2-12 End of Day: Strong Weekly Export Inspections Lead Soybeans Higher

All prices as of 2:00 pm Central Time

| Corn | ||

| MAR ’24 | 430.5 | 1.5 |

| JUL ’24 | 452.25 | 1.5 |

| DEC ’24 | 469.25 | 1 |

| Soybeans | ||

| MAR ’24 | 1193 | 9.5 |

| JUL ’24 | 1207.5 | 7.75 |

| NOV ’24 | 1168.75 | 5 |

| Chicago Wheat | ||

| MAR ’24 | 597.5 | 0.75 |

| JUL ’24 | 600.25 | -0.75 |

| JUL ’25 | 634.75 | -0.5 |

| K.C. Wheat | ||

| MAR ’24 | 598.75 | -2.75 |

| JUL ’24 | 589 | -4.75 |

| JUL ’25 | 632.5 | 0 |

| Mpls Wheat | ||

| MAR ’24 | 682.5 | -1.75 |

| JUL ’24 | 684.75 | -1.25 |

| SEP ’24 | 688.75 | -1.5 |

| S&P 500 | ||

| MAR ’24 | 5042.5 | -1.5 |

| Crude Oil | ||

| APR ’24 | 76.8 | 0.03 |

| Gold | ||

| APR ’24 | 2032.6 | -6.1 |

Grain Market Highlights

- With both China and Brazil on holiday for the week, the corn market was dominated by quiet back-and-forth trade in a 5-cent range that garnered support from neighboring soybeans. Although weekly export inspections came in at the upper end of expectations, and remain 31% above last year, they fell short of the pace needed to reach the USDA’s forecast.

- Strong weekly export inspections helped to rally soybeans with some possible short covering. Export inspections came in at the top end of expectations and well ahead of the pace needed to reach the USDA’s goal, though they remain 23% behind last year’s total for the same period.

- Soybean meal followed through from Friday’s reversal with some likely short covering adding support. Soybean oil also followed through from Friday’s price action, but to the downside as lower heating oil futures (a proxy for diesel fuel) and profit taking from last week’s rally weighed on prices.

- The wheat complex settled mostly lower with Chicago fractionally mixed, whereas KC and Minneapolis posted small losses. Bull spreading was noted in all three classes as funds continued to roll short positions out of the leading March contract to the deferred. Lower Russian export prices continue to add resistance to the US market.

