11-8 End of Day: Corn and Beans Settle Higher Following Today’s USDA Report; Wheat Mostly Lower

All prices as of 2:00 pm Central Time

| Corn | ||

| DEC ’24 | 431 | 3.5 |

| MAR ’25 | 444.25 | 3.75 |

| DEC ’25 | 449 | 2 |

| Soybeans | ||

| JAN ’25 | 1030.25 | 4 |

| MAR ’25 | 1043.5 | 6 |

| NOV ’25 | 1052.5 | 3.75 |

| Chicago Wheat | ||

| DEC ’24 | 572.5 | 1 |

| MAR ’25 | 587.5 | -1.5 |

| JUL ’25 | 605 | -0.5 |

| K.C. Wheat | ||

| DEC ’24 | 564.25 | -4.75 |

| MAR ’25 | 577.5 | -4 |

| JUL ’25 | 595.5 | -3.25 |

| Mpls Wheat | ||

| DEC ’24 | 602.5 | -3 |

| MAR ’25 | 623.75 | -3.75 |

| SEP ’25 | 651 | -2 |

| S&P 500 | ||

| DEC ’24 | 6035.75 | 32 |

| Crude Oil | ||

| JAN ’25 | 70.11 | -1.85 |

| Gold | ||

| JAN ’25 | 2704.7 | -13.5 |

Grain Market Highlights

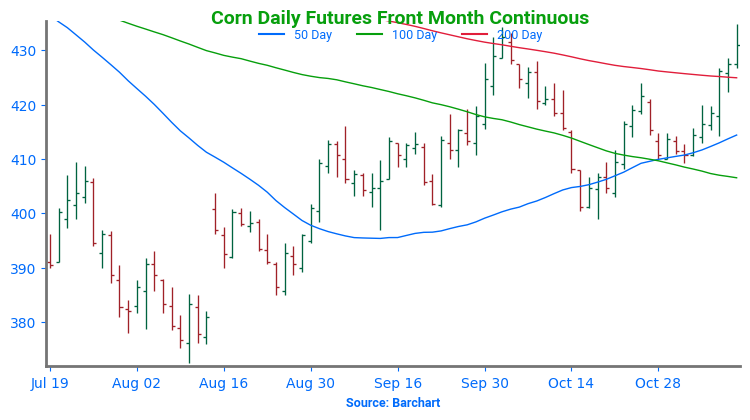

- Corn futures continued their climb today for the sixth consecutive day, with help from friendly yield numbers from the USDA and continued strong demand. While December corn closed strong it failed to close above September’s high.

- Soybeans closed higher on the day with modest gains, despite briefly dipping below unchanged. Much lower-than-expected US soybean ending stocks lent support, along with a third consecutive day of gains in soybean oil. However, lower soybean meal weighed on beans, as it continued to consolidate and closed lower.

- The wheat complex closed mostly lower on the day, as all three classes remain in a sideways trend with little fresh bullish news to trade and a neutral USDA report that came in as expected.

