10-15 End of Day: Grains Continue Their Slide, Closing Lower Across the Board

All prices as of 2:00 pm Central Time

| Corn | ||

| DEC ’24 | 401.25 | -7 |

| MAR ’25 | 417.5 | -7.25 |

| DEC ’25 | 437 | -5.5 |

| Soybeans | ||

| NOV ’24 | 991 | -5 |

| JAN ’25 | 1003.5 | -8 |

| NOV ’25 | 1035.75 | -11.25 |

| Chicago Wheat | ||

| DEC ’24 | 579.5 | -5.75 |

| MAR ’25 | 600.75 | -6.5 |

| JUL ’25 | 616.5 | -8.25 |

| K.C. Wheat | ||

| DEC ’24 | 583 | -7 |

| MAR ’25 | 598.75 | -7.25 |

| JUL ’25 | 617 | -7.5 |

| Mpls Wheat | ||

| DEC ’24 | 616.25 | -10.25 |

| MAR ’25 | 638 | -9.75 |

| SEP ’25 | 661.75 | -7.75 |

| S&P 500 | ||

| DEC ’24 | 5869.25 | -39 |

| Crude Oil | ||

| DEC ’24 | 70.18 | -3.06 |

| Gold | ||

| DEC ’24 | 2681.5 | 15.9 |

Grain Market Highlights

- Harvest pressure and sharply lower crude oil weighed on the corn market throughout the session, pushing the December contract to its lowest close since late August.

- A flash sale to China, solid weekly export inspections, and much higher than expected NOPA crush numbers helped November soybeans curb some of its losses and close 10 cents off its low. Soybean oil found support near the 50-day moving average to close higher on the day, while meal settled lower after resuming its downtrend.

- Despite a flash sale of 120,000 mt of wheat and export inspections running 33% ahead of last year, the wheat complex closed lower across the board for the third consecutive day, pressured by sharp losses in crude oil and a third day of declines in Matif wheat.

