,032 contracts between March 13 – 19, bringing their total position to a net short 22,733 contracts.

Other Charts / Weather

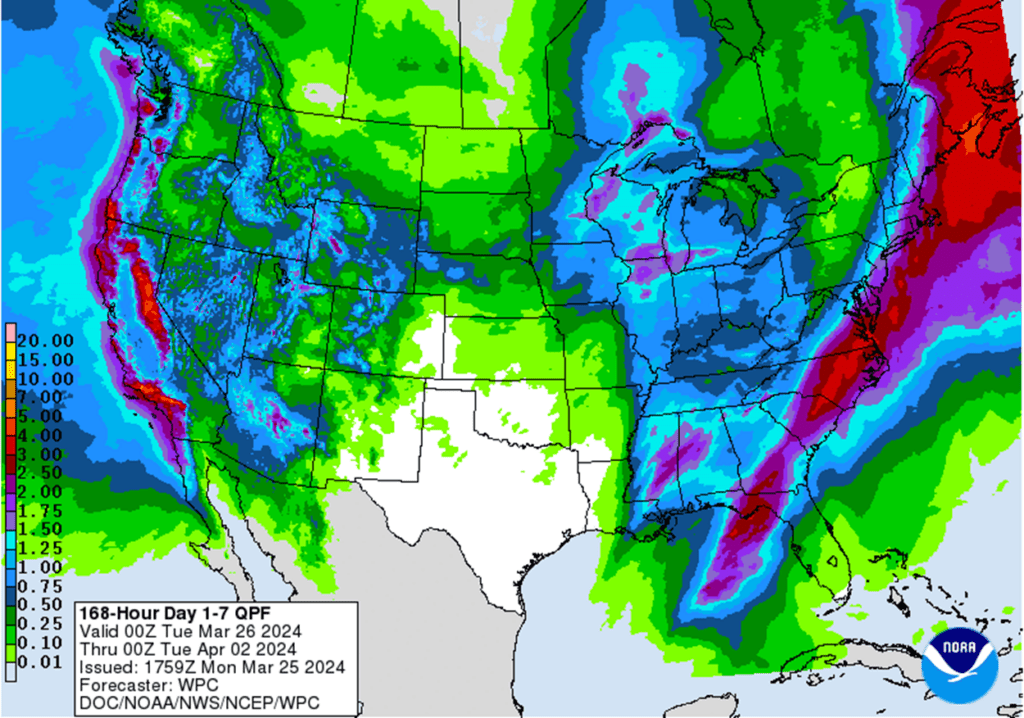

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center

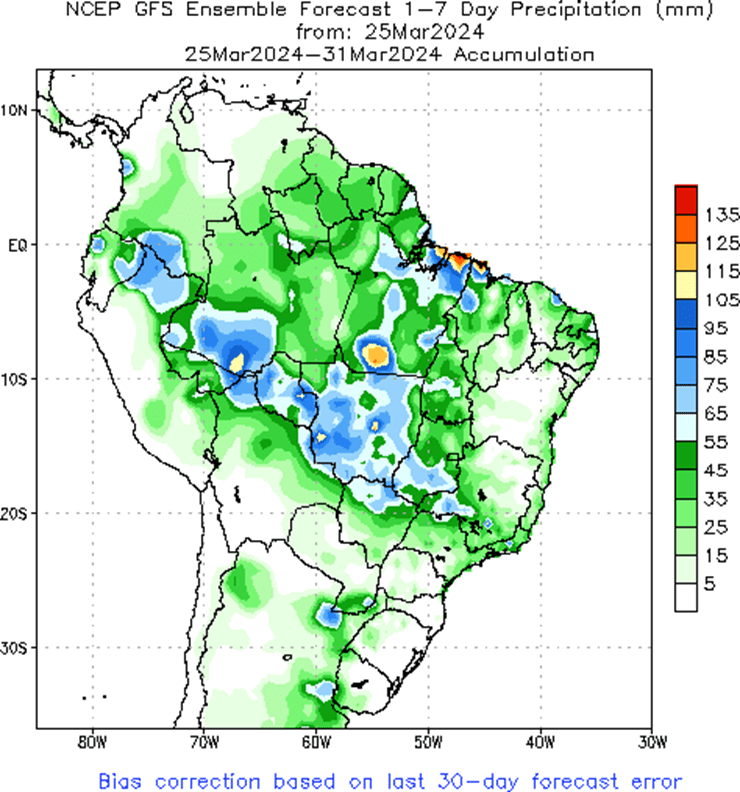

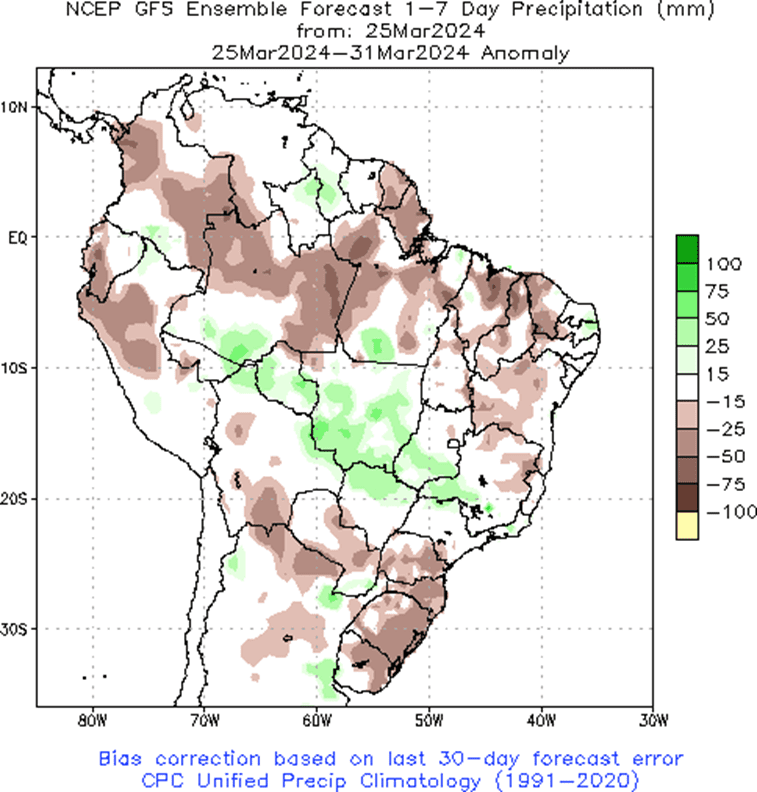

Above: Brazil and N. Argentina 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center

Above: Brazil and N. Argentina 1-week forecast precipitation, percent of normal, courtesy of the National Weather Service, Climate Prediction Center