11-17 Markets Close the Week Softer in Anticipation of SA Rain

All prices as of 2:00 pm Central Time

| Corn | ||

| DEC ’23 | 467 | -7.75 |

| MAR ’24 | 485.25 | -8 |

| DEC ’24 | 511.5 | -4.25 |

| Soybeans | ||

| JAN ’24 | 1340.25 | -20 |

| MAR ’24 | 1356.5 | -18.5 |

| NOV ’24 | 1283.25 | -11.5 |

| Chicago Wheat | ||

| DEC ’23 | 550.75 | -2.75 |

| MAR ’24 | 575.75 | -5.25 |

| JUL ’24 | 605.75 | -4.25 |

| K.C. Wheat | ||

| DEC ’23 | 618 | -9.25 |

| MAR ’24 | 627.5 | -8.5 |

| JUL ’24 | 639 | -8.75 |

| Mpls Wheat | ||

| DEC ’23 | 715.5 | -10.5 |

| MAR ’24 | 731.75 | -8.75 |

| SEP ’24 | 755 | -9.25 |

| S&P 500 | ||

| DEC ’23 | 4531 | 7.75 |

| Crude Oil | ||

| JAN ’24 | 75.95 | 2.86 |

| Gold | ||

| JAN ’24 | 1993 | -4.7 |

Grain Market Highlights

- After giving up yesterday’s gains, the corn market settled lower on the day alongside soybeans and wheat, as the markets extract weather premium on the prospect of beneficial rainfall in Brazil.

- For the third day in a row, soybeans settled in the red as beneficial weather in Argentina may increase soybean plantings, and Brazil continues to see forecasts for much needed rainfall for its soybean crop.

- Soybean meal and oil once again settled in opposite directions, with lower meal outweighing the gains in bean oil in influence on soybeans.

- Despite cuts to Argentina’s wheat crop, the wheat complex continued its slide southward, as weakness from neighboring corn and beans weighed on prices.

