12-27 End of Day: Grains Settle Mixed on Light Holiday Volume

All prices as of 2:00 pm Central Time

| Corn | ||

| MAR ’24 | 476.5 | -3.75 |

| JUL ’24 | 498 | -3.5 |

| DEC ’24 | 506.5 | -3 |

| Soybeans | ||

| JAN ’24 | 1316.75 | 3.5 |

| MAR ’24 | 1320.5 | 1.5 |

| NOV ’24 | 1265.25 | 0 |

| Chicago Wheat | ||

| MAR ’24 | 623 | -13.25 |

| MAY ’24 | 633.75 | -12.5 |

| JUL ’24 | 639.5 | -13.5 |

| K.C. Wheat | ||

| MAR ’24 | 635 | -7.75 |

| MAY ’24 | 637.5 | -8.25 |

| JUL ’24 | 640 | -10.25 |

| Mpls Wheat | ||

| MAR ’24 | 721.75 | -7.5 |

| JUL ’24 | 740 | -7.5 |

| SEP ’24 | 747.75 | -8 |

| S&P 500 | ||

| MAR ’24 | 4820 | -5 |

| Crude Oil | ||

| FEB ’24 | 74.1 | -1.47 |

| Gold | ||

| FEB ’24 | 2088.6 | 18.8 |

Grain Market Highlights

- A more favorable outlook for Brazilian weather, a lower wheat market, and a lack of fresh bullish news led the corn market to end the day lower on light holiday volume, breaking its three day run of higher closes.

- With support coming from a bullish reversal in soybean oil, soybeans closed mostly higher on the day after trading below unchanged for much of the session on low year-end holiday volume.

- Soybean meal and oil closed in opposite directions with meal lower on the day and oil higher, though both products rallied off the day’s lows. Position squaring appears to have dominated the product’s trade, as traders look to even up their respective long meal or short oil positions before the year’s end.

- The falling US dollar failed to ignite any follow through buying in the wheat complex, as all three wheat classes gave up a portion of yesterday’s gains. Chicago, being the weakest of the three, led the way with double digit losses across the board, while old crop KC gained on new crop, likely on improved conditions.

- The US dollar continued its downtrend and traded to its lowest level since July 27, 2023, on expectations that the Federal Reserve will begin reducing rates before other central banks. The downtrend in the dollar makes US exports more competitive and may provide some level of underlying support.