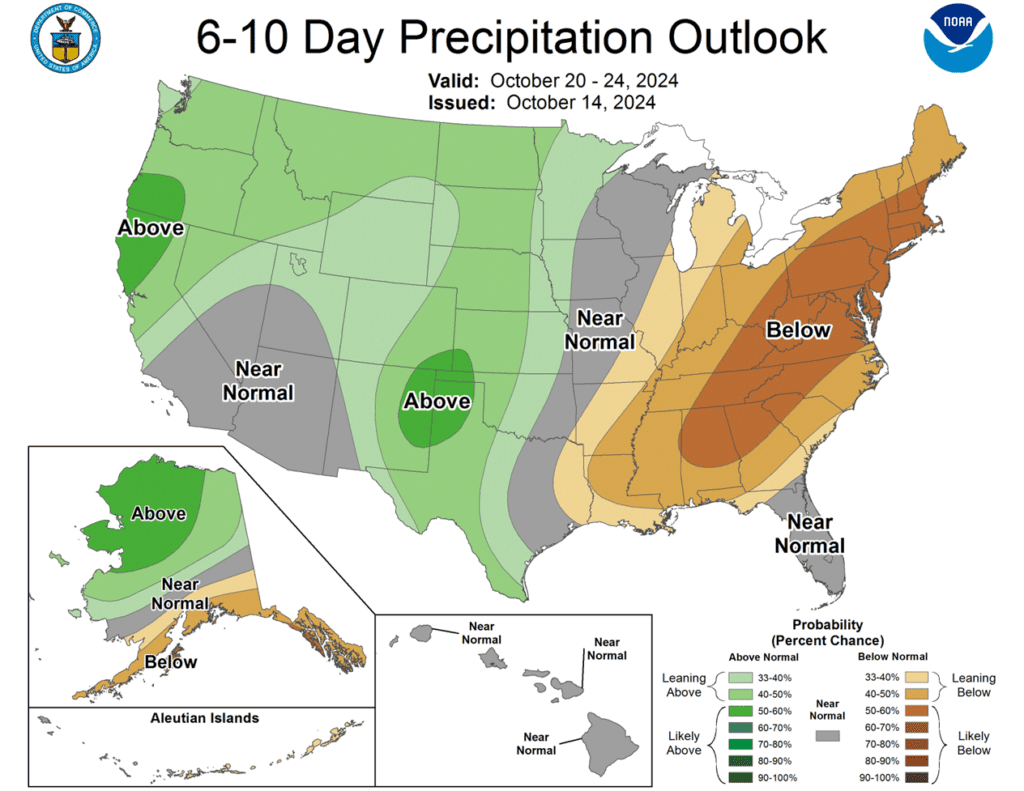

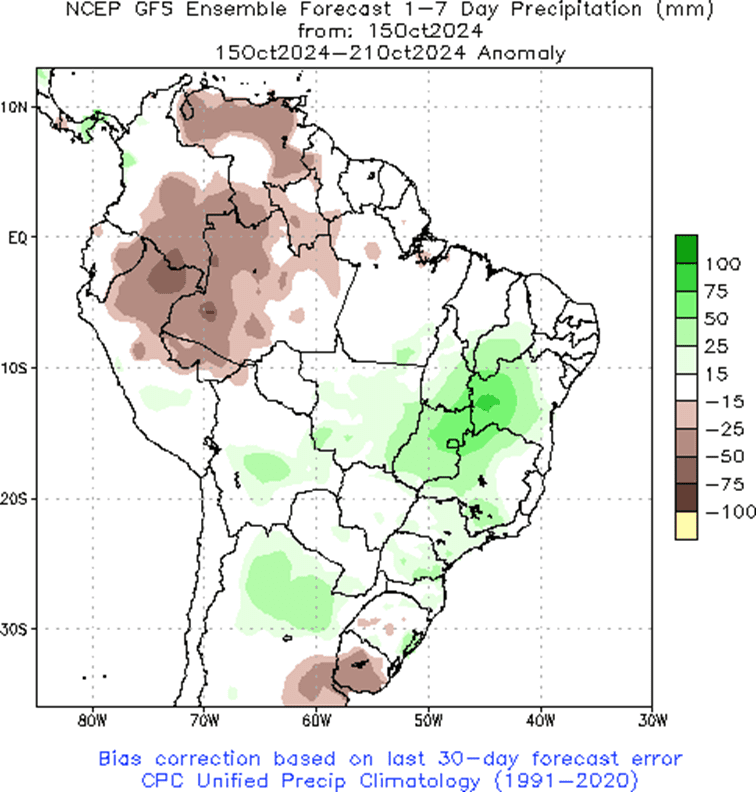

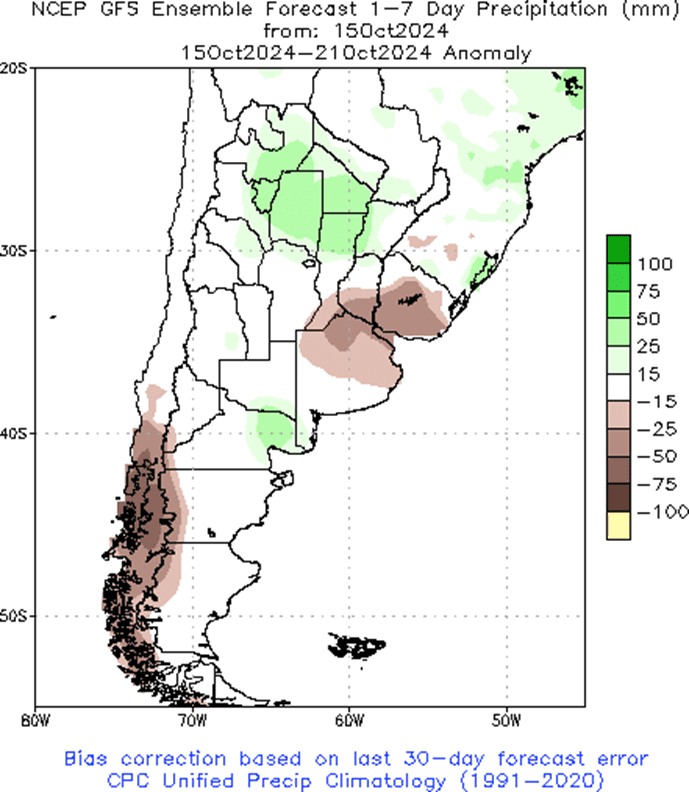

- To see the updated US 7-day precipitation forecast, 6 – 10 day Temperature and Precipitation Outlooks and the South American 1-week forecast total precipitation as a percent of normal, courtesy of the National Weather Service, Climate Prediction Center, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Corn Action Plan Summary

Since hitting a peak in early October, corn prices have fallen off as harvest continues at a rapid pace with record yields according to the USDA, and South American weather has turned more seasonal. Now that managed funds have covered most of their record short positions, they have flexibility to establish net long or net short positions. Any unexpected downward shift in anticipated US supply or deterioration in South American growing conditions could trigger managed funds to continue buying and rally prices further. However, if harvest yields remain strong and South American weather turns more favorable, prices could be at risk of retreating.

