12-13 End of Day: Argentine Currency Devaluation Pressures Grains Lower

All prices as of 2:00 pm Central Time

| Corn | ||

| MAR ’24 | 479.5 | -5.75 |

| JUL ’24 | 501.75 | -4.25 |

| DEC ’24 | 507.75 | -3.75 |

| Soybeans | ||

| JAN ’24 | 1307.5 | -16.25 |

| MAR ’24 | 1326.25 | -16.5 |

| NOV ’24 | 1274.25 | -7.25 |

| Chicago Wheat | ||

| MAR ’24 | 605.25 | -20.25 |

| MAY ’24 | 616.5 | -19 |

| JUL ’24 | 623.75 | -18.25 |

| K.C. Wheat | ||

| MAR ’24 | 632 | -24.75 |

| MAY ’24 | 637 | -23.25 |

| JUL ’24 | 641 | -21.5 |

| Mpls Wheat | ||

| MAR ’24 | 713.5 | -16 |

| JUL ’24 | 730.5 | -15.5 |

| SEP ’24 | 738.25 | -15.25 |

| S&P 500 | ||

| MAR ’24 | 4749.5 | 52.25 |

| Crude Oil | ||

| FEB ’24 | 69.69 | 0.84 |

| Gold | ||

| FEB ’24 | 2032.2 | 39 |

Grain Market Highlights

- Argentina is moving to devalue its currency, which weighed heavily on the soybean complex. The move would likely increase Argentine farmer selling and exports, adding competition to US exports. Soybean meal also continues to see pressure (adding resistance to soybeans) from the improved Argentine weather outlook and crop prospects, which could likely return the country to the world’s top soy product exporter status.

- The devaluation of Argentina’s currency, the world’s 3rd largest corn exporter, also weighed on the corn market, despite strong ethanol production numbers that came in above expectations and well ahead of the pace needed to reach the USDA’s corn usage estimate.

- There are thoughts that the policy changes in Argentina could increase the country’s wheat crop by as much as 60%, and this could have added downward pressure to the wheat markets. While Chicago made new lows for the move, KC and Minneapolis also gave up most, if not all, of yesterday’s gains on the reversal lower.

