1-22 End of Day: Markets Settle Firm to Higher on Little Fresh News

All prices as of 2:00 pm Central Time

| Corn | ||

| MAR ’24 | 445.75 | 0.25 |

| JUL ’24 | 464.75 | 0.5 |

| DEC ’24 | 476.25 | 0.25 |

| Soybeans | ||

| MAR ’24 | 1224.25 | 11 |

| JUL ’24 | 1241.25 | 9.25 |

| NOV ’24 | 1197.5 | 6.25 |

| Chicago Wheat | ||

| MAR ’24 | 596.5 | 3.25 |

| JUL ’24 | 612 | 2.25 |

| JUL ’25 | 654.25 | 2.5 |

| K.C. Wheat | ||

| MAR ’24 | 607 | -1 |

| JUL ’24 | 614.5 | 0.5 |

| JUL ’25 | 652.75 | 0.75 |

| Mpls Wheat | ||

| MAR ’24 | 700.5 | 5 |

| JUL ’24 | 709.75 | 0.75 |

| SEP ’24 | 717.5 | 0 |

| S&P 500 | ||

| MAR ’24 | 4879.25 | 9.75 |

| Crude Oil | ||

| MAR ’24 | 74.71 | 1.46 |

| Gold | ||

| APR ’24 | 2041.3 | -7.3 |

Grain Market Highlights

- Two-sided choppy traded dominated the corn market in a tight 4-cent range with little fresh news to move prices significantly in either direction. Support spilled over from soybeans to help corn prices settle fractionally in the green, as prices continue to consolidate.

- Solid weekly export inspections and a strong soybean oil market that posted a bullish reversal from Friday’s weakness lent support to soybeans, which closed higher for the third day in a row after testing 1200 support in the March contract.

- Despite export inspections that came in on the low end of expectations, and weakness in Matif wheat futures. The wheat complex ended the day mostly firm but mixed with Chicago and Minneapolis mostly higher, while nearby KC settled weak relative to the deferred.

