3-19 End of Day: Mixed Close for Corn, Soybeans Lower, Wheat Drops on Wetter Outlook

All Prices as of 2:00 pm Central Time

| Corn | ||

| MAY ’25 | 462 | 3.25 |

| JUL ’25 | 469.25 | 1.25 |

| DEC ’25 | 451.5 | -2.75 |

| Soybeans | ||

| MAY ’25 | 1008.25 | -4.5 |

| JUL ’25 | 1021.5 | -5 |

| NOV ’25 | 1010 | -5.5 |

| Chicago Wheat | ||

| MAY ’25 | 563.5 | -1.5 |

| JUL ’25 | 580 | -2 |

| JUL ’26 | 645.25 | -0.5 |

| K.C. Wheat | ||

| MAY ’25 | 594.75 | -11.5 |

| JUL ’25 | 608.75 | -10.25 |

| JUL ’26 | 657.75 | -5 |

| Mpls Wheat | ||

| MAY ’25 | 611.75 | -2.25 |

| JUL ’25 | 627.5 | -2.75 |

| SEP ’25 | 641.25 | -2.25 |

| S&P 500 | ||

| JUN ’25 | 5726.25 | 57 |

| Crude Oil | ||

| MAY ’25 | 66.95 | 0.2 |

| Gold | ||

| JUN ’25 | 3084.2 | 15.3 |

Grain Market Highlights

- Corn: Futures ended mixed again on Wednesday, but unlike yesterday, old crop contracts closed higher while new crop contracts finished lower.

- Soybeans: Soybeans ended the day slightly lower, similar to yesterday’s movement. Soybean oil and meal futures also closed lower, with soybean meal posting the larger losses.

- Wheat: Wetter conditions forecasted for the Plains led to a lower close across the board for wheat futures on Wednesday, with KC futures taking the brunt of the decline.