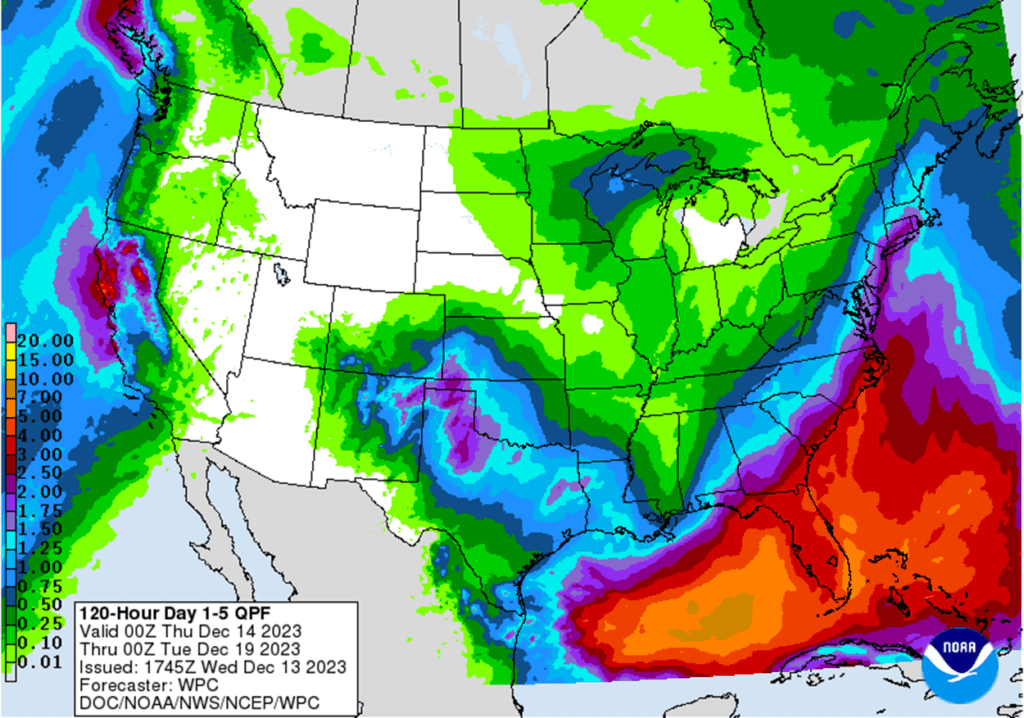

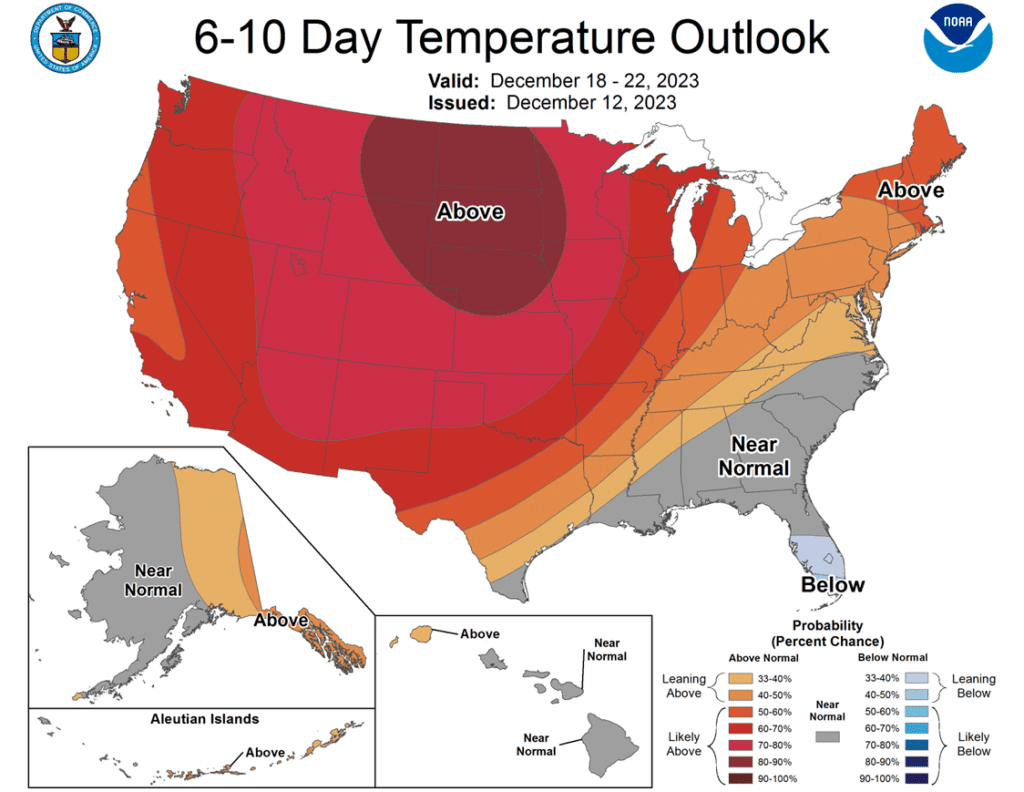

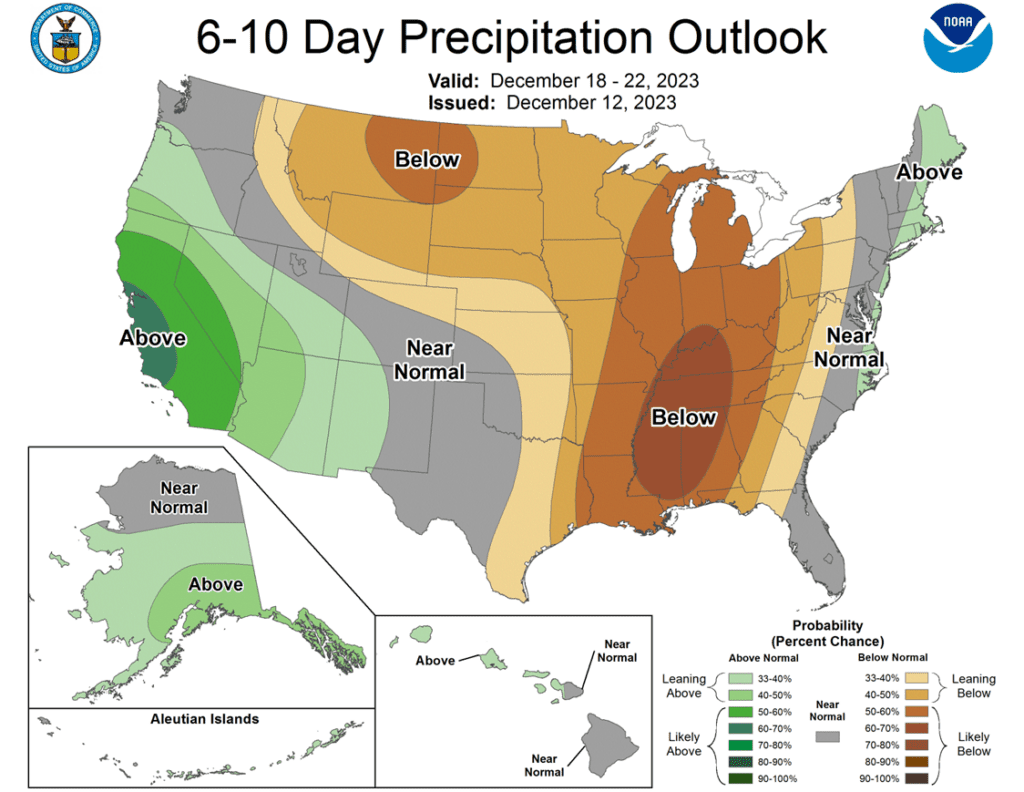

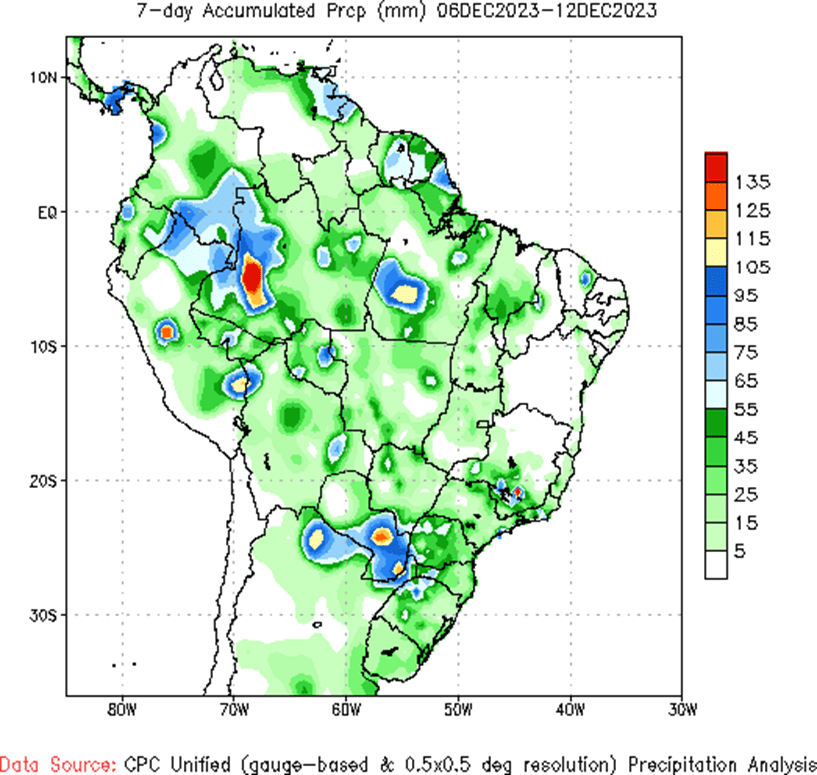

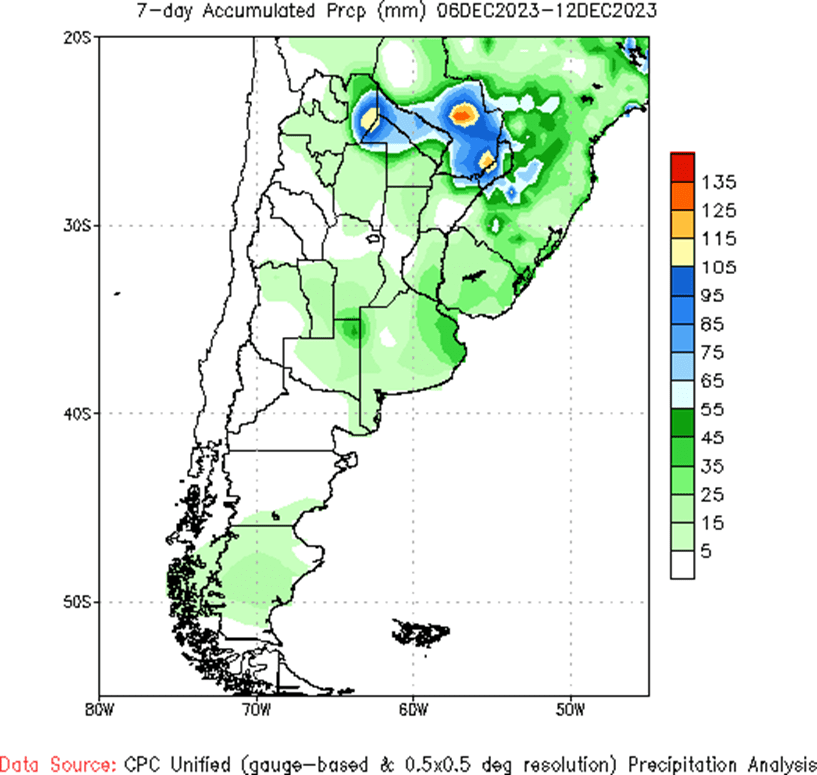

- To see the updated US 5-day precipitation forecast, 6 – 10 day temperature and precipitation outlooks, and Brazil’s and Argentina’s 7-day total accumulated precipitation maps, courtesy of the National Weather Service, NOAA, and Climate Prediction Center, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Corn Action Plan Summary