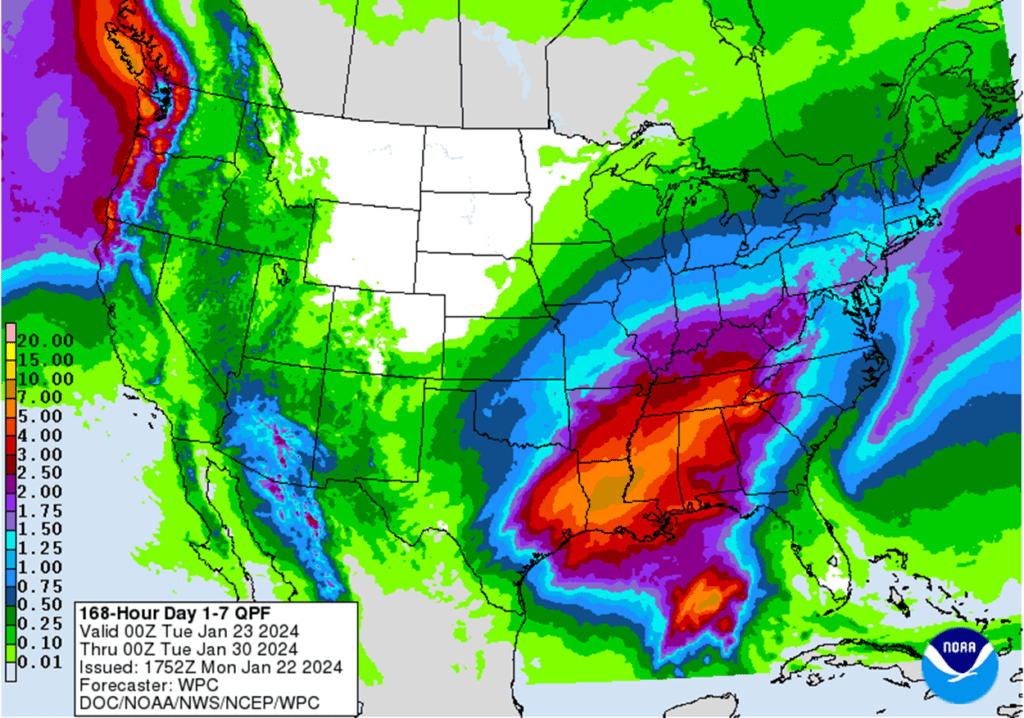

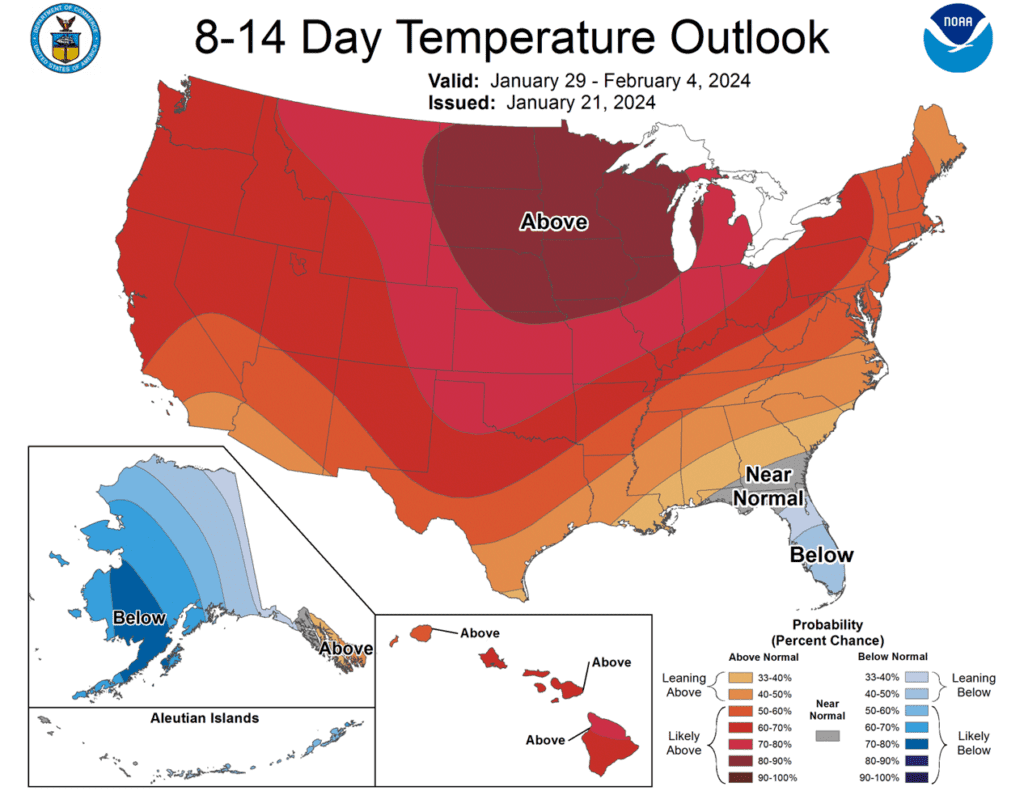

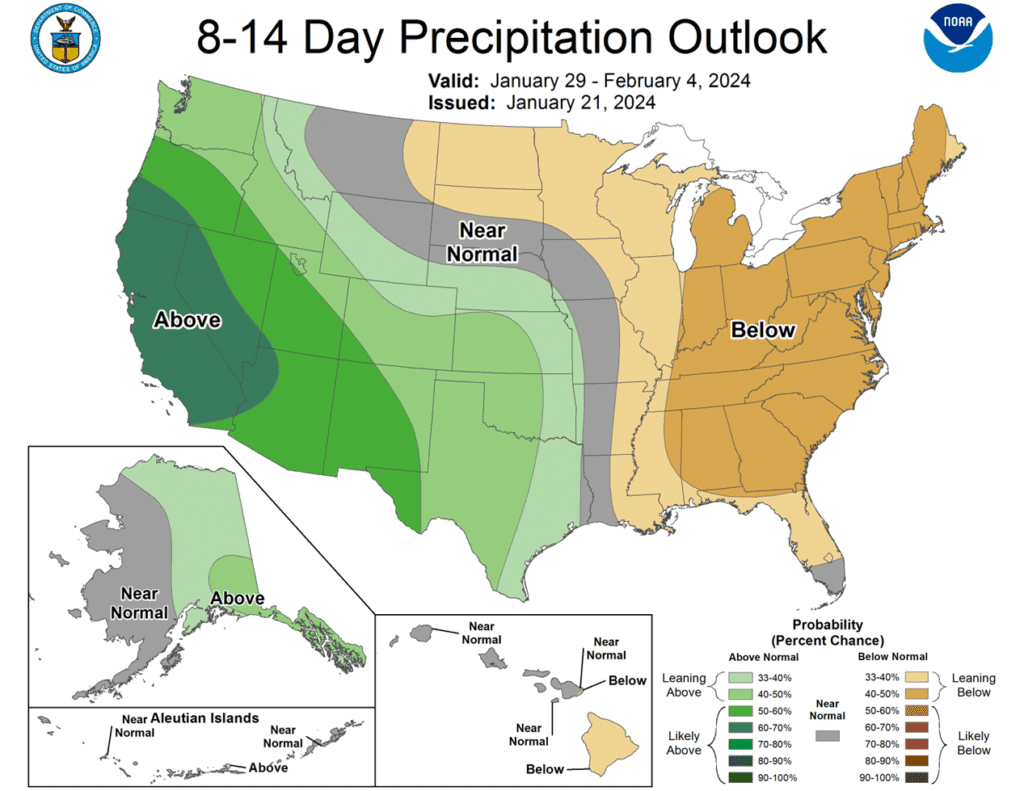

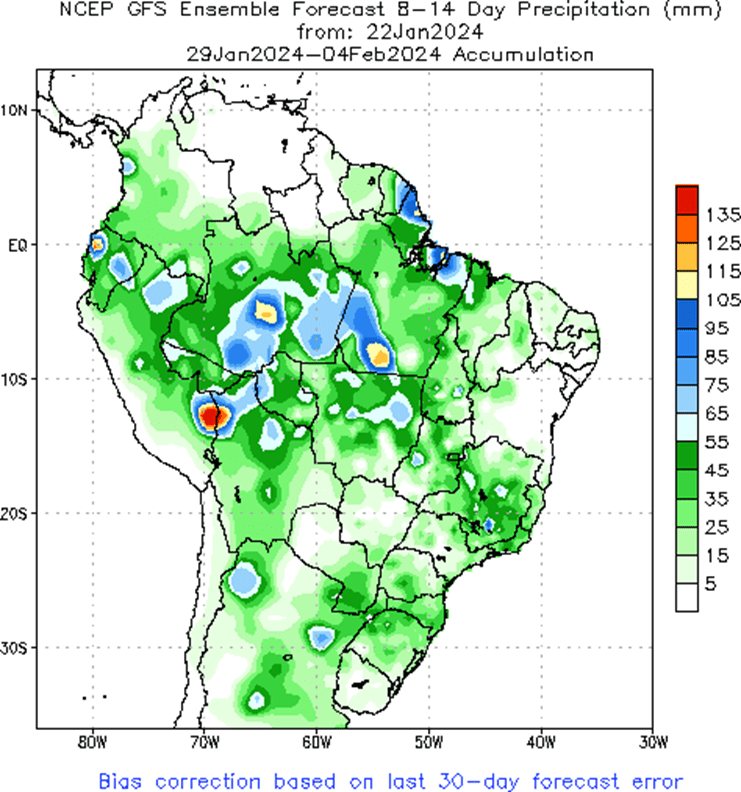

- To see the updated US 7-day precipitation forecast, 8-14 day temperature and precipitation outlooks as well as the Brazil 2 week forecast total precipitation courtesy of the National Weather Service, Climate Prediction Center, scroll down to the other Charts/Weather section.

Note – For the best viewing experience, some Grain Market Insider content is best viewed with your phone held horizontally.

Corn

Action Plan: Corn

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Corn Action Plan Summary

- No new action is recommended for 2023 corn. Front month corn has languished in a sideways to lower trend since printing a high in October, with a general lack of bullish news and an estimated US carryout over 2.1 billion bushels. The failure of the USDA’s January report to provide the bullish news necessary to turn prices higher is disappointing and the market remains at risk of remaining in the same pattern. With that being said, the market does show signs of being oversold, and managed funds hold a sizable net short position, which could trigger a short covering rally if a bullish catalyst enters the scene. For now, Grain Market Insider will continue to hold tight on any further sales recommendations for the next few weeks with the objective of seeking out better pricing opportunities. If the market has not turned around by then, Grain Market Insider may sit tight on the next sales recommendations until spring.

