12-4 End of Day: Wheat Reverses to Close Mixed, with Corn and Soybeans Lower

All prices as of 2:00 pm Central Time

| Corn | ||

| MAR ’25 | 430 | -2.25 |

| JUL ’25 | 438.25 | -2.5 |

| DEC ’25 | 429 | -1.75 |

| Soybeans | ||

| JAN ’25 | 983.75 | -8 |

| MAR ’25 | 989.75 | -7.5 |

| NOV ’25 | 1000.75 | -5.5 |

| Chicago Wheat | ||

| MAR ’25 | 548.25 | 0.75 |

| MAY ’25 | 557 | 0.5 |

| JUL ’25 | 562.75 | 0.75 |

| K.C. Wheat | ||

| MAR ’25 | 542.5 | 0.75 |

| MAY ’25 | 550 | 0.5 |

| JUL ’25 | 557.75 | 1 |

| Mpls Wheat | ||

| MAR ’25 | 589.5 | -0.5 |

| JUL ’25 | 605.75 | -0.75 |

| SEP ’25 | 614.75 | -1 |

| S&P 500 | ||

| MAR ’25 | 6162.25 | 31 |

| Crude Oil | ||

| FEB ’25 | 68.22 | -1.32 |

| Gold | ||

| FEB ’25 | 2676.6 | 8.7 |

Grain Market Highlights

- Weekly ethanol production exceeded USDA projections but fell short of expectations, leaving the corn market under pressure. March futures settled near session lows, as they consolidate around 430.

- Soybeans closed lower on the day but off session lows, supported by a higher close in meal, which reversed mid-session on potential short covering and a drier pattern ahead for Argentina.

- Soybean oil traded lower again, pressuring soybeans, as it tracked weaker Malaysian palm oil and faced additional pressure from the likely delay in 45Z biofuel tax credit guidance.

- The wheat complex rebounded off support near March contract lows across all three wheat classes, aided by rumors of quality concerns over Australia’s wheat crop due to excessive rain.

