12-08 End of Day: Fresh Chinese Purchases Fail to Support as Markets Fade Following USDA Report

All prices as of 2:00 pm Central Time

| Corn | ||

| MAR ’24 | 485.5 | -2.5 |

| JUL ’24 | 506 | -2 |

| DEC ’24 | 512.5 | -0.75 |

| Soybeans | ||

| JAN ’24 | 1304 | -7.75 |

| MAR ’24 | 1323 | -7.25 |

| NOV ’24 | 1270.5 | -4 |

| Chicago Wheat | ||

| MAR ’24 | 631.75 | -10.5 |

| MAY ’24 | 640.5 | -9 |

| JUL ’24 | 645.5 | -7.5 |

| K.C. Wheat | ||

| MAR ’24 | 661 | -6.5 |

| MAY ’24 | 666.5 | -3 |

| JUL ’24 | 669.75 | -0.75 |

| Mpls Wheat | ||

| MAR ’24 | 729.5 | -7.75 |

| JUL ’24 | 745.75 | -9 |

| SEP ’24 | 753.25 | -9.25 |

| S&P 500 | ||

| MAR ’24 | 4663 | 22.5 |

| Crude Oil | ||

| FEB ’24 | 71.42 | 1.83 |

| Gold | ||

| FEB ’24 | 2016.4 | -30 |

Grain Market Highlights

- Following quiet overnight trade that was higher, the corn market faded lower into the close following the release of today’s USDA WASDE update that showed only a minor 25 mb reduction to 23/24 ending stocks by raising export demand by the same amount.

- Markets sold off, giving up earlier gains as the USDA left the soybean complex’s supply/demand numbers unchanged across all three commodities, and increased global stocks above expectations by 1.5 mmt in today’s update.

- Despite the report of another Chinese purchase of SRW and the USDA’s reduction of wheat ending stocks by 25 mb, the wheat complex sold off as world wheat production was raised by 1 mmt and traders took profits from the recent rally.

- US employment data that was released this morning came in better than expected. The unemployment rate came in at 3.7% versus 3.9% expected and rallied the US dollar, possibly adding some resistance to grain markets.

