1-25 End of Day: Wheat Continues Higher, Row Crops Lower on Thursday

All prices as of 2:00 pm Central Time

| Corn | ||

| MAR ’24 | 451.75 | -0.5 |

| JUL ’24 | 469.25 | -1.5 |

| DEC ’24 | 480.75 | -1.5 |

| Soybeans | ||

| MAR ’24 | 1223 | -17.25 |

| JUL ’24 | 1237.5 | -15.25 |

| NOV ’24 | 1196.25 | -11.75 |

| Chicago Wheat | ||

| MAR ’24 | 612.25 | 1.5 |

| JUL ’24 | 627.5 | 1.25 |

| JUL ’25 | 661.5 | 0 |

| K.C. Wheat | ||

| MAR ’24 | 637 | 11.25 |

| JUL ’24 | 633 | 3.75 |

| JUL ’25 | 664.25 | -2.5 |

| Mpls Wheat | ||

| MAR ’24 | 709 | 4.5 |

| JUL ’24 | 719 | 3.75 |

| SEP ’24 | 726.25 | 3.25 |

| S&P 500 | ||

| MAR ’24 | 4905.75 | 7.75 |

| Crude Oil | ||

| MAR ’24 | 77.44 | 2.35 |

| Gold | ||

| APR ’24 | 2037 | 1.8 |

Grain Market Highlights

- Corn futures were lower today for the first time this week. Late day strength in the wheat market helped corn to close well off its daily low.

- Soybeans fell on the day after softer than expected export sales this morning. Brazilian cash market weakness added pressure as harvest is just getting underway.

- Soybean meal and soybean oil futures both were lower on the day as crush margins continue to narrow.

- All three wheat classes closed in the green once again on Thursday. KC wheat led the gains today as continuous KC wheat futures closed above the 50-day moving average for the first time in 2024.