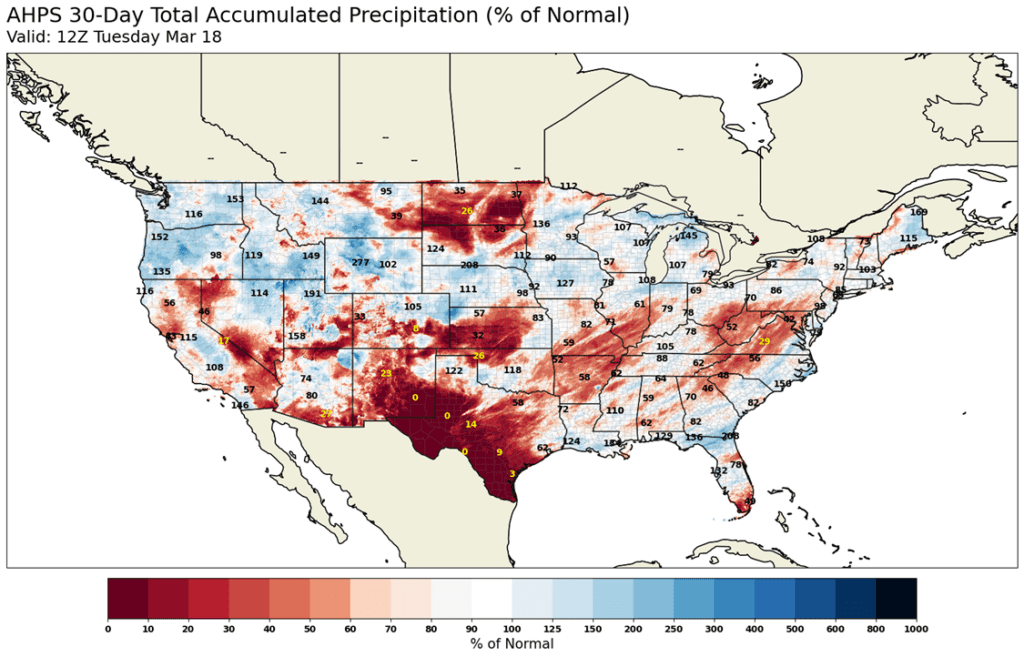

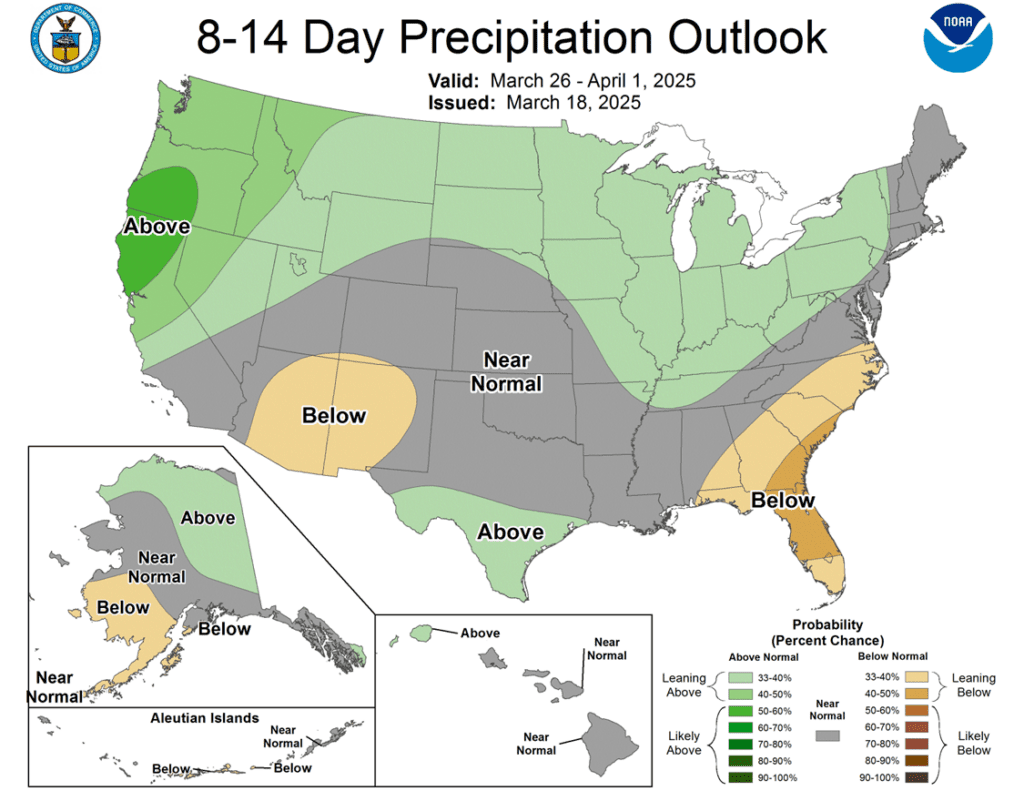

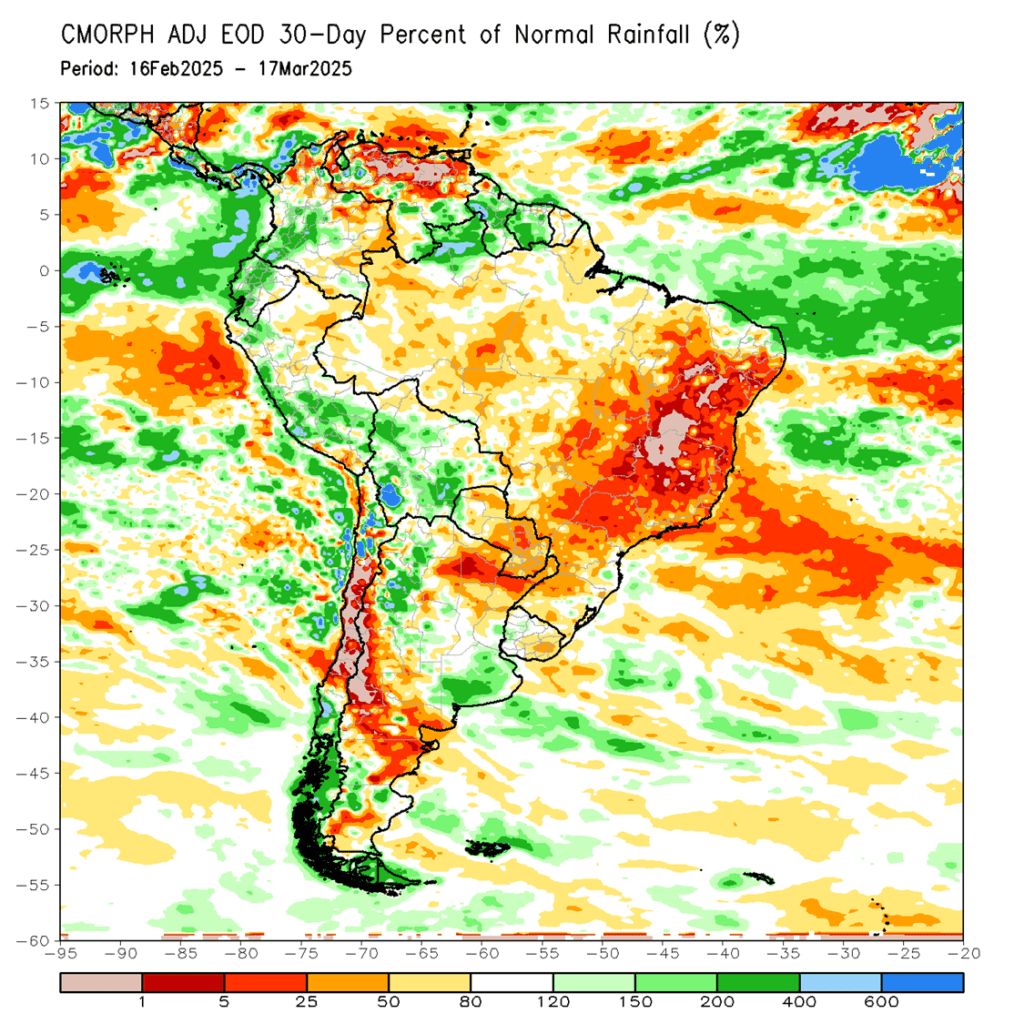

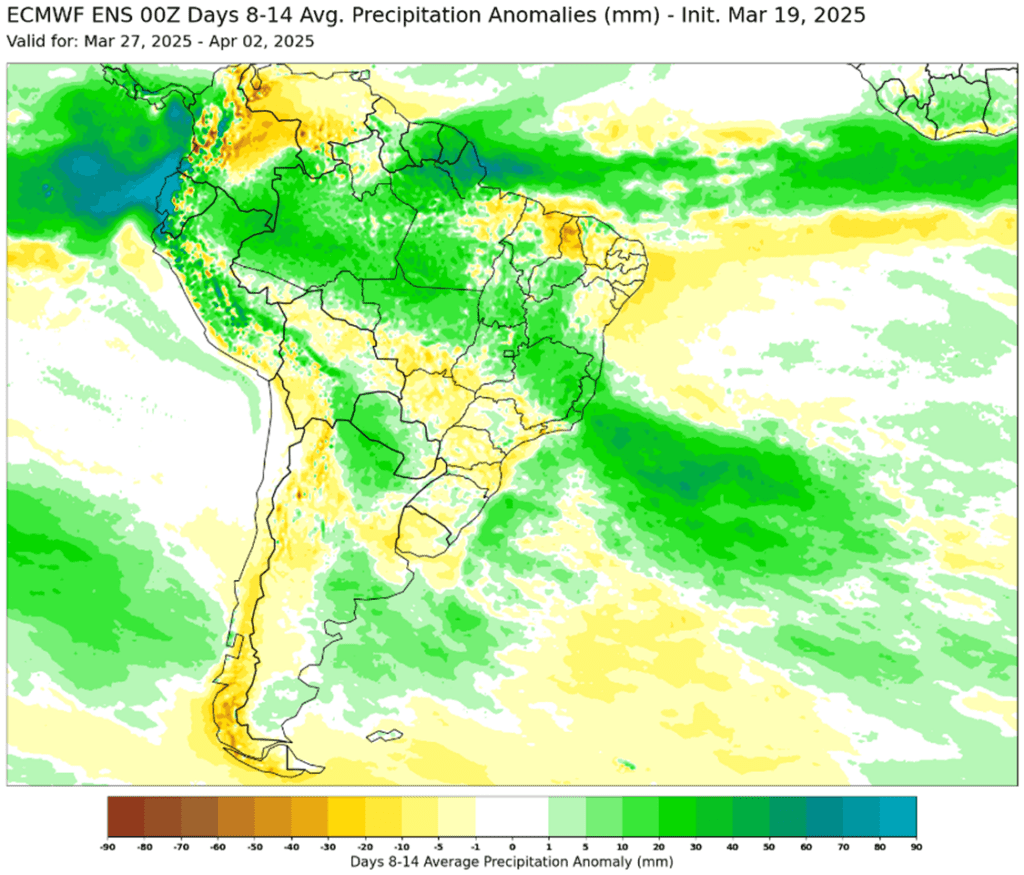

- To see the updated 30-day percent of normal precipitation map and the 8–14-day precipitation outlook for South America and the U.S., scroll down to the charts/weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