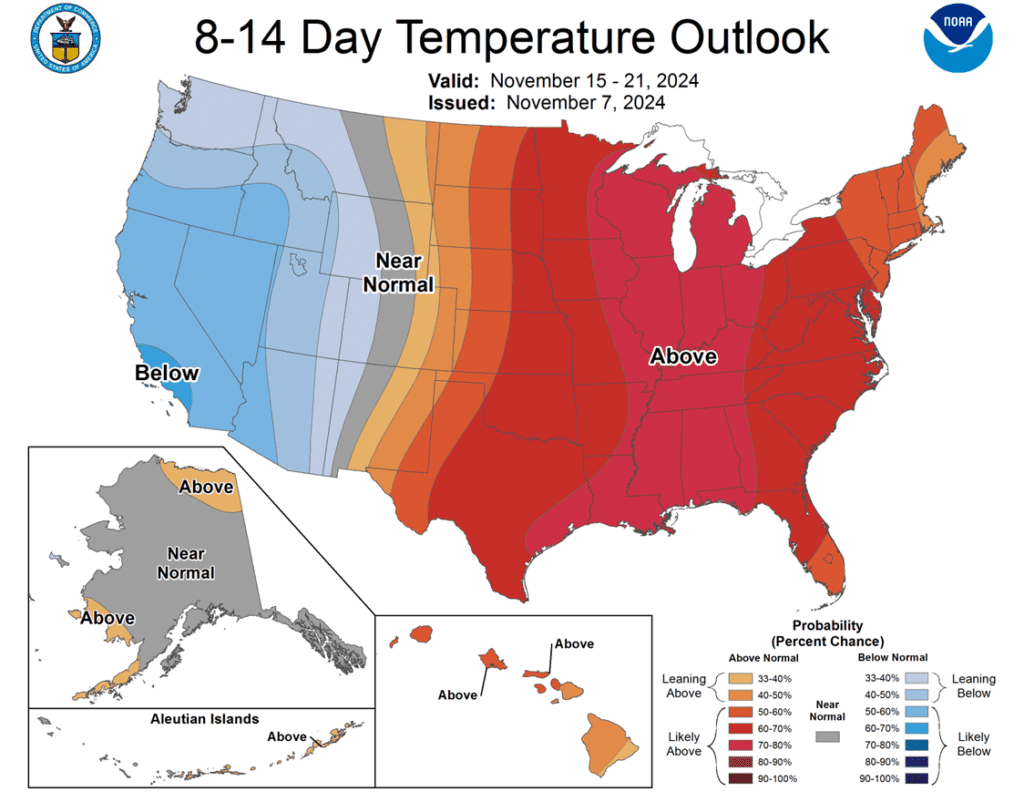

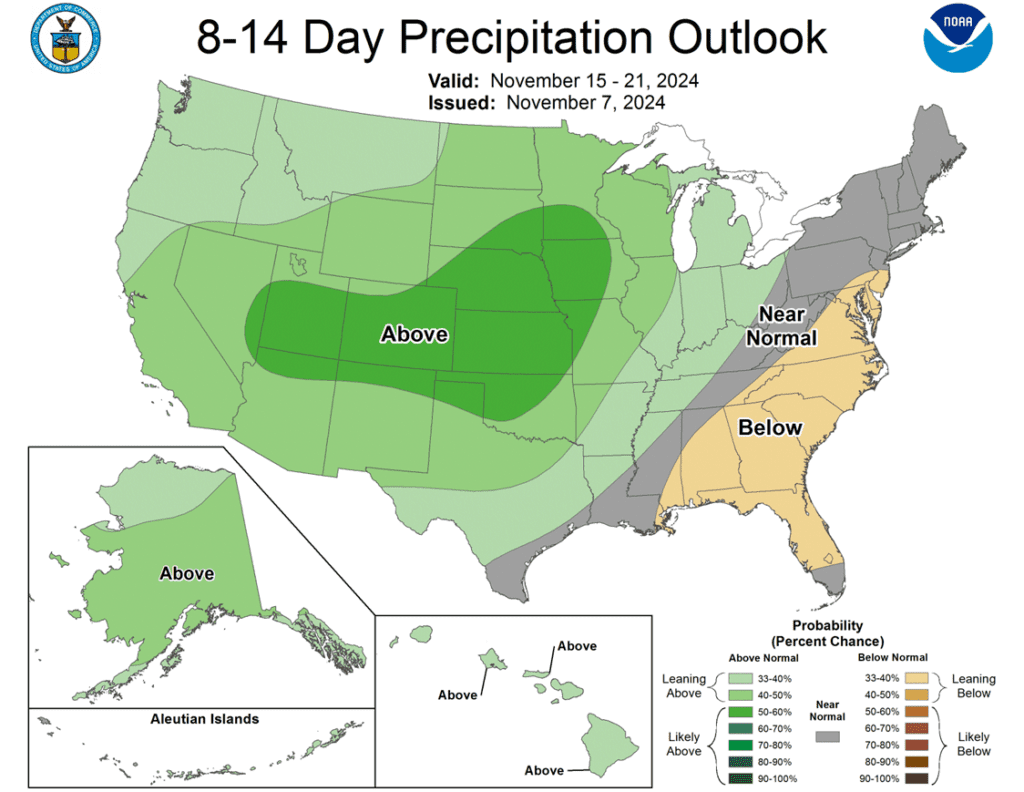

- To see updated US and South American temperature and precipitation forecasts, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Corn Action Plan Summary

- Grain Market Insider sees an opportunity for catch-up sales on a portion of your 2024 corn crop. The corn market has traded back towards the top of the 397 – 434 range that it has been in since September. If you missed any of our three previous sales recommendations from earlier in the season, this rally represents a good opportunity to begin to catch up.

- Catch-up sales opportunity for the 2025 crop. Between early June and late July Grain Market Insider made three separate sales recommendations to get early sales made for next year’s crop. If you happened to miss those opportunities and are looking to make additional early sales for next year, you could consider targeting the 455 – 475 area versus Dec ’25 to take advantage of any post-harvest strength. For now, considering the seasonal weakness of the market around harvest time, we will not be posting any targeted areas for new sales until late fall or early winte. Although we are targeting the 470 – 490 area to buy upside calls to protect current sales in case the market experiences an extended rally beyond that point.