- No new action is recommended for 2024 corn. Following the January USDA Supply and Demand update, Dec ’24 broke through the bottom end of the 485 ¾ to 602 range that had been in place since February ’22. While this is a disappointing development, bear spreading has allowed Dec ’24 to maintain more of its value versus old crop, as traders attempt to price in a larger 2023 carryout with more uncertainty remaining for the 2024 crop. Additionally, Dec ’24 does show signs of being oversold, which is supportive if a bullish catalyst enters the scene. Grain Market Insider continues to watch for signs of a change in the current trend to look at recommending making additional sales and buying Dec ’24 call options.

- No Action is currently recommended for 2025 corn. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be late winter or early spring of 2024 before Grain Market Insider starts considering the first sales targets.

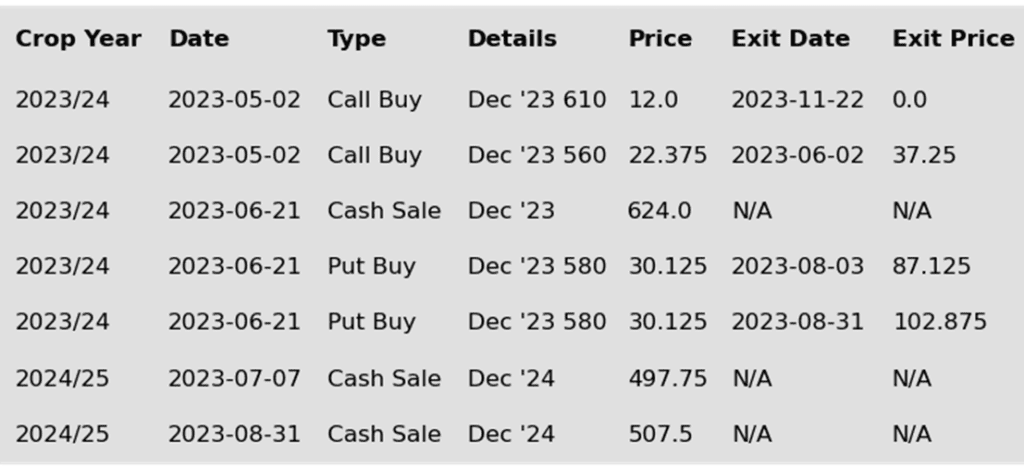

To date, Grain Market Insider has issued the following corn recommendations:

Market Notes: Corn

- Another quiet news day in the grain markets but buying strength in the soybean market did help pull corn futures slightly higher during the session. March corn gained ¼ cents on the day as prices have consolidated the past five sessions around the USDA report day low.