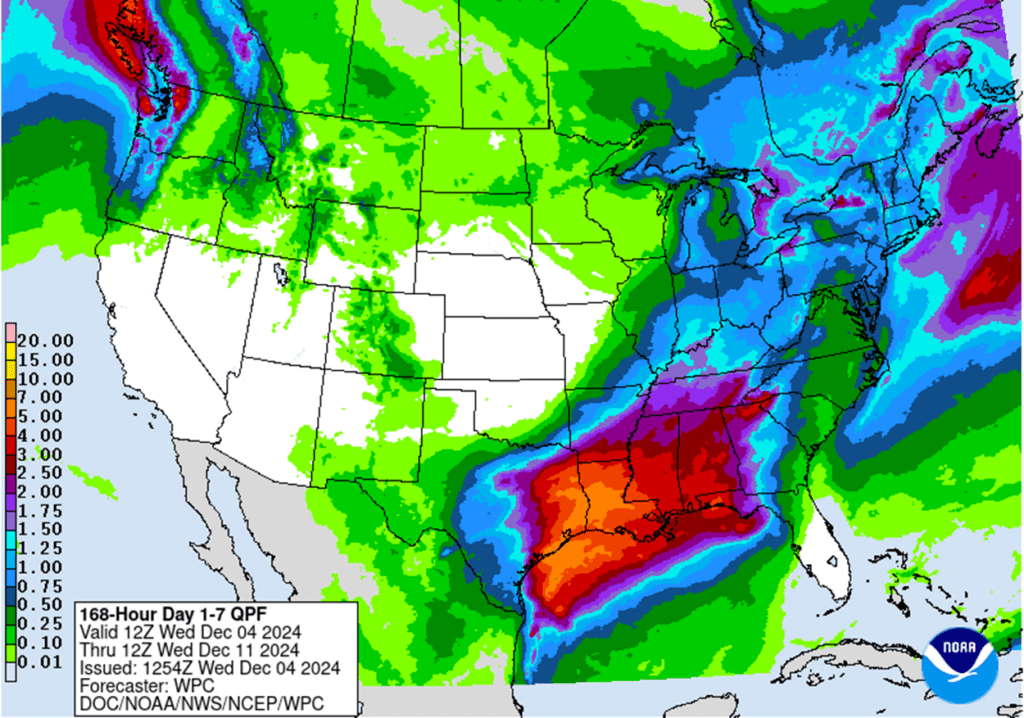

- To see the updated US precipitation forecast and South American 7-day total precipitation, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Corn Action Plan Summary

2024 Crop:

- If you missed our previous sales recommendations, consider targeting the 460 area in March ‘25 for any catch-up sales. Additionally, selling additional bushels into market strength may be beneficial if you have capital needs.

- We are now in the window when seasonal opportunities tend to improve and we anticipate posting target ranges for new sales soon, but they could be as late as early spring.

2025 Crop:

- If you missed previous sales recommendations for next year’s crop, consider targeting 455 – 475 versus Dec’25 to take advantage of any post-harvest strength.

- As we enter the time of year when seasonal opportunities tend to improve, we will begin posting target ranges for additional sales, though this may not happen until late winter or early spring.

- Be on the lookout for a recommendation to buy call options in the 470–490 range versus Dec’25 to protect current sales against a potential extended rally.

2026 Crop:

- Patience is advised. No sales recommendations are planned currently, as we continue to monitor the market for more favorable conditions.

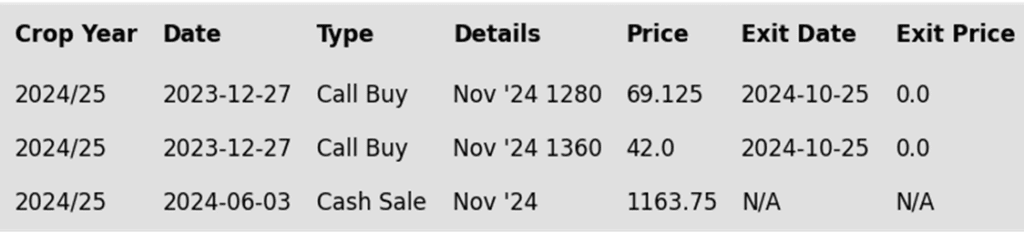

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Overall, the negative tone of the commodity space weighed on corn futures, as corn prices consolidate around the 430 area on the most active March contract.

- Ethanol production fell to 1.073 mbd (315 million gallons/day) last week, down from the previous week’s record of 329 million gallons but still above USDA targets. About 108.4 mb of corn was used for production.

- Uncertainty over clean fuel tax credit guidance (45Z policy) persists, with mixed reports on whether it will be in place before President Biden’s term ends. Traders are likely taking a wait and see approach to this potential policy.

- USDA corn export sales, due Thursday, are expected to range from 750,000–1.5 mmt for last week, following the previous week’s total of 1.062 mmt.

- Brazilian producers are ahead on 2025 Safrinha corn inputs, with 70% secured, driven by favorable exchange rates. Increased second-crop planting remains possible with current weather conditions.