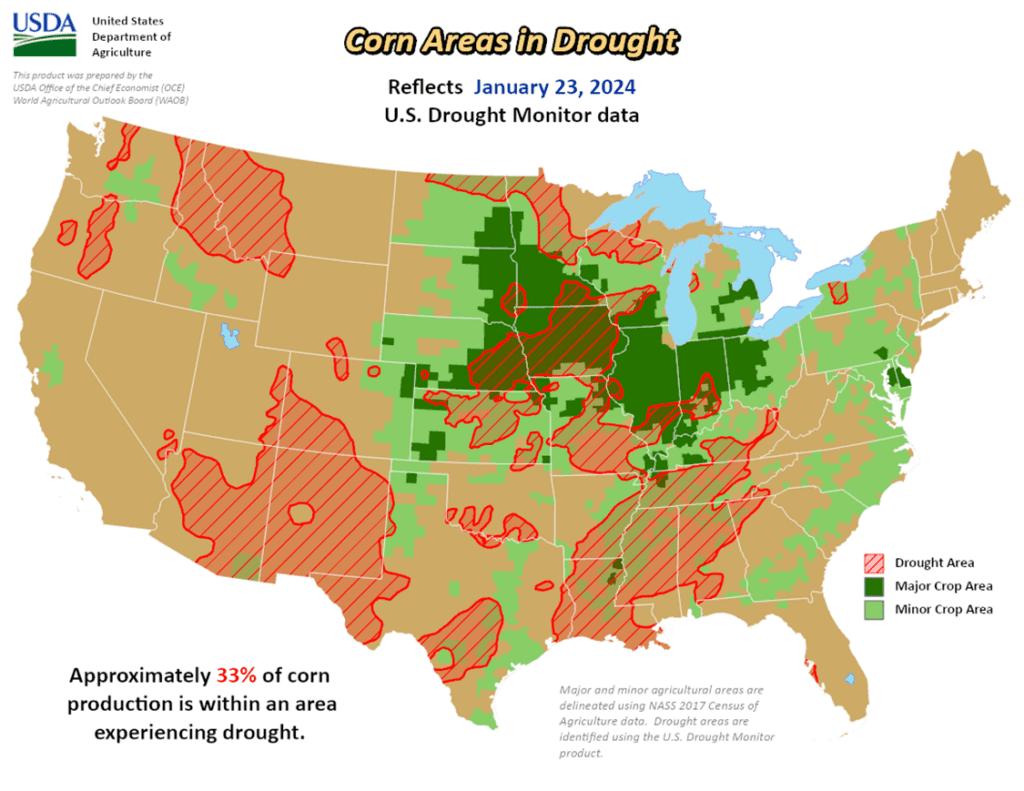

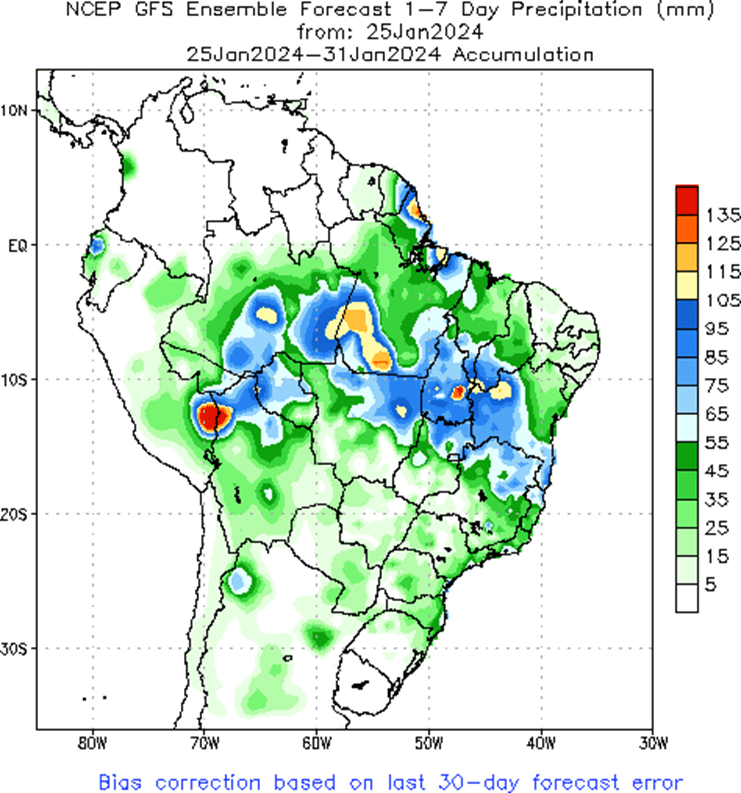

- To see the US Corn Areas in Drought Map as of January 23, 2024, and the 1-week GFS Ensemble Precipitation Forecast for South America courtesy of the USDA Office of the Chief Economist, the World Agricultural Outlook Borad and the Climate Prediction Center, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

- No new action is recommended for 2023 corn. Front month corn has languished in a sideways to lower trend since printing a high in October, with a general lack of bullish news and an estimated US carryout over 2.1 billion bushels. The failure of the USDA’s January report to provide the bullish news necessary to turn prices higher is disappointing and the market remains at risk of remaining in the same pattern. With that being said, the market does show signs of being oversold, and managed funds hold a sizable net short position, which could trigger a short covering rally if a bullish catalyst enters the scene. For now, Grain Market Insider will continue to hold tight on any further sales recommendations for the next few weeks with the objective of seeking out better pricing opportunities. If the market has not turned around by then, Grain Market Insider may sit tight on the next sales recommendations until spring.

- No new action is recommended for 2024 corn. Following the January USDA Supply and Demand update, Dec ’24 broke through the bottom end of the 485 ¾ to 602 range that had been in place since February ’22. While this is a disappointing development, bear spreading has allowed Dec ’24 to maintain more of its value versus old crop, as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Additionally, Dec ’24 does show signs of being oversold, which is supportive if a bullish catalyst enters the scene. Grain Market Insider continues to watch for signs of a change in the current trend to look at recommending making additional sales and buying Dec ’24 call options.