- No Action is currently recommended for 2026 corn. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

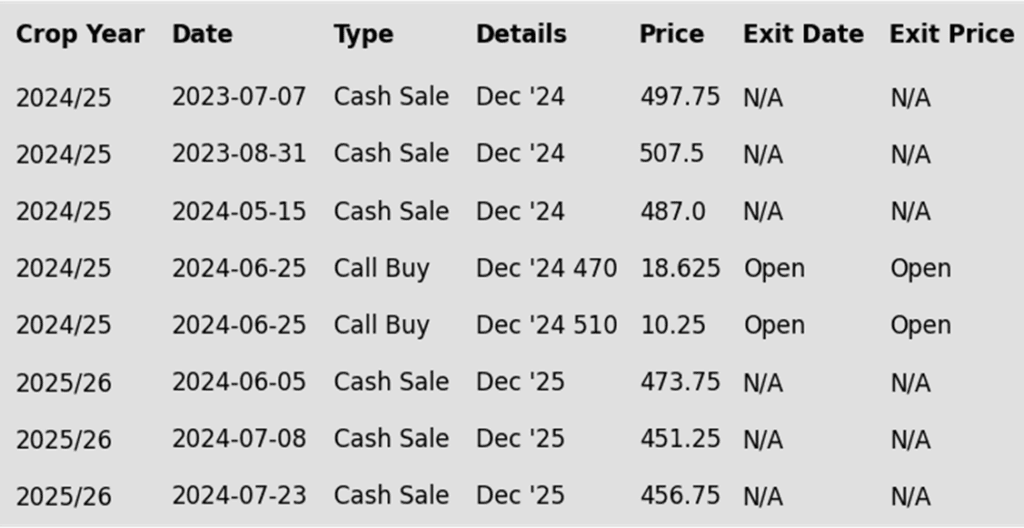

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn futures rose for the sixth consecutive day, driven by steady demand and a larger-than-expected reduction in corn yield in Friday’s USDA report. December corn ended the week up 16 ½ cents.

- Corn futures used a larger than expected cut in corn yield in Friday’s USDA report and consistent demand to push prices higher for the third consecutive day. For the week, December corn finished 16 ½ cents higher.

- The USDA lowered their projected corn yield by 0.7 bpa in Friday’s USDA crop production report to 183.1 bpa. The lower yield was a reflection of the dry weather at the end of the growing season and during harvest.

- Despite a good demand tone, the USDA left current demand projections unchanged given the early time of the marketing year. The reduced production lowered corn carryout projections to 1.938 billion bushels, which was slightly below analyst expectations and the fifth month in a row that carryout has declined.

- Positive gains in the commodity markets may have been limited on talk the President-elect Trump was asking Robert Lighthizer to resume his role as head of US trade policy. Robert Lighthizer is known for having a tough stance when working with China and a supporter of trade tariffs.

- On Friday, the USDA announced another flash corn sale of 200,480 mt (7.9 mb) to unknown destinations for the current marketing year.

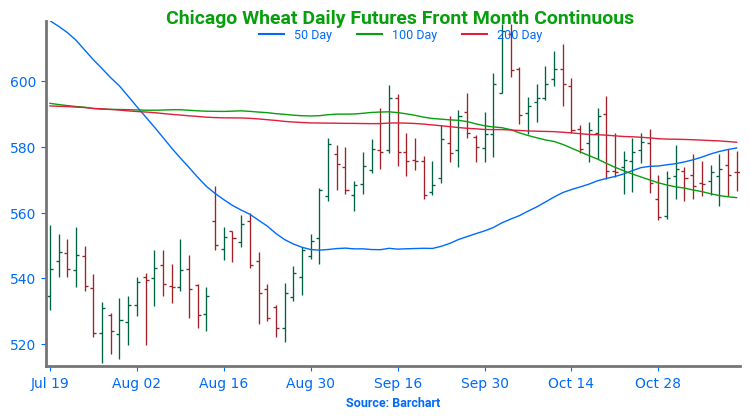

Above: December corn tested the October high and retreated, signaling resistance in that area. A breakout above this level set the market up for a move toward 475, with potential resistance between 450 and 455. Below the market, If prices retreat, support below the market may come in between 415 and 409.