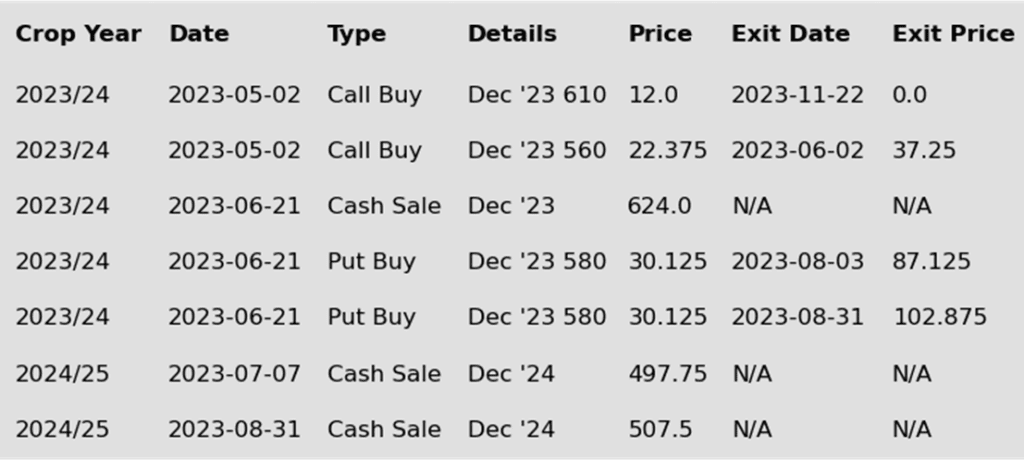

- No new action is recommended for 2023 corn. Since the beginning of August, the corn market has traded sideways largely between 470 and 500. October’s brief breakout to 509 ½ and the subsequent failure to stay above the 50-day moving average indicates there is significant resistance in that price range. The failure of December’s USDA report to provide a bullish influence on the market puts the market at risk of drifting sideways to lower without a bullish catalyst. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. For now, Grain Market Insider will continue to hold tight on any further sales recommendations for the next few weeks with the objective of seeking out better pricing opportunities. If the market has not turned around by then, Grain Market Insider may sit tight on the next sales recommendations until spring.