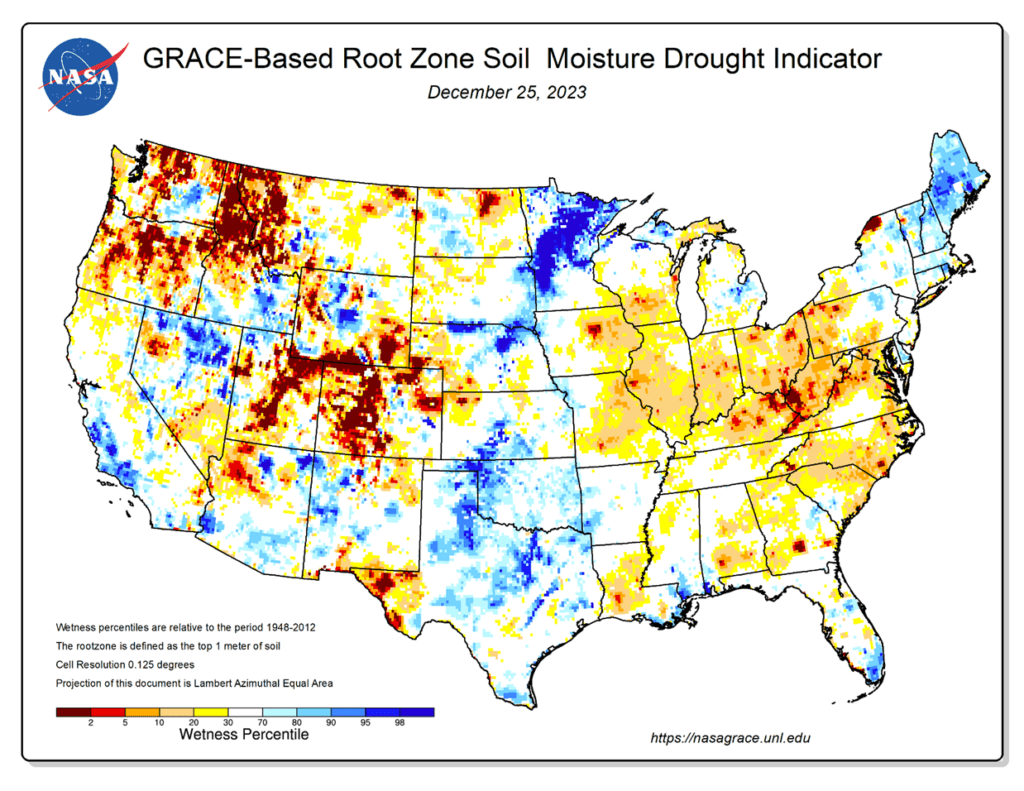

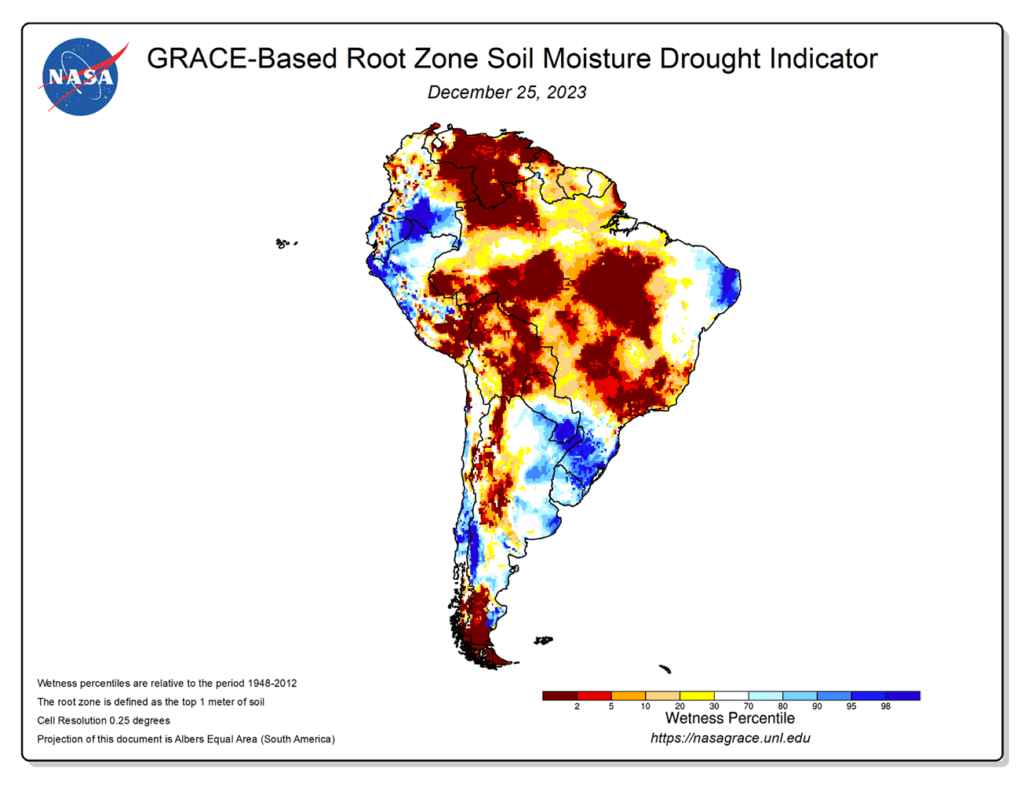

- To see the updated GRACE-Based Root Zone Soil Moisture Drought Indicator maps of the US and South America, courtesy of NASA GRACE and the NDMC, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