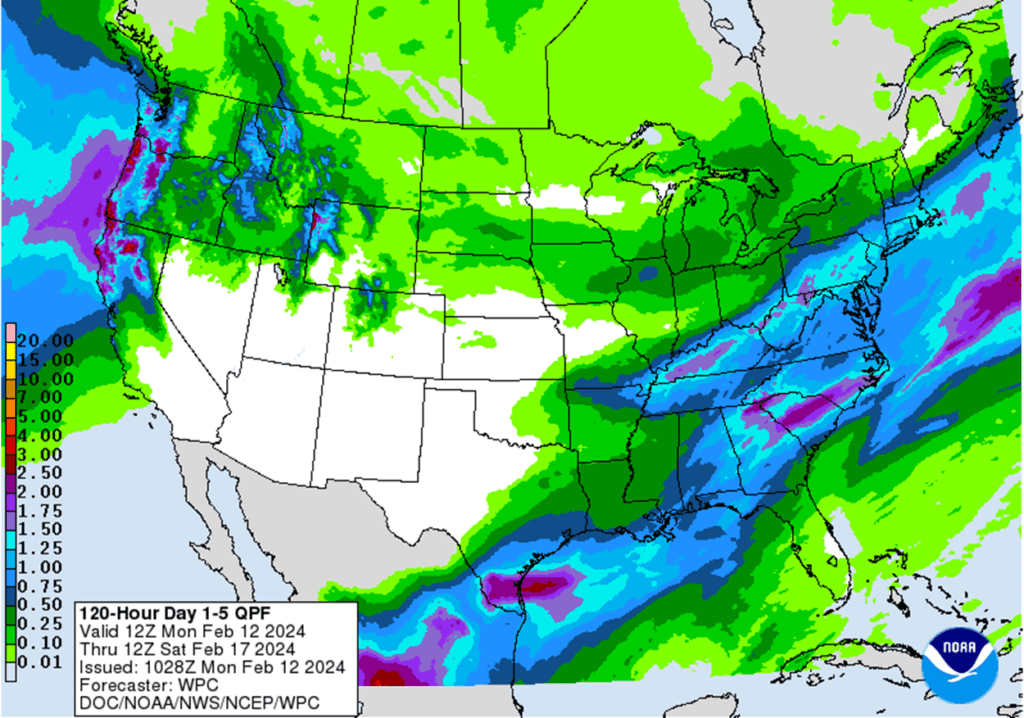

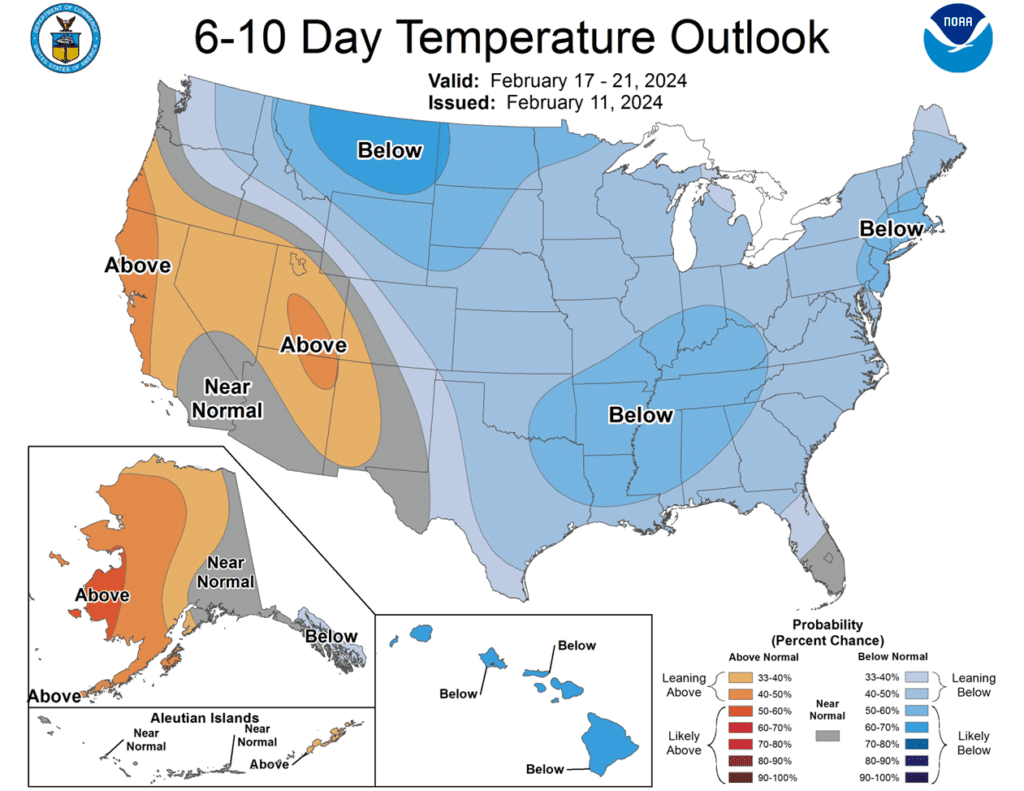

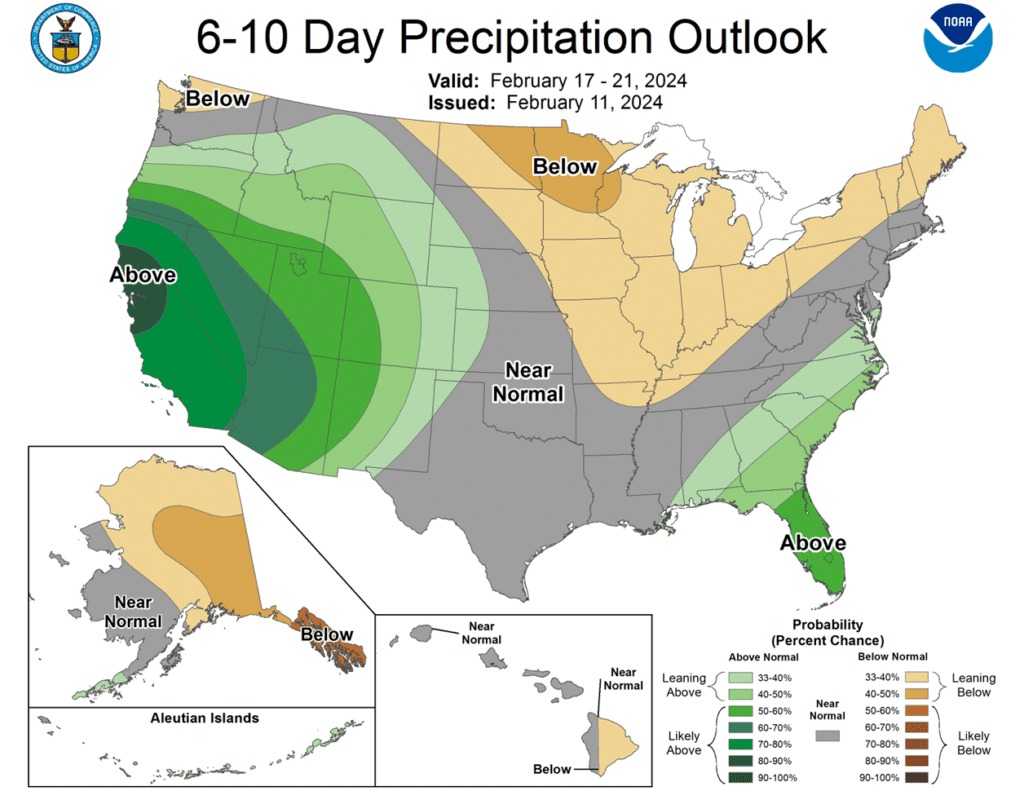

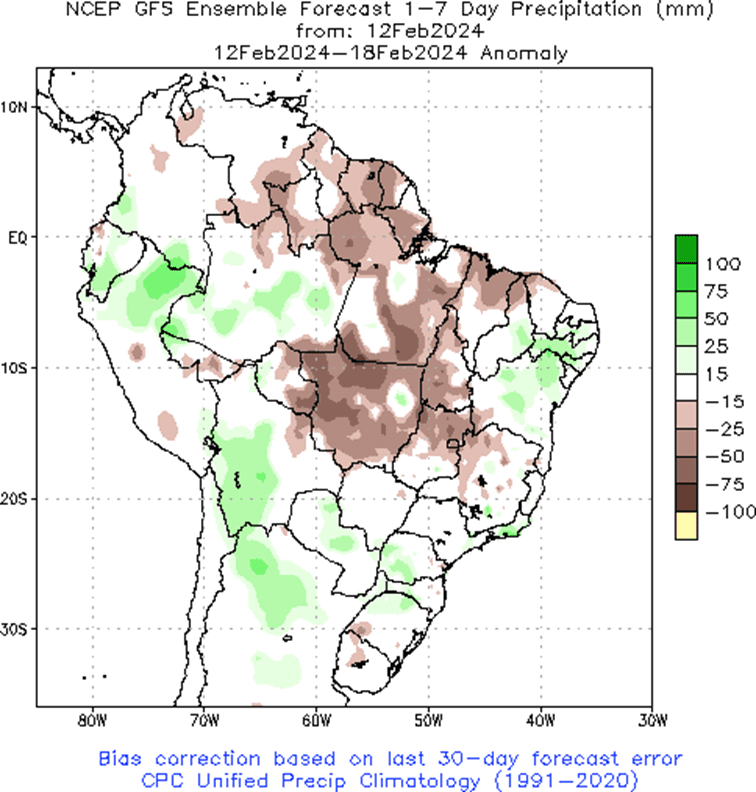

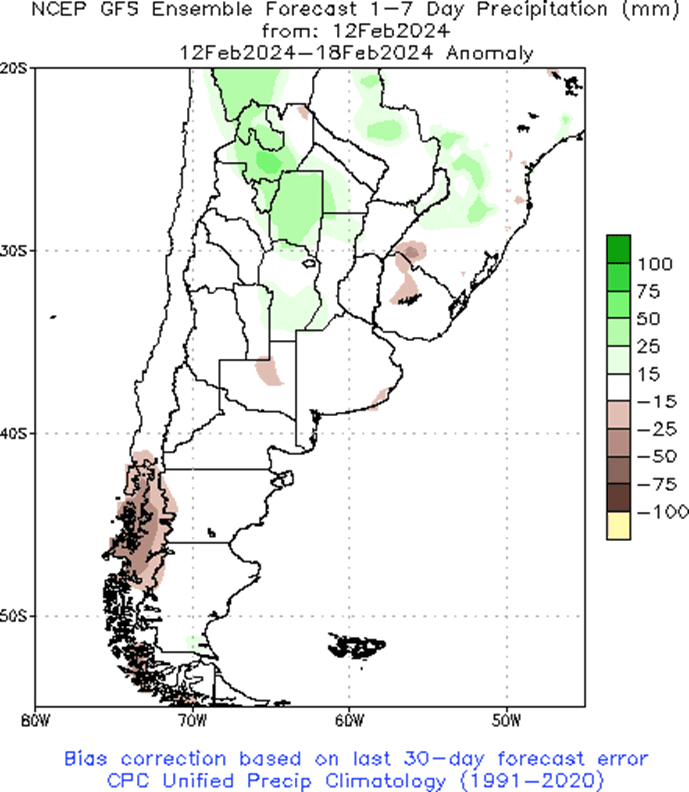

- To see the updated US 5-day total precipitation forecast, 6 – 10 day temperature and precipitation outlooks, and the 1-week South American forecast precipitation anomaly, courtesy of the National Weather Service and the Climate Prediction Center, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

- No new action is recommended for 2023 corn. With a general lack of bullish news and an estimated US carryout over 2.1 billion bushels, front month corn has languished in a sideways to lower trend since printing a high last October. While the lack of a bullish catalyst has been disappointing, the market is in a significantly oversold condition, and managed funds continue to hold a sizable net short position. Either or both could trigger a short covering rally at any time heading into the spring planting window. For now, Grain Market Insider continues to sit tight on any further sales recommendations for the next few weeks with the objective of seeking out better pricing opportunities. If the market has not turned around by then, Grain Market Insider may sit tight on the next sales recommendations until spring or even summer.