- No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

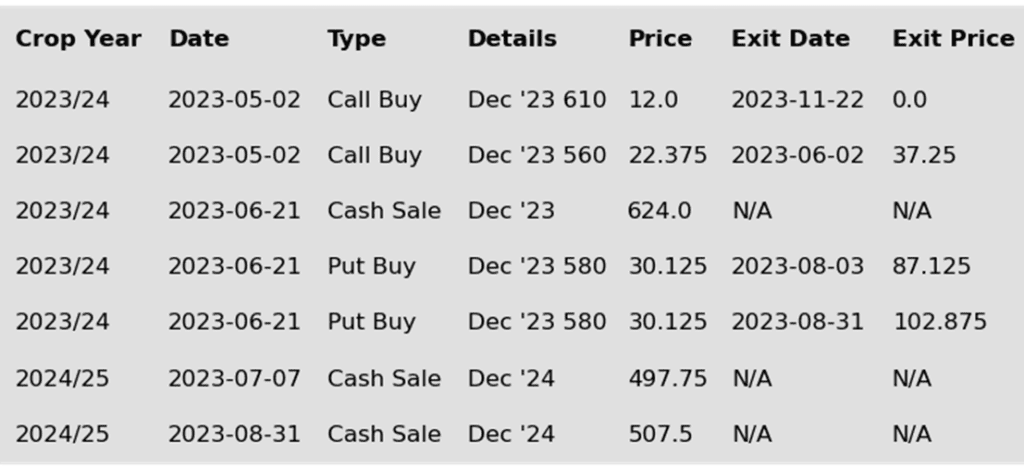

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

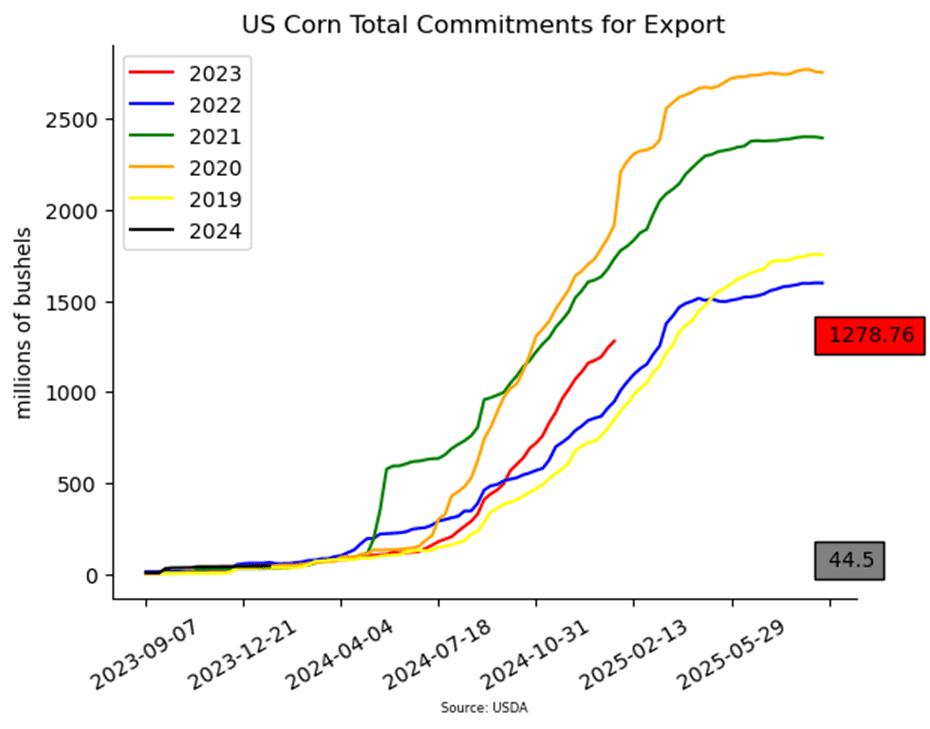

- Weekly corn export sales were within expectations at 954,800 MT (37.6 mb) for the 2023-24 marketing year. This is the key export window for US corn exports over the next couple months, and the market is looking for sales numbers to grow. Current total sales commitments are up 29% over last year.

- China stays absent from the US corn export market, but Mexico has been buying corn at a record pace. As of January 18th, Mexico has bought 15.3 MMT (602 mb), well above previous high from 2022. Mexico is responsible for 47% of all US corn sales for the current 2023/24 marketing year.

- Weather forecasts in Argentina have turned hotter and drier going into February. The change in weather has been enough to trigger some short covering, supporting the market this week. Argentina is forecasted to produce a record corn crop this season after two years of drought.