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Soybeans Action Plan Summary

- Catch-up sales opportunity for the 2024 crop. If you missed any of our previous sales recommendations, there may still be an opportunity to make a catch-up sale. While we don’t expect the fall to offer the best pricing, a rally back to the 1050 – 1070 range versus Jan ‘25 could provide a good opportunity. For those with capital needs, consider making these catch-up sales into price strength. If the market rallies further, additional sales can be considered in the 1090 – 1125 range versus Jan ‘25. No further sales recommendations are anticipated until seasonal pricing opportunities improve, likely late fall to early spring.

- No Action is currently recommended for 2025 Soybeans. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be set in late fall or early winter at the earliest. Currently, our focus is on watching for opportunities to recommend buying call options. Should Nov ‘25 reach the upper 1100 range, the likelihood of an extended rally would increase, and we would recommend buying upside call options at that time in preparation for that possibility.

- No Action is currently recommended for 2026 Soybeans. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

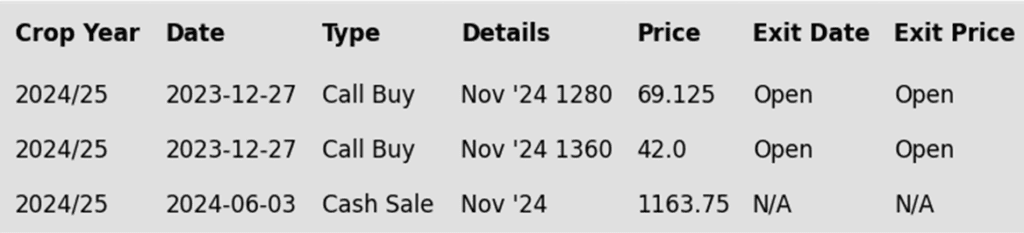

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

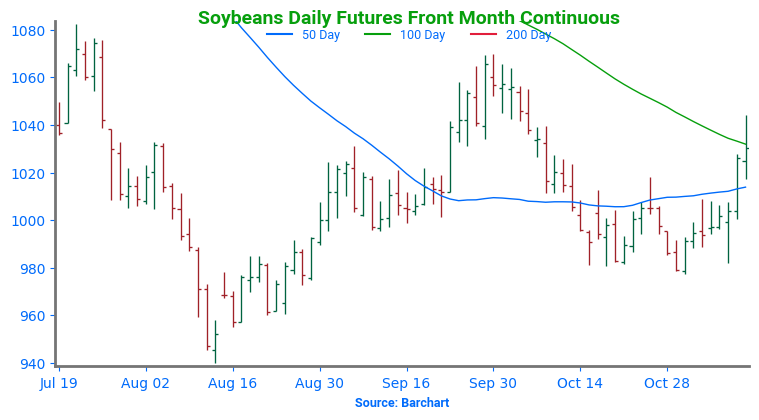

- Soybeans ended the day higher following a volatile day of trade. The WASDE report turned out to be friendly for soybeans, which saw gains of as much as 18 cents, but prices faded into negative territory before recovering into the close. Soybean meal and oil continued their opposing trends with meal lower and soybean oil higher.

- Today’s WASDE report saw soybean yields fall much more than expected to 51.7 bpa from 53.1 bpa last month. Total production fell to 4.461 billion bushels from 4.582 bb as a result, with 24/25 US ending stocks falling to 470 million bushels from 550 mb last month. Export demand was reduced by 25 mb despite strong recent export sales. World ending stocks were lowered as well and were below the lower range of analyst estimates.

- After the USDA report, January soybeans rallied up to their 100-day moving average for the first time the beginning of June. While the following pullback may have been technical, it coincided with the timing of Donald Trump asking protectionist Robert Lighthizer to run the US trade policy. Lighthizer has been tough on China which may have concerned traders today and brought caution to the rally.

- For the week, January soybeans gained 36 ½ cents to 1030 ¼ while new crop November 2025 gained 20 ¼ cents to 1052 ½. December soybean meal managed to gain $0.90 on the week, ending at $296.20 while December soybean oil gained 2.47 cents to 48.77 cents.

Above: The breakout above 1018 on Nov. 7, suggests the market has the potential to test the September highs near 1070. Before reaching that point, prices may encounter nearby resistance between 1044 and 1050. If prices retreat, initial support may be found near the 50-day moving average and again near 975.

Wheat

Market Notes: Wheat

- After a day of two-sided trade, wheat closed mixed in the Chicago contracts but posted losses across the board for Kansas City and Minneapolis. With little supportive news from the USDA and a rebound in the US Dollar index today, wheat had limited reasons to rally.