- No new action is recommended for 2024 corn. In January, Dec ’24 broke through the bottom end of the 485 ¾ to 602 range that had been in place since February ’22. While this was a disappointing development, bear spreading has allowed Dec ’24 to maintain more of its value versus old crop as traders attempt to price in a larger 2023 carryout with more uncertainty ahead for the 2024 crop. Additionally, Dec ’24 is significantly oversold on the weekly chart, which is supportive for a technical rally to begin at any time as the spring planting window quickly approaches. Given the amount of time and uncertainty that remains for the 2024 crop, Grain Market Insider will consider recommending additional sales on a retracement toward the low to mid 500 level.

- No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next year. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

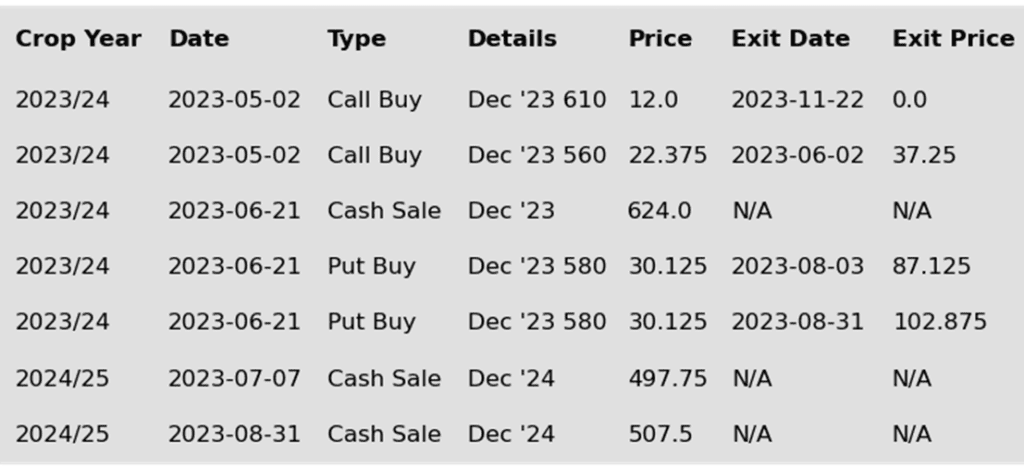

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

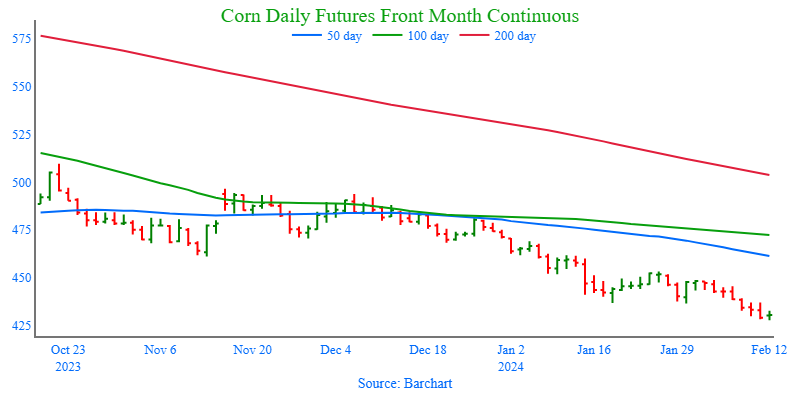

- Quiet day in the corn market, but futures found some footing for the first time in a week. March corn gained 1 ½ cents on the session as overall news was lacking in the corn market.

- Weekly export inspections were within estimates at 34.6 mb (880,00 mt). Total inspections for 23/24 are now at 677 mb, which is up 31% from last year. The corn market is starting to hit a window where the inspection numbers should and need to increase weekly.

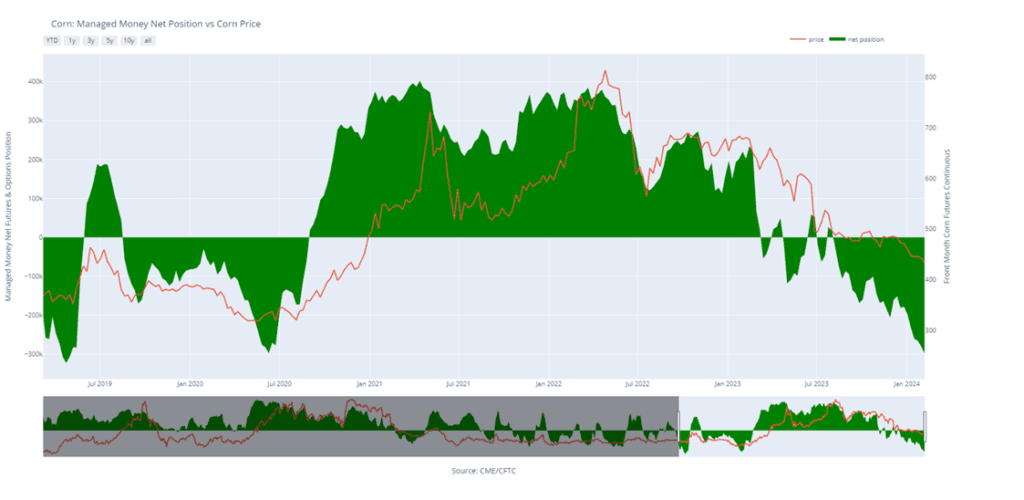

- Managed funds are still pushing the short side of the market. On last week’s Commitment of Traders report, managed funds added 17,593 net short positions to increase their net short position to 297,744 total contracts.