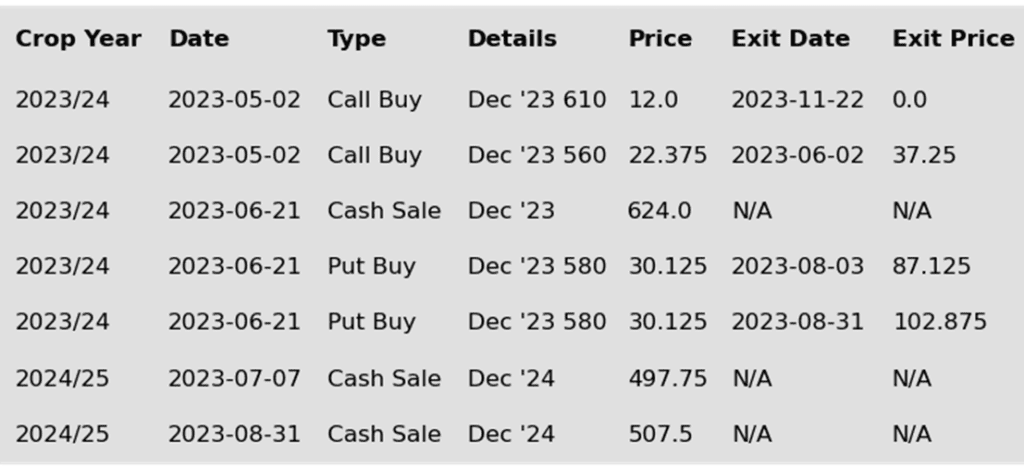

- No new action is recommended for 2023 corn. Since the beginning of August, the corn market has traded sideways largely between 470 and 500. October’s brief breakout to 509 ½ and the subsequent failure to stay above the 50-day moving average indicates there is significant resistance in that price range. The failure of December’s USDA report to provide a bullish influence on the market puts the market at risk of drifting sideways to lower without a bullish catalyst. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. For now, Grain Market Insider will continue to hold tight on any further sales recommendations for the next few weeks with the objective of seeking out better pricing opportunities. If the market has not turned around by then, Grain Market Insider may sit tight on the next sales recommendations until spring.

- No new action is recommended for 2024 corn. Since late February ’22, Dec ’24 has been bound by 485 ¾ on the bottom and 602 on the top. After testing 491 to 547 last July, it has mostly traded between 500 and 525. During this time, Dec ’24 has held up better as bear spreading has allowed Dec ’24 to maintain more of its value versus old crop prices as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Moving forward, the risk for 2024 prices is the same as for 2023 prices, which is a continuation of a sideways to lower trend without a bullish catalyst. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying Dec ‘23 560 and 610 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