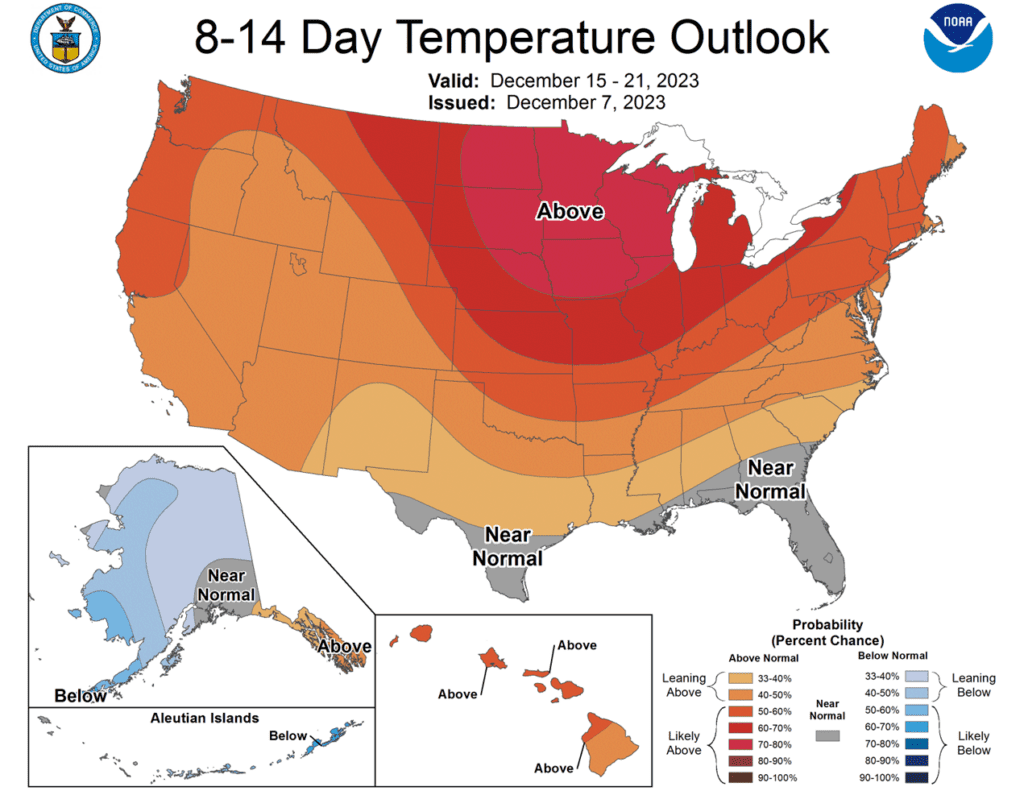

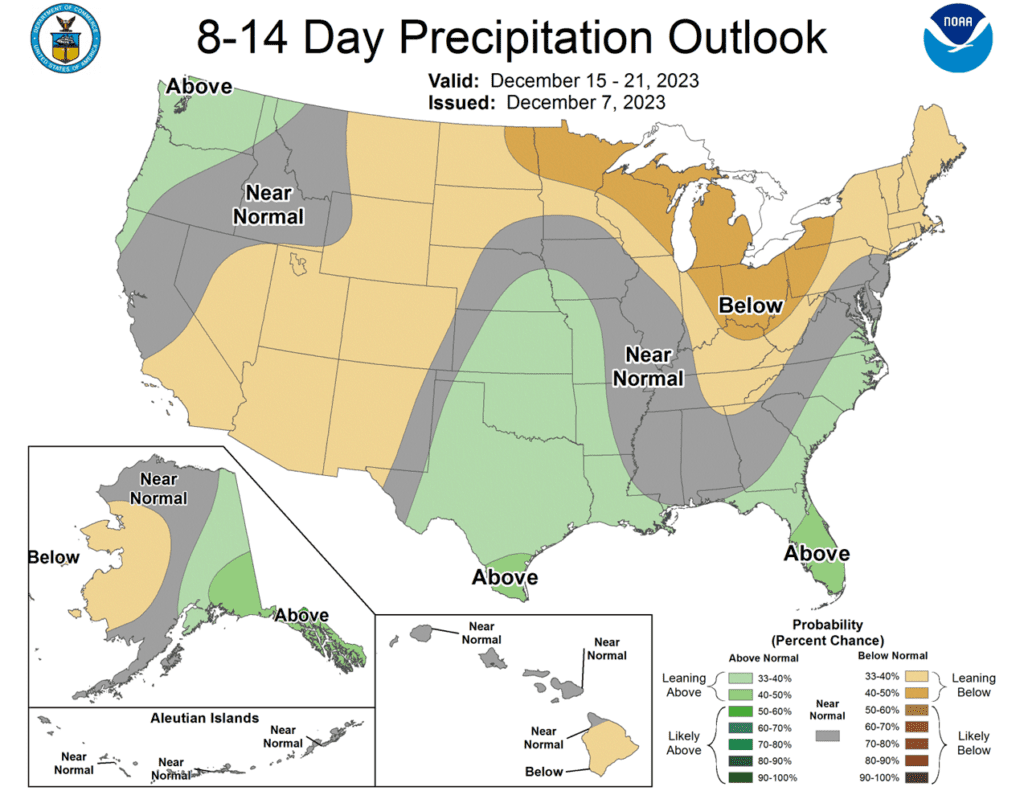

- To see the updated US 8 – 14 da temperature and precipitation outlooks, and South America’s 1 week total accumulated precipitation, the National Weather Service, and Climate Prediction Center, scroll down to other Charts/Weather Section.

- CORN ACTION PLAN SUMMARY (approximately 3 bullet points)

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Corn Action Plan Summary

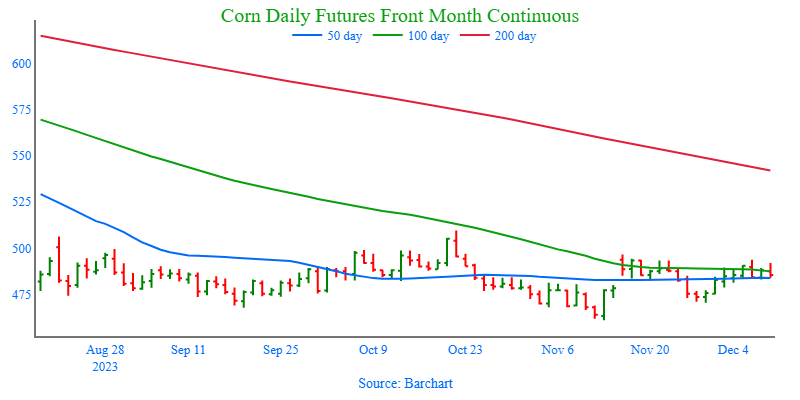

- No new action is recommended for 2023 corn. Since the beginning of August, the corn market has traded sideways largely between 470 and 500. October’s brief breakout to 509 ½ and the subsequent failure to stay above the 50-day moving average indicates there is significant resistance in that price range. The failure of December’s USDA report to provide a bullish influence on the market puts the market at risk of drifting sideways to lower without a bullish catalyst. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. For now, Grain Market Insider will continue to hold tight on any further sales recommendations for the next few weeks with the objective of seeking out better pricing opportunities. If the market has not turned around by then, Grain Market Insider may sit tight on the next sales recommendations until spring.