- Rainfall in Argentina over the weekend has stabilized the crops in many areas. The forecast is staying supportive grain development as adequate moisture stays in the forecast.

Above: The breach of the previous low of 436 puts front month corn at risk of drifting lower without any new bullish input. For now, the next major level of support lies near 415. Should a bullish catalyst enter the scene to move prices higher, overhead resistance may be found between 450 and 460.

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

- No new action is recommended for 2023 soybeans. In early January, front month soybeans broke through the bottom side of the 1290 – 1400 range that had been in place since mid-October. As South American weather forecasts improved, the potential for a reduction in the record large global carryout also lessened, bringing prices down toward the 1180 support level. For now, 1180 support appears to be holding, and though the weak price action has been disappointing, time remains in the South American growing season, and the old crop marketing year, for unforeseen changes to push prices back higher. Given the potential of a downside breakout back in December, Grain Market Insider recommended adding to sales as prices remained historically good, and Grain Market Insider will continue to look at additional sales opportunities heading into spring.

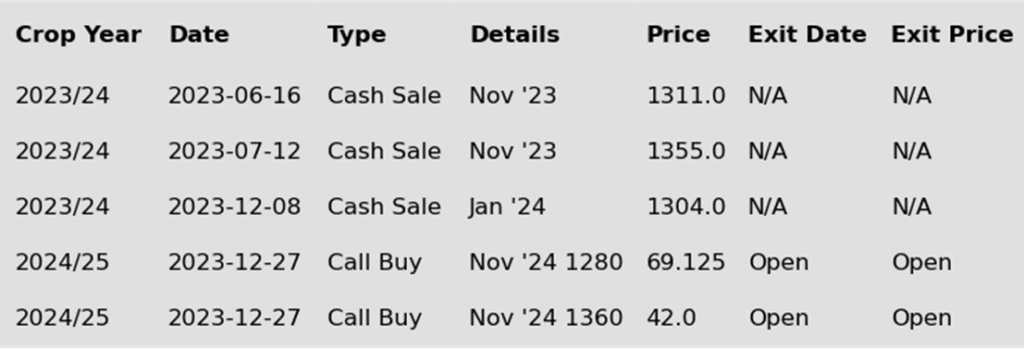

- No new action is recommended for the 2024 crop. After the Nov ’24 contract broke through the bottom side of the 1233 – 1320 range, prices continued to retreat as South American weather conditions improved. Even though Nov ’24 runs similar downside risks as the front month contracts, which could press new crop prices toward 1150 or possibly the May ’23 low near 1115, plenty of time remains to market this crop. Considering the amount of uncertainty that lies ahead with the 2024 soybean crop, Grain Market Insider recommended back in December buying Nov ’24 1280 and 1360 calls to give you confidence to make sales against anticipated production, and to protect any sales in an extended rally. Additionally, the possibility remains that prices could retest the 2022 highs, at which point Grain Market Insider may consider recommending additional sales.

- No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day higher to start the week after a poor showing last week with the WASDE report pressuring prices. Soybean meal ended the day higher, while soybean oil was lower with some possible pressure from lower heating oil.

- This morning, the USDA reported total soybean export inspections at 48.7 mb for the week ending Thursday, February 8. This was near the higher end of the estimated trade range which likely added support today. Total inspections are now at 1,131 mb for 23/24 which is down 23% from the previous year.

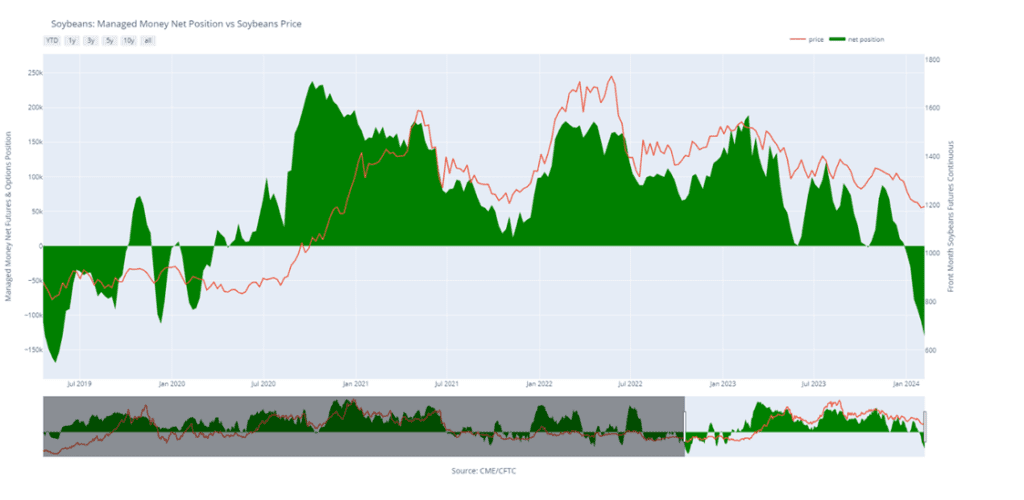

- Funds hold a large net short position in soybeans and sold an additional 22,053 contracts as of February 6, leaving them with a net short position of 130,300 contracts. With the market oversold and funds so short, some short covering may have taken place today.