- Today’s WASDE report was generally neutral for wheat, as expected. US 24/25 ending stocks were raised slightly from 812 million bushels to 815 mb. Global 23/24 carryout was also increased a touch, from 266.2 million metric tons to 266.3 mmt. For 24/25, global carryout was reduced a tad from 257.7 mmt to 257.6 mmt. Additionally, US wheat production was unchanged at 1.971 billion bushels and exports were also untouched at 825 mb.

- According to the Buenos Aires Grain Exchange, Argentina’s wheat harvest is now 12.1% complete, an increase of 4.4% from a week ago. They left total production unchanged at 18.6 mmt, above today’s USDA estimate of 17.5 mmt, which was reduced from the October estimate of 18.0 mmt.

- The USDA did lower their Brazilian wheat production estimate in today’s report, from 9.0 mmt in October to 8.5 mmt today. However, analyst StoneX is even lower with their projection of 7.5 mmt, compared to their previous guess of 7.9 mmt.

- According to Russia’s prime minister, the country’s grain harvest has reached 128 mmt, with the total grain crop estimated at 130 mmt. The Russian agriculture minister also projected the 2024 wheat harvest at 83 mmt. However, today, the USDA estimated Russian wheat production slightly lower, at 81.5 mmt, with Russian wheat exports unchanged at 48 mmt.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Chicago Wheat Action Plan Summary

- No new action is recommended for 2024 Chicago wheat. Back in May, we recommended taking advantage of the elevated prices to make additional sales and buy upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Currently, our strategy remains to target 740 – 760 versus Dec ’24 to recommend further sales. While this range may seem far off, based on our research, it represents the potential opportunity that this crop year can present as we move into the planting and winter dormancy windows of the next crop cycle. Considering this potential, we also continue to target a selling price of about 73 cents in the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is recommended for 2025 Chicago wheat. In September, we recommended taking advantage of the rally in wheat to make additional sales on your anticipated 2025 SRW production. While we continue to recommend holding July ’25 620 puts — after advising to exit the first half back in July — to maintain downside coverage for any unsold bushels, our Plan A strategy is targeting the 650–680 area in July ’25 to suggest making additional sales. Should the market show signs of a potentially extended rally, our Plan B strategy is to protect current sales and target the 745 – 775 area to buy upside calls in case the market rallies significantly beyond that point.

- No action is currently recommended for 2026 Chicago Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