- Hedge funds were holding a large short position in the corn market, over 260,000 net short contracts as of last week Tuesday. Funds have likely begun working out of some of these short positions with the strength in the market this week. The corn market in general looks over-supplied and lacking true bullish news.

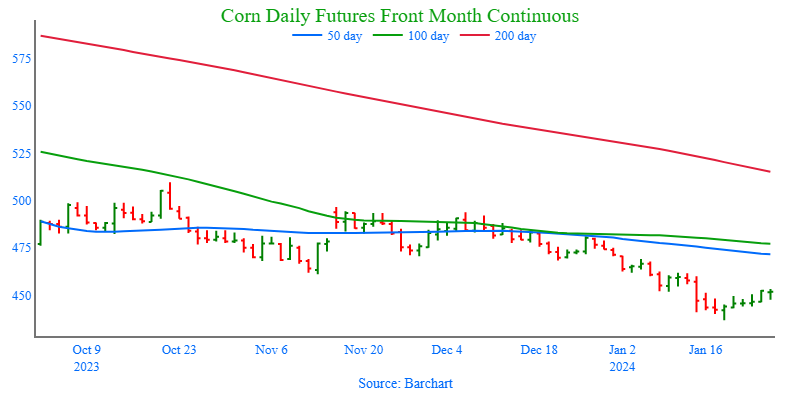

Above: Since posting a low on January 18, March corn has traded higher from being oversold and appears on track to test nearby resistance around 460. If prices turn back lower, initial support on the downside remains near the recent low of 436 ¾, with the next major support level around 415.

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

- No new action is recommended for 2023 soybeans. Front month soybeans recent downside breakout of the 1290 – 1400 range indicates that there is risk that prices may continue to retreat toward 1180, as forecasts for improved South American weather lessen the potential for the record large global carryout to be reduced. Given the potential of a downside breakout, Grain Market Insider recently recommended adding to sales as the current price level is still historically good. It’s been disappointing how the market has been unable to push higher despite the South American production concerns. Because of that, Grain Market Insider’s concern is that, if the weather pattern doesn’t remain adverse, the path of least resistance could be lower. Grain Market Insider will continue to look at additional sales opportunities, as well as potential re-ownership strategies.

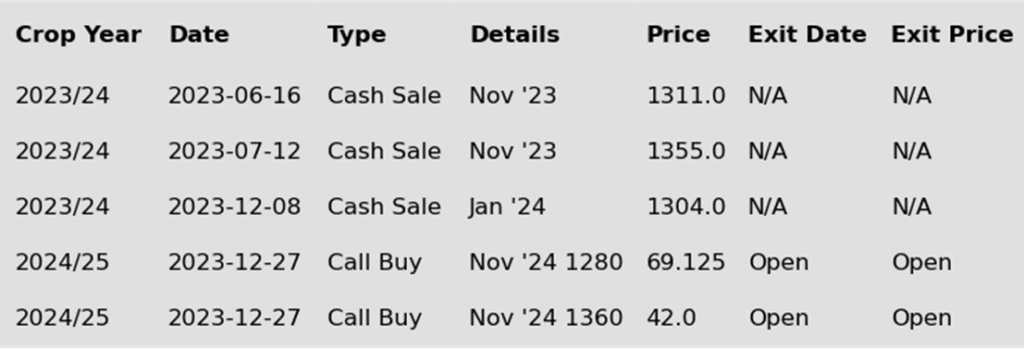

- No new action is recommended for the 2024 crop. The Nov ’24 contract recently broke through the downside of the 1233 – 1320 range that has been in place since the end of July. With this downside breakout, and considering the bullish influence of adverse South American weather, which appears to be improving, Nov ’24 runs the risk of retreating towards 1150 unless another bullish catalyst enters the market. If prices find support and turn back higher, Grain Market Insider recently recommended buying Nov ’24 1280 and 1360 calls to give you confidence to make sales against anticipated 2024 production and to protect any sales in an extended rally. Grain Market Insider will also continue to watch for any sales opportunities.

- No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day significantly lower as a result of softer than expected weekly export sales, scattered showers in Brazil, and a Brazilian cash market that could be pointing to a larger crop than many analysts have been predicting.