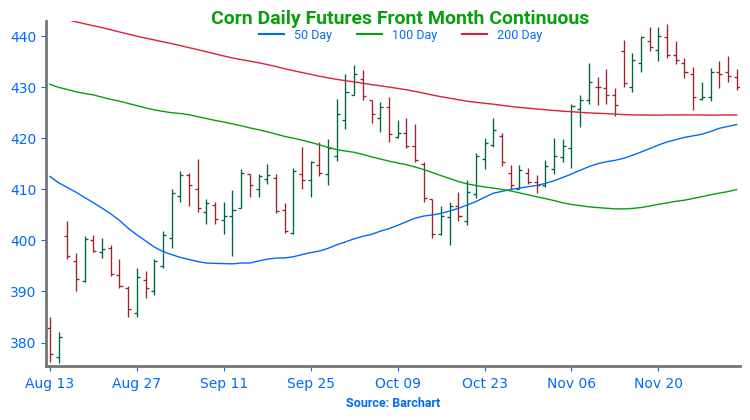

The corn market has, so far, held support near the 425 area and the 200-day moving average (ma), and could potentially retest the 442 area with the possibility of trading towards 465. If prices break through and close below the 50-day moving average (ma), near 422, they run the risk falling further and testing more major support near the 410 area and 100-day ma.

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Soybeans Action Plan Summary

2024 Crop:

- If you missed prior sales recommendations, a rally back to the 1050 – 1070 area versus Jan’25 could provide a good opportunity to make catch-up sales. For those with capital needs, consider making these sales into price strength.

- Additional sales could also be considered in the 1090 – 1125 range versus Jan’25 if prices rally beyond the 1070 area.

- This is the period when seasonal opportunities typically improve, and we plan to post target ranges for new sales soon, though it could be as late as early spring.

2025 Crop:

- We are in the window when targets for additional sales on next year’s crop will start being posted. Though patience is still recommended since they could be set as late as early spring.

- Be on the lookout for a recommendation to buy call options. A rally to the upper 1100 range versus Nov’25 could increase the likelihood of an extended rally, and we would recommend buying calls to prepare for that possibility.

2026 Crop:

- Patience is advised. No sales recommendations are currently planned as we monitor the market for more favorable conditions and timing.