- No new action is recommended for 2024 corn. Since late February ’22, Dec ’24 has been bound by 485 ¾ on the bottom and 602 on the top. After testing 491 to 547 last July, it has mostly traded between 500 and 525. During this time, Dec ’24 has held up better as bear spreading has allowed Dec ’24 to maintain more of its value versus old crop prices as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Moving forward, the risk for 2024 prices is the same as for 2023 prices, which is a continuation of a sideways to lower trend without a bullish catalyst. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying Dec ‘23 560 and 610 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

- No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

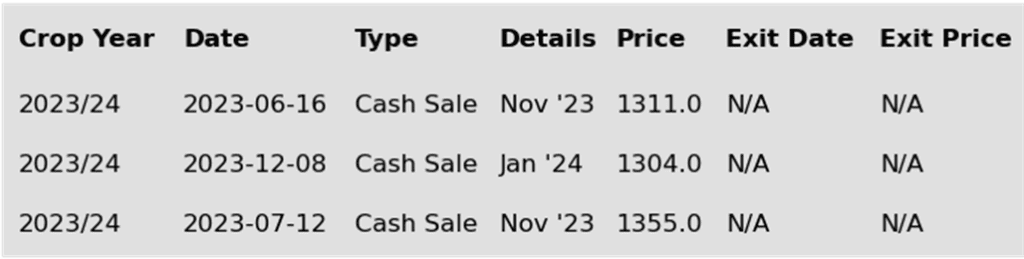

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn prices faded from the highs after the USDA report. Additional purchases by China of wheat and soybeans, and a corn sale to “Unknown destinations” helped support the market early in the session, but prices faded after the USDA report’s release. March corn lost 2 ¼ cents on the day, but finished ¾ cents higher on the week.

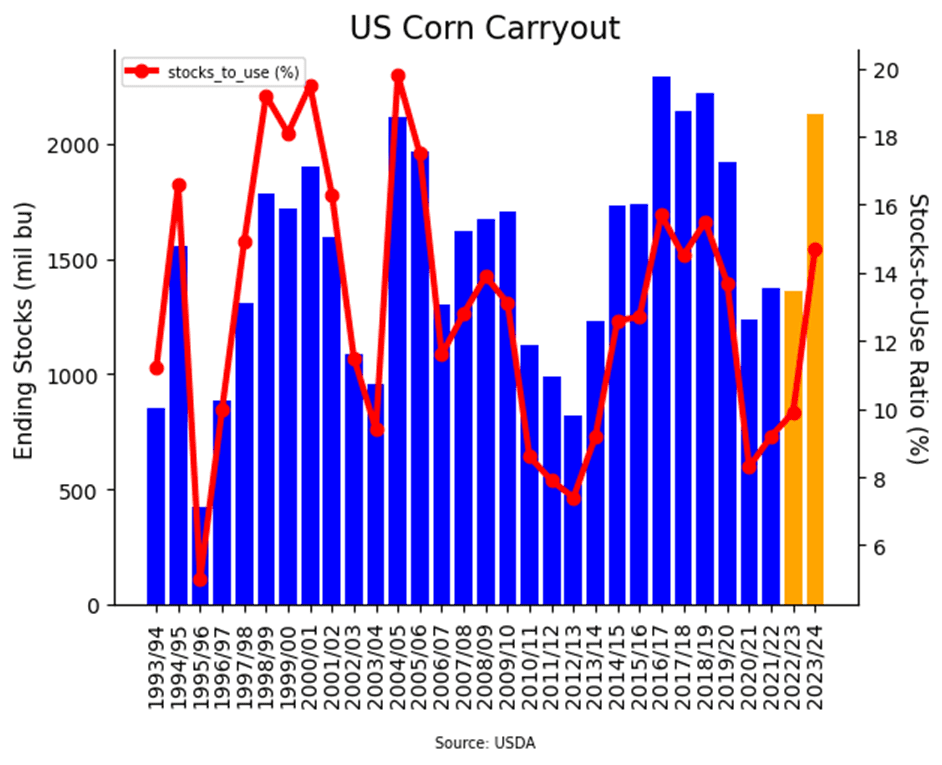

- The USDA raised export projections by 25 mb to 2.100 billion bushels for the marketing year in the USDA WASDE report on Friday morning. The USDA cited recent strength in export demand as the rationale. This lowered projected carryout to 2.131 billion bushels for ending stock for the 23/24 marketing year, below analyst expectations.