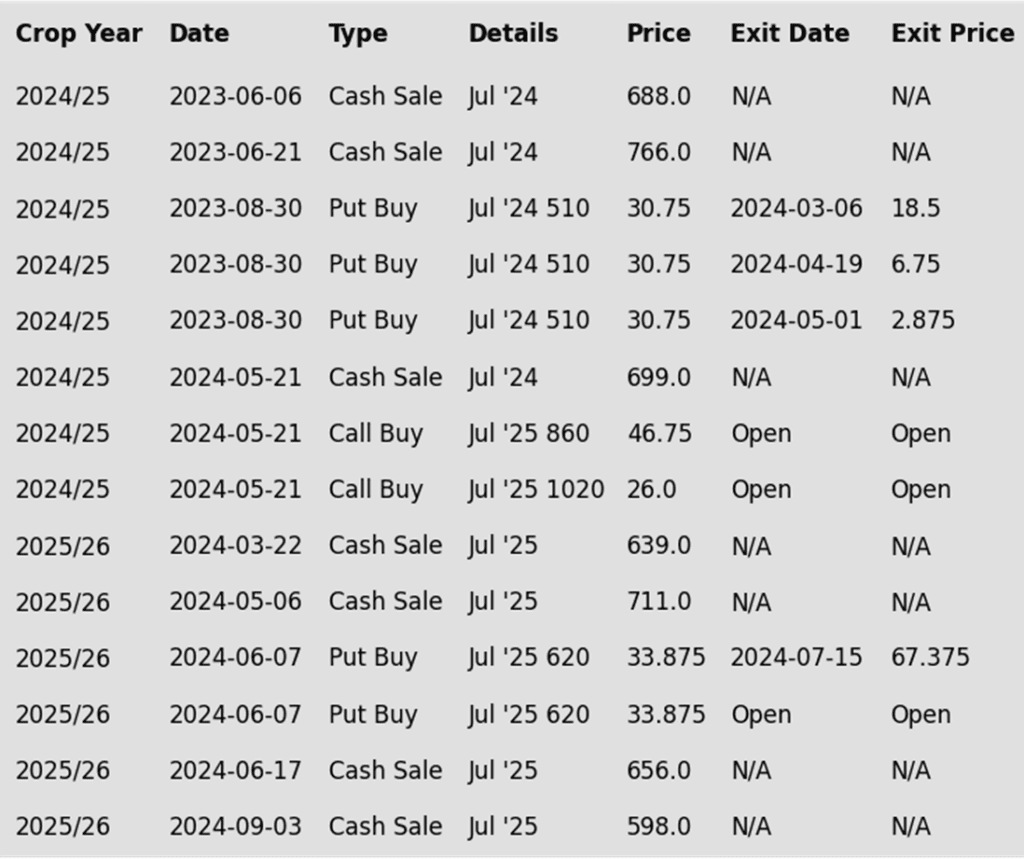

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: The swift turnaround on October 29 suggests initial support below the market may rest near 558. A close below this level could put the market at risk of trading down toward the 521 – 514 support area, with intermediate support possibly around 544. Initial resistance lies near 580 with more significant resistance around 595 – 600.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

KC Wheat Action Plan Summary

- No new action is recommended for 2024 KC wheat. Considering the upside breakout in KC wheat back in May, we recommended buying upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 635 – 660 versus Dec ’24 to recommend further sales, while also targeting a selling price of about 71 cents on the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is currently recommended for 2025 KC Wheat. While we still recommend holding the remaining half of the previously suggested July ’25 620 puts for downside protection on unsold bushels, considering the early October rally, we advised selling another portion of your anticipated 2025 HRW wheat production. Looking ahead, our current Plan A strategy is to target the 640 – 665 range for additional sales, while our Plan B strategies involve targeting the upper 400 range to exit half of the remaining 620 puts if the market turns toward new lows and targeting the 745–770 area to buy upside calls in case the market rallies significantly beyond that point.

- No action is currently recommended for 2026 KC Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

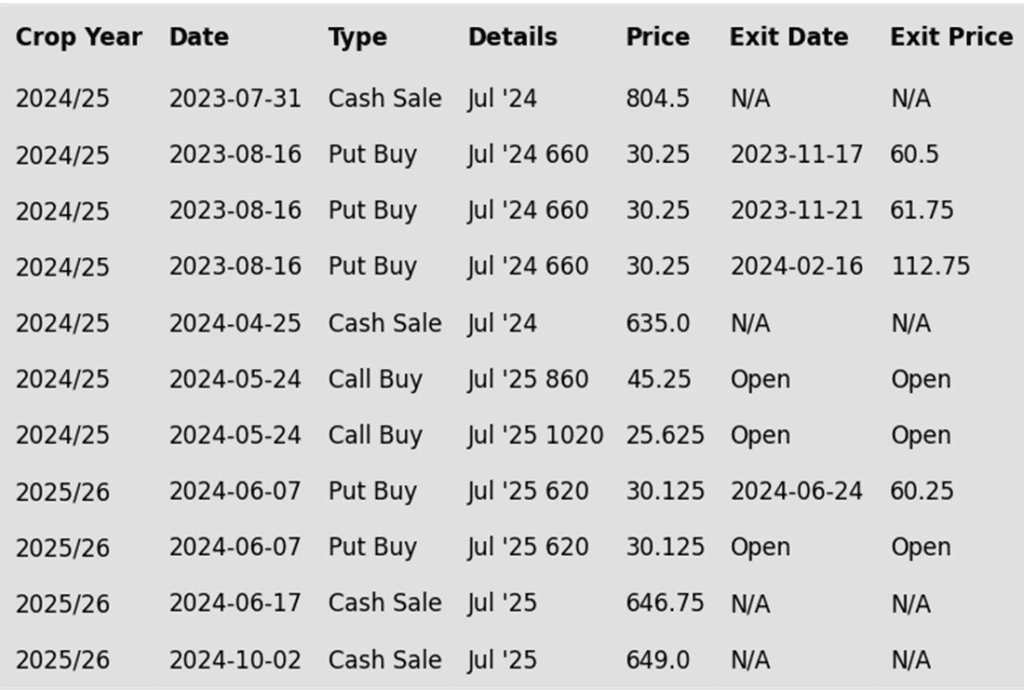

To date, Grain Market Insider has issued the following KC recommendations:

Above: The market has largely been sideways since rallying off 561 support on Oct. 29. A close above 583 could set the market up to rally toward the 593 – 603 resistance area around the 200-day moving average. Otherwise, a break below 561 could find minor support near 555, with major support around the August low of 527.

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Mpls Wheat Action Plan Summary

- No new action is recommended for 2024 Minneapolis wheat. Now that we are at the time of year when seasonal price trends tend to become more friendly, we are targeting the 630 – 655 range to recommend making additional sales. Additionally, given the amount of time that remains to market this crop, we will maintain the current July ’25 KC wheat 860 and 1020 call options. Our target is a selling price of about 71 cents for the 860 calls to achieve a net neutral cost on the remaining 1020 calls. These 1020 calls will continue to protect existing sales and provide confidence to make additional sales at higher prices.