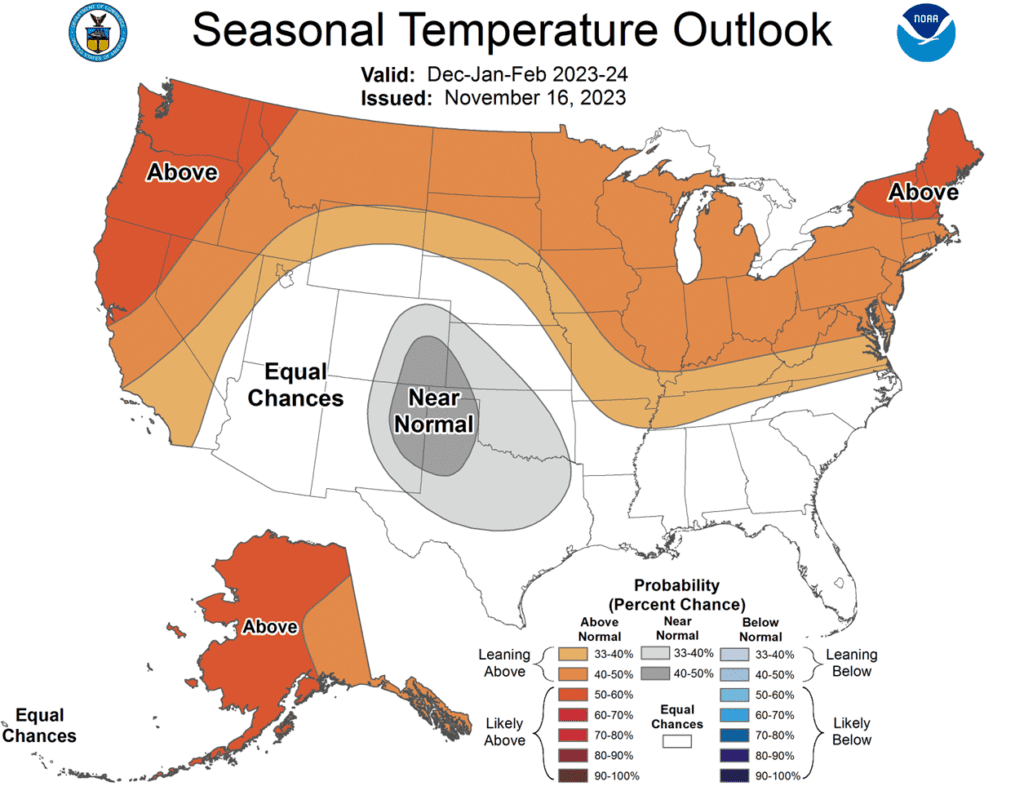

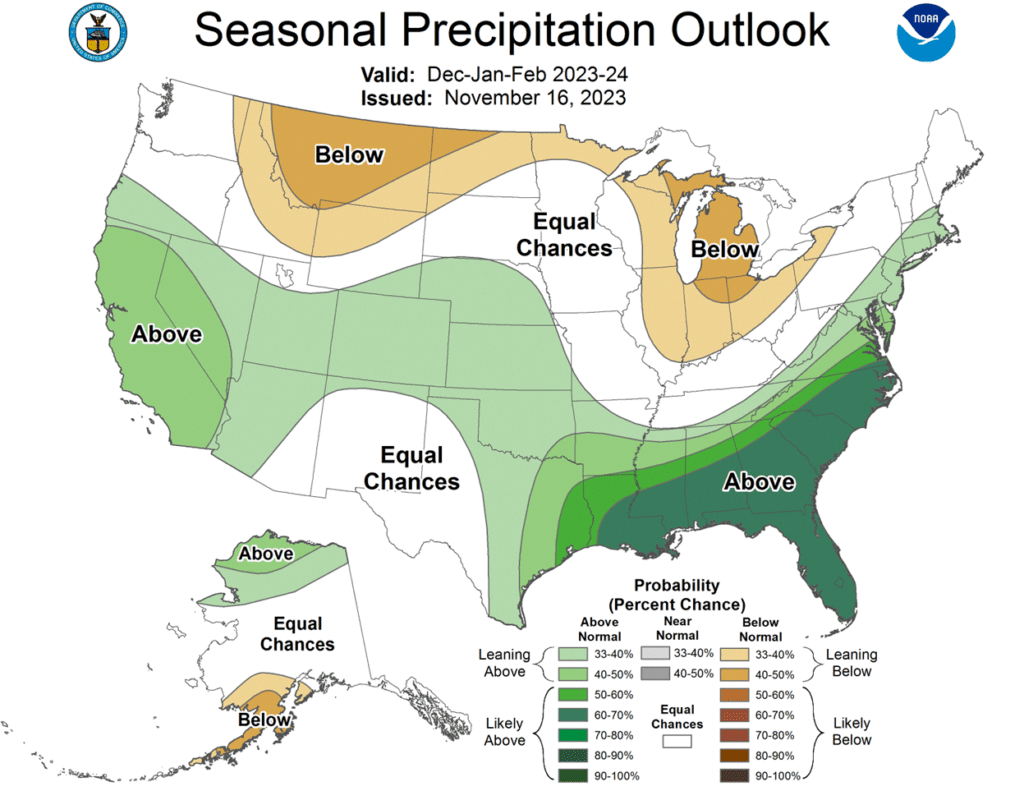

- To see the updated US Seasonal Temperature and Precipitation Outlooks and the Brazil 1 week forecast precipitation, courtesy of the National Weather Service, Climate Prediction Center, scroll down to other Charts/Weather Section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Corn Action Plan Summary