- The slip in prices moved March futures back to the key support level of 485. March futures have traded around this price point the past six sessions and have consistently been in this area since the start of November.

- The USDA announced a private exporter sale of corn to Unknown Destination for 6.5 mb for the 23/24 marketing year this morning. The export sales help support overnight and morning corn prices.

- In the WASDE report, USDA left Brazil and Argentina corn production unchanged from their November projections, taking a “wait and see” approach to the corn crops. On Thursday, CONAB estimated Brazil’s total corn crop for 23/24 at 118.53 mmt, down from previous estimates of 119.02 mmt. The USDA is forecasting a crop of 129 mmt.

Above: Since the lead month rolled to the March contract, the corn market has been rangebound between 470 on the downside and 497 on the upside. Upside resistance appears to be heavy given the bearish reversal that was posted on December 6. That heavy resistance also extends up to the October high of 509 ½, which the market will need more bullish influence to trade through. If the market retreats through nearby 470 support, major support remains near 460.

Soybeans

Action Plan: Soybeans

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

New Alert

Sell JAN ’24 Cash

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Soybeans Action Plan Summary

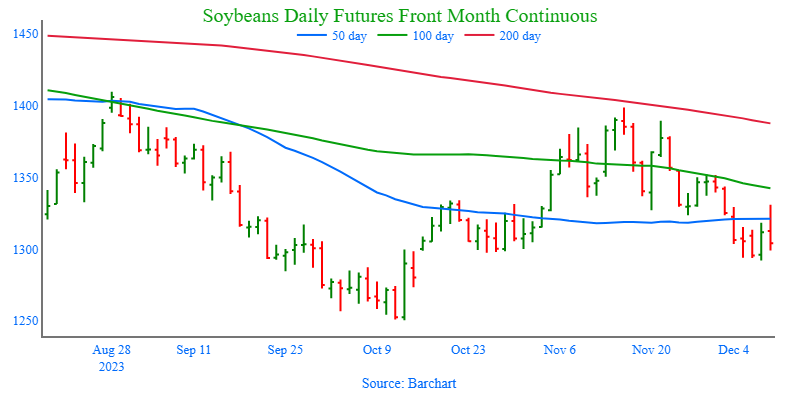

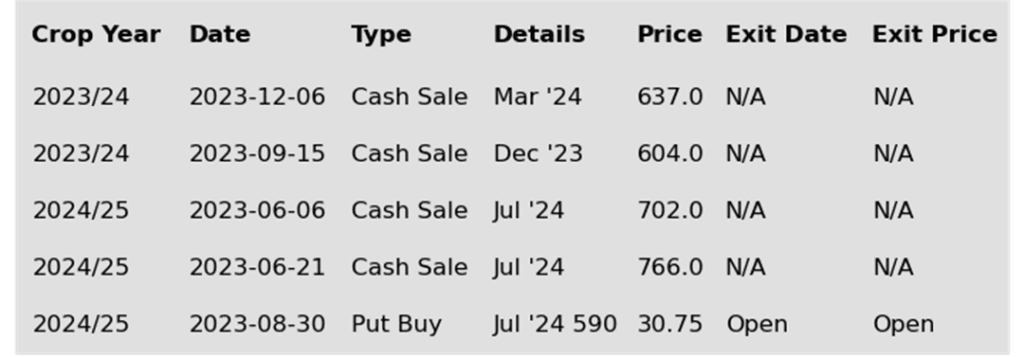

- Grain Market Insider recommends selling a portion of your old crop 2023 soybean production. Since last summer, the soybean market has been mostly rangebound between 1435 on the topside and 1251 on the bottom. Within this range, the 1330 area has been a strong pivot point. Getting over 1330 the front month has been able to challenge the 1400 area, but below 1330 the front month has challenged the 1250 area. Today, the January contract attempted to get back over 1330, with an intraday high of 1330 ¾, but was rejected. This rejection poses the risk that the front month could challenge the 1250 area again. Also, given the projected record large global carryout of soybeans, Grain Market Insider wants to take advantage of the historical value of 1300+ soybean prices.