- No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

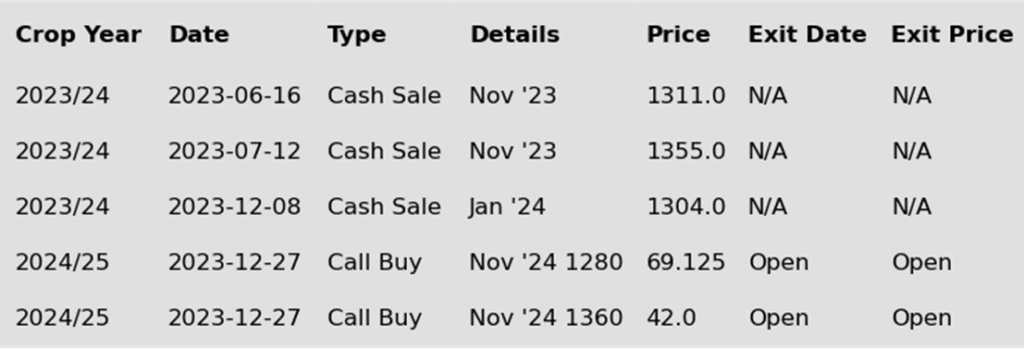

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

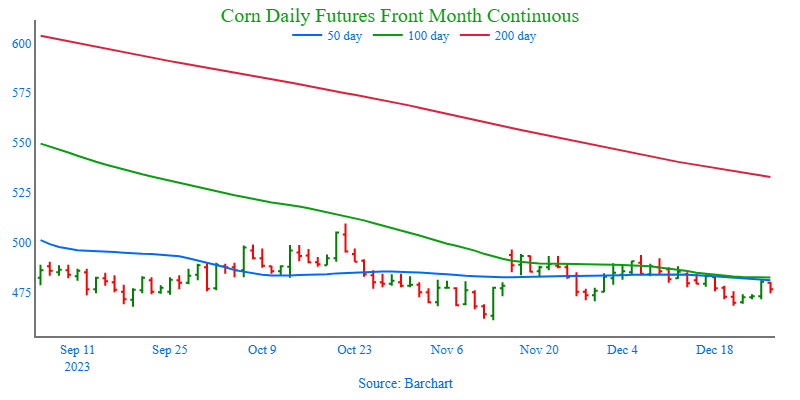

- Today’s lower close in corn marks the end of a three-session rally for the March contract. Without much fresh news to drive the market and a more favorable outlook for Brazil, corn did not find much footing today. Additionally, shortened holiday weeks tend to be a bit choppy with lighter trade volume.

- Private estimates of the Brazil corn crop are as low as 117 mmt, whereas the USDA is using a figure of 129 mmt. There may be some delays to safrinha planting due to weather issues, but without the crop in the ground, it may be too early to determine if that will significantly impact the crop.

- According to the CFTC, as of December 19, managed funds added nearly 30,000 short corn contracts to bring their total short position to 180,724. This may be adding some pressure to the market, but also primes it for a short covering rally, provided there is a catalyst to trigger it.

- China has approved 26 seed companies to sell GMO corn and soybean seed in certain provinces. As China works to become more self-sufficient, it may mean that they import fewer goods and commodities from the US. However, this will be bearish in the long term, and is not necessarily a major concern now. With that said, it has been reported that Chinese corn producers are planning to more than double their GMO corn planting next year versus 670,000 hectares in 2023.

Above: Since the middle of November, the March corn contract has been rangebound mostly between 495 up top and 470 on the bottom. Overhead resistance lies between 490 and 497, with heavier resistance near 510, and without fresh bullish input, the market runs the risk testing major support near 460.

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

New Alert

Enter(Buy) NOV ’24 Calls:

1280 @ ~ 69c & 1360 @ ~ 42c

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

- No new action is recommended for 2023 soybeans. Front month soybeans continue to be rangebound, largely between 1290 and 1400. At some point, the front month will eventually break out of that range, and if it breaks out to the downside, then the first risk would be 1180. If the breakout occurs to the topside, then the first opportunity would be 1510. The biggest looming catalyst behind a potential downside breakout is the projected record global carryout of soybeans, while the biggest looming catalyst for a potential upside breakout is continued adverse South American weather. Given the uncertainty of which direction the market will go, Grain Market Insider recently recommended adding to sales as the current price level is still historically good. It’s been disappointing how the market has been unable to push higher despite the South American planting disruptions. Because of that, Grain Market Insider’s concern is that, if the weather pattern doesn’t remain adverse, the path of least resistance could be lower. Grain Market Insider will continue to look at additional sales opportunities, as well as potential re-ownership strategies.

- Grain Market Insider recommends buying November ’24 1280 soybean calls and November ‘24 1360 calls in equal quantities with a total net spend of approximately 111 cents plus commission and fees. Since the middle of last July, the Nov ’24 contract has been largely rangebound between 1250 and 1320. Today’s settlement of 1265 ¼ is the fourth day in a row with a close above 1250 support and the third day in a row with a stronger closing price. Grain Market Insider wants to take advantage of this value area and recommend purchasing call options. Purchasing call options now will give you confidence to make sales against anticipated production for the 2024 crop, which is yet to be planted, and they will also help to protect those future sales in the event prices continue to rally further.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Year end trade added to the volatility in the soybean complex, which saw two sided trade on relatively low holiday volume. Soybeans reversed course, ending the day higher after trading lower in the overnight session. Soybean oil lent support to soybeans as it posted a bullish reversal and also closed higher on the day, while meal closed lower, but well off its lows.

- Overall, Brazilian weather is improving with showers throughout central and northern Brazil and a wet forecast with shower activity set to favor the northeastern areas, though the forecasts have improved, they still need to verify into actual rainfall, which at times has been less than expected.

- The situation in Argentina has improved considerably from last year, with favorable weather overall and expectations of a normal to possibly above normal crop. The potential increase in Argentina’s production could more than offset the potential losses in Brazil, which is adding resistance to prices.