- Weekly corn export inspections were within expectations at 28.1 mb (713,000 mt). Total inspections for the marketing are now at 579 mb, up 28% from last year. Corn inspections are running ahead of the USDA projections.

- South American weather is looking to trend a little drier in southern areas, but overall weather patterns are staying favorable for crops.

- Brazil’s soybean harvest is progressing ahead of average pace. Brazil’s soybean crop is estimated at 6% harvested, up from 1.8% last year. The key crop production state of Mato Grasso is nearly 13% complete. The early soybean harvest is allowing Brazil producers to begin planting of the key second crop corn in an earlier time window.

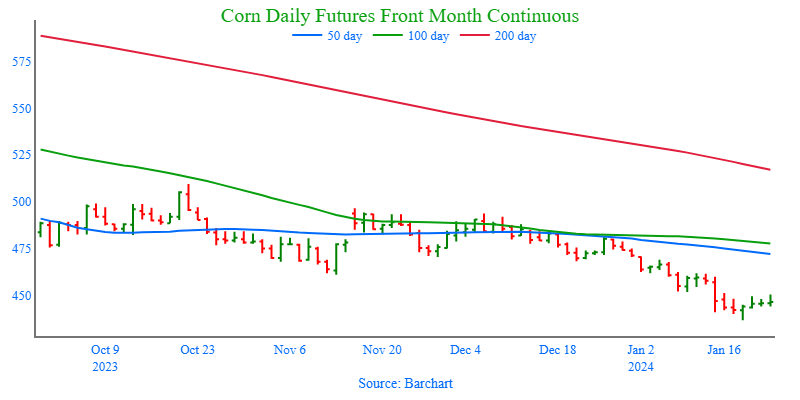

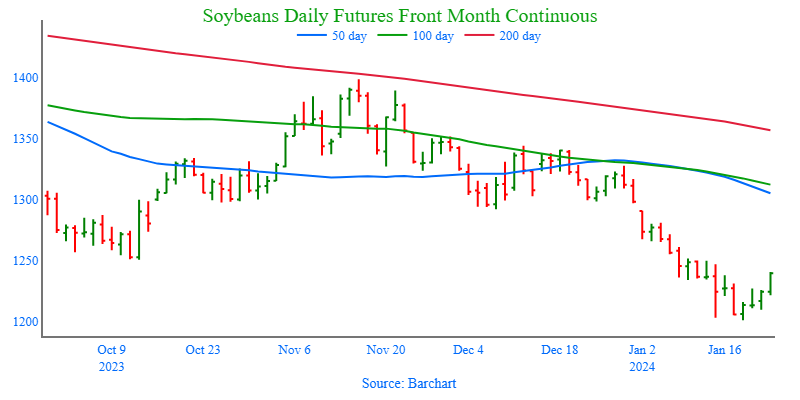

Above: Earlier in January, March corn broke through 460 support, which is now nearby resistance, and retreated toward nearby support around 440. The market shows signs of being oversold, which can be supportive if bullish information enters the market. If prices break below 440, the next major support level comes in near 415. Overhead, if prices rally above 460, additional resistance may enter in between 470-480.

Soybeans

Action Plan: Soybeans

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Soybeans Action Plan Summary

- No new action is recommended for 2023 soybeans. Front month soybeans recent downside breakout of the 1290 – 1400 range indicates that there is risk that prices may continue to retreat toward 1180, as forecasts for improved South American weather lessen the potential for the record large global carryout to be reduced. Given the potential of a downside breakout, Grain Market Insider recently recommended adding to sales as the current price level is still historically good. It’s been disappointing how the market has been unable to push higher despite the South American production concerns. Because of that, Grain Market Insider’s concern is that, if the weather pattern doesn’t remain adverse, the path of least resistance could be lower. Grain Market Insider will continue to look at additional sales opportunities, as well as potential re-ownership strategies.

- No new action is recommended for the 2024 crop. The Nov ’24 contract recently broke through the downside of the 1233 – 1320 range that has been in place since the end of July. With this downside breakout, and considering the bullish influence of adverse South American weather, which appears to be improving, Nov ’24 runs the risk of retreating towards 1150 unless another bullish catalyst enters the market. If prices find support and turn back higher, Grain Market Insider recently recommended buying Nov ’24 1280 and 1360 calls to give you confidence to make sales against anticipated 2024 production and to protect any sales in an extended rally. Grain Market Insider will also continue to watch for any sales opportunities.