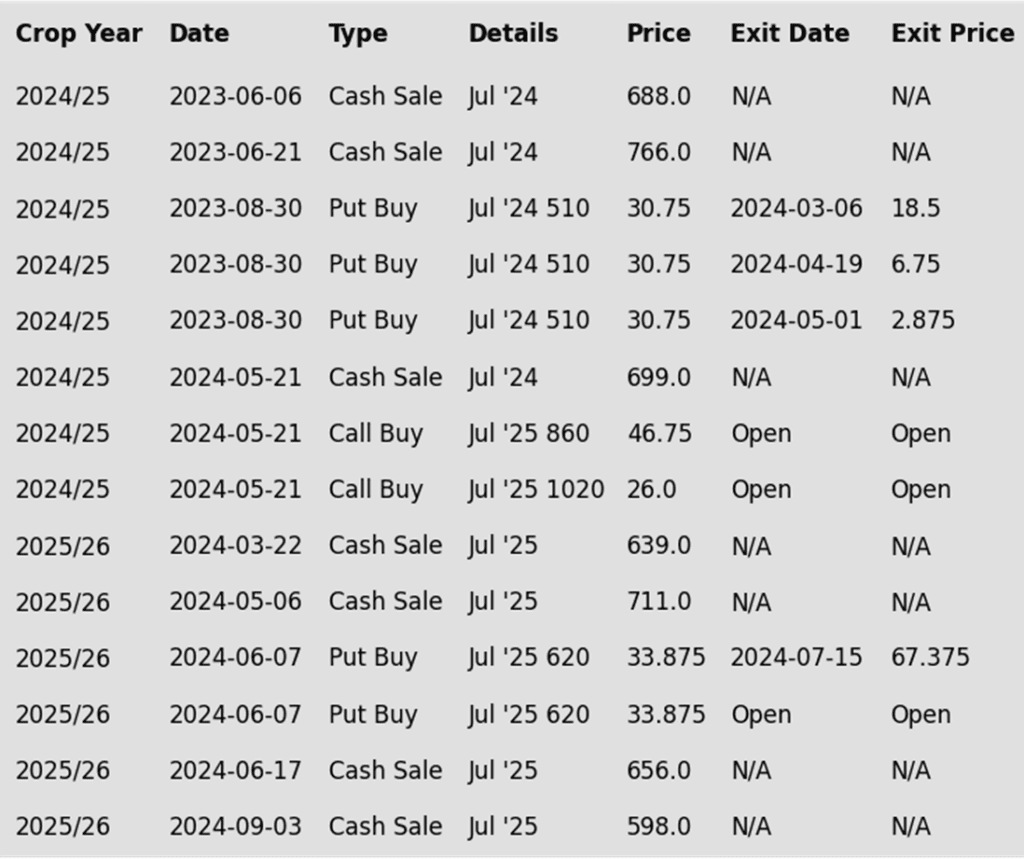

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans closed lower, erasing all of yesterday’s gains and more, as the market continues to trade sideways. Favorable South American weather and rising production estimates weighed on prices. Soybean meal finished higher, while soybean oil tracked weaker palm oil prices.

- This morning, the USDA reported private export sales of 30,000 metric tons of soybean oil to South Korea for delivery during the 24/25 marketing year, highlighting strong demand potential with soybean oil currently at a steep discount to palm oil.

- In November, Malaysian palm oil inventories fell 4.3% to 1.8 million tons, while crude palm oil production declined 5.6% to 1.7 million tons. This has been supportive to palm oil prices, but soybean oil has been following those moves less closely.

- Some pressure in the soybean oil market may be coming from the incoming administration’s potential policies on biofuel use in the US, and the lack of current guidance on the 45Z policy. It is unlikely that these will have any long term effect on demand as global biofuel use has trended significantly higher over recent years.

The soybean market continues to trend sideways just above 975 support. Should the market close below there, it could be at risk of sliding toward the 940 support area near the August low. Conversely, if prices gain traction and rally, they could resistance near the 50-day moving average and 1013 before retesting 1045.

Wheat

Market Notes: Wheat

- Wheat clawed back to a positive close in Chicago and Kansas City futures, while Minneapolis posted small losses. Matif wheat’s mixed close and the consolidating US Dollar Index offered little direction.

- Rumors of wheat quality concerns from excessive rains in southeastern Australia, despite projections of a larger crop than last year, may have supported the US market.

- Ukraine’s 24/25 wheat shipments reached 8.96 mmt from July to November, up from 5.8 mmt last year. Despite elevated Black Sea tensions, grain exports remain largely unaffected.

- Statistics Canada will release updated wheat production estimates tomorrow, with an average pre-report projection of 34.3 mmt, matching August’s forecast and 4.1% above last year’s crop.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Chicago Wheat Action Plan Summary

2024 Crop:

- Target the 740 – 760 range versus March ‘25 to make additional sales. While this range may seem far away, it aligns with the market’s potential based on our research as we approach winter dormancy.

- For those holding open July ’25 860 and 1020 call options that were recommended in May, target a selling price of about 73 cents for the 860 calls to offset the cost of the remaining 1020 calls. Holding the 1020 calls will provide protection for existing sales and give you confidence to make additional sales at higher prices.

2025 Crop:

- Continue holding open July ’25 620 puts to maintain coverage for unsold bushels. Back in July Grain Market Insider recommended selling the first half to offset the cost of the now remaining puts.

- Target the 650 – 680 range versus July ’25 to make additional sales.

- Look to protect current sales by buying upside calls in the 745 – 775 range if signs of an extended rally appear. This will give you confidence to sell more bushels at higher prices.

2026 Crop:

- Patience is advised, as we monitor the market for improved conditions and timing. It may be some time before target ranges are set for the 2026 crop.