- Brazilian crop watcher, Dr. Michael Cordonnier, lowered his estimate of Brazil’s soybean production to 153 mmt, and cited the variable rain amounts and coverage over the past week for his conclusions.

- In other news, according to China’s Ministry and Agricultural and Rural Affairs, China approved 26 seed companies to produce, distribute, and sell GMO corn and soybean seeds. The move comes as the country attempts to become more self-sufficient in securing its own food supply.

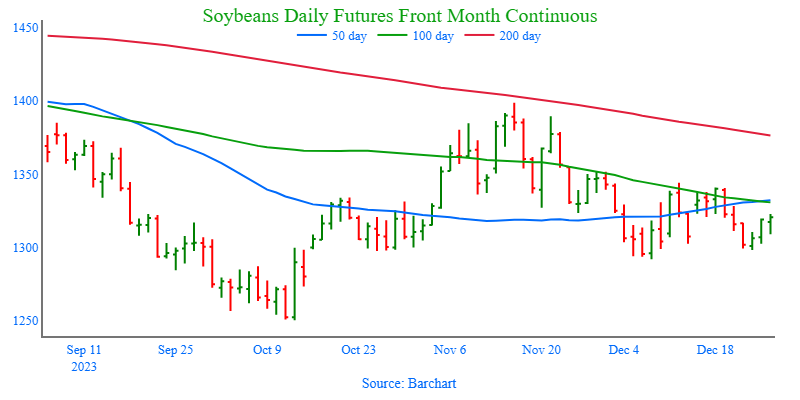

Above: After posting a high of 1398 ½ in November, soybeans found support around 1292. Overhead, nearby resistance remains near 1350 and again around 1400. If the market breaks support at 1292, it runs the risk of testing 1250.

Wheat

Market Notes: Wheat

- Most of yesterday’s gains in wheat were erased today with lower closes in all three US futures classes. In addition, the spread between the March contracts of Chicago and Kansas City wheat has been narrowing as the conditions in the US southern Plains improve with more moisture.

- Wheat also saw weakness today, even though the US Dollar Index continues to drop. At the time of this writing, it has broken below the 101 level and is the lowest it has been since July 27. This should make US wheat more attractive to global importers. But Russia continues to be the cheapest origin with FOB values around $240 to $243 per mt.

- Coceral, a grain trade association, has estimated that EU soft wheat production next year will be 139.4 mmt, up just 0.1 mmt from 2023. This is practically no change and comes even though France may have reduced production due to weather issues that delayed planting; Spain is expected to make up the difference.

- According to Russia, their 2023 grain harvest is the second largest on record at 142.6 mmt. Of that total, wheat accounted for about 93 mmt. That is down from 104.2 mmt of wheat in 2022, but is still a large amount that is sure to keep Russian prices low and a dominance in terms of the export market.

Action Plan: Chicago Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Chicago Wheat Action Plan Summary

- No new action is currently recommended for 2023 Chicago wheat. Between late July and the end of November, front month Chicago wheat trended lower, driven mostly by weak US demand and lower world wheat prices. During that time, and as managed funds established most of their short position of nearly 120,000 contracts, the market became extremely oversold. Since then, as the market rallied to a high of 649 ½, China made several US SRW wheat purchases, and funds covered more than 23,000 short contracts. During that runup, Grain Market Insider recommended making an additional sale to take advantage of the elevated prices in case the rally was temporary since US wheat prices remain elevated relative to other world exporters, despite the increase in demand. If the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