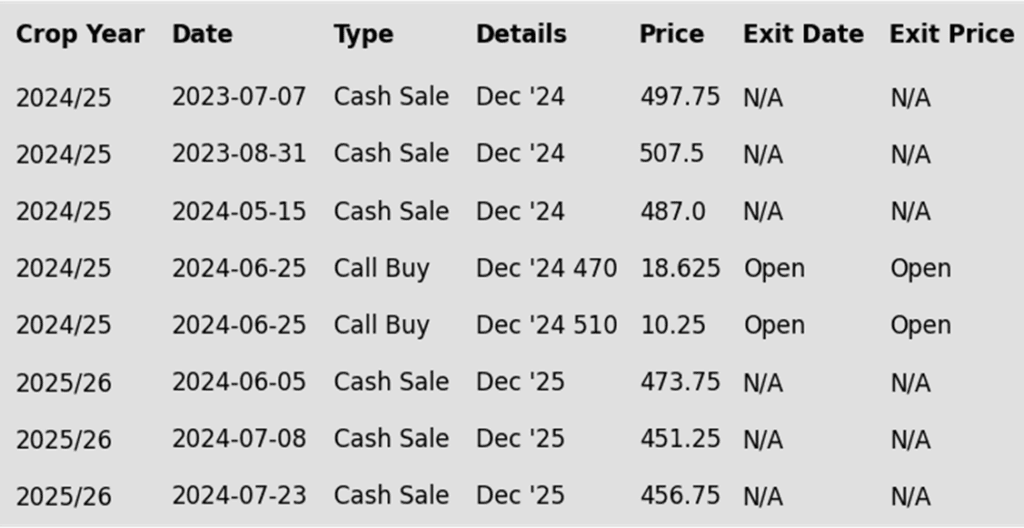

- No new action is recommended for 2024 corn. Considering harvest time doesn’t typically offer the most advantageous sales prices, we don’t anticipate making any sales recommendations until late fall at the earliest, or possibly as late as early spring when opportunities tend to improve. For those who need to sell bushels due to space constraints or to raise capital, consider targeting a rally back to the 429 – 460 range versus Dec ’24 to make any necessary sales.

- No new action is currently recommended for 2025 corn. Between early June and late July Grain Market Insider made three separate sales recommendations to get early sales made for next year’s crop. Considering the seasonal weakness of the market into harvest, we will not be looking to post any targeted areas for new sales until late fall or early winter. Although we will look to protect current sales, in the form of buying call options, should the market begin to show signs of a potential extended rally. Until we post new sales targets, if you are looking to make additional early sales for next year, you could consider targeting the 455 – 475 area versus Dec ’25 to take advantage of any post-harvest strength.

- No Action is currently recommended for 2026 corn. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Corn futures fell to the lowest price levels since September 23 during Tuesday’s session, as strong selling in the crude oil market and ongoing harvest pressure weighed on corn prices. With today’s close, December corn is now trading 33 cents off the October 1 high of 434.

- The crude oil market traded over 5% lower during the session as global demand concerns and easing tension between Iran and Israel pushed sellers into the market. The sharp break in crude prices limited commodity gains in general on Tuesday.

- Weekly corn export inspections were below market expectations. Last week, the US shipped 16.9 mb (430,000 mt) of corn. This total was less than half of the previous week’s total as exporters are likely shifting to shipping fresh soybean supplies. Current corn inspections are up 19% year over year and running above the pace needed to hit the USDA targets.

- The weather forecast continues to stay favorable for corn harvest. With strong yields overall, the market is seeing selling pressure as fresh supplies enter the pipeline. Corn harvest was 34% complete last week, and the market is anticipating a good jump on the harvest percentage in today’s USDA Crop Progress report.

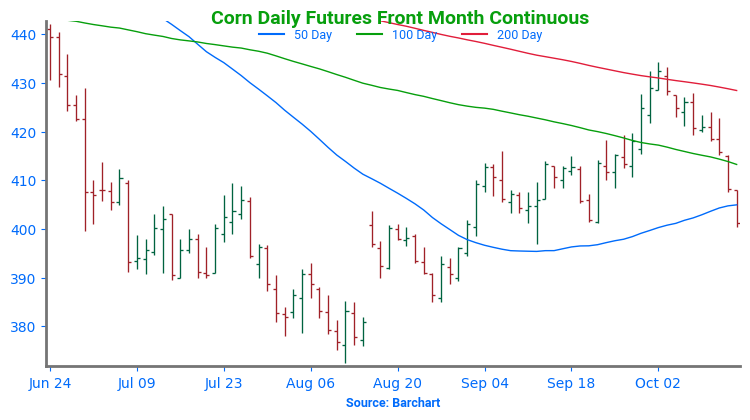

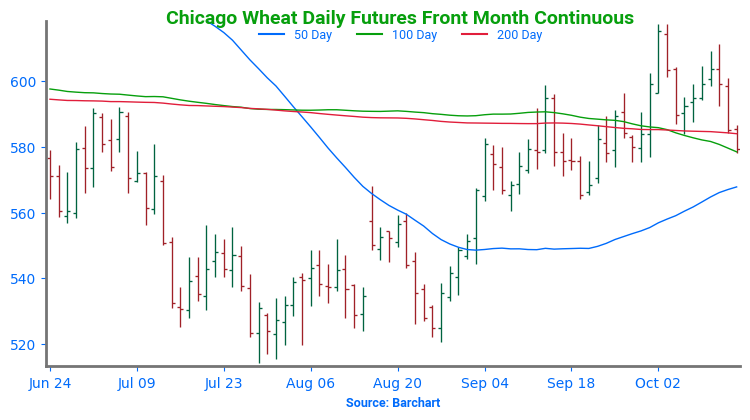

Above: Since the beginning of October, the near-term trend has been down. Initial support may come in near 410, with further support near the 50-day moving average and again around 397-400. On the top side, initial resistance may come in near 428, with heavier resistance near the recent high of 434 ¼.

