2-27 End of Day: Grains Close Lower Following Reports of Tariff Implementation

All Prices as of 2:00 pm Central Time

| Corn | ||

| MAR ’25 | 464.75 | -13.5 |

| JUL ’25 | 486.75 | -11.75 |

| DEC ’25 | 461.75 | -5.25 |

| Soybeans | ||

| MAR ’25 | 1022.75 | -1.75 |

| JUL ’25 | 1052 | -4.25 |

| NOV ’25 | 1041.75 | -3.75 |

| Chicago Wheat | ||

| MAR ’25 | 546.75 | -19.25 |

| JUL ’25 | 576.75 | -17 |

| JUL ’26 | 633.75 | -12.75 |

| K.C. Wheat | ||

| MAR ’25 | 571.25 | -13.75 |

| JUL ’25 | 597.5 | -13.75 |

| JUL ’26 | 642.5 | -11 |

| Mpls Wheat | ||

| MAR ’25 | 587 | -12.5 |

| JUL ’25 | 618.25 | -14 |

| SEP ’25 | 630.75 | -13.75 |

| S&P 500 | ||

| MAR ’25 | 5920.5 | -50.25 |

| Crude Oil | ||

| APR ’25 | 70.34 | 1.72 |

| Gold | ||

| APR ’25 | 2890.4 | -40.2 |

Grain Market Highlights

- Corn: Corn futures closed lower today, driven by weak export sales and the news of impending tariffs from Canada and Mexico, which added further pressure on the market.

- Soybeans: After starting the day higher, soybeans ultimately closed lower, pressured by declines in the corn and wheat markets.

- Wheat: Wheat futures experienced significant losses across all three classes, driven by the rise in the US Dollar Index and reports of tariffs set to begin next week.

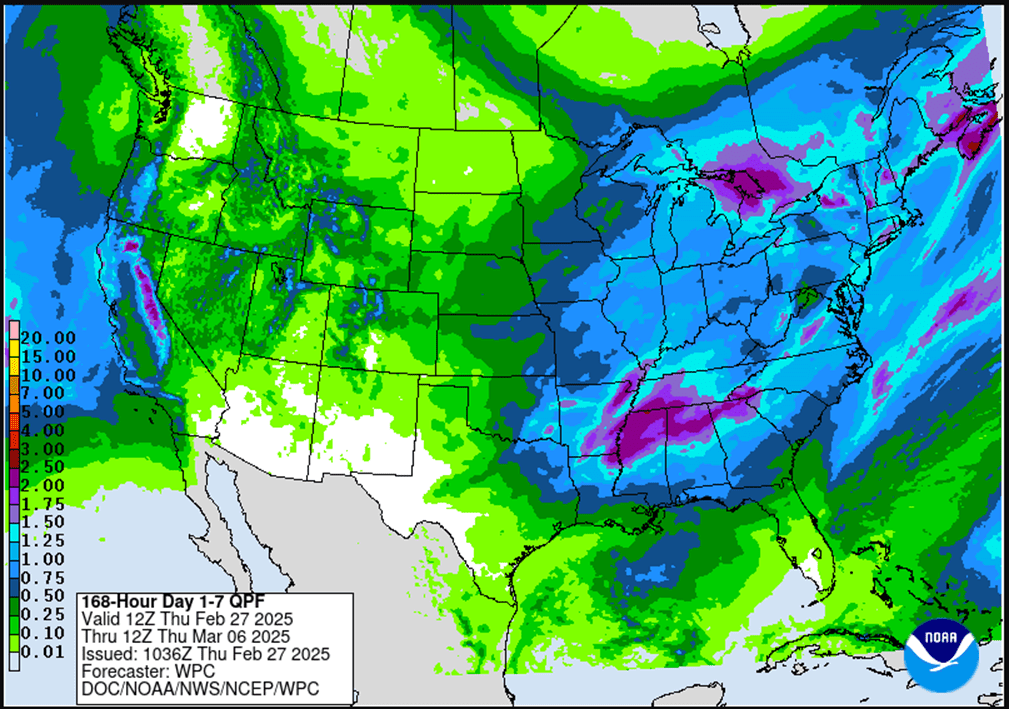

- To see the updated U.S. 7-day precipitation forecast as well as the Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center and NOAA scroll down to the other Charts/Wheat section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Hold Recommendation: Following last week’s two sales recommendations, the advice is to pause making any additional sales for now.