- No action is recommended for the 2024 crop. Since the inception of the Nov ’24 contract, it has traded at a discount to the 2023 crop from as much as 142 back in July, to as little as 17 ¾ in early October during harvest. While the spread difference between the two crops has seen a good amount of volatility, Nov ’24 has been largely rangebound between 1250 and 1320 since it rallied off its 1116 ¼ low last May. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the earliest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

- No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day lower following today’s lackluster WASDE report, which saw very few changes from last month’s report. Both soybean meal and oil ended the day lower as well, with larger losses in soybean oil.

- For the week, January soybeans lost 21 cents, January soybean meal lost 8.0 dollars, and January soybean oil lost 1.25 cents. This comes as non-commercials have been exiting a portion of their net long positions with improvements in South American weather.

- In today’s USDA report, US ending stocks were unchanged at 245 mb, which was mostly in line with expectations. World ending stocks were reduced slightly, Argentinian soybean production was unchanged at 48.0 mmt, and Brazilian soybean production was reduced to 161.0 mmt from 163.0 mmt.

- This morning, the USDA reported a private exporter sale of 136,000 metric tons of soybeans for delivery to China during the 23/24 marketing year.

Above: Since retreating from the November highs, soybeans have traded back through the 50-day moving average and 1297 support. Currently, the trend is lower, but the market shows signs of being oversold, which can be supportive if prices turn back higher. For now, support below the market remains near 1250, with nearby resistance near the 50-day moving average, around 1320, and again near 1352.

Wheat

Market Notes: Wheat

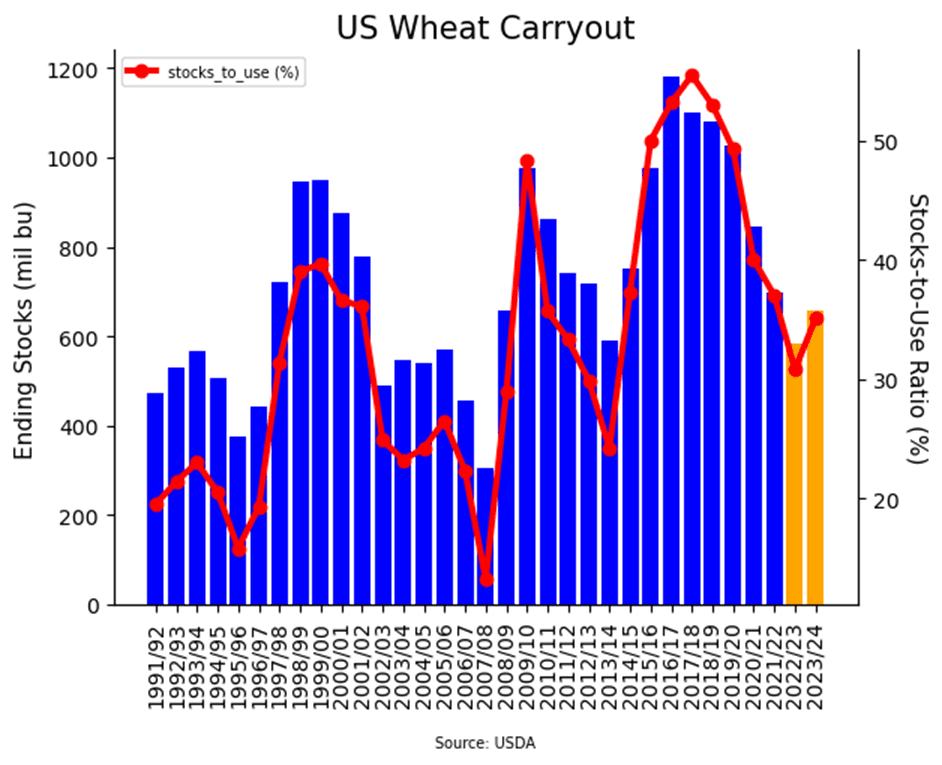

- Wheat closed lower in all three US classes today after a relatively neutral WASDE report. The US 23/24 wheat ending stocks number was lowered to 658 mb, versus 684 mb last month. The world carryout came in at 258.2 mmt, compared to 258.7 in November.

- US wheat exports were raised 25 mb from last month’s estimate, now at 725 mb for 23/24. The negativity at the close may be a reflection of a higher world production number though, at 783.01 mmt versus 781.98 mmt last month. With the recent run higher, profit taking was also a likely culprit.