Soybeans

Action Plan: Soybeans

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Soybeans Action Plan Summary

After hitting a seasonal low in mid-August, the soybean market rose steadily, reaching its peak in early October, driven by drier conditions in the US during the later stages of crop development and continued dryness in key soybean-growing regions of South America. During this time, managed funds covered over 80% of their significant short positions, creating the potential for volatility in either direction. Prices could rise if South American conditions worsen, encouraging further fund buying, or decline if conditions improve, prompting funds to potentially rebuild short positions. Seasonally, once harvest is complete, prices tend to firm as hedge pressure subsides and the market begins to price in any potential South American weather premium.

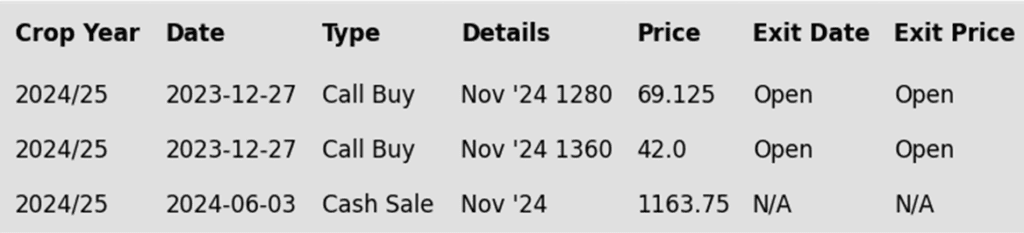

- No new action is recommended for the 2024 crop. In early June, when our Plan B strategy was triggered by the market’s close below 1180, we recommended making sales at that time due to the potential change in trend signaled by that weak close. Because harvest time typically does not present the most advantageous pricing opportunities, we don’t anticipate making any sales recommendations until seasonal opportunities improve, potentially as early as late fall or as late as early spring. For those who need to sell bushels due to space constraints or to raise capital, consider selling into price strength and targeting a rally back to the 1050 – 1070 range versus Nov ’24 to make any necessary sales. Should the market rally beyond there, consider additional sales in the 1090 – 1125 area versus Nov ’24.

- No Action is currently recommended for 2025 Soybeans. To date, Grain Market Insider has not recommended any sales for next year’s soybean crop yet. First sales targets will probably be set in late fall or early winter at the earliest. Currently, our focus is on watching for opportunities to recommend buying call options. Should Nov ‘25 reach the upper 1100 range, the likelihood of an extended rally would increase, and we would recommend buying upside call options at that time in preparation for that possibility.

- No Action is currently recommended for 2026 Soybeans. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day lower but were bull spread with the front months down less than the deferred contracts. Soybeans had bullish fundamental news like a flash sale, strong export inspections, and strong NOPA crush numbers. Soybean meal ended the day lower, while soybean oil was higher despite sharply lower crude oil.

- Today’s NOPA crush report showed US soybean crush up significantly to 177.320 million bushels for September, which compared to the average trade estimate of 170 mb. This was up 12.2% from the 158 mb in August. Soybean oil stocks fell to 1.066 billion pounds and are the lowest they have been since November 2014.

- This morning, the USDA reported private export sales totaling 131,000 metric tons of soybeans for delivery to China during the 24/25 marketing year.

- Today’s export inspections report showed soybeans inspected for export totaled 57.9 mb for the week ending October 10. This was at the higher end of analyst estimates and puts total inspections for the 24/25 marketing year at 189 mb, which is down 7% from the previous year.

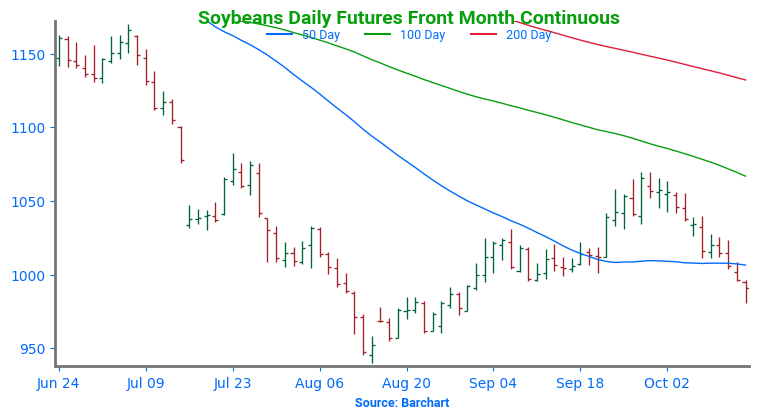

Above: The recent downtrend appears to have found support near 1080 in the November contract, and with the market showing signs of being oversold, prices could rebound toward recent highs near 1070. Before that, prices may encounter resistance around 1025. If prices break the 980 support level, they could find additional support near 955 and again around 940.