- No new action is recommended for 2024 corn. Since late February ’22, Dec ’24 has been bound by 485 ¾ on the bottom and 602 on the top. After testing 491 to 547 last July, it has mostly traded between 500 and 525. During this time, Dec ’24 has held up better as bear spreading has allowed Dec ’24 to maintain more of its value versus old crop prices as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Moving forward, the risk for 2024 prices is the same as for 2023 prices, which is a continuation of a sideways to lower trend without a bullish catalyst. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying Dec ‘23 560 and 610 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

- No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

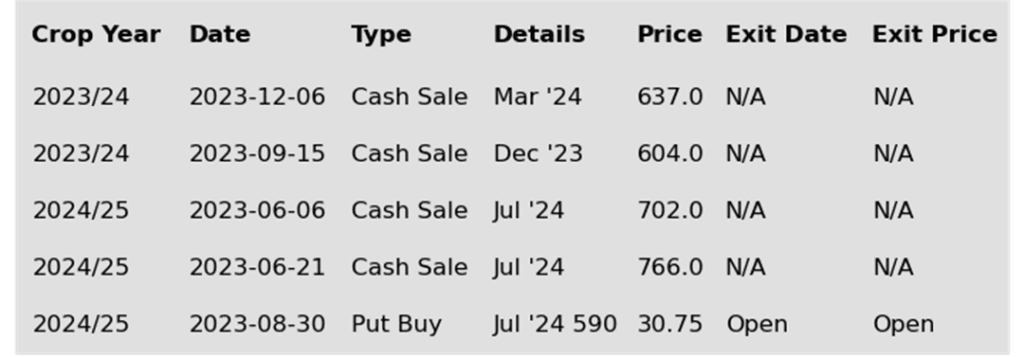

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn futures and the grain markets traded lower on Wednesday. March corn lost 5 ¾ cents on the session as grain markets saw broad based selling pressure.

- Argentina devalued their currency, the peso, versus the dollar to stabilize Argentina’s economy. The drop in the peso value makes Argentina’s ag exports more competitive on the world export market, which pressured the ag commodity markets on Wednesday.

- Ethanol production fell to 1,074,000 barrels/day, down slightly from last week, but up 1.2% from last year. Production was above expectations and the 2nd highest of the marketing year. There was 108 mil. bu. of corn used in the production process. Ethanol margins are likely to tighten as pressure in the crude oil market could be starting to tighten those margins.

- The USDA will release weekly export sales on Thursday morning. Corn sales have improved, which is needed by the market given the supply. Expectations for new sales to range from 800,000 – 1,600,000 mt last week.

- South American weather stays a focus. The next 7 days show a drier forecast with a strong heat wave returning. Longer extended forecasts are more favorable for crop growth if those forecasts materialize.

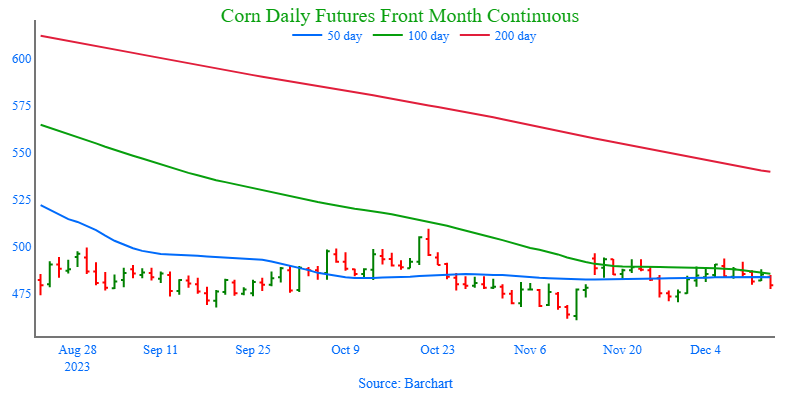

Above: Since the lead month rolled to the March contract, the corn market has been rangebound between 470 on the downside and 497 on the upside. Upside resistance appears to be heavy given the bearish reversal that was posted on December 6. That heavy resistance also extends up to the October high of 509 ½, which the market will need more bullish influence to trade through. If the market retreats through nearby 470 support, major support remains near 460.