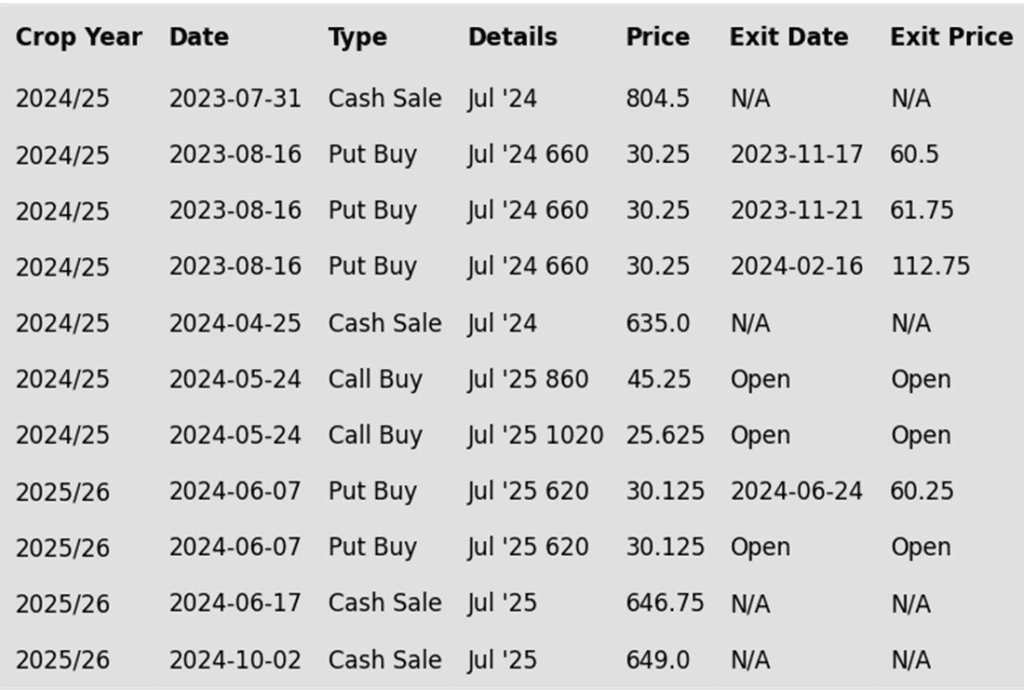

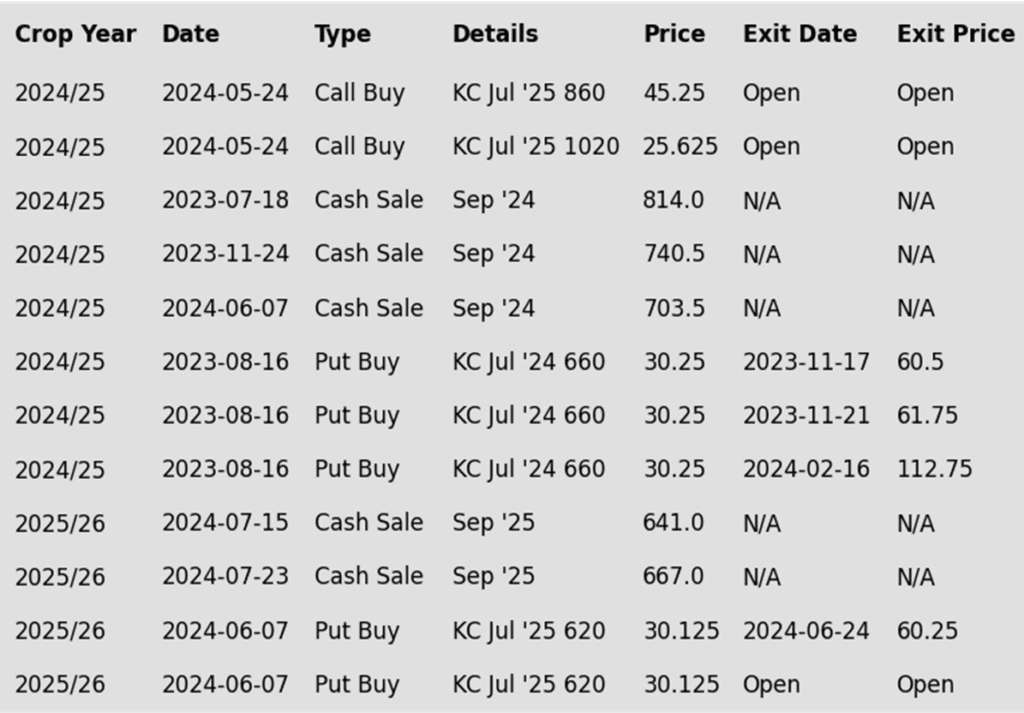

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Front-month Chicago wheat continues to hover just above support at the 540 level. If a bullish trigger emerges, pushing prices through the 50- and 200-day moving averages and closing above 586, it could be poised to retest the 617 area. Conversely, if it slides lower and closes below 536, it may retreat toward the 521–514 support zone.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

KC Wheat Action Plan Summary

2024 Crop:

- Target the 635 – 660 versus March ‘25 area to sell more of your 2024 HRW wheat crop.

- For those holding the previously recommended July ’25 860 and 1020 calls,target a selling price of about 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls, and still give you confidence to sell more bushels at higher prices.

2025 Crop:

- Target the 640 – 665 range versus July ’25 to make additional 2025 HRW wheat sales.

- If the market rallies considerably, look to protect sales by buying upside calls in the 745 – 770 range versus July ’25. This will also give you confidence to sell more bushels at higher prices.

- Continue to hold the remaining half of the previously recommended July ’25 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 to exit half of these remaining puts if the market makes new lows.

2026 Crop:

- Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following KC recommendations:

Since failing to trade above the 50-day moving average (ma), March KC wheat has trended lower and is testing the bottom of the 536 – 577 range. A close below this level could put the market at risk of testing the August low of 527 ¼. Should a bullish catalyst emerge to push prices higher, they could encounter resistance near 567 before re-testing 577.

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Mpls Wheat Action Plan Summary