Wheat

Market Notes: Wheat

- Wheat closed the session with modest losses, finishing near daily lows across all three futures classes. Paris milling wheat futures declined for the third consecutive day, adding pressure. Meanwhile, the US Dollar Index, though nearly unchanged at the time of writing, strengthened throughout the session after finding support around the 103 level. The index is now above its 100-day moving average for the second straight day, a level it had not surpassed since July 11, 2023.

- Weekly wheat export inspections of 13.6 mb bring total 24/25 inspections to 330 mb, up 33% from last year. Additionally, the USDA estimates wheat exports at 825 mb (unchanged from the last WASDE report), which would be a 17% increase from the previous year.

- Crude oil experienced another sharp drop today, at one point falling more than four dollars per barrel. This appears to be tied to news that Israel does not intend to target Iranian oil facilities as previously expected. Furthermore, both OPEC and the International Energy Agency reduced their global oil demand estimates. The downturn in crude likely added pressure to the grain complex, and if the trend continues, it could also limit upward grain price movement in the event of a recovery.

- On a bullish note, the USDA announced a flash sale this morning, reporting that private exporters sold 120,000 mt of soft red winter wheat to Mexico for delivery during the 24/25 marketing year. In other news, Jordan reportedly passed on its tender for 120,000 mt of wheat.

- CONAB estimates Brazil’s 24/25 wheat production at 8.26 mmt, unchanged from last month and below the USDA’s estimate of 9 mmt. Additionally, recent rains in Argentina’s wheat-growing areas have helped improve conditions, though at this point it may be too little, too late. Last week, the Rosario Grains Exchange lowered its Argentina wheat harvest estimate to 19.5 mmt due to a lack of precipitation.

- According to the French agriculture ministry, the soft wheat harvest estimate has been reduced from 25.8 to 25.4 mmt. If accurate, this would represent a 27.6% decline from last season’s production. Additionally, barley production is expected to fall, though the corn production estimate has been raised slightly from last month.

Action Plan: Chicago Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Chicago Wheat Action Plan Summary

After posting a low in late July, the wheat market staged a rally triggered by crop concerns due to wet conditions in the EU, smaller crops out of Russia and Ukraine, and dryness in the US plains. The nearly 100-cent rally from the August low to October high also saw Managed funds cover about two-thirds of their net short positions. While cheaper Russian export prices continue to be a limiting factor for US prices, a new season is upon us with many uncertainties ahead that could keep volatility in the market. Additionally, US export sales remain ahead of the pace set last year and in 2022, and any increase in demand from lower World supplies could rally prices further.

- No new action is recommended for 2024 Chicago wheat. Considering the rally in wheat back in May, we recommended taking advantage of the elevated prices to make additional sales and buy upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 740 – 760 versus Dec ’24 to recommend further sales, while also targeting a selling price of about 73 cents in the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is recommended for 2025 Chicago wheat. Recently, we recommended taking advantage of the wheat rally to sell more of your anticipated 2025 SRW production. While we continue to recommend holding the remaining July ’25 620 puts — after advising to exit the first half back in July — to maintain downside coverage for any unsold bushels, we are targeting a 10-15% extension from our last sale to the 650–680 area in July ’25 to suggest making additional sales.

- No action is currently recommended for 2026 Chicago Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