- Over the weekend, Argentina benefited from much needed rain in some of the drier areas, while Brazil received scattered showers as well. Private analysts are still expecting Brazilian soy production to be lower than USDA estimates with many projecting total production around 149 mmt.

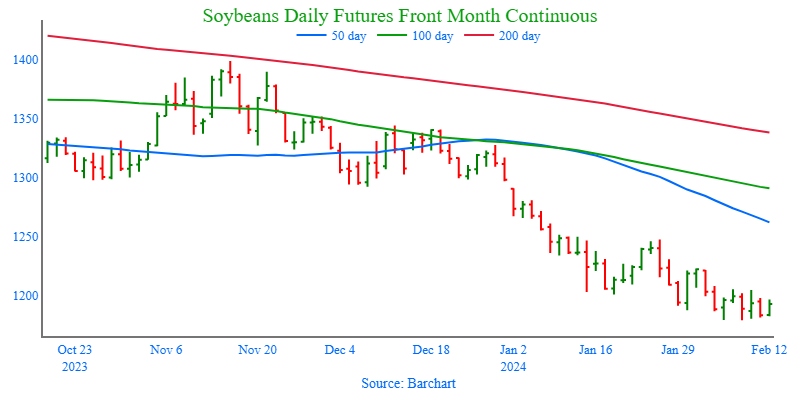

Above: Front month soybeans appear to be consolidating just above 1180 support and continue to show signs of being very oversold on the weekly charts. If this support level holds, the market’s oversold status should be supportive with some bullish input. Right now, overhead resistance comes in between 1205 and 1210, with additional resistance around 1225. Support below the 1180 area remains between 1140 and 1145.

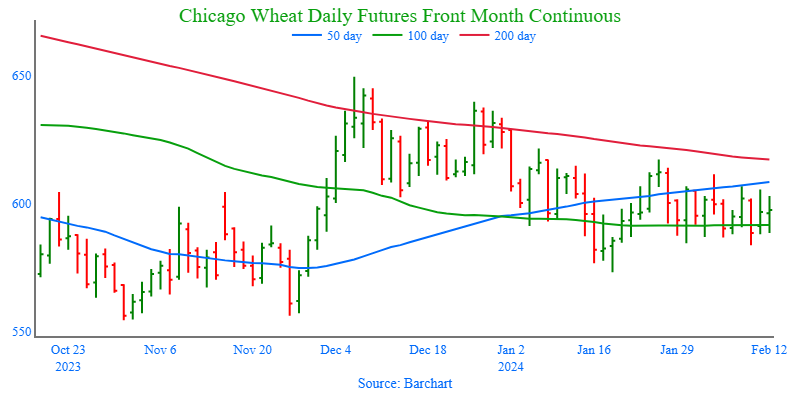

Wheat

Market Notes: Wheat

- US wheat closed mostly lower in all three classes today, with the exception being March and May Chicago wheat. The former gained less than a penny, while the latter was neutral. Paris milling wheat also closed lower for the session, offering some weakness to the US market. Competitive Russian exports continue to act as the main anchor; their FOB values are said to be around $235 per mt, which is up from last week, but well below the $250 area at the end of December.

- Weekly wheat inspections at 15 mb bring total 23/24 inspections to 430 mb. That is down 18% from last year and current inspections are behind the USDA’s projected pace. On last week’s WASDE report, they left their estimate of 23/24 wheat exports unchanged at 725 mb.

- Ukraine’s Ag Minister said that their winter wheat acres are down compared to last year, which along with the grain quality and economic issues they are facing may lower production. However, their spring wheat acreage may be higher and potentially reduce that concern.