- No Action is currently recommended for 2025 Soybeans. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now, and it may be some time before conditions are conducive to consider making any recommendations. Be patient as we monitor the markets for signs of improvement.

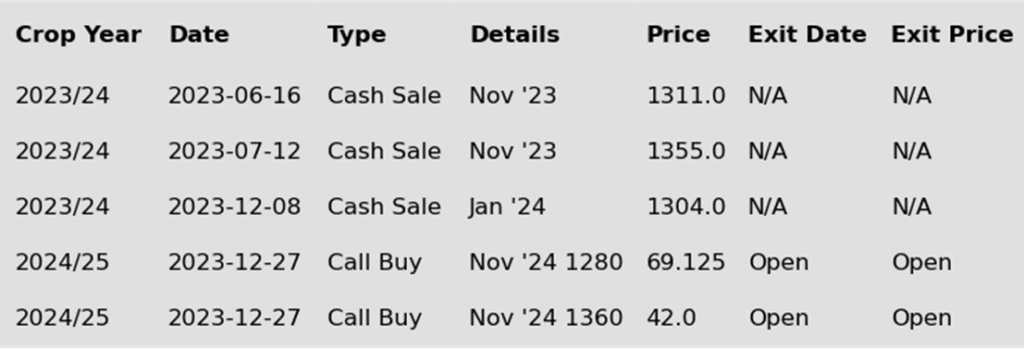

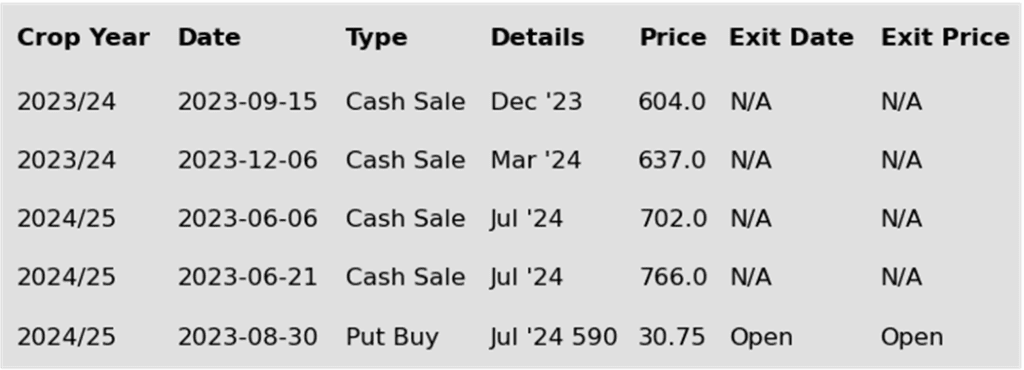

To date, Grain Market Insider has issued the following soybean recommendations:

Market Notes: Soybeans

- Soybeans ended the day higher with the March contract now 23 cents off its low from last Thursday. Soybean meal continued its trek lower today, while soybean oil was supported from higher crude oil and palm oil.

- Today’s export inspections were decent with 42.7 mb inspected for the week ending January 18. Total inspections are now at 983 mb for 23/24 which is down 22% from the previous year. No flash sales were reported today, but there was a large sale to China last Friday.

- South American weather is forecast to be slightly drier over the next 10 days with the decline in precipitation mainly in Argentina and Brazil’s Mato Grosso do Sul. The majority of Brazil is expected to continue getting scattered showers as harvest begins.

- Brazil is currently 6% complete with harvest which is up 2% from last week, and early yields have been poor, but the majority of this early harvested crop is the part that was under the most stress from dry and hot weather. More accurate yield estimates will not be available until harvest is further along.