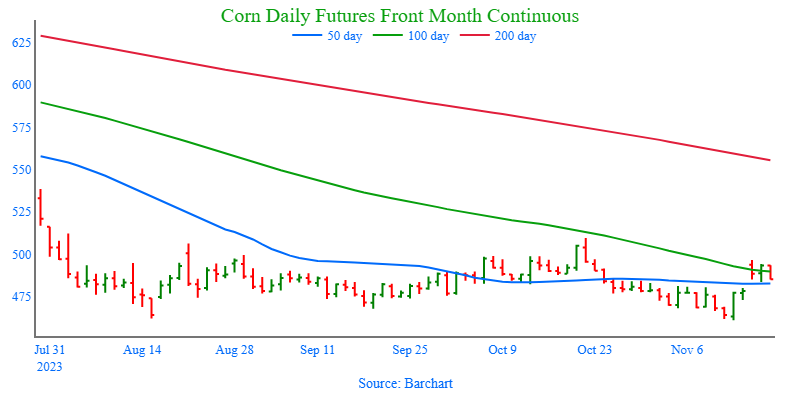

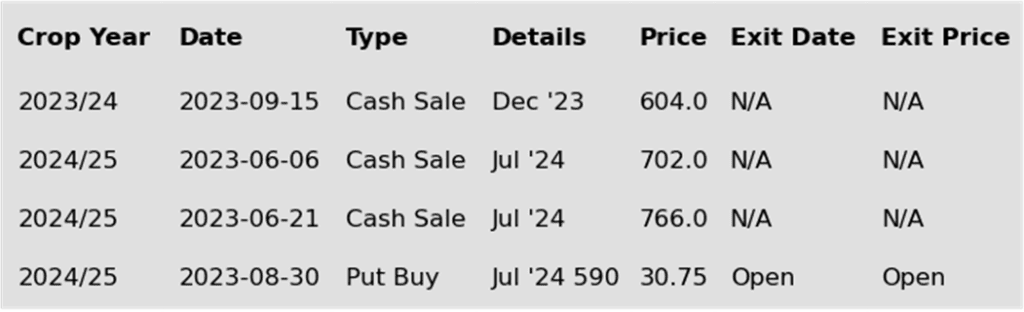

- No new action is recommended for 2023 corn. Since the beginning of August, the corn market has traded sideways largely between 470 and 500. October’s brief breakout to 509 ½ and the subsequent failure to stay above the 50-day moving average indicates there is significant resistance in that price range. The failure of November’s USDA report to provide a bullish influence on the market puts the market at risk of drifting sideways to lower without a bullish catalyst. During last summer’s June rally, Grain Market Insider recommended making sales when Dec ’23 was around 624. So, for now, the thought process is to hold tight on any further sales recommendations until later this fall or early winter, with the objective of seeking out better pricing opportunities. If the market has not turned around by early winter, then Grain Market Insider may sit tight on the next sales recommendations until spring. If you end up harvesting more bushels than you can store this fall and must move them, consider protecting those sold bushels with either July or September ’24 call options.

- No new action is recommended for 2024 corn. Since late February ’22, Dec ’24 has been bound by 489 ¾ on the bottom and 600 on the top. After testing 491 to 547 last July, it has mostly traded between 500 and 525. During this time, Dec ’24 has held up better as bear spreading has allowed Dec ’24 to maintain more of its value versus Dec ’23 as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Moving forward, the risk for 2024 prices is the same as for 2023 prices, which is a continuation of a lower trend without further bullish input. Grain Market Insider is watching for signs of a change in the current trend to look at recommending buying Dec ’24 call options. This past spring, Grain Market Insider recommended buying 560 and 610 Dec ’23 call options ahead of the summer rally and having those in place helped provide confidence to pull the trigger on recommending 2023 sales into that sharp rally, knowing that if corn kept rallying and went to 700 or 800 that the call options would protect those sold bushels.

- No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn futures gave back yesterday’s gains and then some, as sellers stepped back into the corn market, fueled by a wetter near-term forecast in Brazil and improving weather in Argentina. December corn lost 7 ¾ cents on the session, but managed improving 3 cents on the week over last week overall.

- Improved chances of rainfall in Brazil weighed on soybean prices, and with wheat futures seeing additional selling pressure, the negative tone weighed on corn futures as well.

- The corn market has been supported by an improving demand tone. Ethanol grind has been ahead of expectations, and export sales have been more active. Weekly export sales last week were above expectations, and currently total export sales are 40% of the USDA export target. The 5-year average is 39%, so sales are back on track so far.