Active

Sell DEC ’26 Cash

Puts

2024

No New Action

2025

No New Action

2026

No New Action

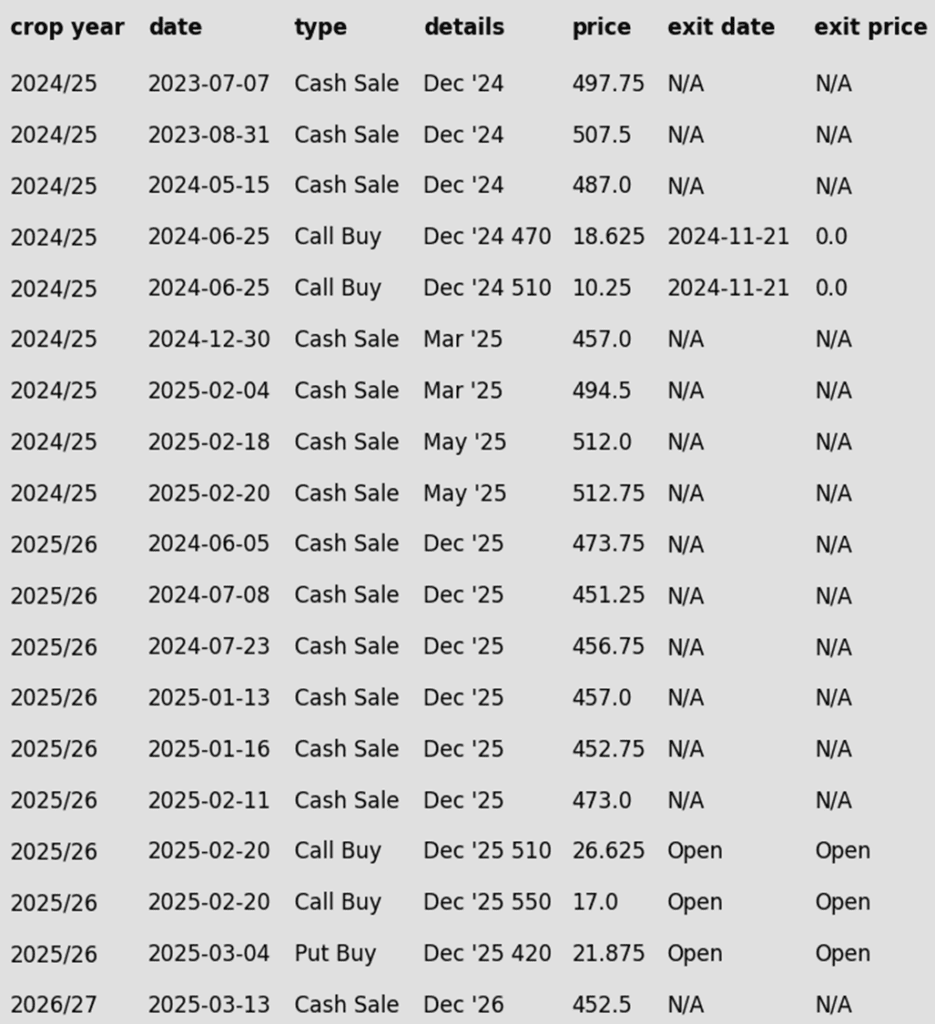

2024 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Since last summer, seven official sales recommendations have been made at an average price of 495.50. If you are behind, target 480 vs May as a first spot to begin catching up.

- Grain Market Insider has not yet set an official price target for an eighth sale but remains satisfied with the sales recommendations made to date. The Prospective Plantings and Grain Stocks reports, scheduled for release on March 31, are approaching quickly. Given the high volatility typically seen on report day, Grain Market Insider is likely to hold off on any new recommendations until after the report — unless market conditions shift significantly.

2025 Crop:

- Plan A: Exit all 510 December calls @ 43-5/8 cents. Exit half of the December 420 puts @ 43-3/4 cents.

- Plan B: No active targets.

- Details:

- Since last spring, six sales recommendations have been made for the 2025 crop at an average price of 460.75. If you are behind, target 462 vs December as a first spot to begin catching up.

- Grain Market Insider feels confident about the overall strategy heading into the volatile March 31 reports and into spring/summer. There are the six sales recommendations on the books at an average price of 460.75. Additionally, 510 and 550 call options are in place to capture upside potential if the highs are not in. On the downside, 420 put options cover unsold bushels, providing protection against lower prices. This balanced strategy allows flexibility to adjust as the market moves in either direction.