- Aside from today’s USDA report, there was also another announced sale of US wheat to China for the 23/24 marketing year, this time for 110,000 mt. Despite a lower close today, if these purchases continue, it will lend support to the market. On the other hand, rain forecasted for the US southern Plains next week may keep upside potential limited for now.

- Egypt’s most recent wheat tender for 420,000 mt was fulfilled by Russia at $260 per mt FOB. France’s offer at $268 was the next cheapest, with Romania following them. Given the competition, it is a bit surprising, albeit welcome, that China is purchasing US wheat.

- Today’s Jobs report indicated that the US added 199,000 jobs, and unemployment has fallen to 3.7%. This has the US Dollar Index higher, which may also have contributed to the negative close in wheat. Additionally, this may mean that the Federal Reserve sticks with their plan to have higher interest rates for longer; this may continue to affect commodity prices down the road.

- From a global perspective, as of the July 1, the beginning of their marketing year, Ukraine’s total grain harvest has reached 57.6 mmt. Of that total, 22.5 mmt is wheat, which is said to be up 16% year on year. Over in France, winter wheat planting is 89% complete as of December 4. Typically, they are done by the end of November, but significant rain delays were present this year. Additionally, 77% of the French crop is reported to be in good to excellent condition.

Action Plan: Chicago Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

Active

Sell MAR ’24 Cash

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Chicago Wheat Action Plan Summary

- Grain Market Insider sees an active opportunity to sell a portion of your 2023 Soft Red Winter wheat crop. Since the end of July, the wheat market has been in a downtrend due to low world wheat prices generating weak US export demand, with no significant rallies to take advantage of. This current rally has now taken prices in excess of 80 cents from the November low and coincides with a 38% retracement back toward last July’s highs, and the 612 to 646 congestion area from last September. Considering this bounce in the market may be temporary, Grain Market Insider recommends taking advantage of this rally, and these still historically good prices, to make an additional sale on your 2023 crop.

- No new action is recommended for 2024 Chicago wheat. Since July, new crop Chicago wheat has slowly worked its way lower with no significant opportunities to make additional sales. The lower market was driven mostly by managed fund selling from lower world wheat prices and weak US demand. As the market sold off, it became significantly oversold with managed funds building a short position in excess of 100,000 contracts. While bearish headwinds remain, the large fund short position and oversold condition of the market are two factors that could fuel a sizeable, short-covering rally. Additionally, price seasonals are supportive as prices tend to build in some risk premium going into the winter months. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for further price erosion, and back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset much of the original cost and move toward a net neutral cost for the remaining position.

- No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: Short covering and a seasonal build up of weather premium has driven Chicago wheat through the late August highs and may be on track to test the next level of resistance between 660 and 665 left in early August. The market shows signs of being overbought and could retreat. If it does, support may come in around 605 – 600, and again near the 50-day moving average near 575.

Action Plan: KC Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

KC Wheat Action Plan Summary

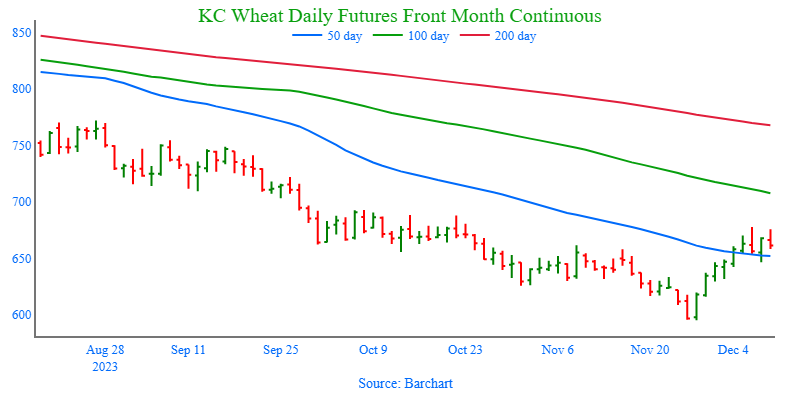

- No new action is recommended for 2023 KC wheat crop. Since late July old crop KC wheat has been in a downtrend that has largely been driven by managed fund selling on low world wheat prices and weak US export demand. As the selloff progressed, the market became oversold, and the funds established the largest short position in three years. Even though bullish headwinds remain, these two factors have fueled the recent short-covering rally, which could extend much further if a bullish catalyst enters the market. This would also line up with the historical tendency for price appreciation as the market builds risk premium going into wintertime. Grain Market Insider’s strategy is to look for price appreciation going into this winter, as weather becomes a more prominent market mover and may consider suggesting additional sales if prices become over extended.