2024 Crop:

- Target a rally to the 610 – 635 area versus March ‘25 to sell more of your 2024 crop. We are at that time of year when seasonal price trends become more favorable.

- For those holding the previously recommended July ’25 KC wheat 860 and 1020 calls, target a selling price of approximately 71 cents on the 860 calls. This would achieve a net-neutral cost on the remaining 1020 calls and provide confidence to sell more bushels at higher prices.

2025 Crop:

- Target a rally back to the 710 – 735 range versus Sept. ’25 to make additional early sales on your 2025 crop. While this target area may seem far off, it aligns with the market’s potential based on our research. conditions improve seasonally. This could be as early as late November or December.

- Look to protect existing sales by buying upside calls in the 745 – 770 range versus July ’25 KC wheat if the market turns higher and rallies considerably. This will also give you confidence to sell more bushels at higher prices.

- Continue holding the remaining half of the previously recommended July ’25 KC wheat 620 puts to provide downside protection for unsold bushels. Additionally, target the upper 400 range versus July ’25 KC wheat to exit half of these remaining puts if the market makes new lows.

2026 Crop:

- Patience is recommended. It may be some time before targets are set for the 2026 crop, as we continue to monitor the market for better conditions and timing.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Since late November, Minneapolis wheat has drifted lower, finding support just above the March contract low of 584 ½. If the market closes below this level, it could risk trading down to the 563 support area. Conversely, if a bullish trigger pushes prices higher and close above 613, they could be poised to test the October highs near 655.