Soybeans

Action Plan: Soybeans

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

Active

Sell JAN ’24 Cash

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Soybeans Action Plan Summary

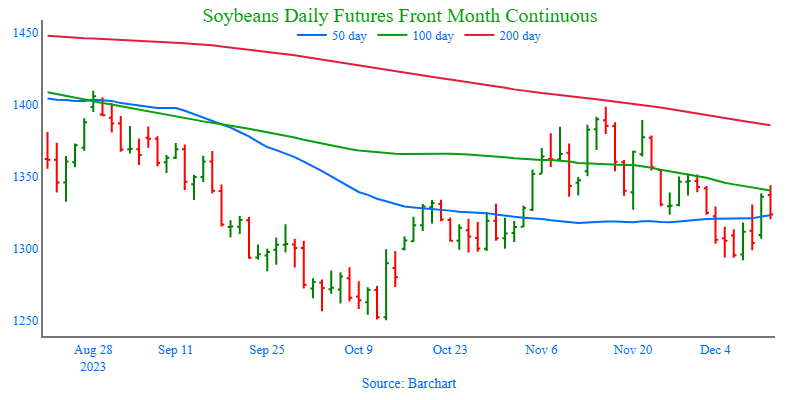

- Grain Market Insider sees a continued opportunity to sell a portion of your old crop 2023 soybean production. Since last summer, the soybean market has been mostly rangebound between 1435 on the topside and 1251 on the bottom. Within this range, the 1330 area has been a strong pivot point. When over 1330, the front month has been able to challenge the 1400 area, but below 1330 the front month has challenged the 1250 area. Following last Friday’s USDA update, the market has attempted to rally above 1330, but so far that rally has been rejected. This rejection poses the risk that the front month could challenge the 1250 area again. Also, given the projected record large global carryout of soybeans, Grain Market Insider wants to take advantage of the historical value of 1300+ soybean prices.

- No action is recommended for the 2024 crop. Since the inception of the Nov ’24 contract, it has traded at a discount to the 2023 crop from as much as 142 back in July, to as little as 17 ¾ in early October during harvest. While the spread difference between the two crops has seen a good amount of volatility, Nov ’24 has been largely rangebound between 1250 and 1320 since it rallied off its 1116 ¼ low last May. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the earliest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

- No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day lower again with prices now back below all major moving averages on a nearby, front month chart. The forecast for more favorable Brazilian weather a week from now, along with anticipation of increased Argentine selling pressured the soy complex lower today.

- Newly inaugurated Argentinian president, Javier Milei, has been preparing to get inflation in check with policy changes to grain export taxes. So far, they temporarily suspended export licenses and devalued the Argentinian peso by half. Milei is also expected to make adjustments to export taxes on grain, which could further incentivize selling.

- This morning, the USDA reported private exporter sales of 125,000 metric tons of soybeans for delivery to unknown destinations during the 2024/2025 marketing year. This is the fifth consecutive sale since last Thursday by either China or unknown destinations.

- Brazilian weather is set to remain hot and dry over the next 5 days, but rain is forecast to return on December 19 and is expected to last well into January. Southern Brazil is still too wet and is expected to receive more rain over the next 7 days before drying out slightly into the new year.

Above: Since retreating from the November highs, soybeans traded through 1297, but held support around 1292. If prices retreat lower through 1292, they could test support near 1250. Up above, psychological resistance may enter in near 1350, with heavy resistance up near recent highs around 1400.

Wheat

Market Notes: Wheat

- Kansas City futures led the wheat complex lower today, but all three classes had sharp losses. The big news weighing on the grain markets relates to Argentina’s new president and his economic policy. In addition to currency devaluation and possible export tax adjustments, there is also talk that Argentina will expand wheat production under his leadership. Some estimates see production increase as much as 60% to 25 mmt next growing season, due to deregulation that encourages more output.

- This afternoon, the Fed announced that they will be keeping interest rates unchanged for the third time in a row. After the announcement, the US Dollar Index dropped significantly, and this may provide some support to wheat tomorrow, as the two tend to share an inverse relationship.

- According to Argus, Ukrainian wheat production in 2024 will fall to 20.2 mmt, a 12-year low, and representing a 9% decline. Smaller plantings are said to be the cause of the decline, which would be the lowest since 12/13.

- Adding to bearishness today was an estimate from FAO-AMIS, which raised world wheat stockpiles for the 23/24 season from 315.1 mmt to 319.3 mt. The production estimates for Russia, Turkey, and Saudi Arabia were increased. Additionally, corn and rice stockpile estimates were also increased.