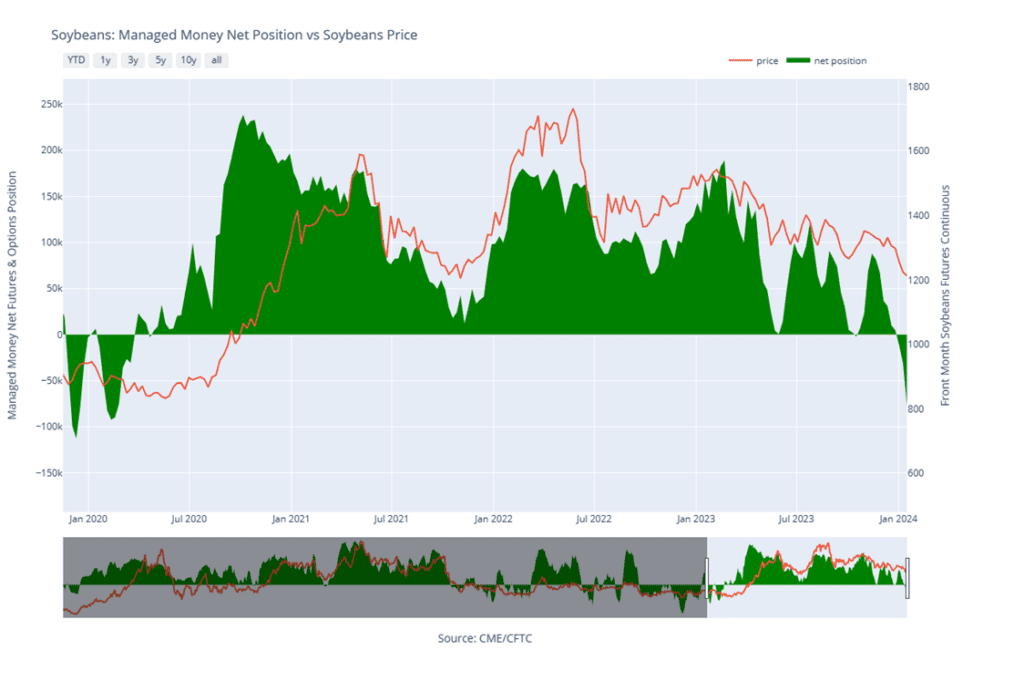

Above: Soybeans have steadily retreated after leaving a 6-cent gap between 1290 ¾ and 1296 ¾. The market is showing signs of being extremely oversold, which can be supportive if bullish information enters the market to turn prices around. If prices do turn back higher, resistance rests around the price gap and again near the 50-day moving average. Otherwise, the next major support level comes in near the November ’21 low of 1181.

Wheat

Market Notes: Wheat

- Despite a lack of fresh news, wheat was able to close mostly higher today following a day of two sided trade. This was also in the face of a mostly lower close for Matif wheat futures. With US futures at or very near oversold levels technically, this may indicate that the market has found a near term bottom. This marks the fourth higher session for March Chicago wheat.

- Weekly wheat inspections totaling 11.6 mb bring the 23/24 total inspections to 394 mb, which is down 16% from last year. Inspections are also running behind the pace needed to meet the USDA’s 725 mb goal for 23/24 wheat exports.

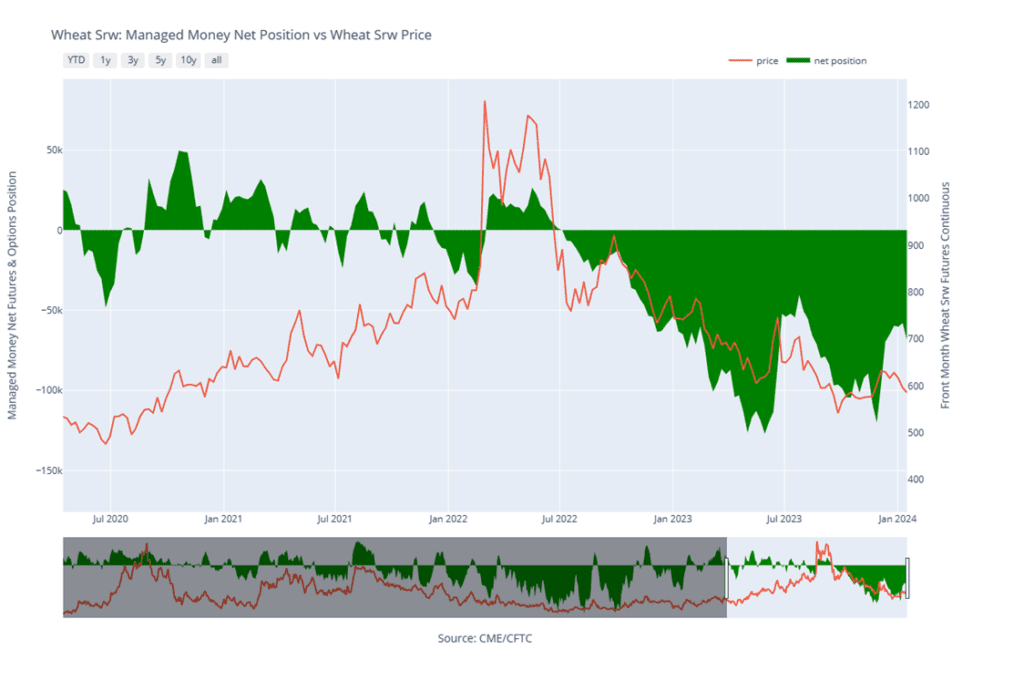

- According to the CFTC, as of January 16, managed funds were short 68,575 contracts of Chicago wheat. That is an addition of 10,587 contracts from the previous week, representing an 18.3% increase to their short position.

- Due to the ongoing issues in the Red Sea, more and more European vessels transporting wheat are being re-routed to avoid using the Suez Canal. According to the World Trade Organization, shipments from Russia, Ukraine, and the EU using alternative routes have increased 42% by mid-January. This compares to just 8% in December.