- To start the day, soybean meal was higher and had been trending higher since last Thursday, but reversed lower after export sales were released. Soybean oil was lower as well despite a very strong palm oil market, but it did not help that palm oil was not trading today due to a holiday. With the value of soy products falling, crush margins are narrowing which could slow the record crush numbers that have been recently reported.

- In Brazil, weather has improved, and even Mato Grosso and Parana are beginning to receive scattered showers again. There has been a lot of talk among analysts of a shrinking Brazilian soy crop, but recent rains and a steep decline in basis today as harvest ramps up may be indicating that total production will be closer to the USDA’s estimate of 157 mmt than the lower estimates by analysts of 145 mmt or below.

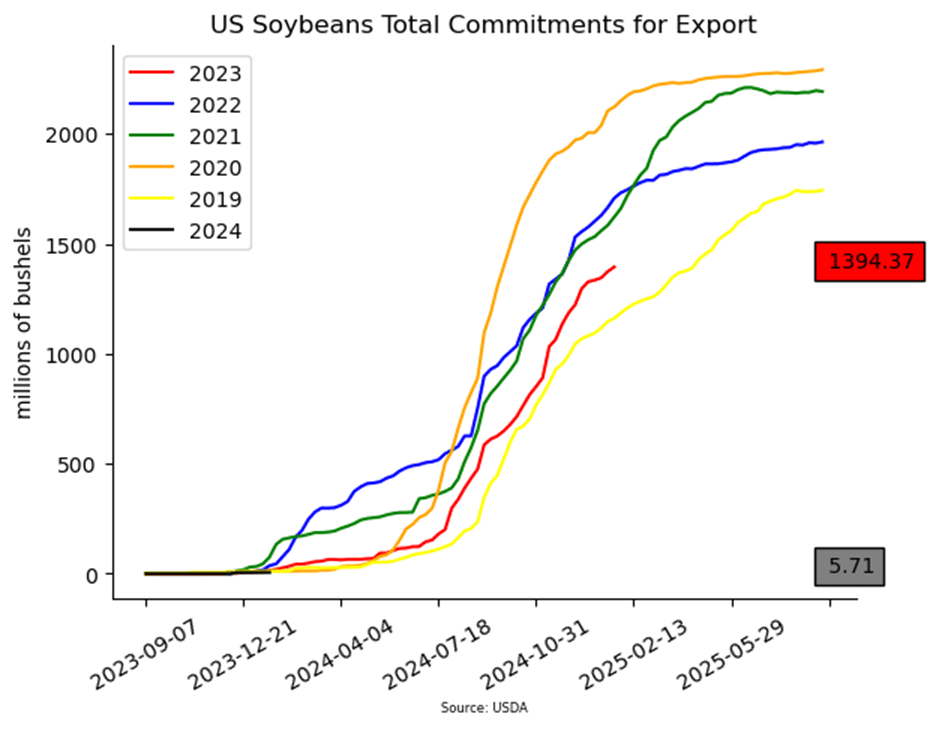

- Export sales for soybeans were on the lower end of expectations with an increase of 20.6 mb for 23/24. This was down 28% from the previous week but up 6% from the prior 4-week average. Last week’s export shipments for soybeans of 41.1 mb were well above the 23.9 mb needed each week to achieve the USDA’s estimates. Primary destinations were to the Philippines, Japan, and South Korea.

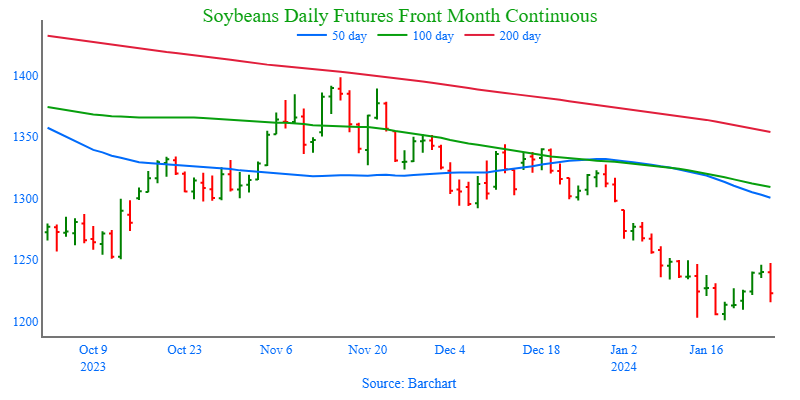

Above: After posting the 1201 low, short covering from oversold conditions has enabled March soybeans to rebound. Overhead resistance remains in the 1250 area and again near 1290. If prices turn lower, support comes in around 1200 and then near the November ’21 low of 1181.