- Top or Correction? – The May contract has seen a notable pullback, closing lower in six of the last seven sessions and now sitting 38 cents below its recent high. While this could be a healthy correction within an ongoing uptrend, the nature of the recent selloff raises some concerns. Is this just a pause, or a sign of a bigger shift? Stay alert for further signals.

2025 Crop:

- Scenario Planning: With the existing sales recommendations and the recent call option recommendation, Grain Market Insider aims to be positioned for any market direction. Given the many unpredictable wild cards that will influence the market in the months ahead — especially weather — it is critical to be prepared for both $7–$8 corn on the upside and $3–$4 corn on the downside.

- Balanced Approach: Last week’s sales recommendations provide a stronger buffer against downside price scenarios, while the active call options strategy reopens upside opportunities on those prior sales recommendations. This balanced approach ensures flexibility in an unpredictable market.

- Potential Put Options: Next week, as we enter March, Grain Market Insider may recommend adding December ’25 put options. These options can be a valuable hedging tool, helping to protect against downside risk on bushels that cannot be forward sold before harvest. If put options are recommended, they will combine with the existing call options to form a strategy known as a Strangle — a common approach when a significant price move is expected, but the direction remains uncertain.

2026 Crop:

- Hold Recommendation: No sales targets are expected to post for the crop to be planted in spring 2026 for at least another week.

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn futures faced strong selling pressure on Thursday due to soft export sales, the USDA Outlook Forum, First Notice Day, and the implementation of tariffs on Canada and Mexico. March corn futures closed at their lowest level since the January WASDE report.

- The USDA outlook for gave baseline projections for corn acreage for the 2025-26 marketing year on Thursday morning. The USDA feels that U.S. producer could plant 94 million acres of corn in the next marketing year. This was up 3.4 million for 2024-25. The increased acres could push early carryout projection toward 2.0 billion for the 2025-26 marketing year.

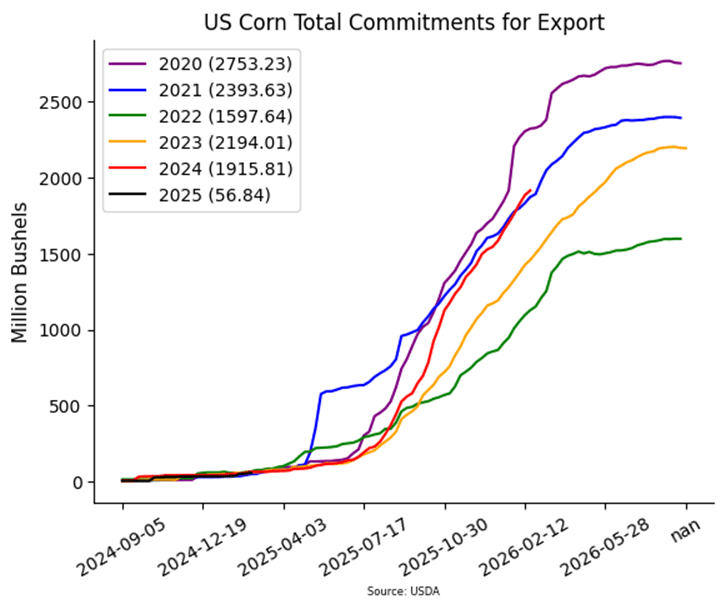

- Weekly corn export sales were disappointing this week. For the week ending February 20, the USDA reported new sales of 795,000 mt, below the low end of analysts’ expectations. The market may be concerned about slowing demand due to higher corn prices and the approaching harvest of South American corn. Total sales are still running 28% ahead of last year’s pace, slightly down from 29% last week.