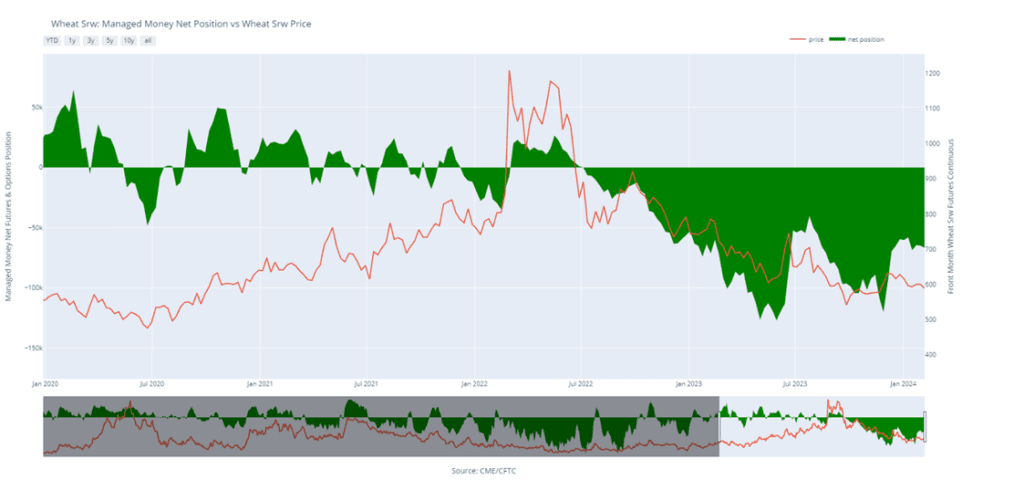

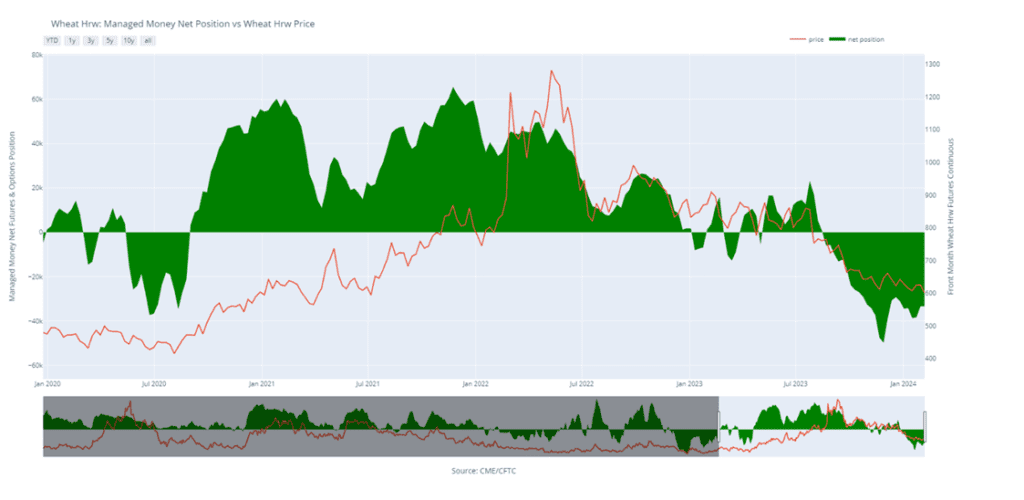

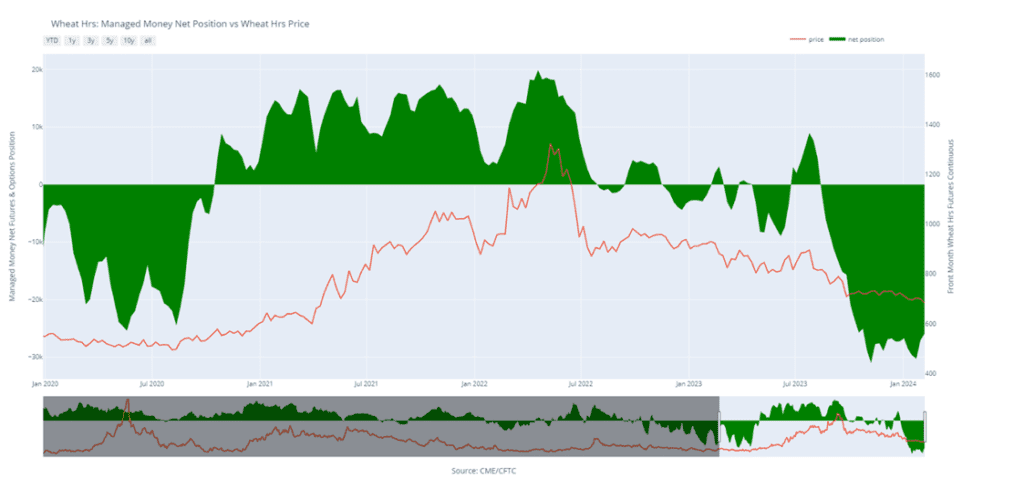

- According to the CFTC, as of February 6, the fund short position in Chicago wheat increased by about 3% from the previous data on January 30. The net short went from 64,818 to 66,738 contracts. The net short Kansas City wheat position was virtually unchanged for the same time period at around 33,000 contracts. While over in the Minneapolis wheat, funds covered 1,174 contracts, almost 5%, of their net short positions to bring their net short position to 25,906 contracts.

- Later this week the USDA will hold their annual Ag Outlook Forum. While the numbers they will give are by no means official estimates, the trade will likely react to them anyways. Last year the forum’s estimate of wheat acreage was 49.5 million, which was in line with the actual 49.6 ma planted.