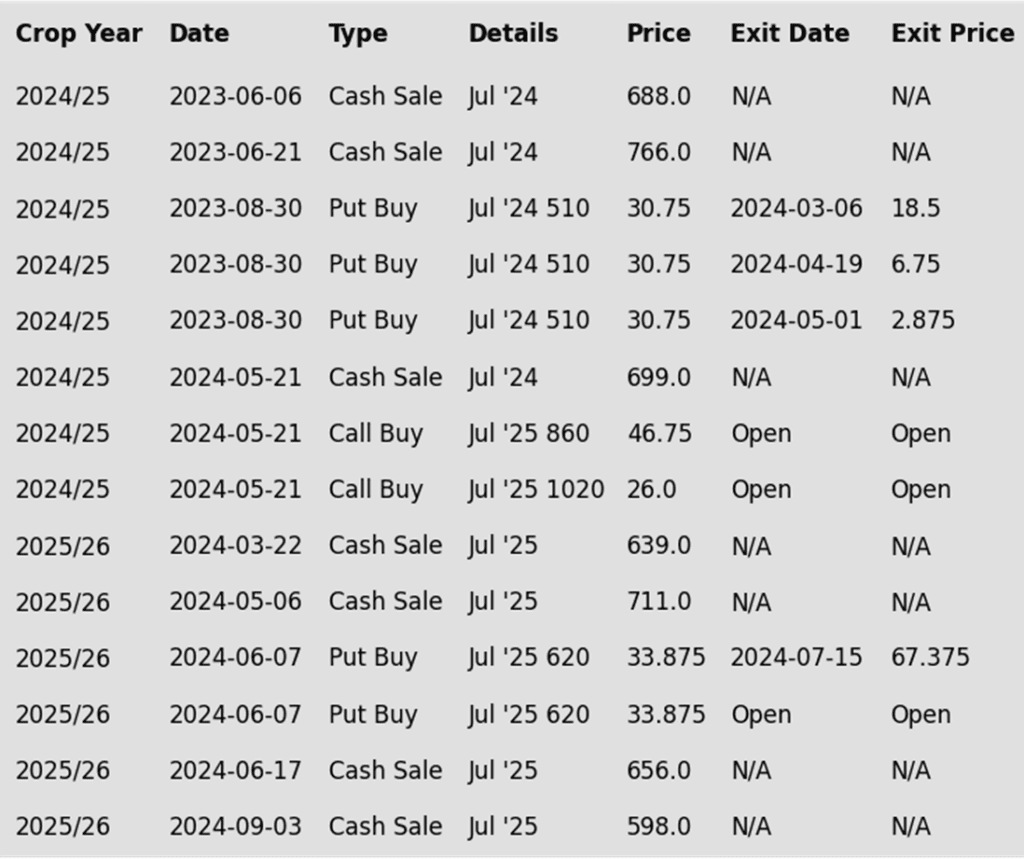

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: The upside breakout in Chicago wheat was met with resistance near 617. Should prices turn back higher and close above 617, they could make a run towards the 645 resistance area. Otherwise, if prices drift lower, they could find support between 575 and 560.

Action Plan: KC Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

KC Wheat Action Plan Summary

After hitting a market low in late August, the wheat market has rallied driven by crop concerns in the EU and reduced production from Russia and Ukraine. The rise in prices from late August through early October also prompted Managed funds to cover a significant portion of their net short positions. Although more competitive Russian export prices continue to cap potential gains for US wheat, the onset of a new season introduces a range of uncertainties that could fuel market volatility. Moreover, US export sales are currently outpacing last year’s figures and those from 2022, meaning that any uptick in demand due to tighter global supplies could further lift prices.

- No new action is recommended for 2024 KC wheat. Considering the upside breakout in KC wheat back in May, we recommended buying upside July ’25 860 and 1020 calls (for their extended time frame) in case of a protracted rally. Our current strategy is to target 635 – 660 versus Dec ’24 to recommend further sales, while also targeting a selling price of about 71 cents on the 860 calls to achieve a net neutral cost on the remaining 1020 calls. The remaining 1020 calls would then continue to protect existing sales and give you confidence to make additional sales at higher prices.

- No new action is currently recommended for 2025 KC Wheat. While we still recommend holding the remaining half of the previously suggested July ’25 620 puts for downside protection on unsold bushels, we recently advised selling another portion of your anticipated 2025 HRW wheat production in light of the early fall rally in the wheat market. Looking ahead, our current strategy is to target the 700–725 range for additional sales, while also targeting the upper 400 range to exit half of the remaining 620 puts, in case the market turns toward new lows.

- No action is currently recommended for 2026 KC Wheat. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted next year, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

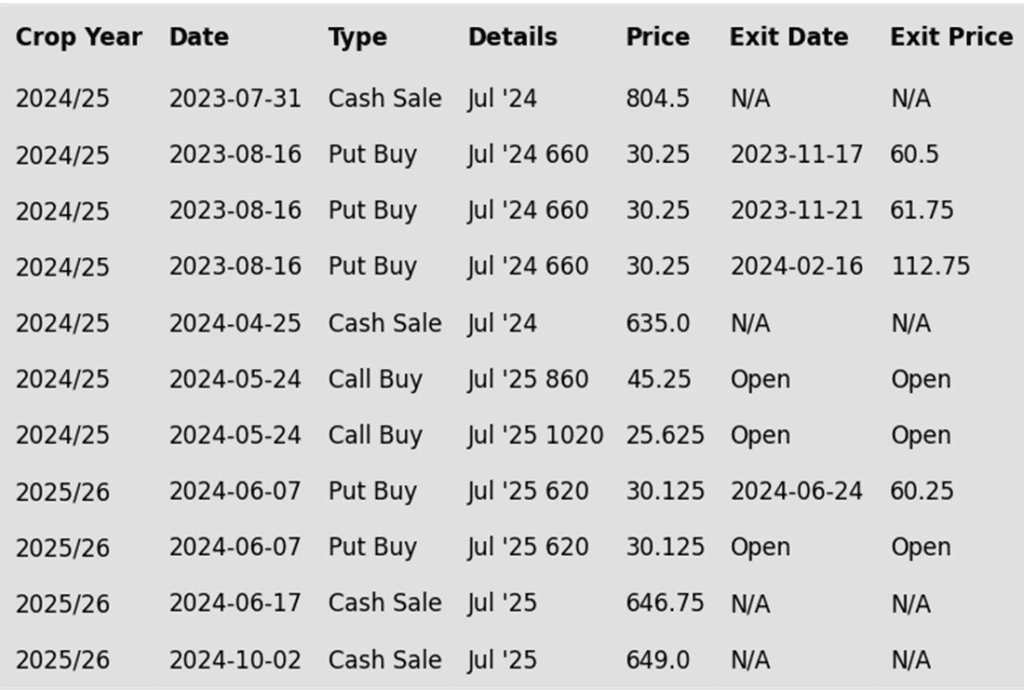

To date, Grain Market Insider has issued the following KC recommendations:

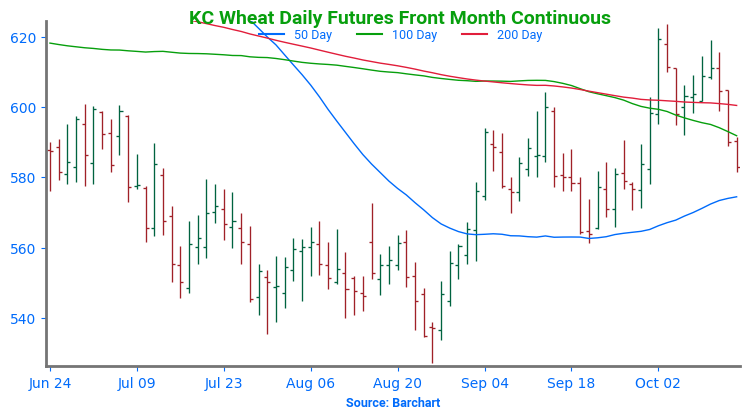

Above: The December contract’s break below 592 suggests that prices could decline further toward 561, with initial support likely around the 50-day moving average before reaching that level. On the upside, initial resistance is expected near 592, with stronger resistance around 623.

Action Plan: Mpls Wheat

Calls

2024

No New Action

2025

No New Action

2026

No New Action

Cash

2024

No New Action

2025

No New Action

2026

No New Action

Puts

2024

No New Action

2025

No New Action

2026

No New Action

Mpls Wheat Action Plan Summary

Since posting a seasonal low in late August, Minneapolis wheat has traded up to its 200-day moving average and its highest level since mid-July. During this period, managed funds have covered about 75% of their short positions in Minneapolis wheat. While more competitive export prices out of Russia continue to limit upside opportunities, concerns regarding world wheat supplies remain, which could increase opportunities for US exports and potentially drive prices higher.

- No new action is recommended for 2024 Minneapolis wheat. With the close below 712 support in June, Grain Market Insider implemented its Plan B stop strategy, recommending additional sales for the 2024 crop due to waning upside momentum and an increased likelihood of a downward trend. Given the heightened volatility and the amount of time that remains to market this crop, we will maintain the current July ’25 KC wheat 860 and 1020 call options. Our target is a selling price of about 71 cents for the 860 calls to achieve a net neutral cost on the remaining 1020 calls. These 1020 calls will continue to protect existing sales and provide confidence to make additional sales at higher prices. Now that the spring wheat harvest is behind us, and we are at the time of year when seasonal price trends tend to become more friendly, we are targeting the 675 – 700 range to recommend making additional sales.

- No new action is currently recommended for the 2025 Minneapolis wheat crop. Since the growing season can often yield some of the best sales opportunities, we made two separate sales recommendations in July to get some early sales on the books for next year’s crop. While we will not be targeting any specific areas to make additional sales until later in the marketing year, we will continue to monitor the market for opportunities to exit the remaining July ’25 KC 620 puts that were recommended in June. To that end, we are currently targeting the upper 400 range versus July ’25 KC to exit half of those remaining puts.

- No Action is currently recommended for the 2026 Minneapolis wheat crop. We currently aren’t considering any recommendations at this time for the 2026 crop that will be planted 2 years from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