- President Trump announced that the 25% tariffs on imports from Mexico and Canada, scheduled to take effect on March 4, will proceed as planned. Mexico is the largest buyer of U.S. corn, and the market is concerned about the potential for retaliatory tariffs or a loss of demand. Additionally, President Trump revealed a 10% across-the-board tariff on Chinese goods, also set to be activated on March 4.

- The Buenos Aires grain exchange saw the Argentina corn crop conditions improve last week and rainfall has turned more beneficial. Corn conditions rose to 21% Good/Excellent, up 3% over last week’s total. Weather forecasts remain wet for key growing regions, which should help support the crop.

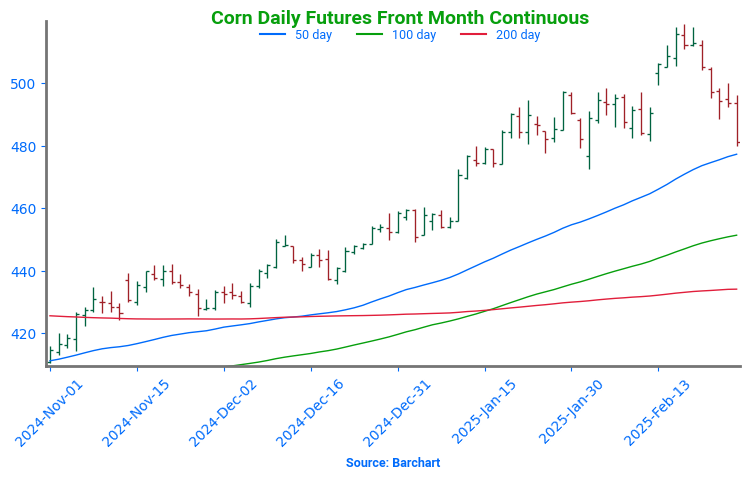

Corn Rally Pauses

The corn market has been performing well in 2025, with steady demand keeping buyers engaged and driving prices to 16-month highs. Last week, technical indicators reached overbought levels, and without new positive developments, prices began to pull back. If this correction continues, support is expected around 475, with stronger support near 450. On the other hand, if buyers step back in, the next target would be 535, with more significant resistance at the spring 2023 lows near 550.

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Hold: With recent sales recommendations in place, the guidance is to pause additional sales for now, as the May contract has closed lower in four of the last five sessions.

- Potential Call Strategy: If May soybeans close above 1079.75, Grain Market Insider may recommend a call option strategy to reown previous sales recommendations…stay tuned.

2025 Crop:

- Sales Target Range: 1090 – 1125 remain the upside target range vs November ‘25.

- Call Option Target: The target to exit all the 1100 Nov ‘25 call options is approximately 88 cents in premium. If the 1100 calls can be exited for that price, it should cover the cost of the 1180 Nov ‘25 calls, providing a net-neutral cost position that can continue to protect the upside on the recent sales recommendation.

2026 Crop:

- No Change: Still no sales recommendations expected until spring.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day lower after starting higher, fading into the close under pressure from corn and wheat, which led the market lower. This morning’s acreage report from the USDA was supportive for soybeans. Both soybean meal and oil also closed lower, with meal posting the larger losses.

- This morning, the USDA Ag Outlook Forum released its estimates for the 2025 planted acres, and for soybeans, they are estimating 84.0 million acres. This would be down from last year’s 87.1 ma as the USDA assumes that acres will be given to corn. This would put ending stocks at 320 million bushels.