Action Plan: Chicago Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Chicago Wheat Action Plan Summary

- No new action is currently recommended for 2023 Chicago wheat. The wheat market has continued to be dominated by lower world export prices that have stymied US export sales and depressed US prices. In early December, Grain Market Insider recommended taking advantage and making a sale on a short covering rally which was sparked by several Chinese purchases of US wheat. Since then, China has been silent in the US wheat export market, and prices remain somewhat elevated. Any remaining 2023 soft red winter wheat should be getting priced into market strength with the goal of having zero bushels unpriced by the end of January. Grain Market Insider won’t have any “New Alerts” for 2023 Chicago wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Chicago wheat. Since early December, the July ’24 contract has traded mostly sideways to slightly lower after its brief short covering runup on Chinese buying. Although China has since been absent from the US wheat export market, prices appear to have found support above 585, and managed funds continue to hold a sizeable, short position that could trigger another short covering rally if a bullish impetus enters the market. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for further price erosion. Although, if the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset much of the original cost and move toward a net neutral cost for the remaining position.

- No action is currently recommended for 2025 Chicago Wheat. Since early September, the July ’25 contract has been mostly rangebound with 632 at the low end and 685 at the top. Grain Market Insider’s strategy for the 2025 crop year up to this point has been to sit tight. Though if prices rally toward the upper end of this range, we will consider taking advantage of the rally’s historically good prices to make sales recommendations.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: Chicago wheat has been in a congestion pattern bordered between 614-618 on the top and 584 on the bottom. A breakout through the top end could send prices toward the 640 – 650 resistance area, while a downside breakout may find initial support around 573 with more support around 556.

Action Plan: KC Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

KC Wheat Action Plan Summary

- No new action is recommended for 2023 KC wheat crop. Since last fall, front month KC wheat has been mostly rangebound between 678 up top and the 590 area down below. The latter has held as support for the past three months. Although fundamentals remain weak, considering support lies just below the market and managed funds continue to carry a sizable short position, these factors could trigger a return to higher prices if any unforeseen risks enter the market. Grain Market Insider’s strategy is to look for price appreciation as weather becomes a more prominent market mover and may consider suggesting additional sales if prices make a modest 20% retracement of the 2022 highs back toward 730.

- No new action is recommended for 2024 KC wheat. At the end of August, the July ’24 contract broke out of roughly a one-year trading range and stepped down to a 609 ¼ low in late November, largely driven by managed fund selling in the front month on weak US export demand and lower world wheat prices. Since then, the funds covered part of their large short position which also rallied prices in the July ’24 contract. While bearish headwinds remain, managed funds continue to hold a sizable, short position, and price seasonals remain positive for adding weather risk premium. These are two factors that could fuel additional short covering and rally prices in the months ahead. Back in August, Grain Market Insider recommended buying Jul’24 KC wheat 660 puts to protect the downside following the range breakout. As the market recently got further extended into oversold territory and the July contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. Moving forward, Grain Market Insider is prepared to recommend exiting the last 25% on any further supportive market developments.

- No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

Above: Front month Minneapolis wheat broke through nearby downside support of 688 and may continue to drift lower to test the January low of 678 ¾. If the 678 ¾ area fails, the next major support level may come in around 669. Overhead, resistance remains between 710 and 720.

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

- No new action is currently recommended for the 2023 New Crop. For the last six months, front month Minneapolis wheat has slowly stair-stepped lower with little bullish news to move markets higher. During this time, the 50-day moving average has acted as resistance, above which the market has not been able to hold for very long. Managed funds have also established and maintained a record (or near record) short position for much of the same time. Although bullish headwinds remain, support may be building in the 670 – 675 area, and the large fund net short position continues to leave the market susceptible to a short-covering rally at any time here. Grain Market Insider’s strategy is to look for a modest retracement of the July high and consider additional sales around 725 – 750.

- No new action is recommended for 2024 Minneapolis wheat. Much like the front month contracts, Sept ’24 has been in a downward trend since last summer. And just as Sept ’24 has been influenced to the downside by the front months, it could be similarly influenced to the upside by the front months if a bullish impetus enters the scene and triggers a short covering rally due to the fund’s large short position. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside following a 1-year range breakout in KC wheat, and in November recommended exiting 75% of the originally recommended position as July ’24 KC wheat showed signs of support around 630. While in the same time frame, Grain Market Insider also recommended making an additional sale as the Sept ’24 Minneapolis contract broke long time 743 support. Grain Market Insider remains prepared to recommend exiting the last 25% of the open puts on any further supportive market developments and consider recommending additional sales if prices make a modest retracement of the 2022 highs.

- No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next year. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: Front month Minneapolis wheat continues to consolidate with overhead resistance remaining between 710 and 720, and nearby support just under the market at 688. If prices break through nearby support, they may fade and test the January low of 678 ¾. Support below there may come in around 669.

Other Charts / Weather