- The Buenos Aires Grain Exchange cut its forecast for corn planting estimates and raised their soybean planting totals. The exchange lowered its planting estimate to 7.1 million hectares, down .2 million from their last estimate. The return of rainfall in Argentina is allowing for land to be planted into soybeans, shifting away from corn and wheat.

- The corn market still struggles to find its footing as late harvest is triggering corn bushel movement and the hedge pressure limits potential for a strong near-term rally.

Above: The nearby contract in corn has rolled from the December to the March, and while the chart looks like prices made a significant jump, it is in fact the premium in the March that is being represented on the chart. Upside resistance remains between 500 and 509 ½, while support below the market remains 460, with the next major area of support near 415.

Soybeans

Action Plan: Soybeans

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Soybeans Action Plan Summary

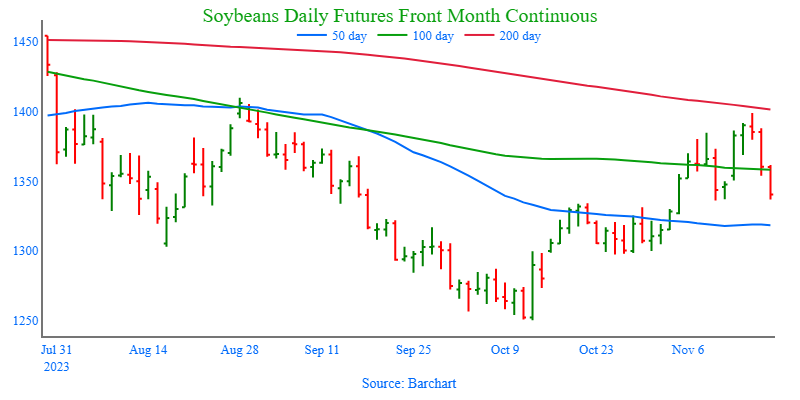

- No new action is recommended for 2023 soybeans. At the end of August, the soybean market turned lower and didn’t find any significant buying interest until it traded down to 1251 in early October. Since then, the nearby contract has traded through nearby resistance and the 50-day moving average and tested the August high. Looking back, since last May, nearby soybeans have been in a range from 1435 up top to 1251 down below. Last summer, Grain Market Insider did make two sales recommendations in the 1310 – 1360 price window versus Nov ’23. Given that those sales recommendations were made and given that now is not the time of year to be making many sales, if any, Grain Market Insider is content to hold tight on any further sales recommendations until later this fall or early winter. The focus for strategy right now is to be on the lookout for any call option buying opportunities. If you end up harvesting more bushels than you can store this fall, consider protecting any sold bushels with July or Aug ’24 call options.

- No action is recommended for the 2024 crop. Since the inception of the Nov ’24 contract, it has traded at a discount to the 2023 crop, from as much as 142 back in July, to as little as 17 ¾ in early October during harvest. And while the spread difference between the two crops has seen a good amount of volatility, Nov ’24 has been largely rangebound between 1250 and 1320 since it rallied off its 1116 ¼ low last July. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop. First sales targets will probably be early winter at the soonest. Currently, Grain Market Insider’s focus is also on watching for any opportunities to recommend buying call options.

- No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day lower for a third consecutive day and have lost 55 cents since the recent high was posted on Wednesday. The recent rally in soybeans was caused by dry South American weather, and this recent sell off has been caused by wetter South American forecasts.

- Argentina has been receiving more favorable weather lately and is in a good place to be planting soybeans, and it is being reported that planted acreage for beans will increase by 500k acres. In Brazil, rain chances are improved, but still limited until Thanksgiving, and afterwards, it is expected to dry out again.

- With the prospect of a larger Argentinian soy crop next year, soybean meal has begun slipping from its recent highs. A large portion of their rally has been due to increased export demand, and that will likely change next year. Soybean oil has trended slightly higher, but is under pressure from crude oil.

- Yesterday’s export sales report featured a very large increase of 144.0 mb of soybeans for 23/24, which was a marketing year high and was in large part due to the big and consistent purchases from China over the past two weeks. In addition, a new sale to China was reported yesterday of 8.1 mb.