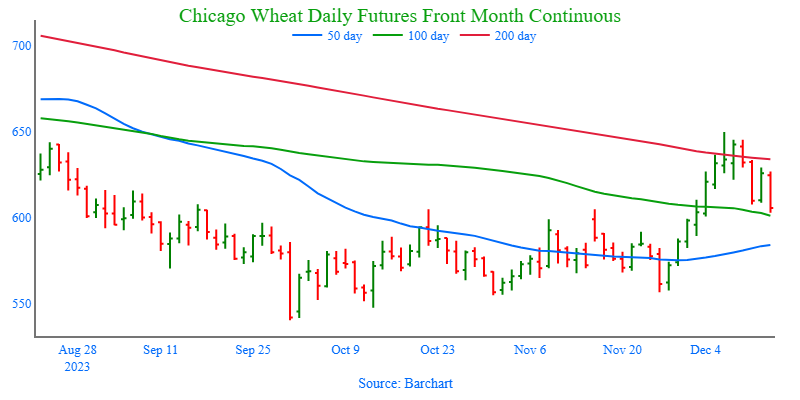

- From a technical perspective, March Chicago wheat did hold just above the six-dollar level today, with a low of 6.02-1/2. The 21, 40, and 50-day moving averages all converge around this level, making six dollars an important area of support. A break below this level would make the market look more technically weak.

Action Plan: Chicago Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Chicago Wheat Action Plan Summary

- No new action is currently recommended for 2023 Chicago wheat. Between late July and the end of November, front month Chicago wheat trended lower, driven mostly by weak US demand and lower world wheat prices. During that time, and as managed funds established most of their short position of nearly 120,000 contracts, the market became extremely oversold. Since then, as the market rallied to a high of 649 ½, China made several US SRW wheat purchases, and funds covered more than 23,000 short contracts. During that runup, Grain Market Insider recommended making an additional sale to take advantage of the elevated prices in case the rally was temporary since US wheat prices remain elevated relative to other world exporters, despite the increase in demand. If the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

- No new action is recommended for 2024 Chicago wheat. Since July, new crop Chicago wheat has slowly worked its way lower with no significant opportunities to make additional sales. The lower market was driven mostly by managed fund selling from lower world wheat prices and weak US demand. As the market sold off, it became significantly oversold with managed funds building a short position in excess of 100,000 contracts. While bearish headwinds remain, the large fund short position and oversold condition of the market are two factors that could fuel a sizeable, short-covering rally. Additionally, price seasonals are supportive as prices tend to build in some risk premium going into the winter months. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for further price erosion, and back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset much of the original cost and move toward a net neutral cost for the remaining position.

- No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: After rallying to 649 ½ on short covering activity largely, from being oversold, Chicago wheat became overbought and began to turn lower following the December 8 USDA update. Overhead resistance comes in near 650, and again between 660 and 665. The overbought status of the market may encourage additional selling and a test of the 50-day moving average near 580, with further support near 556.

Action Plan: KC Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

KC Wheat Action Plan Summary

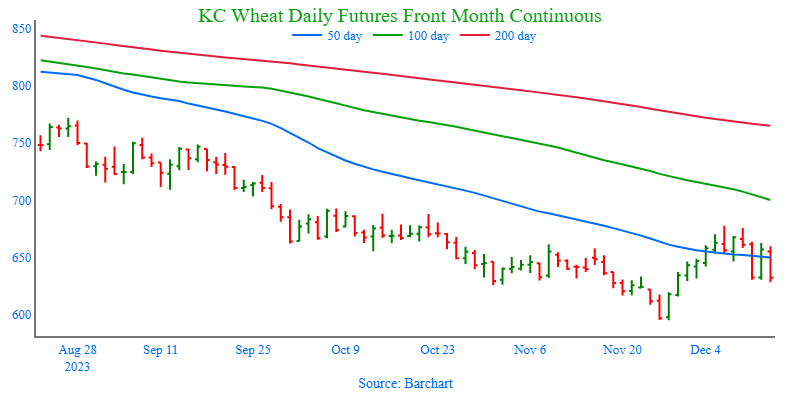

- No new action is recommended for 2023 KC wheat crop. Since late July old crop KC wheat has been in a downtrend that has largely been driven by managed fund selling on low world wheat prices and weak US export demand. As the selloff progressed, the market became oversold, and the funds established the largest short position in three years. Even though bullish headwinds remain, these two factors have fueled the recent short-covering rally, which could extend much further if a bullish catalyst enters the market. This would also line up with the historical tendency for price appreciation as the market builds risk premium going into wintertime. Grain Market Insider’s strategy is to look for price appreciation going into this winter, as weather becomes a more prominent market mover and may consider suggesting additional sales if prices become over extended.