- No new action is currently recommended for the 2025 Minneapolis wheat crop. Since the growing season can often yield some of the best sales opportunities, we made two separate sales recommendations in July to get some early sales on the books for next year’s crop. While we will not target any specific areas for additional sales until November or December, we continue to hold the remaining July ’25 KC 620 puts that were recommended in June for downside protection. To that end, we are currently targeting the upper 400 range versus July ’25 KC to exit half of those remaining puts. Additionally, should the wheat market show signs of an extended rally, we are targeting the 745–770 area in July ’25 KC to buy July ’25 KC upside calls in case the market rallies significantly beyond that point.

- No Action is currently recommended for the 2026 Minneapolis wheat crop. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

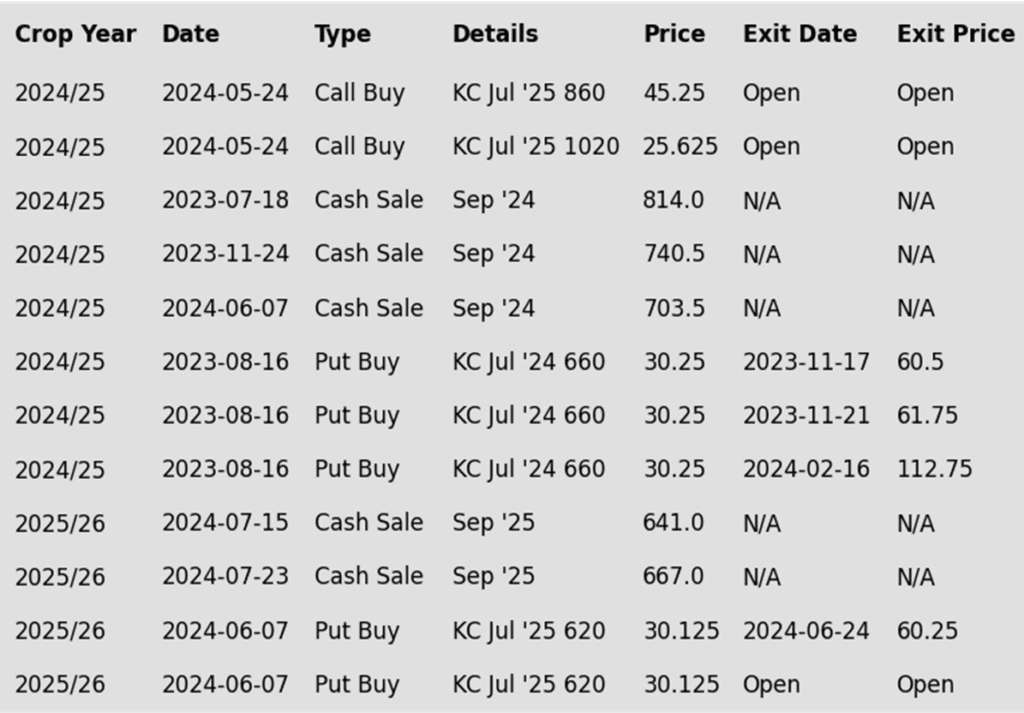

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

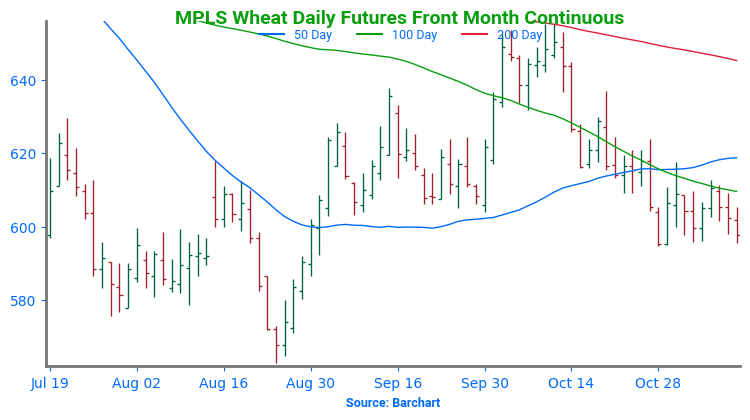

Above: Since late October Minneapolis wheat has mostly traded between 615 overhead and 595 down below. A close below 595 could lead to further weakness with prices trading towards the August low of 563, with potential support near 583. A rally above the 615 – 624 resistance area could set the market up for a rally towards the October highs with intermediate resistance near 637.