Above: On November 15, January soybeans posted a bearish reversal after coming within 11 cents of the August high. Since then, prices have traded lower and filled the gap left from 1349 ¾. For now, heavy resistance remains between 1400 and 1410, with support below the market between 1336 and the 50-day moving average near 1318.

Wheat

Market Notes: Wheat

- Wheat continued its slide with all three classes lower on the day. As the complex followed corn and soybeans lower, KC made a fresh contract low, while Chicago held more of its value versus both Minneapolis and KC.

- Even though the crop benefited from October’s rainfall, the Buenos Aires Grain Exchange lowered its estimate for Argentina’s wheat crop to 14.7 mmt, down from 15.4 mmt, primarily due to frost damage.

- With EU soft-wheat production seen at 125.8 mmt, a slight increase from last month’s estimate, EU crop analyst Strategie Grains reported that France may see a surplus in wheat and barley for 23/24 crop year.

- Japan’s Ministry of Agriculture in a regular tender bought 104,677 metric tons of food grade milling wheat from the US, Canada, and Australia.

- On the weather front, dry conditions continue to be a concern for much of the recently planted HRW wheat crop, which makes Sunday and Monday’s anticipated rain more significant. So far, 42.5% of the Kansas crop is estimated to be under severe drought according to Thursday’s release of the US Drought Monitor.

Action Plan: Chicago Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

No Action

2025

No Action

Chicago Wheat Action Plan Summary

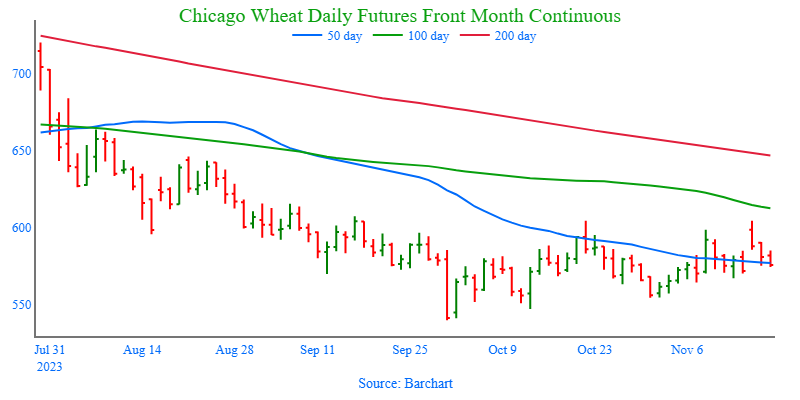

- No new action is currently recommended for 2023 Chicago wheat. After making a high in late July, nearby Chicago wheat trended lower until finding support at 540 on September 29, from which it rallied back, briefly piercing 600 and the 50-day moving average. The market now appears to be finding value in the 540 – 616 range established since early September, as weak US export demand, driven by cheap Russian exports, remains the dominant headwind to higher prices. Grain Market Insider made sales recommendations in the late June rally around 720 and again earlier this fall near 604. With those two sales, Grain Market Insider’s strategy is to look for price appreciation going into this winter as weather becomes a more prominent market mover, with an eye on considering additional sales in the 625 – 650 range. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

- No new action is recommended for 2024 Chicago wheat. After retesting the 800 level back in July, new crop Chicago wheat retreated steadily until hitting the late September low of 610 ¼. Since then, prices have been mostly rangebound between 620 and 650. Just as fund positioning and weak fundamentals have driven old crop prices down closer to the mid to upper 500 range and new crop prices to the low to mid 600s. The risk of further new crop price erosion remains without fresh bullish input to move prices higher. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for this possibility, and back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels, and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset some of the original cost and move toward a net neutral cost for the remaining position.

- No action is currently recommended for 2025 Chicago Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: The nearby contract in corn has rolled from the December to the March, and while the chart looks like prices made a significant jump, it is in fact the premium in the March that is being represented on the chart. Upside resistance remains between 604 ½ and 618, while support below the market may be found between 564 and 554.