2026 Crop:

- CONTINUED OPPORTUNITY – Sell the first portion of your 2026 corn crop.

- Details: Early sales can be impactful in years when prices trend sideways or lower. For last year’s 2024 corn crop, the sales recommendations made in 2023 at 497.75 and 507.50 ended up outperforming anything offered after January 1, 2024, for bushels that had to be sold at harvest. While this won’t be the case every year, history shows that sideways or lower years tend to outnumber higher years. Consistently applying early sales strategies year after year can provide long-term benefits.

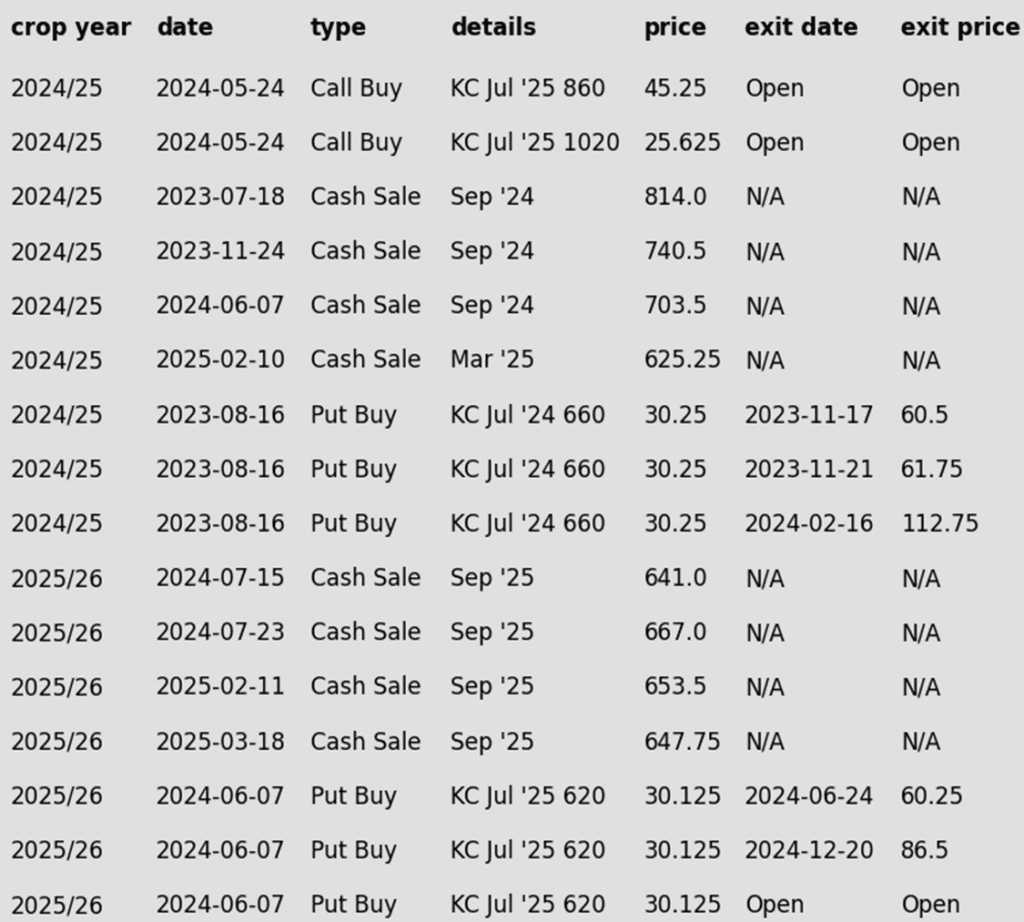

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn futures traded mixed on Wednesday, with light buying strength returning to old crop contracts, while new crop prices remained under pressure.

- Traders are positioning ahead of the USDA Prospective Planting and Grain Stocks report, which could shape market direction. Analysts expect strong demand to be reflected but also anticipate a significant increase in corn acreage compared to last year.

- Weekly ethanol production rebounded over last week. Production jumped to 325 million barrels/day (mbpd) versus 312 mbpd last week, up 5.6% over last year. An estimated 111 mb of corn was used in the production of ethanol last week. This total is still trending ahead of USDA targets for the marketing year.

- USDA export sales data will be released Thursday, with new corn sales for the week ending March 13 projected between 800,000 MT and 1.7 MMT. Last week’s total was 967,000 MT.

- With planting mostly complete on the key second crop Brazil corn, weather becomes the focus. Early-season conditions are favorable, with expected rainfall supporting crop development.