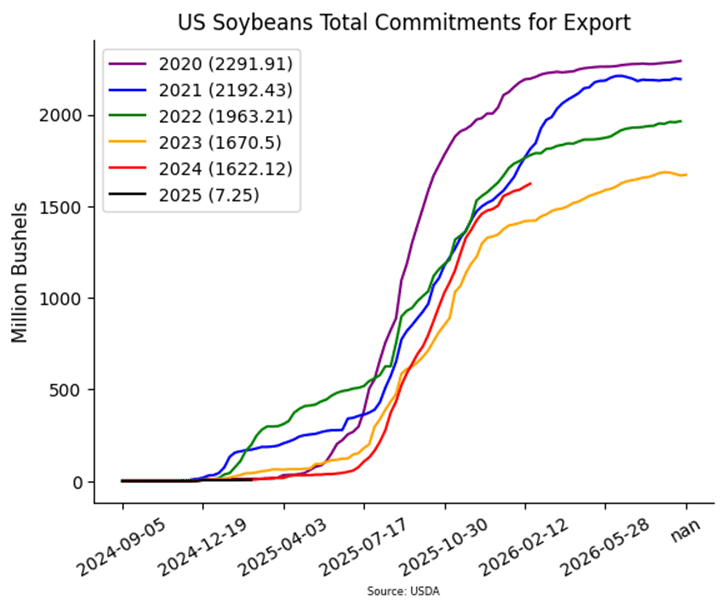

- Today’s export sales report showed another week of disappointing soybean sales. The USDA reported an increase of 15.1 million bushels of export sales for 24/25 and an increase of 0.1 mb for 25/26. Last week’s export shipments of 35.7 mb were above the 17.5 mb needed each week to meet the USDA’s expectations. Primary destinations were to China, Egypt, and Mexico.

- On March 4, it is expected that President Trump will enact 25% tariffs on Mexico and Canada after pushing the tariffs off 30 days ago. While it is possible that further negotiations could delay these tariffs again, the market will likely be volatile until it is confirmed.

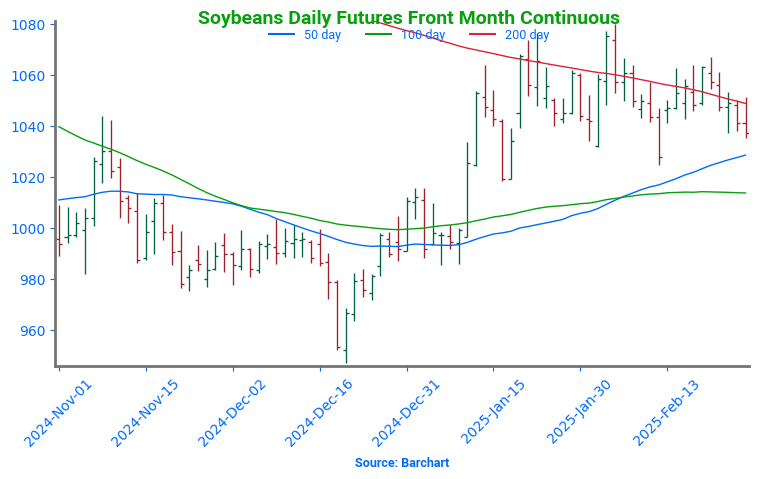

Soybeans Continue Sideways Grind

Front-month soybean futures continue to flirt with the 200-day moving average, a formidable resistance that has capped gains for over 18 months. A decisive move past this level could trigger bullish momentum, paving the way for a rise toward the key 1100 mark. Should prices dip, reliable support is expected near 1030, with a more stable floor around 1000.

Wheat

Market Notes: Wheat

- Wheat futures took a hit today, posting sharp losses across all three classes. Traders’ focus was on the USDA’s remarks, but a sharp rise in the US Dollar Index, a lower close for Paris milling wheat, and declines in corn and soybeans all weighed negatively on the wheat market. Additionally, reports indicate that tariffs on Mexico and Canada will begin next week, adding further pressure to the grain markets.

- At the USDA Outlook Forum today, 2025 wheat acreage was estimated at 47 million, an increase of 0.9 million from last year. Additionally, the trendline yield of 50.1 bpa would result in a production estimate of 1.926 bb and ending stocks of 826 mb. While these numbers were largely in line with expectations, the absence of supportive news contributed to the negative price action today.