- No new action is recommended for 2024 KC wheat. At the end of August, the Jul ’24 contract broke out of roughly a one-year trading range, between 740 and 860, to the downside. Since that breakout, the market has continued to slowly stair-step lower, largely driven by managed fund selling, weak US export demand, and lower world wheat prices. As the selloff progressed, the funds built up the largest net short position in three years. While bearish headwinds remain, the significant oversold condition of the market and the large fund net short position are two factors that could fuel a short-covering rally in the months ahead. Price seasonals are also supportive as prices tend to build in some risk premium going into the winter months. Back in August, Grain Market Insider recommended buying Jul’24 KC wheat 660 puts to protect the downside following the range breakout. Though as the market recently got further extended into oversold territory and the July contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. Moving forward, Grain Market Insider is prepared to recommend exiting the last 25% on any further supportive market developments.

- No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

Above: Since the end of November, the wheat market has rallied largely on short covering activity from being extremely oversold. The market is now showing signs of being overbought and has posted a bearish reversal, though it’s close above the 50-day moving average suggests that there could still be more strength in the market. If not, and prices retreat below the 50-day moving average, support below the market may come in between 595 and 575.

Action Plan: Mpls Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Mpls Wheat Action Plan Summary

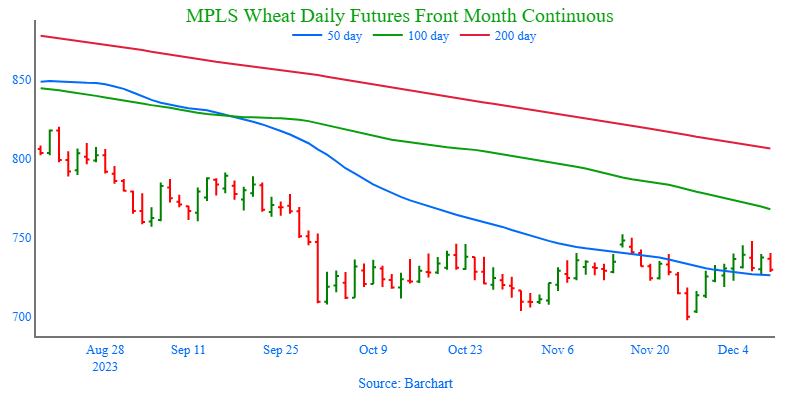

- No new action is currently recommended for the 2023 New Crop. Following last July’s rally, the market has slowly stair-stepped lower, primarily due to low world wheat prices, weak US export demand, and managed fund selling. With the funds building a record large short position as the market sold off. Since weak US export demand remains the main impediment to higher prices, the market continues to be at risk of further downside erosion. The record large fund short position could fuel a rally back higher if a bullish catalyst enters the scene, and if that happens, it may signal that a near-term low is in place. Earlier this year, Grain Market Insider made a sales recommendation during the July rally near 820, and with that sale in place, Grain Market Insider’s strategy is to look for price appreciation this winter with an eye on considering additional sales around 725 – 775, and again north of 800. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

- No new action is recommended for 2024 Minneapolis wheat. At the end of August, the Sept ’24 contract traded to a peak of 871 ¾ and has continued to slowly stair-step lower, largely driven by lower world wheat prices, weak US export demand, and managed fund selling, and as the selloff progressed, the funds built up a record large short position. While bearish headwinds remain, the significant oversold condition of the market and the large fund net short position are two factors that could fuel a short-covering rally in the months ahead. Price seasonals are also supportive as prices tend to build in some risk premium going into the winter months. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside following a 1-year range breakout in KC wheat. Though recently, as the KC market extended further into oversold territory and the July ‘24 KC wheat contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. While in the same time frame, Grain Market Insider also recommended making an additional sale as the Sept ’24 Minneapolis contract broke long time 743 support. For now, moving forward, Grain Market Insider is prepared to recommend exiting the last 25% of the open puts on any further supportive market developments.

- No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: After making a new contract low on November 27, the March contract found buying interest from its oversold status and record fund short. Since then, the market posted a bearish reversal on December 6, showing significant resistance in the 750 area. If prices can break through upside resistance, they could run toward 790. If prices retreat, nearby support could be found around 718, with further support near the recent low of 697 ½.