Other Charts / Weather

US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

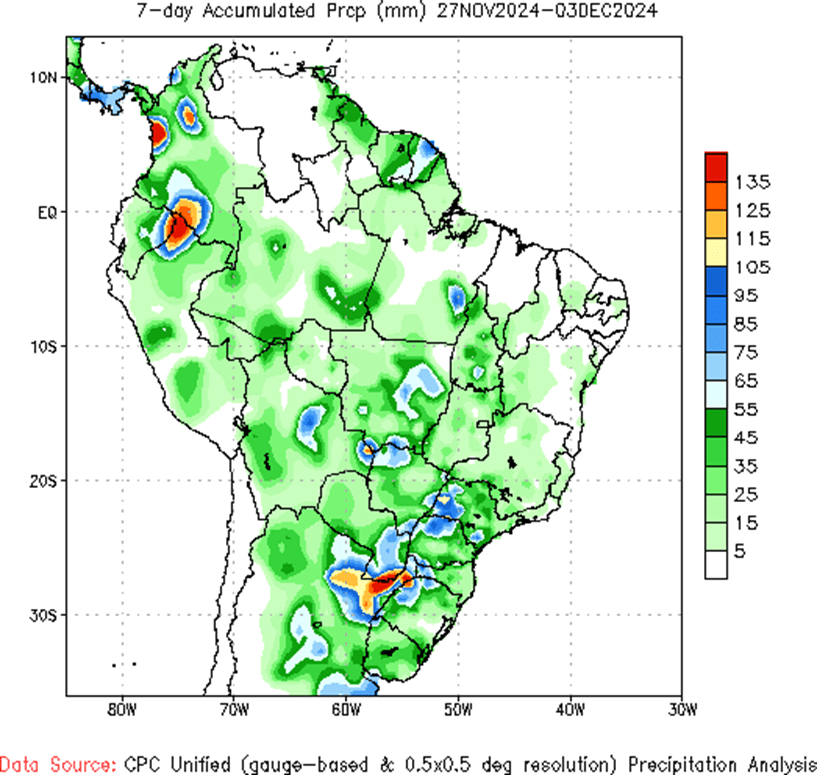

Brazil 7-day total accumulated precipitation courtesy of the National Weather Service, Climate Prediction Center.

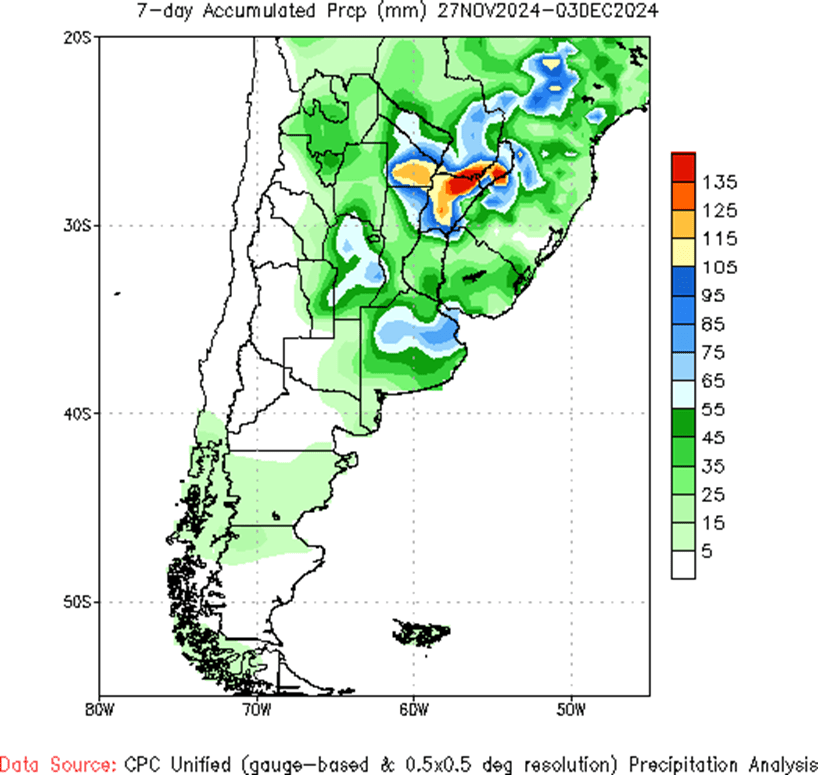

Argentina 7-day total accumulated precipitation courtesy of the National Weather Service, Climate Prediction Center.