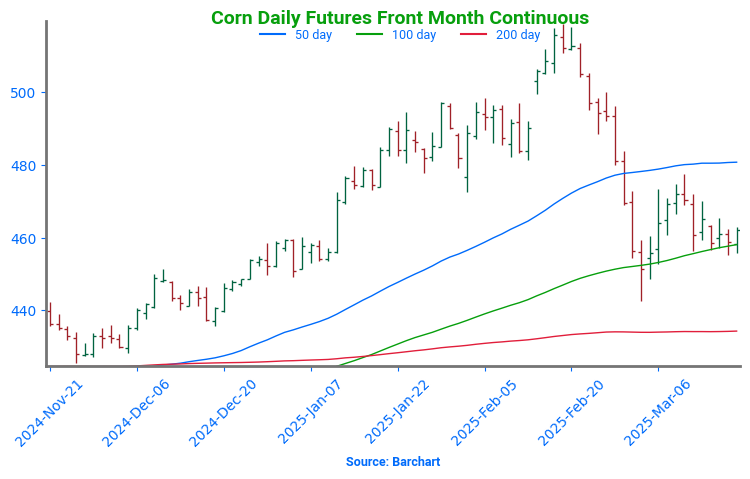

Corn Finds Its Footing After Sharp Pullback

After soaring to 16-month highs in late February, corn futures took a steep dive, retreating to test key technical levels. Prices recently found support near 450, aligning with both the 100-day moving average and a critical trendline—potentially marking a short-term low as the market pivots toward spring planting.

A rebound from this level suggests renewed strength, but hurdles remain. Initial resistance looms near the 50-day moving average, while stronger support sits deeper at the 200-day moving average. With the USDA’s March planting intentions report on the horizon and weather developments in both South America and the U.S., volatility could return swiftly, keeping traders on high alert.

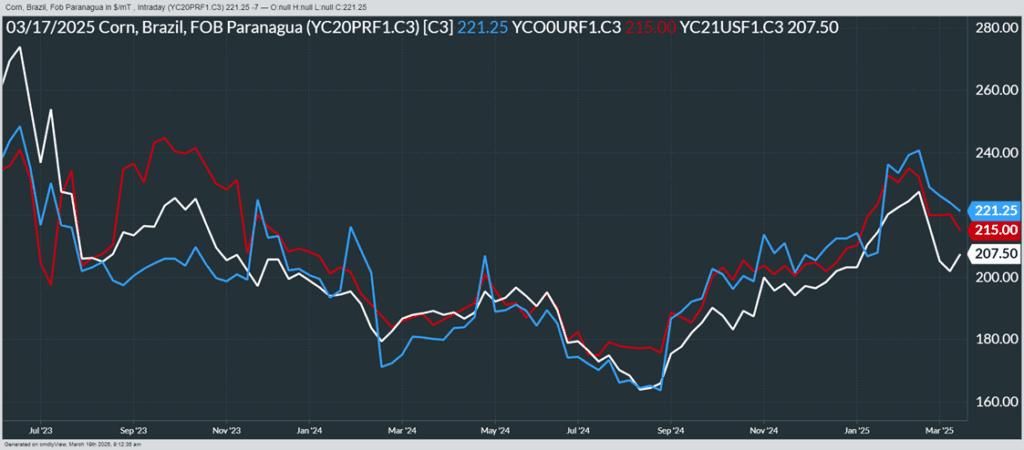

Above: From Barchart – World Corn Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red)

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: Next cash sale at 1107 vs May. Buy calls with a close over 1079.75 vs May.

- Plan B: No active targets.

- Details:

- Since last spring, three official sales recommendations have been made at an average price of 1089. If you’re behind, consider targeting 1056 vs May as a good starting point to begin catching up.

- The official target for a fourth sale is 1107 vs May. Since soybeans tend to have later seasonal pricing opportunities than corn, the plan is to aim for an aggressive target for now.

- A close above the February high resistance of 1079.75 would trigger a recommendation to re-own the three prior sales with August call options.

2025 Crop:

- Plan A: Next cash sale at 1114 vs November. Exit all 1100 November call options at 88 cents.

- Plan B: No active targets.

- Details:

- There has been one official sales rec on 2025 soybeans to date. If you’re behind, consider targeting 1040 vs November to catch up.