Other Charts / Weather

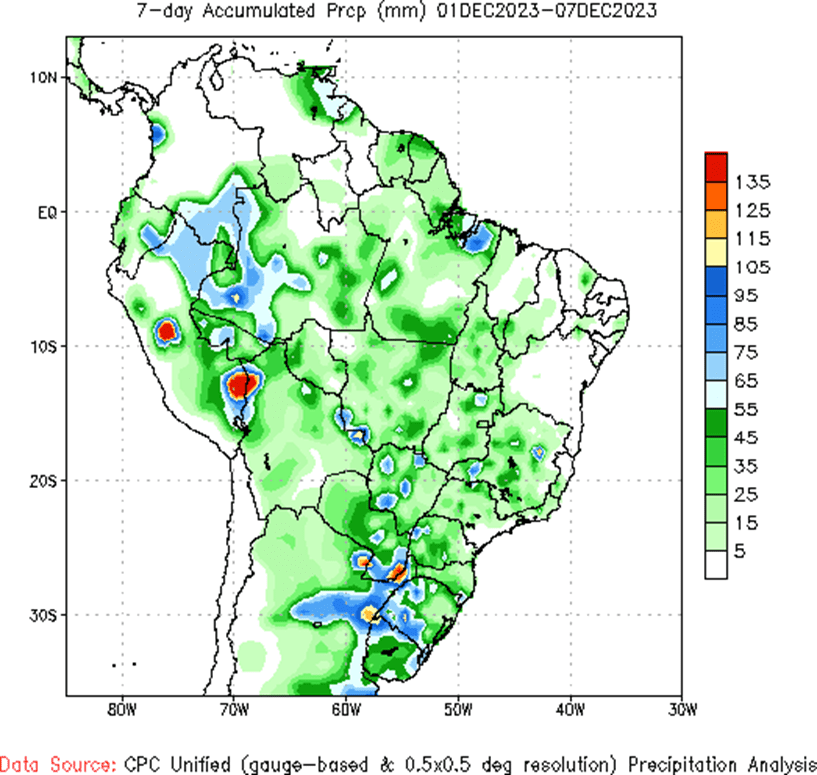

Brazil 7 day total accumulated precipitation courtesy of the National Weather Service, Climate Prediction Center.

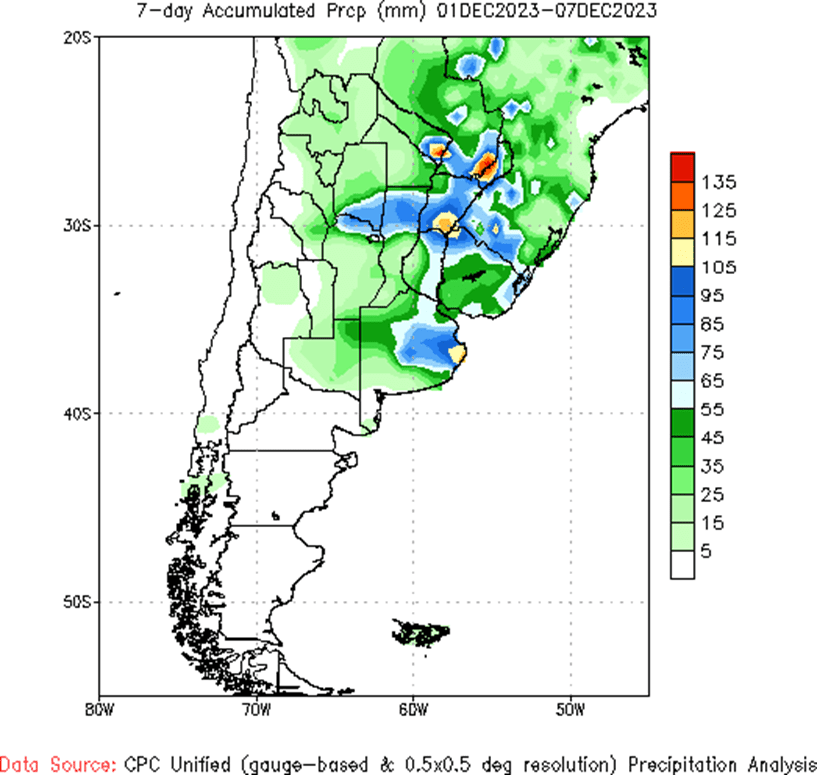

Argentina 7 day total accumulated precipitation courtesy of the National Weather Service, Climate Prediction Center.