Action Plan: Chicago Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Chicago Wheat Action Plan Summary

- No new action is currently recommended for 2023 Chicago wheat. The wheat market has continued to be dominated by lower world export prices that have stymied US export sales and depressed US prices. In early December, Grain Market Insider recommended taking advantage and making a sale on a short covering rally which was sparked by several Chinese purchases of US wheat. Since then, China has been silent in the US wheat export market, and prices remain somewhat elevated. Any remaining 2023 soft red winter wheat should be getting priced into market strength with the goal of having zero bushels unpriced by the end of January. Grain Market Insider won’t have any “New Alerts” for 2023 Chicago wheat – either Cash, Calls, or Puts, as we have moved focus onto 2024 and 2025 Crop Year Opportunities.

- No new action is recommended for 2024 Chicago wheat. Since early December, the July ’24 contract has traded mostly sideways to slightly lower after its brief short covering runup on Chinese buying. Although China has since been absent from the US wheat export market, managed funds continue to hold a sizeable, short position that could trigger another short covering rally if a bullish impetus enters the market. At the end of August, Grain Market Insider recommended purchasing July 590 puts to prepare for further price erosion. Back in June, Grain Market Insider recommended two separate sales that averaged about 720 to take advantage of the brief upswing. If the market receives the needed stimulus to move prices back toward this summer’s highs, Grain Market Insider is prepared to recommend adding to current sales levels and possibly even purchasing call options to protect those sales. Otherwise, the current recommended put position will add a layer of protection if prices erode further, and Grain Market Insider will be prepared to recommend covering some of those puts to offset much of the original cost and move toward a net neutral cost for the remaining position.

- No action is currently recommended for 2025 Chicago Wheat. Since early September, the July ’25 contract has been rangebound, largely between 650 on the bottom and 675 on the top. Grain Market Insider’s strategy for the 2025 crop year up to this point has been to sit tight. Though if prices break out of the topside of this range toward the 690 – 705 area, we will consider taking advantage of the rally and making sales recommendations.

To date, Grain Market Insider has issued the following Chicago wheat recommendations:

Above: March Chicago wheat has been consolidating after uncovering initial support just below the market around 573. If that holds, the market may test resistance near the 50-day moving average, and again between 620 and 625, while heavy resistance remains near 650. If 573 does not hold, the market may run the risk of retreating and testing the next level of major support near 556.

Action Plan: KC Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

KC Wheat Action Plan Summary

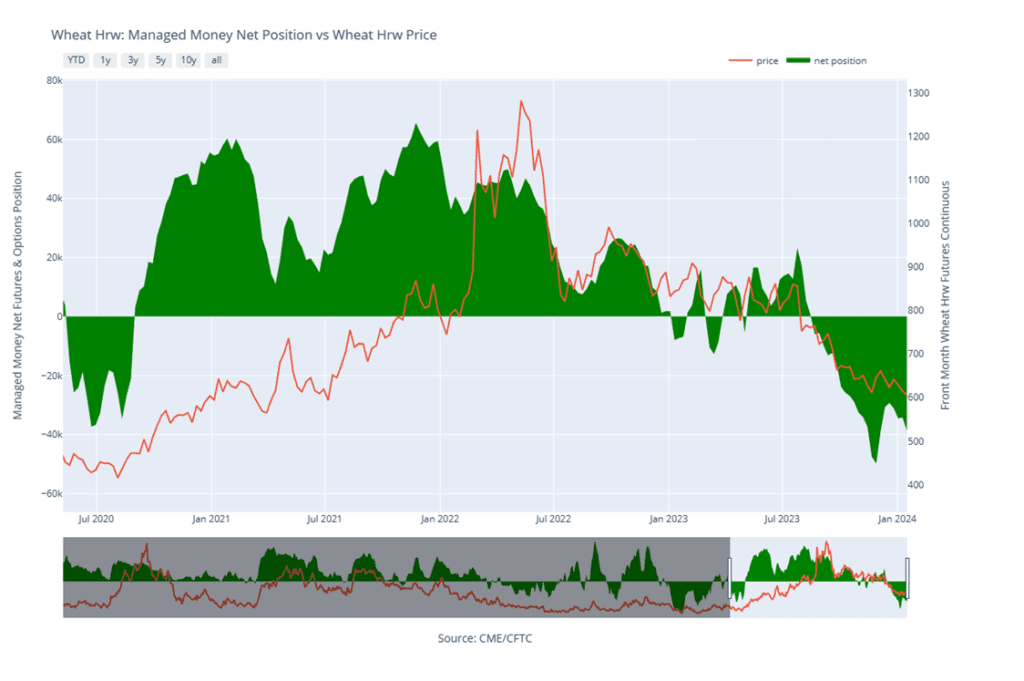

- No new action is recommended for 2023 KC wheat crop. After posting an 80-cent rally in late November and early December, front month KC wheat has languished and drifted lower while retracing about 50% of the upward move. Managed funds continue to carry a significant short position, and even though bullish headwinds like weak US demand and low world wheat prices remain, this could fuel a return to higher prices as winter weather risks add volatility to the market. Grain Market Insider’s strategy is to look for price appreciation this winter, as weather becomes a more prominent market mover, and may consider suggesting additional sales if prices become over-extended.