Action Plan: KC Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

New Alert

Exit Half JUL ’24 KC 660 Puts ~ 60c

2025

No Action

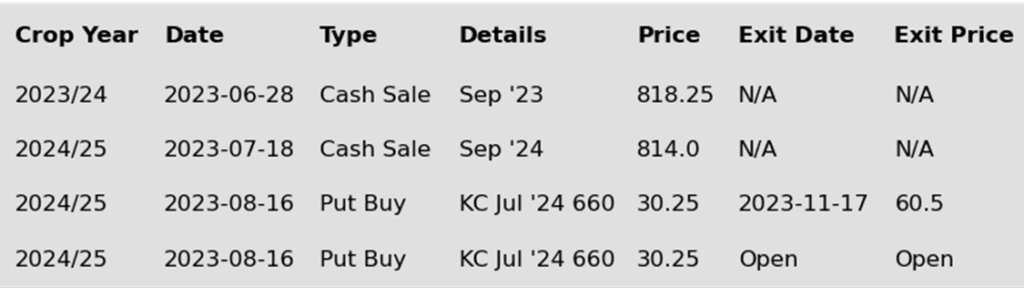

KC Wheat Action Plan Summary

- No new action is recommended for 2023 KC wheat crop. Since late July the nearby KC wheat has been in a downtrend that has had periods of relative stability, but not any significant reversals higher. The market once again found nearby support as it traded to, and held, its recent low of 625 ½. Currently, weak US export demand, driven by cheap Russian exports, remains the dominant headwind, and the market is in need of bullish input to stabilize and rally prices back higher. If a bullish catalyst enters the market to push prices above 700, it may signal that a fall low is in place and would line up with the historical tendency for prices to appreciate into winter and early spring. Grain Market Insider’s strategy is to look for price appreciation going into this winter, as weather becomes a more prominent market mover with an eye on considering additional sales near 750 – 800. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices.

- Grain Market Insider recommends selling half of your July ‘24 660 KC Wheat puts at approximately 61 cents in premium minus fees and commission. Back in August, Grain Market Insider recommended buying July ’24 660 KC wheat puts for approximately 30 cents in premium, plus commission and fees, to protect the downside for both KC wheat and Minneapolis wheat (KC puts were recommended for Minneapolis due to KC wheat’s greater liquidity and high correlation to Minneapolis wheat). At the time, US export demand was very weak, and July KC wheat had just broken through long-term support near 738. The breaking of 738 support increased the risk of the market retreating further. Since then, July ’24 KC wheat has broken through the September ’21 low and nearly 100 cents, with the July ’24 KC wheat 660 puts gaining nearly 200% in value. Though US export demand remains weak, plenty of time remains to market the ’24 crop, and the Drought Monitor still shows dry conditions in the HRW and HRS growing areas. Following the recent market drop, any increase in demand or threat of yield loss could rally prices. Grain Market Insider recommends selling half of the previously recommended July ’24 660 KC wheat puts to lock in gains in case prices rally back, and holding the remaining puts, which will continue to protect any unsold bushels if prices erode further.

- No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

Above: Since breaking through the bottom of the consolidation range at 655, the market has drifted lower and tested minor support which has held so far with the low at 625 ½. The next level of major support below that remains near 575. Major resistance above the market remains around 690 – 700.

Action Plan: Mpls Wheat

Calls

2023

No Action

2024

No Action

2025

No Action

Cash

2023

No Action

2024

No Action

2025

No Action

Puts

2023

No Action

2024

New Alert

Exit Half JUL ’24 KC 660 Puts ~ 60c

2025

No Action

Mpls Wheat Action Plan Summary

- No new action is currently recommended for the 2023 New Crop. After making highs in July, and the subsequent downtrend to the October 2 low of 707 ½, nearby Minneapolis wheat has traded mostly sideways with no significant reversal higher. With weak US export demand still the primary impediment to higher prices, the market remains at risk of trending lower if September’s low close of 709 is violated to the downside unless another bullish impetus enters the scene. If that happens and prices begin to push back toward 775, it may signal that a near-term low is in place. Earlier this year, Grain Market Insider made a sales recommendation during the July rally near 820, and with that sale in place, Grain Market Insider’s strategy is to look for price appreciation going into this winter with an eye on considering additional sales around 750 – 800, and again north of 825. If at that point the market remains strong and continues to rally, Grain Market Insider will consider potential re-ownership strategies to protect current sales and add confidence to make additional sales at higher prices. Even though the primary strategy is to look for higher prices, Grain Market Insider may also consider a “plan b” in the next couple of weeks if prices grind sideways to lower.