- If the 1100 November calls can be exited for 88 cents, that should cover the cost of the 1180 calls, providing a net-neutral cost position that can continue to protect the upside on the previous sales recommendation.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Still not expecting the first targets for at least another couple months.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans were lower to end the day but have maintained their rangebound trade. Weather in Brazil has been relatively good for the completion of harvest, and the country has been exporting large amounts of soybeans putting pressure on U.S. demand. Both soybean meal and oil ended the day lower with meal posting the larger losses.

- Brazilian soybean basis has improved recently due to high Chinese demand despite the record large crop being harvested, and Chinese February soybean imports increased to 13.6 mmt which is up 4.4% from a year ago. Brazilian exports for March are expected to reach 15.6 mmt compared to 13.5 mmt a year ago.

- It is expected that the EPA will propose U.S. biofuel blending targets for 2026 in April or May according to Darling Ingredients. The industry is asking for a 2 billion gallon increase to biomass-based diesel volumes from existing blending targets.

- Brazil’s soybean harvest reached 70% as of March 13, the fastest pace on record per AgRural. The southeast and northern regions expect above-average rainfall in the next 6-10 days.

Soybeans Find Support Near 1000

Soybean futures tested the 200-day moving average in early 2025, a stubborn resistance level that has kept rallies in check for 18 months. As March unfolded, favorable weather and harvest pressure from South America triggered a sharp selloff, sending prices tumbling. Despite the decline, support held firm around the psychological 1000 level, with a stronger backing near 950. If the market continues to rebound, initial resistance sits at 1030, but the 200-day moving average remains a formidable hurdle.

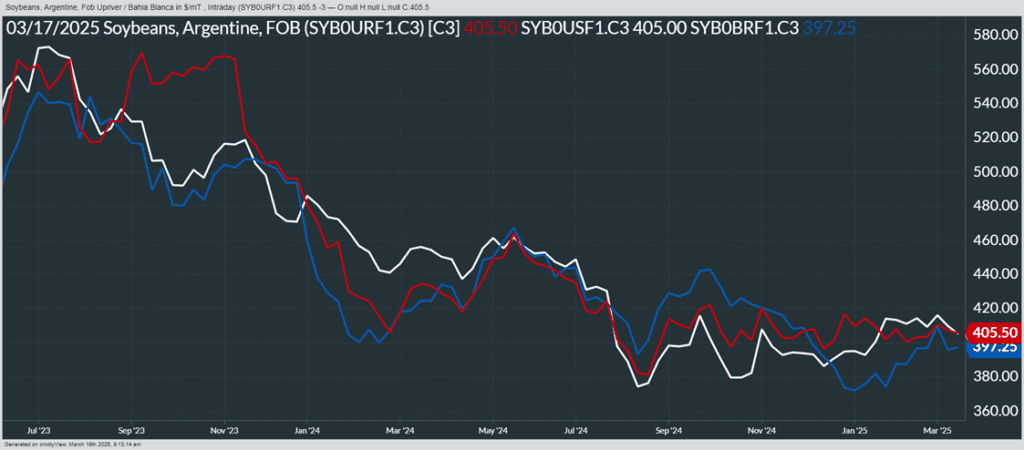

Above: From Barchart – World Soybean Export Prices in U.S. Dollars per metric ton. Brazil (Blue), U.S. NOLA (White), Argentina (Red)

Wheat

Market Notes: Wheat

- Improved precipitation chances from a Midwestern storm pressured the wheat market Wednesday, leading to profit-taking from the recent rally. HRW futures saw the most selling pressure.

- Rain and snowfall forecasts for parts of Kansas are expected to provide much-needed moisture to winter wheat crops.

- Technically, wheat futures followed through from the soft close on Tuesday. Wheat futures are testing support levels with today’s close. These levels need to hold, or the wheat market is at risk of breaking the most recent trend higher, likely leading to further downside correction.

- The USDA will release weekly export sales for wheat on Thursday morning. For the week ending March 13, reported sales are expected to range from 300,000-700,000 MT of new sales. Last week US exporters sold 783,416 MT, which was above trade expectations.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: Target 701 vs May to make the next sale.

- Plan B: No active targets. Monitoring various indicators for the development of sell signals that could suggest making a preemptive sale — before 701 hits.

2025 Crop:

- Plan A: Target 714 vs July ‘25 to make the next sale.

- Plan B: No active targets. Monitoring various indicators for the development of sell signals that could suggest making a preemptive sale — before 714 hits.

2026 Crop:

- Plan A: Target 704 vs July ‘26 to make the next sale.