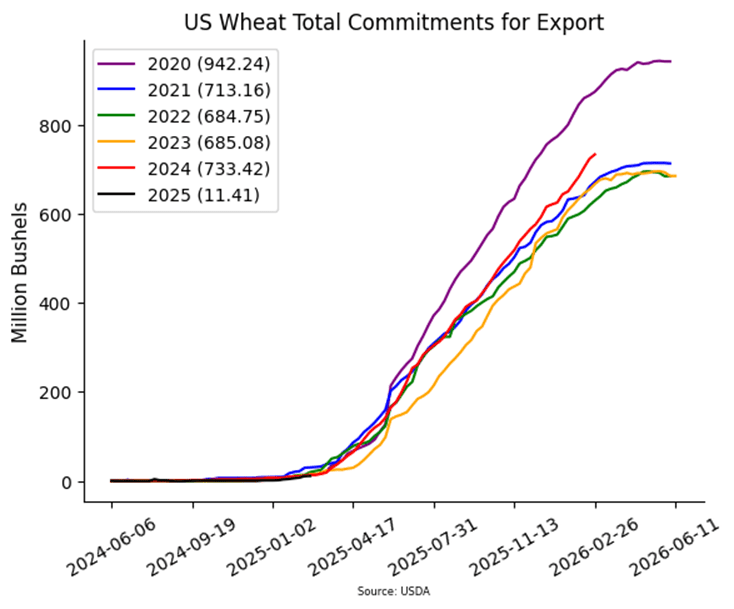

- The USDA reported an increase of 9.9 mb of wheat export sales for 24/25 and an increase of 0.2 mb for 25/26. Shipments last week at 13.9 mb fell under the 20.2 mb pace needed per week to reach the export goal of 850 mb. Sales commitments at 733 mb for 24/25 are up 10% from last year, which is behind the USDA estimated pace.

- IKAR has reduced their estimate of Russian wheat exports for 24/25 by 0.5 mmt to 42.5 mmt. Additionally, their range of production estimates declined. In a normal scenario, they project wheat production to decline from 82 to 81 mmt. Under optimal conditions, their estimate has been reduced from 87 to 85 mmt. In a negative scenario, their forecast remains unchanged at 77 mmt.

- On a bullish note, above-average temperatures are forecasted for India in March, which could potentially reduce wheat yields as the crop matures. After three consecutive years of poor yields, India may need to import wheat if the 2025 harvest is not abundant.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Hold: The May contract has now closed lower in six of the last seven sessions and is down about 60 cents from its recent high already. Current guidance is to hold off on making additional old crop sales for now.

- Maintain Call Options: Continue to hold onto the July ‘25 860 and 1020 call options.

2025 Crop:

- No current targets: The severity of the recent pullback has clouded the trend, making the next move uncertain. Grain Market Insider will hold off on setting new targets until there’s a clearer indication of potential direction. Stay tuned for further updates.

- Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

- No Change: The next target range for a sale on the 2026 crop remains 700–720 vs July ‘26.

To date, Grain Market Insider has issued the following Chicago Wheat recommendations:

Chicago Wheat Surges Past Resistance

Chicago wheat broke out of its prolonged sideways trend with a strong February rally, reaching key resistance at the early October highs just above 615. A decisive weekly close above the 200-day moving average now positions it as a potential support level on any near-term pullbacks. The next upside targets are near 650, with stronger resistance in the 680-700 range.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Hold: The May contract has closed lower in six of the last seven sessions and is down about 57 cents from its recent high. Current guidance is to hold off on making additional old crop sales for now.

- Maintain Call Options: Continue to hold onto the July ‘25 860 and 1020 call options.

2025 Crop:

- No current targets: The severity of the recent pullback has clouded the trend, making the next move uncertain. Grain Market Insider will hold off on setting new targets until there’s a clearer indication of potential direction. Stay tuned for further updates.

- Maintain Put Options: Continue holding the final quarter of July ’25 620 put options.

2026 Crop:

- Hold: No first sales targets or recommendations are expected until the late May, early June window.