- Grain Market Insider recommends selling half of your July ‘24 660 KC Wheat puts at approximately 61 cents in premium minus fees and commission. Back in August, Grain Market Insider recommended buying July ’24 660 KC wheat puts for approximately 30 cents in premium, plus commission and fees, to protect the downside for both KC wheat and Minneapolis wheat (KC puts were recommended for Minneapolis due to KC wheat’s greater liquidity and high correlation to Minneapolis wheat). At the time, US export demand was very weak, and July KC wheat had just broken through long-term support near 738. The breaking of 738 support increased the risk of the market retreating further. Since then, July ’24 KC wheat has broken through the September ’21 low and nearly 100 cents, with the July ’24 KC wheat 660 puts gaining nearly 200% in value. Though US export demand remains weak, plenty of time remains to market the ’24 crop, and the Drought Monitor still shows dry conditions in the HRW and HRS growing areas. Following the recent market drop, any increase in demand or threat of yield loss could rally prices. Grain Market Insider recommends selling half of the previously recommended July ’24 660 KC wheat puts to lock in gains in case prices rally back, and holding the remaining puts, which will continue to protect any unsold bushels if prices erode further.

- No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: The nearby contract in corn has rolled from the December to the March, and while the chart looks like prices made a significant jump, it is in fact the premium in the March that is being represented on the chart. Nearby resistance remains near 755 with heavy resistance above the market near the September high of 791. Below the market initial support lies near 721, with major support down near 669, the May ’21 low.

Other Charts / Weather

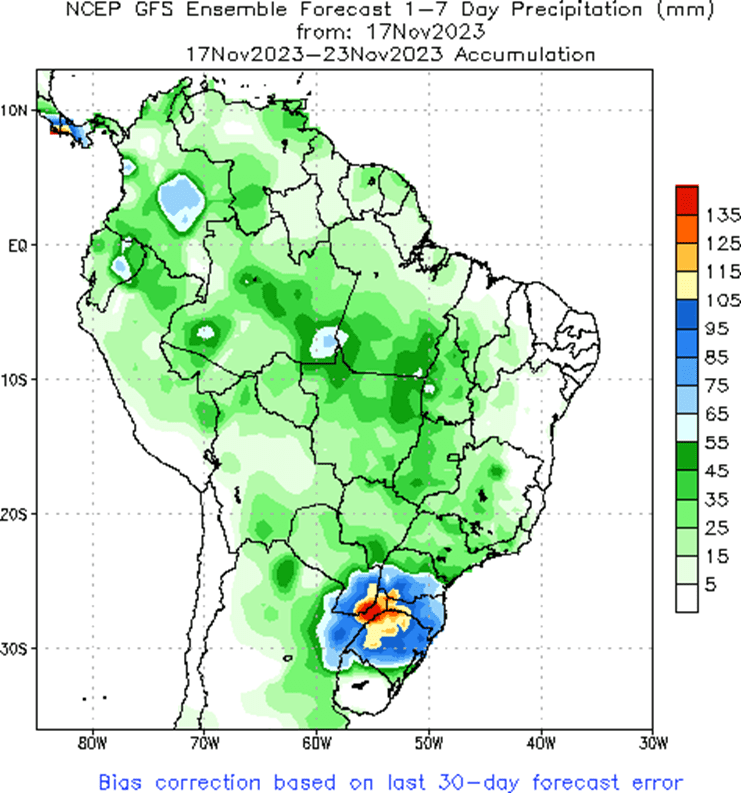

Brazil 1 week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center.