Wheat

Market Notes: Wheat

- After trading both sides of neutral, all three US wheats closed higher. This marks six higher closes out of the past seven sessions for March Chicago wheat. The exception was on Tuesday when prices settled unchanged. This continued recovery for wheat comes despite today’s rebound in the US dollar, as well as lower corn and sharply soybean futures.

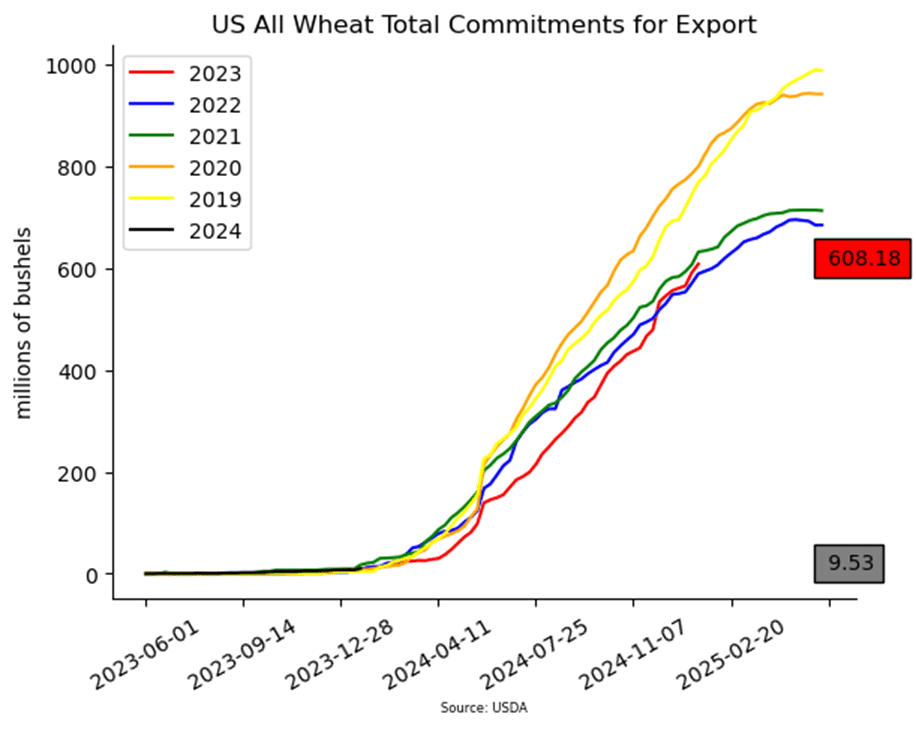

- The USDA reported an increase of 16.6 mb of wheat export sales for 23/24 as well as an increase of 2.2 mb for 24/25. Shipments last week at 11.9 mb were below the 17.0 mb pace needed per week to reach the USDA’s goal of 725 mb. However, commitments are now at 608 mb which is slightly above the USDA’s pace.

- One of the factors that may have supported the wheat market today is talk that drought in northern Africa could expand, requiring them to import more wheat. A neutral to mostly higher close for Paris milling wheat futures also offered some support.

- SovEcon has estimated the Russian 2024 wheat crop at 92.2 mmt. For reference the 2023 crop totaled 92.8 mmt. Though this is a decline, it is only a 0.6% drop and is unlikely to have a major impact if true. In addition, SovEcon’s projection for 2024 was actually an increase from their previous estimate by 0.9 mmt. For the time being, Russia is likely to remain aggressive on exports, which may limit upside potential for futures.