To date, Grain Market Insider has issued the following KC recommendations:

KC Wheat Signals Breakout Potential

Kansas City wheat futures surged into February with strong bullish momentum, closing above the 200-day moving average and testing multi-month highs near 620. A breakout above the October peak of 623 could fuel a rally toward the key 700 level. On the downside, the 200-day moving average provides initial support, with stronger backing around 575.

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

2024 Crop:

- Hold: The May contract has closed lower for seven consecutive sessions and is down about 55 cents from its recent high. Current guidance is to hold off on making additional old crop sales for now.

- Maintain Call Options: Continue to hold onto the July ‘25 KC 860 and 1020 call options.

2025 Crop:

- No current targets: The severity of the recent pullback has clouded the trend, making the next move uncertain. Grain Market Insider will hold off on setting new targets until there’s a clearer indication of potential direction. Stay tuned for further updates.

- Maintain Put Options: Continue to hold the last quarter of July ‘25 KC 620 put options.

2026 Crop:

- No Change: No first sales recommendations are expected until early summer.

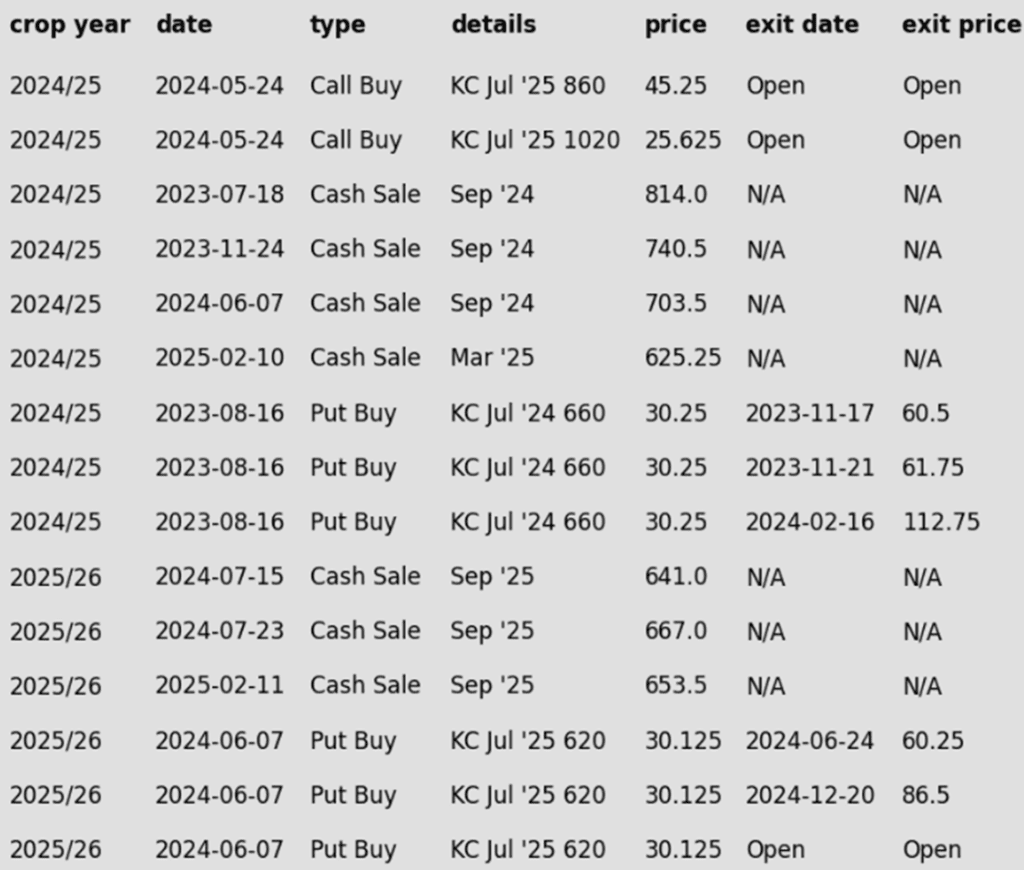

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

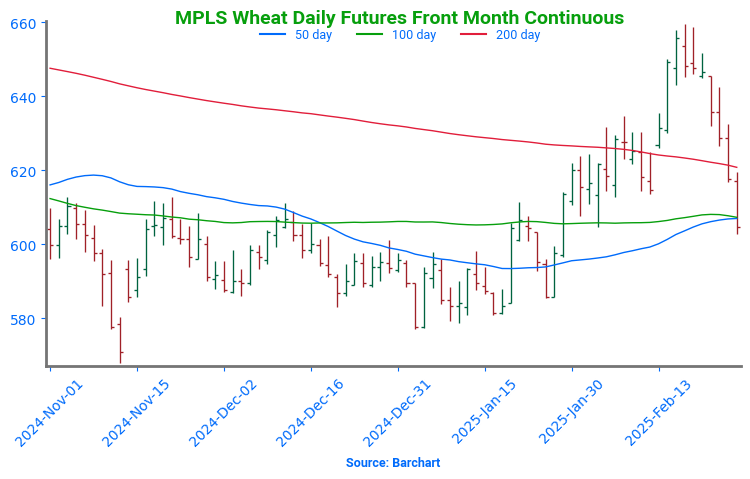

Spring Wheat Confirms Breakout

Spring wheat broke free from its prolonged sideways range in late January, signaling bullish momentum. A mid-February close above the 200-day moving average reinforces the breakout, with initial support at the 200-day MA and stronger backing near 615 — the top of the previous range. On the upside, 650 is the next key resistance before bulls target the elusive 700 level.

Other Charts / Weather

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

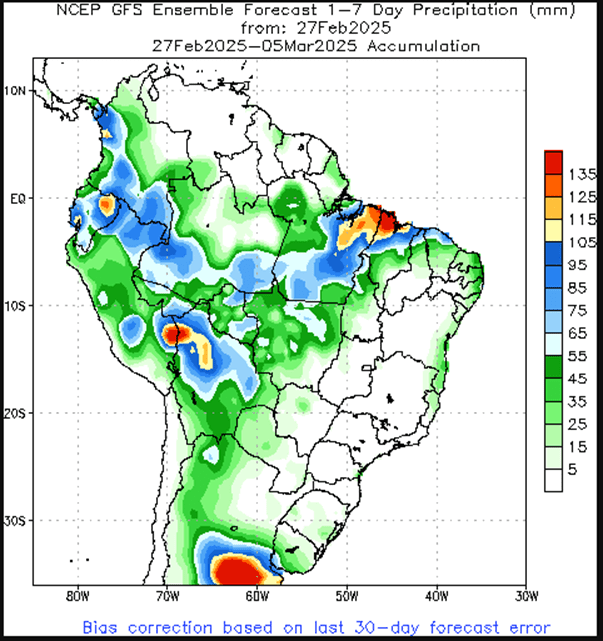

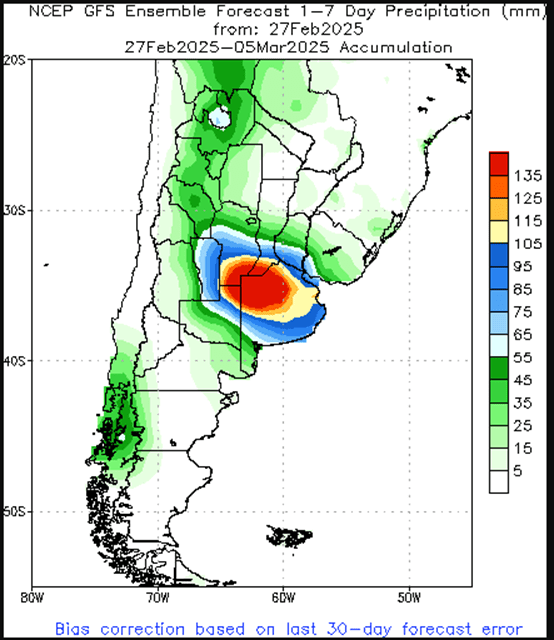

Above: Brazil and Argentina one-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.