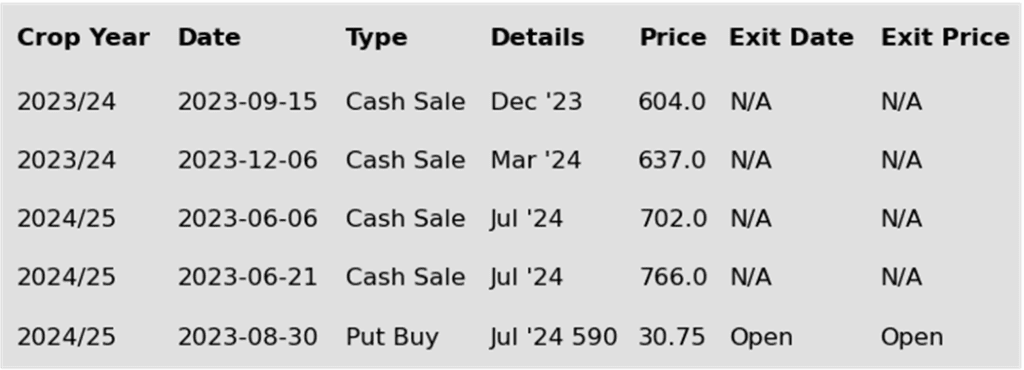

- No new action is recommended for 2024 Chicago wheat. From the end of July, the July ’24 contract has slowly stepped its way down to a low of 586 in sympathy with the front month contract where managed money established a large short position during that time. Since then, July ’24 rallied alongside the March ’24 contract, as the funds covered over 30k contracts of their nearly 130k short contract position. While bearish headwinds remain, the funds continue to carry a large short position and seasonals remain supportive for the addition of weather risk premium, which are two factors that could fuel further short covering and another leg up in prices. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for further price erosion. Back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset much of the original cost and move toward a net neutral cost for the remaining position.

- No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

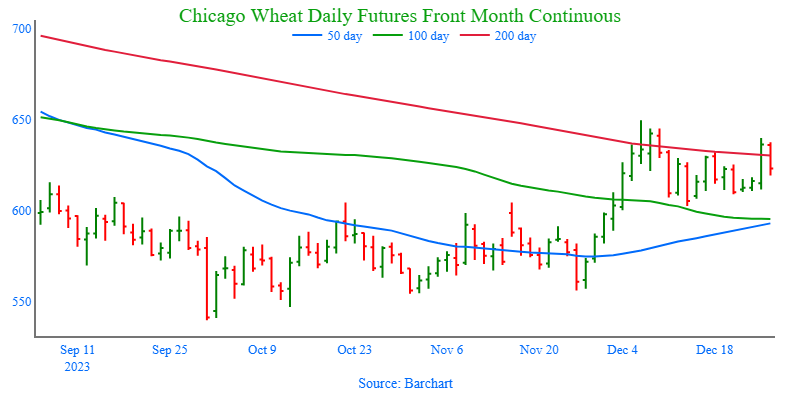

Above: After rallying to 649 ½, Chicago wheat became overbought and turned lower after the December 8 USDA report. Since then, the market has found nearby support near 600. Nearby resistance remains overhead near 650, with additional resistance between 660 and 665. If the market breaks nearby support, it may test the 50-day moving average, and then support near 556.

Action Plan: KC Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

KC Wheat Action Plan Summary

- No new action is recommended for 2023 KC wheat crop. Since late July old crop KC wheat has been in a downtrend that has largely been driven by managed fund selling on low world wheat prices and weak US export demand. As the selloff progressed, the market became oversold, and the funds established the largest short position in three years. Even though bullish headwinds remain, these two factors have fueled the recent short-covering rally, which could extend much further if a bullish catalyst enters the market. This would also line up with the historical tendency for price appreciation as the market builds risk premium going into wintertime. Grain Market Insider’s strategy is to look for price appreciation going into this winter, as weather becomes a more prominent market mover and may consider suggesting additional sales if prices become over extended.

- No new action is recommended for 2024 KC wheat. At the end of August, the July ’24 contract broke out of roughly a one-year trading range and stepped down to a 609 ¼ low in late November, largely driven by managed fund selling in the front month on weak US export demand and lower world wheat prices. Since then, the funds covered part of their large short position which also rallied prices in the July ’24 contract. While bearish headwinds remain, managed funds continue to hold a sizable, short position, and price seasonals remain positive for adding weather risk premium. These are two factors that could fuel additional short covering and rally prices in the months ahead. Back in August, Grain Market Insider recommended buying Jul’24 KC wheat 660 puts to protect the downside following the range breakout. As the market recently got further extended into oversold territory and the July contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. Moving forward, Grain Market Insider is prepared to recommend exiting the last 25% on any further supportive market developments.