- No new action is recommended for 2024 KC wheat. At the end of August, the July ’24 contract broke out of roughly a one-year trading range and stepped down to a 609 ¼ low in late November, largely driven by managed fund selling in the front month on weak US export demand and lower world wheat prices. Since then, the funds covered part of their large short position which also rallied prices in the July ’24 contract. While bearish headwinds remain, managed funds continue to hold a sizable, short position, and price seasonals remain positive for adding weather risk premium. These are two factors that could fuel additional short covering and rally prices in the months ahead. Back in August, Grain Market Insider recommended buying Jul’24 KC wheat 660 puts to protect the downside following the range breakout. As the market recently got further extended into oversold territory and the July contract showed signs of support near 630, Grain Market Insider recommended exiting 75% of the originally recommended position. Moving forward, Grain Market Insider is prepared to recommend exiting the last 25% on any further supportive market developments.

- No action is currently recommended for 2025 KC Wheat. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted next fall. It will probably be mid-winter before Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following KC recommendations:

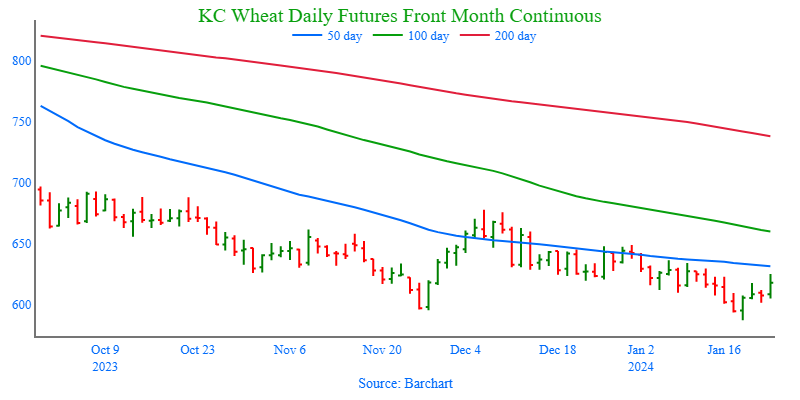

Above: With little bullish news in the market, KC wheat has been drifting sideways to lower since the middle of December with the 50-day moving average (632) acting as nearby resistance. If bullish news does enter the scene to move prices higher, major resistance beyond 632 lies between 650 and 678. Otherwise, major support below the market remains between 595 and 575.

Action Plan: Mpls Wheat

Calls

2023

No New Action

2024

No New Action

2025

No New Action

Cash

2023

No New Action

2024

No New Action

2025

No New Action

Puts

2023

No New Action

2024

No New Action

2025

No New Action

Mpls Wheat Action Plan Summary

- No new action is currently recommended for the 2023 New Crop. For much of the second half of last year, driven mostly by fund selling and slow US export demand, front month Minneapolis wheat slowly stair-stepped lower until hitting the November low. During this time, managed funds also established a record net short position. Since then, with the market mostly sideways, the November low of 697 ½ has held, and prices have pierced the 50-day moving average just once. Although bearish headwinds remain, the large fund net short position could fuel a short-covering rally if a bullish catalyst enters the scene to move prices to close above the 50-day moving average. Back in June, Grain Market Insider made a sales recommendation during the July rally near 820, and with that sale in place, Grain Market Insider’s strategy is to look for price appreciation this winter with an eye on considering additional sales around 725 – 775, and again north of 800.

- No new action is recommended for 2024 Minneapolis wheat. After trading to a peak of 871 ¾ last August, the Sept ’24 gradually retreated to a low in November in concert with the front month as managed funds built a record large net short position mostly on weak US export demand. And while Sept ’24 has failed to close above the 50-day moving average since late August, the 726 ¼ November low remains intact. Although bearish headwinds remain, the large fund net short position could fuel a short-covering rally if prices move higher and close above the 50-day moving average. Back in August, Grain Market Insider recommended buying July ’24 KC wheat 660 puts to protect the downside following a 1-year range breakout in KC wheat, and in November recommended exiting 75% of the originally recommended position as July ’24 KC wheat showed signs of support around 630. While in the same time frame, Grain Market Insider also recommended making an additional sale as the Sept ’24 Minneapolis contract broke long time 743 support. For now, Grain Market Insider remains prepared to recommend exiting the last 25% of the open puts on any further supportive market developments.

- No action is currently recommended for the 2025 Minneapolis wheat crop. Grain Market Insider isn’t considering any recommendations at this time for the 2025 crop that will be planted two springs from now. It will probably be mid-winter before Grain Market Insider starts considering the first sales targets.

To date, Grain Market Insider has issued the following Minneapolis wheat recommendations:

Above: The breach of 700 in the March contract could indicate further weakness with the next area of major support down near 669. The market does show signs of being oversold, which is supportive if the market turns back higher. Overhead initial resistance lies around 700 and then again between 721 and 734.

Other Charts / Weather