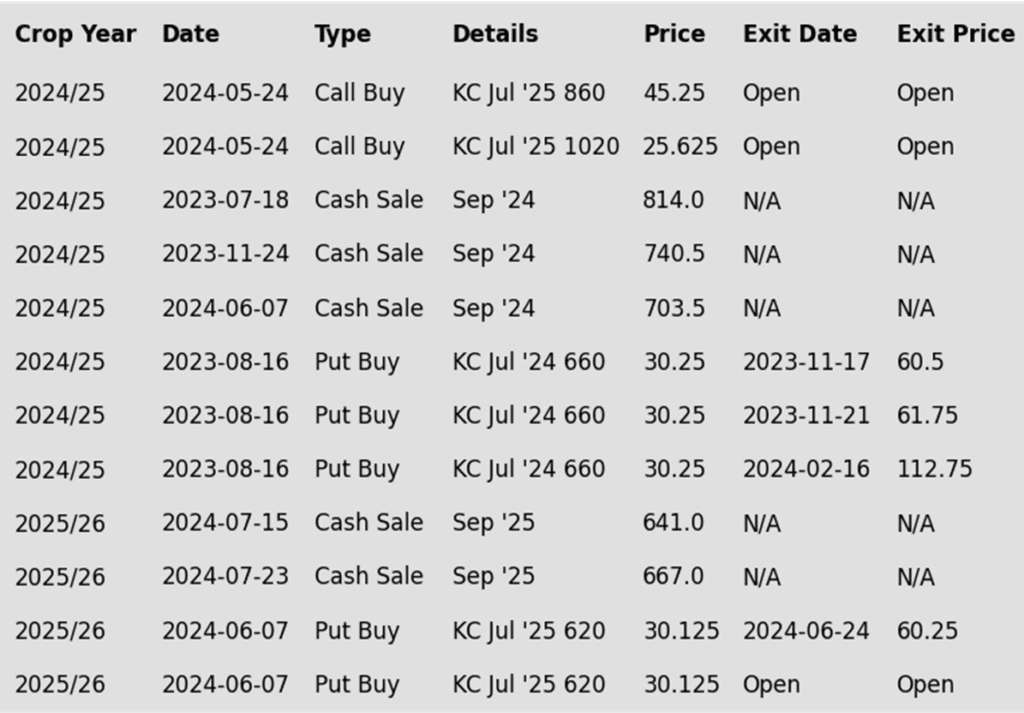

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

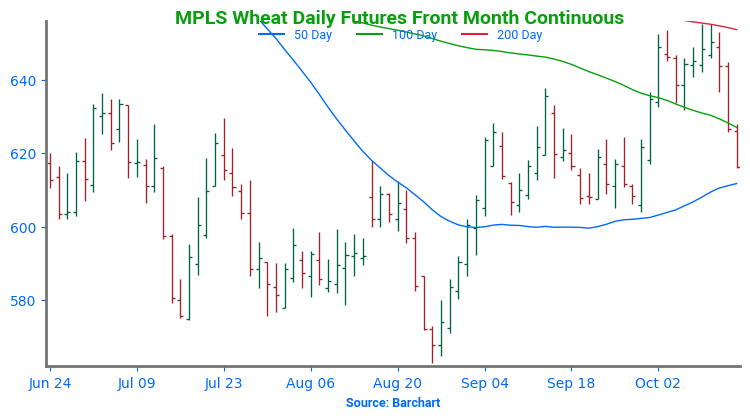

Above: The recent break below the 200-day moving average suggests that prices could drift further toward the 604 support area, with additional support near the 50-day moving average before reaching that level. If prices turn higher, overhead resistance may be around 632, with stronger resistance near 655.

Other Charts / Weather

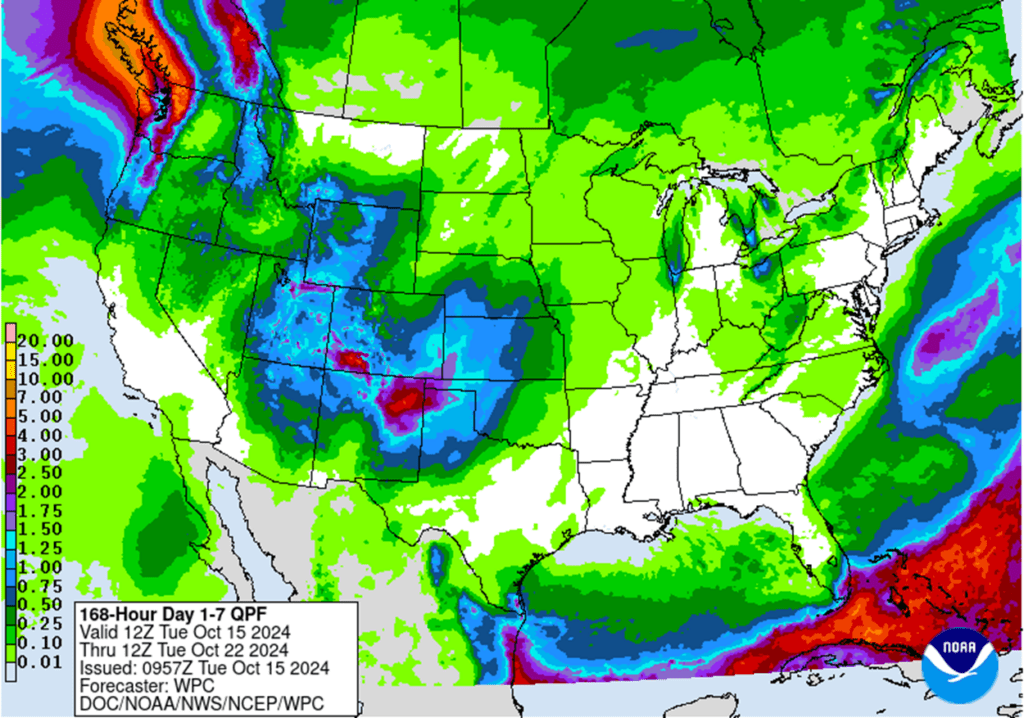

Above: US 7-day precipitation forecast courtesy of NOAA, Weather Prediction Center.

Above: Brazil, N. Argentina 1 week forecast precipitation, percent of normal, courtesy of the National Weather Service, Climate Prediction Center.

Above: Argentina 1 week forecast precipitation, percent of normal, courtesy of the National Weather Service, Climate Prediction Center.