- No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

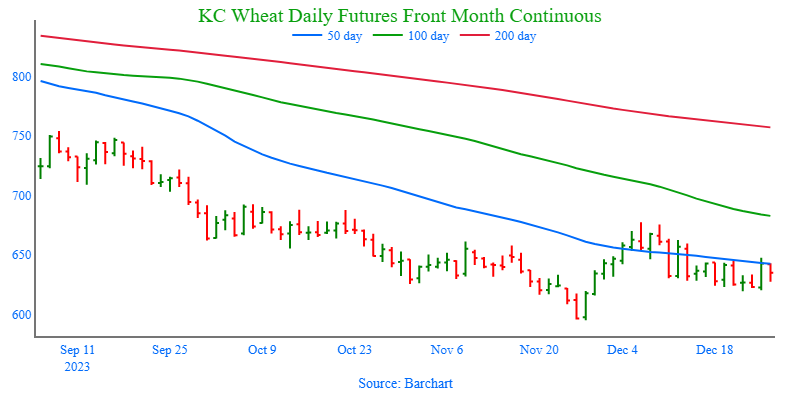

Above: Since posting bearish reversals on December 6 and 8, the market has been consolidating while holding support around 625, with close in resistance just overhead at the 50-day moving average. If the market breaks lower, the next area of support may come in around 595 and 575. Resistance above the 50-day moving average remains around 675 – 680.

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

- No new action is currently recommended for the 2023 New Crop. Following last July’s rally, the market has slowly stair-stepped lower, primarily due to low world wheat prices, weak US export demand, and managed fund selling. With the funds building a record large short position as the market sold off. Since weak US export demand remains the main impediment to higher prices, the market continues to be at risk of further downside erosion. The record large fund short position could fuel a rally back higher if a bullish catalyst enters the scene, and if that happens, it may signal that a near-term low is in place. Earlier this year, Grain Market Insider made a sales recommendation during the July rally near 820, and with that sale in place, Grain Market Insider’s strategy is to look for price appreciation this winter with an eye on considering additional sales around 725 – 775, and again north of 800. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

- No new action is recommended for 2024 Minneapolis wheat. At the end of August, the Sept ’24 contract traded to a peak of 871 ¾ and has continued to slowly stair-step lower, largely driven by lower world wheat prices, weak US export demand, and managed fund selling, and as the selloff progressed, the funds built up a record large short position. While bearish headwinds remain, the significant oversold condition of the market and the large fund net short position are two factors that could fuel a short-covering rally in the months ahead. Price seasonals are also supportive as prices tend to build in some risk premium going into the winter months. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside following a 1-year range breakout in KC wheat. Though recently, as the KC market extended further into oversold territory and the July ‘24 KC wheat contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. While in the same time frame, Grain Market Insider also recommended making an additional sale as the Sept ’24 Minneapolis contract broke long time 743 support. For now, moving forward, Grain Market Insider is prepared to recommend exiting the last 25% of the open puts on any further supportive market developments.

- No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

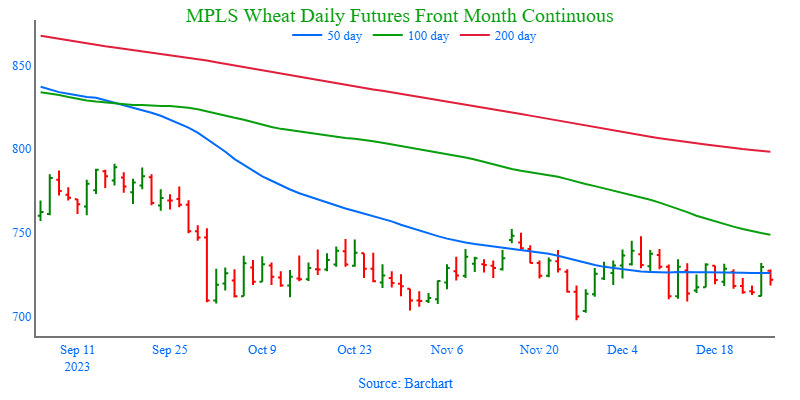

Above: After making a new contract low on November 27, the March contract found buying interest from its oversold status and record fund short. Since then, the market posted a bearish reversal on December 6, showing significant resistance in the 750 area. If prices can break through upside resistance, they could run toward 790. If prices retreat, nearby support could be found around 718, with further support near the recent low of 697 ½.

Other Charts / Weather