- Plan B: No active targets. Monitoring various indicators for the development of sell signals that could suggest making a preemptive sale — before 704 hits.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Faces Key Test After February Surge

After months of sideways grinding, Chicago wheat broke out in February, rallying to early October highs just above 615. However, that mid-month peak quickly turned into a reversal point, with futures slipping back into the previous trading range that defined late 2024. For now, support near 540 has held firm, marking the lower boundary of this range, while the 200-day moving stands as the next major test. A decisive weekly close above this level could shift momentum, potentially setting the stage for a trend reversal and renewed upside.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: Target 717 vs May to make the next sale.

- Plan B: No active targets. Monitoring various indicators for the development of sell signals that could suggest making a preemptive sale — before 717 hits.

2025 Crop:

- Plan A: Target 677 vs July ’25 to make the next sale.

- Plan B: No active targets. Monitoring various indicators for the development of sell signals that could suggest making a preemptive sale — before 677 hits.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Still not expecting the first targets for another two to three months — likely around May or June.

To date, Grain Market Insider has issued the following KC recommendations:

Kansas City Wheat Seeks Direction After February Whiplash

February was a wild ride for Kansas City wheat, with prices surging higher before tumbling back down, ultimately finishing the month little changed. Now, with weather concerns heating up in March, futures have regained momentum, climbing back above the pivotal 200-day moving average. Looking ahead, the 200-day moving average should act as support on any pullback, while February highs near 640 remain a formidable barrier to the upside. A breakout above this level could signal a more sustained rally, but for now, the market remains in a tug-of-war between bullish weather risks and technical resistance.

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

Active

Sell SEP ’25 Cash

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Plan A: Target 625 vs May to make the next sale.

- Plan B: No active targets. Monitoring various indicators for the development of sell signals that could suggest making a preemptive sale — before 625 hits.

2025 Crop:

- CONTINUED OPPORTUNITY – Sell another portion of your 2025 HRS wheat crop following the recent hit of the 647.75 target.

- Plan A: No active targets.

- Plan B: No active targets.

2026 Crop:

- Plan A: No active targets.

- Plan B: No active targets.

- Details:

- Still not expecting the first targets for another three to four months — likely around June or July.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Spring Wheat Struggles to Hold Breakout Amid Volatility

Spring wheat broke out of its long-standing sideways range in late January, sparking a wave of bullish momentum. The rally gained traction in mid-February with a close above the 200-day moving average, but late-month weakness erased those gains, pulling futures back below key technical levels. Now, the 200-day moving average looms as resistance, capping any rebound attempts, while support near 580 remains critical to preventing further downside. To reignite the uptrend, futures would need a sustained move back above the 200-day, with the next upside test at February highs near 660. Until then, the market remains in search of direction amid shifting fundamentals.

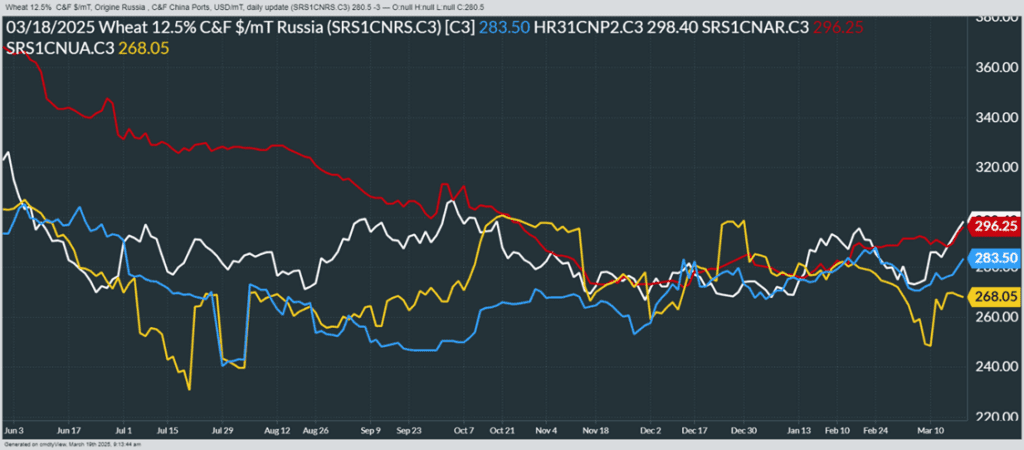

Above: From Barchat – World Wheat Export Prices in U.S. Dollars per metric ton. Russia (Blue), U.S. PNW (White), Argentina (Red), Ukraine (Yellow)

Other Charts / Weather