Action Plan: Chicago Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Chicago Wheat Action Plan Summary

- No new action is currently recommended for 2023 Chicago wheat. The wheat market has continued to be dominated by lower world export prices that have stymied US export sales and depressed US prices. In early December, Grain Market Insider recommended taking advantage and making a sale on a short covering rally which was sparked by several Chinese purchases of US wheat. Since then, China has been silent in the US wheat export market, and prices remain somewhat elevated. Any remaining 2023 soft red winter wheat should be getting priced into market strength with the goal of having zero bushels unpriced by the end of January. Grain Market Insider won’t have any “New Alerts” for 2023 Chicago wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Chicago wheat. Since early December, the July ’24 contract has traded mostly sideways to slightly lower after its brief short covering runup on Chinese buying. Although China has since been absent from the US wheat export market, managed funds continue to hold a sizeable, short position that could trigger another short covering rally if a bullish impetus enters the market. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for further price erosion. Back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset much of the original cost and move toward a net neutral cost for the remaining position.

- No action is currently recommended for 2025 Chicago Wheat. Since early September, the July ’25 contract has been rangebound, largely between 650 on the bottom and 675 on the top. Grain Market Insider’s strategy for the 2025 crop year up to this point has been to sit tight. Though if prices break out of the topside of this range toward the 690 – 705 area, we will consider taking advantage of the rally and making sales recommendations.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: Since uncovering support around 573, March Chicago wheat has rallied through both the 100 and 50-day moving averages and is on track to test the 620 – 625 resistance area. If prices turn back lower, initial support remains near 573, with the next major support level around 556.

Action Plan: KC Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

KC Wheat Action Plan Summary

- No new action is recommended for 2023 KC wheat crop. After posting an 80-cent rally in late November and early December, front month KC wheat has languished and drifted lower while retracing about 50% of the upward move. Managed funds continue to carry a significant short position, and even though bullish headwinds like weak US demand and low world wheat prices remain, this could fuel a return to higher prices as winter weather risks add volatility to the market. Grain Market Insider’s strategy is to look for price appreciation this winter, as weather becomes a more prominent market mover, and may consider suggesting additional sales if prices become over-extended.

- No new action is recommended for 2024 KC wheat. At the end of August, the July ’24 contract broke out of roughly a one-year trading range and stepped down to a 609 ¼ low in late November, largely driven by managed fund selling in the front month on weak US export demand and lower world wheat prices. Since then, the funds covered part of their large short position which also rallied prices in the July ’24 contract. While bearish headwinds remain, managed funds continue to hold a sizable, short position, and price seasonals remain positive for adding weather risk premium. These are two factors that could fuel additional short covering and rally prices in the months ahead. Back in August, Grain Market Insider recommended buying Jul’24 KC wheat 660 puts to protect the downside following the range breakout. As the market recently got further extended into oversold territory and the July contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. Moving forward, Grain Market Insider is prepared to recommend exiting the last 25% on any further supportive market developments.

- No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

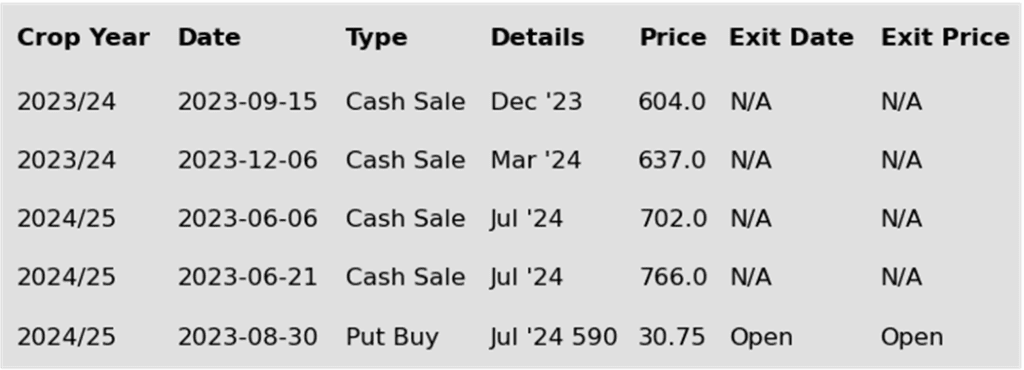

To date, Grain Market Insider has issued the following KC recommendations:

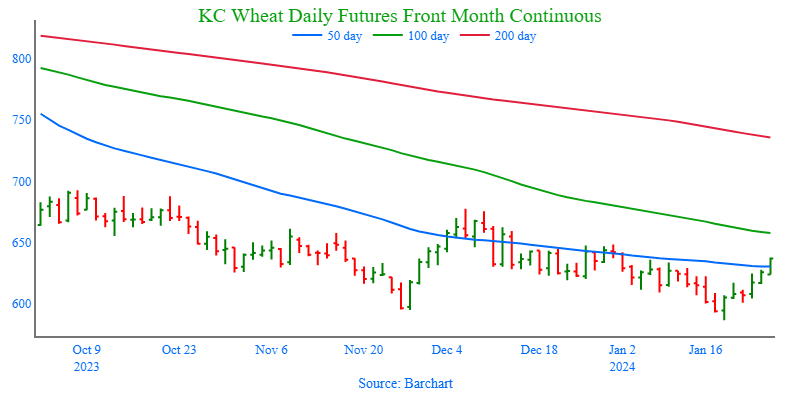

Above: With little bullish news in the market, KC wheat has been drifting sideways to lower since the middle of December with the 50-day moving average acting as nearby resistance. If bullish news does enter the scene to move prices higher, major resistance beyond the 50-day moving average lies between 650 and 678. Otherwise, major support below the market remains between 595 and 575.

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

- No new action is currently recommended for the 2023 New Crop. For much of the second half of last year, driven mostly by fund selling and slow US export demand, front month Minneapolis wheat slowly stair-stepped lower until hitting the November low. During this time, managed funds also established a record net short position. Since then, with the market mostly sideways, the November low of 697 ½ has held, and prices have pierced the 50-day moving average just once. Although bearish headwinds remain, the large fund net short position could fuel a short-covering rally if a bullish catalyst enters the scene to move prices to close above the 50-day moving average. Back in June, Grain Market Insider made a sales recommendation during the July rally near 820, and with that sale in place, Grain Market Insider’s strategy is to look for price appreciation this winter with an eye on considering additional sales around 725 – 775, and again north of 800.

- No new action is recommended for 2024 KC wheat. In early December the July ’24 contract posted a 70-cent rally mostly on short covering activity in the front month contracts. Since then, July ’24 has drifted lower as growing conditions have seen improvement. Still, much of the growing season remains, and managed funds continue to carry a significant short position in old crop. Even though bullish headwinds remain, this could fuel another short covering rally if any production concerns come to the forefront. Back in August, Grain Market Insider recommended buying Jul ’24 KC wheat 660 puts to protect the downside. As the market got further extended into oversold territory and July ’24 showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. Grain Market Insider remains prepared to recommend exiting the last 25% on any further supportive market developments.

- No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

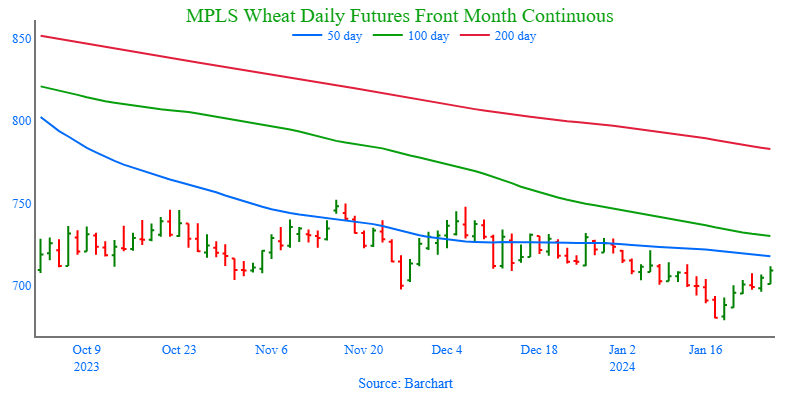

Above: Since the March contract closed below 700 support in early January, the 700 area has acted as resistance for the recent rally. If prices close above that area, the next areas of resistance may come in between 721 and 734. Otherwise, below the market support remains near 669.

Other Charts / Weather