- No new action is recommended for 2024 KC wheat. At the end of August, the Jul ’24 contract broke out of roughly a one-year trading range, between 740 and 860, to the downside. Since that breakout, the market has continued to slowly stair-step lower, largely driven by managed fund selling, weak US export demand, and lower world wheat prices. As the selloff progressed, the funds built up the largest net short position in three years. While bearish headwinds remain, the significant oversold condition of the market and the large fund net short position are two factors that could fuel a short-covering rally in the months ahead. Price seasonals are also supportive as prices tend to build in some risk premium going into the winter months. Back in August, Grain Market Insider recommended buying Jul’24 KC wheat 660 puts to protect the downside following the range breakout. Though as the market recently got further extended into oversold territory and the July contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. Moving forward, Grain Market Insider is prepared to recommend exiting the last 25% on any further supportive market developments.

- No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

Above: Following bearish reversals on December 6th and December 8th, the market has shown that there is significant overhead resistance above 680. The market is also showing signs of being oversold following the recent runup, which adds upward resistance and could add pressure if the market continues lower. Below the market, initial support comes in near 630, with further support remaining around 595 and 575.

Action Plan: Mpls Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Mpls Wheat Action Plan Summary

- No new action is currently recommended for the 2023 New Crop. Following last July’s rally, the market has slowly stair-stepped lower, primarily due to low world wheat prices, weak US export demand, and managed fund selling. With the funds building a record large short position as the market sold off. Since weak US export demand remains the main impediment to higher prices, the market continues to be at risk of further downside erosion. The record large fund short position could fuel a rally back higher if a bullish catalyst enters the scene, and if that happens, it may signal that a near-term low is in place. Earlier this year, Grain Market Insider made a sales recommendation during the July rally near 820, and with that sale in place, Grain Market Insider’s strategy is to look for price appreciation this winter with an eye on considering additional sales around 725 – 775, and again north of 800. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

- No new action is recommended for 2024 Minneapolis wheat. At the end of August, the Sept ’24 contract traded to a peak of 871 ¾ and has continued to slowly stair-step lower, largely driven by lower world wheat prices, weak US export demand, and managed fund selling, and as the selloff progressed, the funds built up a record large short position. While bearish headwinds remain, the significant oversold condition of the market and the large fund net short position are two factors that could fuel a short-covering rally in the months ahead. Price seasonals are also supportive as prices tend to build in some risk premium going into the winter months. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside following a 1-year range breakout in KC wheat. Though recently, as the KC market extended further into oversold territory and the July ‘24 KC wheat contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. While in the same time frame, Grain Market Insider also recommended making an additional sale as the Sept ’24 Minneapolis contract broke long time 743 support. For now, moving forward, Grain Market Insider is prepared to recommend exiting the last 25% of the open puts on any further supportive market developments.

- No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

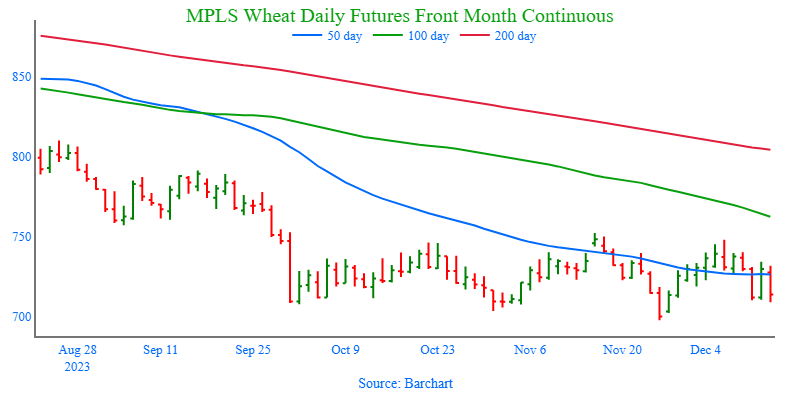

Above: After making a new contract low on November 27, the March contract found buying interest from its oversold status and record fund short. Since then, the market posted a bearish reversal on December 6, showing significant resistance in the 750 area. If prices can break through upside resistance, they could run toward 790. If prices retreat, nearby support could be found around 718, with further support near the recent low of 697 ½.

Other Charts / Weather