Other Charts / Weather

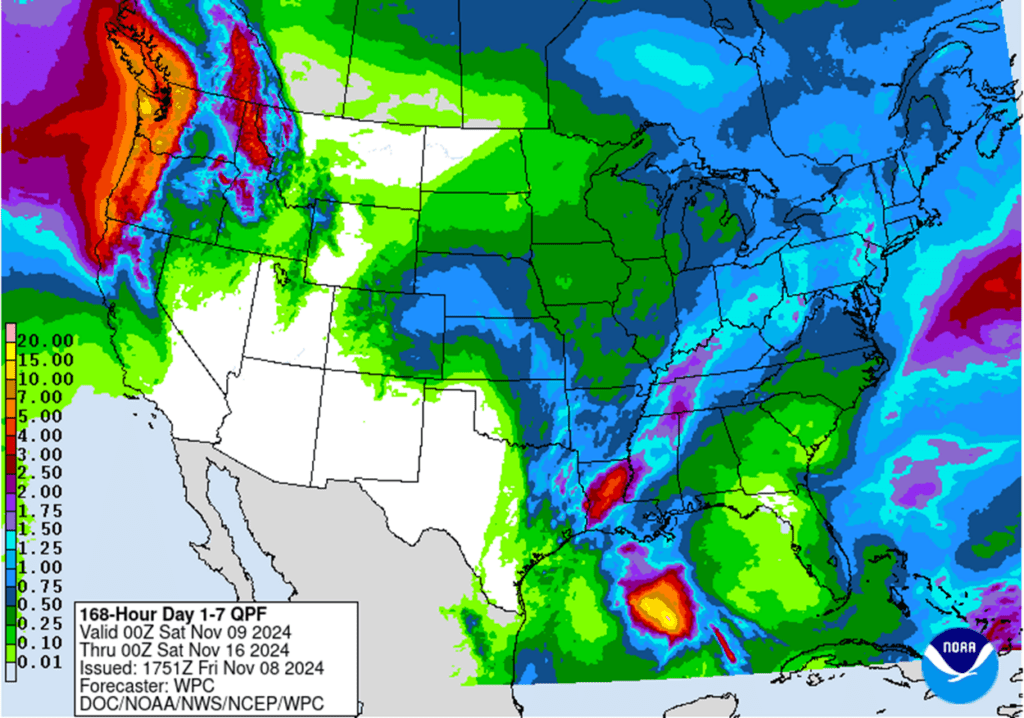

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

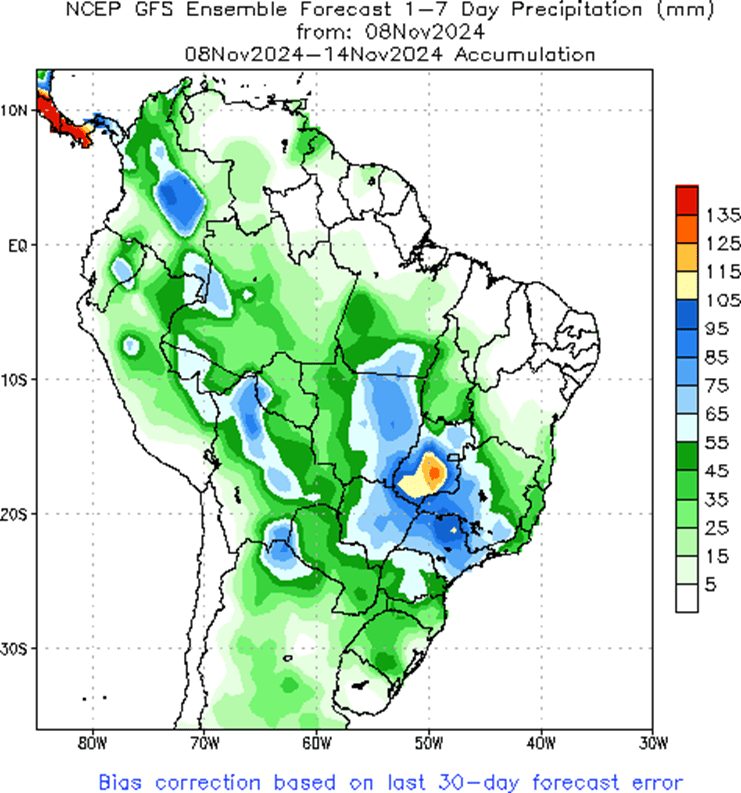

Brazil and N. Argentina 1-week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.